Tax Debt by Amount

I Owe the IRS $30,000: What Are My Options in 2026?

The short answer: if you owe the IRS $30,000, you're under the $50,000 ceiling for a self-service payment plan of up to 72 months — roughly $417 a month at the baseline — but above the $25,000 line where the IRS requires direct debit. If that payment genuinely doesn't fit your budget, hardship status and settlement exist, both means-tested.

The divorce is final, the accounts are split, and somehow a five-figure tax bill landed on your side of the ledger — a balance built during a marriage that no longer exists. Here's the part that matters: $30,000 sits in one of the most fixable bands of IRS debt there is. You can usually resolve it online, this week, without ever speaking to a collector — if you move before the notice stream escalates.

⏱ The real clock: there's no single deadline printed on a $30,000 balance — but the meter runs every month. The failure-to-pay penalty adds 0.5% of the unpaid tax monthly, and interest compounds daily on top. On $30,000, doing nothing costs roughly $150 a month in penalty alone, before interest.

How a $30,000 IRS balance happens

A $30,000 IRS debt is almost never one bad decision — it's one hard year plus compounding. The most common paths we see at this amount: a divorce-year return where withholding was set for two incomes and life changed mid-year; a first full year of 1099 income with no estimated payments; a retirement withdrawal taken to cover legal fees or a buyout; or a CP2000 adjustment from income a spouse handled.

Whatever started it, the balance you see today usually isn't the tax you originally owed. Penalties and interest typically account for a meaningful slice of any balance that's more than a year old — which matters, because penalties can sometimes be removed even when the tax can't. More on that in the options below.

Recently divorced? Sort out who actually owes it first

If the $30,000 comes from a jointly filed return, the IRS can collect all of it from either ex-spouse — regardless of what the divorce decree says. That's called joint and several liability, and it surprises almost everyone. The decree is a contract between you and your ex; it gives you the right to sue them in state court, but it's not a defense the IRS has to honor. Our guide to divorce and IRS debt: who pays walks through this in depth.

Two relief paths can genuinely reassign part of a joint debt, and both require you to apply:

- Innocent spouse relief (Form 8857) — applies when the debt came from your ex's errors or omissions on the return, like unreported income you didn't know about. See innocent spouse relief: how to qualify.

- Equitable relief — the one path that can apply when the return was accurate but the tax simply went unpaid (for example, your ex kept the money that was earmarked for the IRS). It's fact-intensive, but it exists precisely for divorce situations like this.

One honest caveat: if you both knew about the balance and it's simply unpaid, classic innocent spouse relief won't apply — only the equitable route might. Get this question answered before you sign up to pay the whole thing yourself.

What happens if you ignore a $30,000 IRS balance

An unpaid $30,000 balance moves through an automated notice sequence that ends in levy power — no human has to review your file for it to escalate. The stages run in this order, typically several weeks apart:

- CP14 — the first bill. You have about 21 days from the notice date (10 business days if the balance is $100,000 or more) before the sequence advances. No enforcement yet; this is the cheapest moment to act.

- CP501 / CP503 — reminders. Still just bills, but the balance is compounding monthly, and the IRS is now weighing a Notice of Federal Tax Lien — a public claim against everything you own, generally considered on balances over $10,000.

- CP504 — intent to levy your state refund. Under IRC §6331(d), the IRS can now seize your state tax refund. It is not the final notice, but it's the last inexpensive off-ramp.

- LT11 / Letter 1058 — final notice of intent to levy. This starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). After 30 days, wages and bank accounts are fair game.

- Enforcement. A bank levy freezes funds for 21 days before they're sent to the IRS; a wage levy is continuous until released. At $30,000, both are routine outcomes of silence — not extreme ones.

One 2026 reality worth knowing: the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder than ever — but the notice and levy systems are automated and never stopped. The machine escalates on schedule whether anyone answers the phone or not.

Staring at a $30,000 balance right now?

