IRS Relief Programs

Innocent Spouse Relief: How to Qualify in 2026 (All Three Types, Explained)

The short answer: for innocent spouse relief, how to qualify comes down to three things — you filed a joint return, the tax problem traces to your spouse's or ex-spouse's errors, and you didn't know about them when you signed. You request it on IRS Form 8857, generally within 2 years of the IRS's first collection action against you.

You're being pursued for a tax debt someone else created. Maybe the audit letters started after the divorce, maybe your refund vanished into a balance you'd never heard of — either way, your name is on that joint return, and the IRS is treating the whole bill as yours. There is a legal exit, and it has three separate doors: traditional innocent spouse relief, separation of liability, and equitable relief.

Every one of those doors opens through a single document — Form 8857 — and the visual guides below map the key facts, deadlines, and options that decide your case. This guide walks through each relief type, the knowledge test that decides most cases, and the deadlines that quietly close them.

⏱ Your deadline: you have 2 years from the IRS's first collection activity against you — a refund offset, a levy notice, a collection suit — to request traditional innocent spouse relief or separation of liability. Equitable relief has a longer window: generally as long as the IRS can still collect the debt (typically 10 years from assessment), or within the refund statute if you want money back. The clock starts with IRS action, not your divorce date and not the day you discovered the debt.

Why the IRS is billing you for your spouse's tax debt

A joint tax return makes both signers 100% liable for the entire tax bill — the law calls it joint and several liability, and divorce does not undo it. The IRS can collect the full amount from whichever spouse is easier to reach, and it usually does exactly that.

Your divorce decree doesn't change this. A decree assigning the debt to your ex binds your ex, not the IRS — the agency wasn't a party to your divorce and ignores its terms, a trap covered in depth in our guide to divorce decree irs debt and the broader question of divorce and IRS debt: who pays.

Before going further, confirm you're reading the right guide. If your refund was seized for a debt that was never yours — your spouse's child support, student loans, or pre-marriage taxes — you need injured spouse relief on Form 8379, a completely different filing. The distinction is laid out in injured spouse vs. innocent spouse. Innocent spouse relief is for when the joint debt itself shouldn't be yours.

One more distinction that decides which relief you can even request: an understatement means the IRS added tax the return never showed — hidden income, inflated deductions, an audit or CP2000 assessment. An underpayment means the return was accurate but the balance was never paid. Two of the three relief types only cover understatements; only equitable relief reaches unpaid balances. Keep your category in mind as you read.

What happens if you do nothing about the joint debt

If you take no action, the IRS collects the joint balance from you exactly as if the debt were 100% yours. The notice sequence is automated and doesn't pause to ask whose income created the bill:

- Balance-due notices (CP14, CP501, CP503) — bills addressed to both names on the return, with penalties and interest compounding monthly.

- Refund offsets — every refund you're owed, on every future return, gets swallowed until the joint balance is gone.

- CP504 — the IRS can seize your state tax refund, and a federal tax lien becomes likely, attaching to your home and hurting your business credit.

- LT11 / Letter 1058 — final notice of intent to levy. After 30 days, the IRS can levy bank accounts and income. If you're self-employed, that means your business operating account (funds are held 21 days before they're gone) and even levies on your clients' payments to you.

- Passport certification — once the assessed balance passes $66,000 (the 2026 threshold), the IRS can certify the debt to the State Department, blocking passport renewal.

Here's the part that changes everything: filing Form 8857 generally suspends collection against you for the years in your request while the IRS decides. In 2026, with IRS staffing down roughly 27% but automated levies running uninterrupted, that pause is the difference between arguing your case calmly and arguing it while your bank account is frozen. And remember the 2-year window from the deadline box — an offset you shrugged off two winters ago may already have started it.

Being collected on for a spouse's or ex-spouse's tax debt?

If the IRS has already taken a refund or sent a levy notice, your 2-year window for two of the three relief types is already running. Get your innocent spouse case reviewed free — an experienced tax professional will tell you which relief type fits and how much time you have left.

Innocent spouse relief: how to qualify under each of the three types

Innocent spouse relief under IRC §6015 comes in three distinct types — traditional relief, separation of liability, and equitable relief — and each has different eligibility rules, knowledge standards, and deadlines. Form 8857 asks the IRS to consider you for all three, but knowing which one your facts fit tells you what evidence to lead with.

| Requirement | Traditional — §6015(b) | Separation of liability — §6015(c) | Equitable — §6015(f) |

|---|---|---|---|

| Covers | Understatements only (audit / CP2000 assessments) | Understatements only | Understatements and unpaid balances |

| Marital status | Any — including still married | Divorced, legally separated, widowed, or living apart 12+ months | Any |

| Knowledge standard | You had no actual knowledge and no reason to know | The IRS must prove you had actual knowledge of the item | Knowledge is one factor, not an automatic bar |

| Deadline | 2 years from first collection activity | 2 years from first collection activity | While the IRS can still collect; refund statute for refunds |

| Refund of amounts paid | Possible | No | Sometimes |

Traditional innocent spouse relief — §6015(b)

This is the original version, and the hardest test. You must show the understatement is entirely attributable to your spouse's erroneous items, that when you signed you neither knew nor had reason to know of it, and that holding you liable would be unfair given all the circumstances — did you benefit from the unreported money, are you divorced, were you deceived. Fail the "reason to know" prong and this door closes, which is why most requesters also need one of the next two.

Separation of liability — §6015(c)

If you're divorced, legally separated, widowed, or have lived apart for the 12 months before filing, this is usually the strongest path for audit debts. Instead of erasing the assessment, the IRS splits it — allocating each erroneous item to the spouse it belongs to, as if you'd filed separately. Its key advantage: the burden flips. The IRS must prove you had actual knowledge of the specific item; suspicion or "should have known" isn't enough. Full mechanics are in our guide to separation of liability. The tradeoff: no refunds of amounts already paid, and you keep whatever slice of the debt traces to your own items.

Equitable relief — §6015(f)

Equitable relief is the safety net, and the only type that covers underpayments — the return was right, but your spouse promised to pay the balance and never did. It's decided on a weighing of fairness factors (covered in the next section) rather than bright-line rules, and it's where abuse, financial control, and economic hardship carry real weight. It has its own full guide: equitable relief irs.

Community property and state caveats. If you live in a community property state and filed separately, §6015 doesn't apply — but relief under §66 does; see community property tax relief. And IRS relief never automatically fixes a state balance. California runs its own program with its own rules through the Franchise Tax Board — see FTB innocent spouse — and remember the FTB can collect for 20 years, twice the IRS's window.

The knowledge test: where most innocent spouse cases are won or lost

"Reason to know" — not the paperwork — is the hurdle that decides most innocent spouse cases. The IRS reconstructs what a reasonable person in your position would have noticed: Did the household spend more than the reported income could support? Did you handle the bills or the bookkeeping? Do you have business or financial experience? Did your spouse act evasively about money?

Be honest with yourself about one edge case here: if you're self-employed or run your own business, expect a higher bar. The IRS tends to presume that someone who manages a Schedule C, invoices, and quarterly estimates understands financial documents — so "I just signed where the preparer pointed" lands weaker coming from a business owner than from a spouse with no financial role. It doesn't sink the case; it means your evidence must show you had no access to or involvement in the specific item — a brokerage login you never had, a separate account statement mailed to a P.O. box, gambling activity concealed from you (a pattern common enough that we cover it separately in spouse hid income from me and spouse gambling tax debt).

Three points people get wrong about knowledge:

- Signing without reading is not a defense. The law charges you with what a reasonable review would have revealed on the face of the return.

- Under separation of liability, the burden is the IRS's. The agency must prove actual knowledge of the item itself — a far friendlier standard than "reason to know."

- Abuse changes the analysis. If you signed under duress, or your spouse controlled the finances and retaliation was a real fear, even actual knowledge may not bar relief. Document it — police reports, medical records, protective orders, or a detailed written account all count.