Every month you wait adds roughly $150 in penalties before interest even starts. An experienced tax professional will review your balance, your divorce-year liability questions, and your realistic options — free, confidential, no pressure.

Owe the IRS $30,000 and can't pay in full? Your real options

At $30,000, you're under the $50,000 online payment-plan ceiling but above the $25,000 line where the IRS requires direct debit for a streamlined agreement. That single fact shapes everything about this band — here's where $30,000 sits against its neighbors:

| Balance | What changes | Payment-plan path |

|---|---|---|

| Up to $10,000 | Simplest tier — lien rarely filed (see I owe the IRS $10,000) | Guaranteed installment agreement, any payment method |

| $10,001–$25,000 | Lien becomes a real consideration (see I owe the IRS $20,000) | Streamlined plan, any payment method |

| $25,001–$50,000 — you are here | Direct debit required for streamlined treatment; still no full financial disclosure | Streamlined plan, direct debit only, up to 72 months |

| $50,001–$100,000 | Financial disclosure (Form 433-F) typically enters the picture | Non-streamlined agreement, negotiated terms |

| Over $100,000 | Possible revenue-officer assignment, full asset review (see I owe the IRS $100,000+) | Full financials, managed collection |

Now the options themselves. (The general mechanics of each program live in our DIY hub, how to settle tax debt yourself — here's how each one plays at exactly $30,000.)

Short-term payment plan (up to 180 days)

No setup fee, no monthly commitment — you just pay in full within 180 days. On $30,000 that means finding roughly $5,000 a month, so this fits only if money is coming: a house-sale closing, a retirement distribution, a bonus. It stops the notice sequence while you wait for the funds.

Streamlined installment agreement (the main path at $30,000)

This is the workhorse. Because you're under $50,000, you can set up a plan of up to 72 months online without submitting a financial statement — but above $25,000, the IRS requires the payments come by direct debit. Two quiet advantages of that requirement: the failure-to-pay penalty drops to 0.25% per month while the agreement is in effect (half the default rate), and a direct-debit agreement set up before a lien is filed makes a lien far less likely. Setup fees are modest — lowest for online direct-debit applications, and waived or reimbursed if your income qualifies. Full details in our streamlined installment agreement guide, or jump straight to setting up an IRS payment plan online.

The catch: the plan defaults if you miss payments or rack up a new balance next April. If you're newly single and newly on one income, fix your withholding or estimated payments the same week you set up the plan.

Partial-pay installment agreement

If roughly $417 a month is genuinely out of reach, the IRS can accept a lower payment based on what your budget actually allows — with the balance expiring unpaid when the 10-year collection statute runs. This requires a Form 433-F financial disclosure, periodic re-reviews, and usually a lien filing. It's real, but it's a documented-hardship path, not a discount you ask for.

Currently Not Collectible status

If paying anything would leave you unable to cover necessary living expenses — common in the first year after a divorce, when one income is carrying two households' worth of obligations — collection can be paused entirely. The debt remains and grows, and any refunds get kept, but levies and garnishments stop. See Currently Not Collectible status for how the hardship math works.

Offer in Compromise: settling for less

An Offer in Compromise lets you settle for less than $30,000 — but only when the IRS's own math says $30,000 is uncollectible. The IRS calculates your Reasonable Collection Potential: the equity in what you own plus a multiple of your monthly disposable income. If that number is below $30,000, an offer near that number can succeed; if it's above, the offer fails no matter how well it's written. You can estimate your own offer with our Offer in Compromise Calculator before spending anything.

The honest numbers: the IRS accepted roughly 1 in 5 offers in FY2024. The application costs $205 plus 20% down on a lump-sum offer — both waived if your income falls at or below 250% of the federal poverty line — and if the IRS doesn't decide within two years, the offer is accepted automatically, with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count. Ignore any ad promising to settle for "pennies on the dollar"; acceptance is arithmetic, not negotiation, and a divorce that cut your income and assets can genuinely change that arithmetic in your favor.

Penalty relief: shrink the balance before you pay it

If a chunk of your $30,000 is penalties, first-time penalty abatement can remove them entirely when your prior three years are clean — one phone call or letter, no fee. And starting summer 2026, the IRS is replacing this with the Automatic Exemption from Penalty (AEP), which applies without a request. Interest on the tax itself almost never gets waived, but interest charged on an abated penalty comes off with it.

| Option | Upfront cost | Timeline & monthly reality |

|---|---|---|

| Short-term plan (180 days) | $0 setup | ~$5,000/month equivalent; interest and penalties accrue until paid |

| Streamlined direct-debit plan (72 mo.) | Modest setup fee (lowest online; low-income waiver) | ~$417/month baseline; penalty rate halves to 0.25%/month while active |

| Partial-pay installment agreement | Setup fee + Form 433-F disclosure | Payment set by budget; reviewed periodically; lien likely; balance can expire at the CSED |

| Currently Not Collectible | $0 (financial disclosure required) | Collection paused; debt keeps growing; refunds offset; status reviewed if income rises |

| Offer in Compromise | $205 + 20% down on lump-sum (waived for low-income) | Often the better part of a year to decide; auto-accepted if no decision in 2 years (with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count) |

| Penalty abatement (FTA / AEP) | $0 | Removes qualifying penalties and their interest; the underlying tax remains |

What $30,000 actually costs: a worked example

Say your divorce finalized last spring, and the final joint return showed $23,800 in tax due — money that was supposed to come from a house sale that netted less than planned. You filed on time (which was smart — it avoided the 5%-per-month filing penalty) but couldn't pay. Two years later, here's the hypothetical math:

- Failure-to-pay penalty: 0.5% × 24 months = 12% of $23,800 ≈ $2,856

- Interest, compounding daily on the growing balance at recent federal rates: roughly $3,300

- Total: about $30,000 — a quarter more than the original tax

Now the resolution math. On a 72-month direct-debit plan, the baseline is $30,000 ÷ 72 ≈ $417/month, with the penalty rate halved while the plan runs. Push the payment to $600/month and you're done in roughly four and a half years, saving a meaningful slice of interest. And if the prior three years were clean, first-time abatement could remove that ~$2,856 penalty (plus its interest) before you ever start paying — that's several months of payments erased with one request.