How the IRS weighs equitable relief: the seven factors

Equitable relief is decided under Revenue Procedure 2013-34, which lists seven weighing factors — no single factor controls, and no single bad factor is fatal. There's also a fast lane: if you're divorced or separated, would suffer economic hardship, and had no reason to know, the IRS can grant "streamlined" relief without the full weighing.

| Factor | Weighs toward relief | Weighs against relief |

|---|---|---|

| Marital status | Divorced, separated, or widowed | Neutral if still married |

| Economic hardship | Paying would leave you unable to cover basic living costs | Neutral if you can pay comfortably |

| Knowledge or reason to know | You didn't know and couldn't reasonably have known | You knew or should have known |

| Legal obligation | Divorce decree assigns the debt to your ex | Decree assigns it to you |

| Significant benefit | You saw none of the money beyond normal support | You enjoyed a lifestyle the hidden income funded |

| Tax compliance since | You've filed and paid on time in later years | Ongoing noncompliance |

| Abuse or poor health | Documented abuse, financial control, or serious illness — can outweigh other negative factors | — |

Notice what this table rewards: paper. A decree page, a lease showing separate households, bank statements proving you never touched the account — each converts a "he said, she said" into a factor in your column.

A worked example: $83,100 of joint debt and a sole proprietor

Say you run a sole-proprietor landscaping business and filed jointly for 2022. In 2025 the IRS audited the return and assessed $83,100 — and your divorce finalized while the audit was still open. This is hypothetical, but the arithmetic is how these cases actually get decided:

- $68,300 traces to your ex-spouse's items: about $52,000 in tax on options-trading gains from a brokerage account you never had access to, plus a $10,400 accuracy-related penalty (20% of that tax) and roughly $5,900 of interest.

- $14,800 traces to your items: the auditor disallowed $38,000 of your Schedule C vehicle and equipment deductions, adding about $11,300 in tax, a $2,260 penalty, and $1,240 in interest.

- $68,300 + $14,800 = $83,100.

Under separation of liability, the IRS allocates each item to the spouse it belongs to. If the agency can't prove you actually knew about the brokerage account, the $68,300 shifts entirely to your ex — and you remain liable for the $14,800 that came from your own deductions. Traditional relief wouldn't do better: it only ever reaches the spouse's erroneous items, so your $14,800 slice was never eligible under any type. (You can still attack that remainder separately — the 20% penalty on it may qualify for reasonable-cause penalty abatement, and the balance fits an ordinary payment plan.)

Two more things this example shows. First, at $83,100 the balance sits above the $66,000 passport-certification threshold — so doing nothing carries consequences beyond money. Second, relief rarely means the whole bill vanishes; it means you stop paying for someone else's items. That's the honest version of this program, and it's still worth tens of thousands of dollars here.