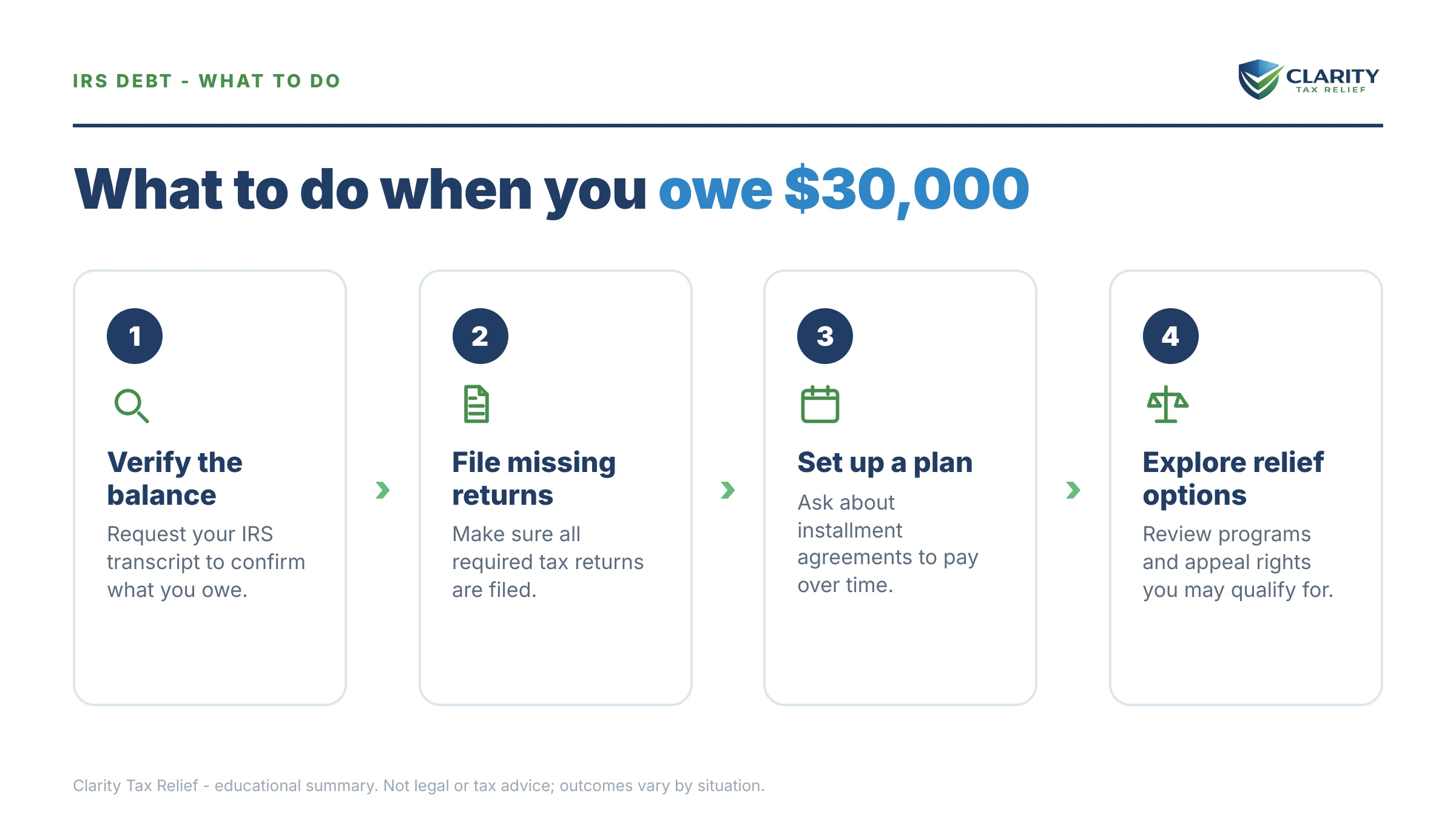

How to respond to a $30,000 IRS balance, step by step

- Confirm the exact balance. Log into your IRS online account and note the total and which tax years it covers — you'll want to resolve every year in one agreement, not one at a time.

- File any missing returns. The failure-to-file penalty runs 5% per month — ten times the failure-to-pay penalty — and the IRS won't approve any agreement until all required returns are in.

- Pick the option that fits your real budget. A direct-debit plan if you can sustain roughly $417 a month or more; hardship status or an Offer in Compromise if the numbers genuinely don't work.

- Set it up before a lien or final notice arrives. A direct-debit agreement started at the notice stage usually heads off both the lien and the levy track entirely.

- Request penalty relief. First-time abatement can strip the failure-to-pay penalty if your prior three years are clean — and it works alongside a payment plan, not instead of one.

Applications and current terms live on the IRS's own payment plans and installment agreements page, and settlement criteria on its Offer in Compromise page.

When you can handle $30,000 yourself — and when help changes the outcome

Plenty of people resolve a $30,000 balance without hiring anyone. You're a good DIY candidate if all of these are true: the balance is from one tax year you agree with, every return is filed, and roughly $417+ a month fits your budget. In that case, the online direct-debit application takes about 20 minutes, and paying a professional mostly buys convenience.

Experienced help tends to change the outcome — not just the stress level — in these situations: the debt is from a joint return and innocent spouse or equitable relief is on the table (the application is fact-intensive and one shot matters); you have multiple years or unfiled returns (the order you fix things changes what you pay); an LT11 or levy is already in motion; or you're a candidate for an Offer in Compromise, where the Reasonable Collection Potential math determines everything. If collection action is causing genuine hardship and you can't get traction, the independent Taxpayer Advocate Service is also a free resource worth knowing.

Terms you'll run into, decoded

- Joint and several liability — on a joint return, the IRS can collect 100% of the debt from either spouse, before or after divorce.

- Streamlined installment agreement — a payment plan approved without full financial disclosure; at $25,001–$50,000, it requires direct debit.

- DDIA (direct-debit installment agreement) — a plan paid automatically from your bank account; it halves the monthly penalty rate and reduces lien risk.

- Notice of Federal Tax Lien — a public claim against your property securing the debt; different from a levy, which actually takes money or assets.

- Reasonable Collection Potential (RCP) — the IRS's formula (asset equity plus future income) that decides whether a settlement offer can be accepted.

- CSED — the Collection Statute Expiration Date: generally 10 years from assessment, after which unpaid balances expire (see the 10-year collection statute), though certain events pause the clock.

$30,000 IRS debt questions, answered

Can I get a payment plan if I owe the IRS $30,000?

In most cases, yes — $30,000 is under the $50,000 ceiling for a long-term online installment agreement of up to 72 months. Because your balance is above $25,000, the IRS requires direct-debit payments for the streamlined version. You must also be current on filing all required returns before the IRS will approve any agreement.

How much is the monthly payment on $30,000 of IRS debt?

The baseline is about $417 a month — $30,000 spread across the 72-month maximum — though the IRS sets the actual figure slightly higher because interest and a reduced 0.25% monthly late-payment penalty keep accruing during the plan. You can always pay more than the minimum, and paying the balance off early cuts the total interest significantly.

Can I settle $30,000 in IRS debt for less than I owe?

Only through an Offer in Compromise, and only if your income and assets show the IRS could never collect the full $30,000 before the collection statute runs out. The IRS accepted roughly one in five offers in FY2024 — acceptance is arithmetic, not negotiation. If you can genuinely afford about $417 a month, an offer is unlikely to succeed and a payment plan is the realistic path.

Will the IRS file a tax lien if I owe $30,000?

It can — the IRS generally considers filing a Notice of Federal Tax Lien on balances over $10,000, and $30,000 is well inside that range. Setting up a direct-debit installment agreement before a lien is filed makes one much less likely. If a lien has already been filed, paying the balance below $25,000 on a direct-debit plan opens the door to requesting a lien withdrawal.

Can the IRS take my passport over $30,000?

No — passport certification applies only to seriously delinquent tax debt above $66,000 in 2026, and $30,000 is well below that line. The caution is that an ignored balance grows: penalties and interest compound monthly, and adding new unpaid years can push a $30,000 debt toward the threshold faster than most people expect.

Is my ex-spouse responsible for our joint $30,000 tax debt?

If the debt comes from a jointly filed return, the IRS can collect the full amount from either of you, no matter what your divorce decree says. The decree only gives you the right to pursue your ex in state court. Relief through the innocent spouse rules or equitable relief may reassign part of the debt, but you have to apply — it never happens automatically.

Does $30,000 in IRS debt go away after 10 years?

The IRS generally has 10 years from assessment to collect, after which the balance expires. But that clock pauses during bankruptcy, a pending Offer in Compromise, and certain appeals, so the real expiration date is often later than the 10-year mark. Waiting it out also means a decade of notices, liens, and potential levies along the way.

Will the IRS garnish my wages over a $30,000 balance?

Not immediately — a wage levy can only follow a final notice of intent to levy (LT11 or Letter 1058) plus a 30-day window to respond. If you are still receiving CP14 or reminder notices, garnishment is not imminent. But once a wage levy starts, it is continuous until released, which is why acting during the notice stage matters so much.

Your next 24 hours

- Pull the real number. Log into your IRS online account and write down the exact balance and every tax year it covers — the notices in your drawer may already be out of date.

- Gather three things: your most recent tax return, your current income information, and — if this is joint-return debt — your divorce decree and the return in question.

- Get a free case review. Penalties and interest are compounding on this balance every month; a review costs nothing and maps your cheapest path out. Use the 2-minute form or call (888) 825-7779.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.