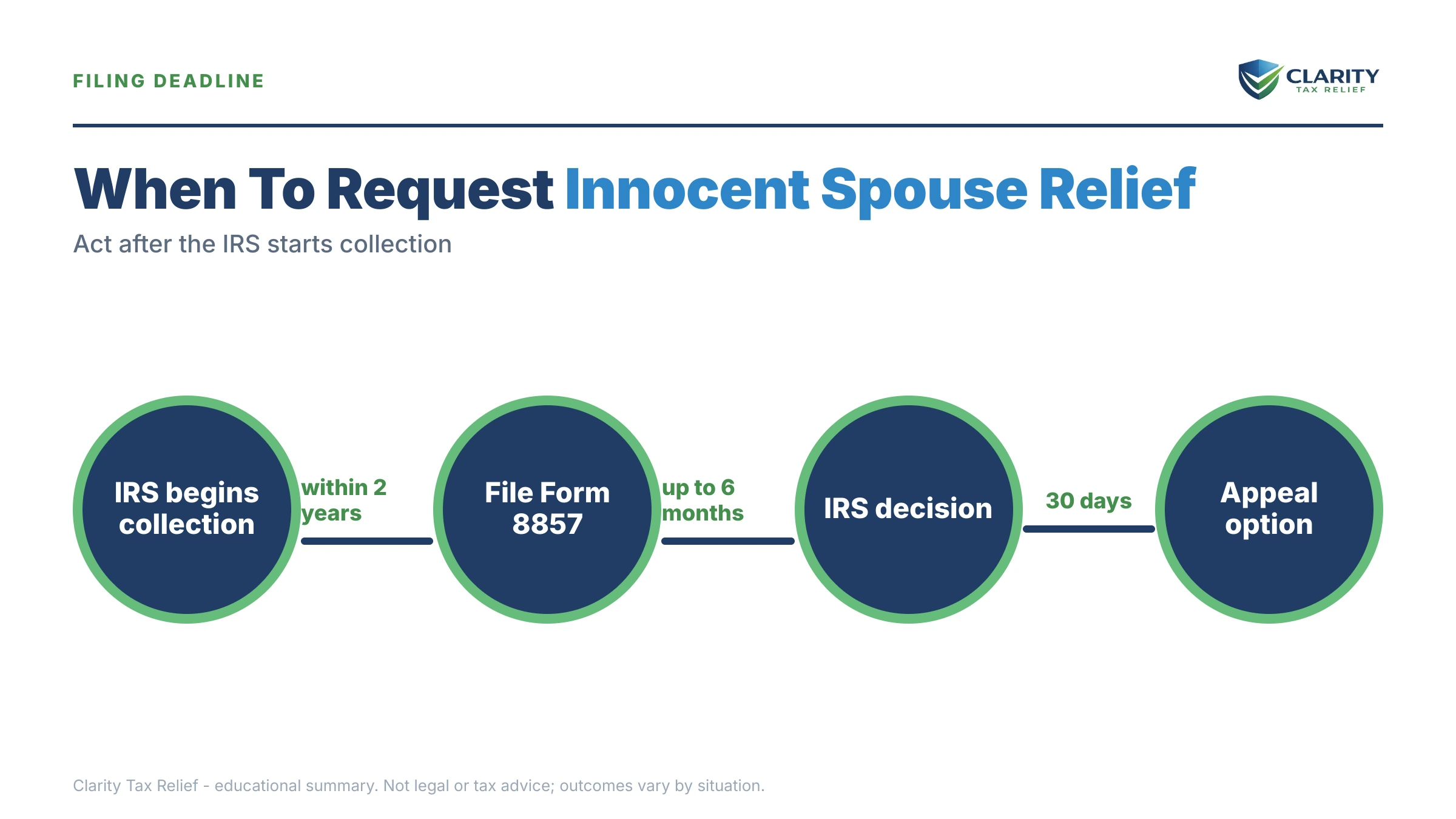

Innocent spouse relief deadlines: what happens after you file Form 8857

After you file Form 8857, the IRS must contact your ex-spouse, issue a preliminary determination both of you can appeal, and then a final determination that starts a 90-day Tax Court clock. There's no exception to the ex-spouse contact rule — they'll get Form 12508 asking for their side — but the IRS won't reveal your current address, phone, or employer, and documented abuse strengthens your claim rather than weakening it.

Expect the review to take months — often six or more, and longer with 2026's reduced IRS staffing. Collection against you is generally paused while the request is pending, but interest keeps running on whatever you ultimately owe, and the 10-year collection statute is extended by the pause plus 60 days. If you're weighing the equitable relief window, that statute is the whole game — you can estimate how much collection time remains with our CSED Calculator.

| Trigger | Your window | What you lose if it passes |

|---|---|---|

| IRS's first collection activity (offset, levy notice, suit) | 2 years to file Form 8857 | Traditional relief and separation of liability — only equitable relief remains |

| Assessment of the joint debt | Equitable relief available while the collection statute is open (typically 10 years) | All relief on the unpaid balance |

| Payments you made toward the debt | Refund claims: generally 3 years from filing or 2 years from payment | Recovery of money already paid |

| Final determination letter | 90 days to petition the U.S. Tax Court | Judicial review of the denial |

If the answer comes back no, that's the middle of the process, not the end — the appeal and Tax Court routes are mapped in innocent spouse denied.

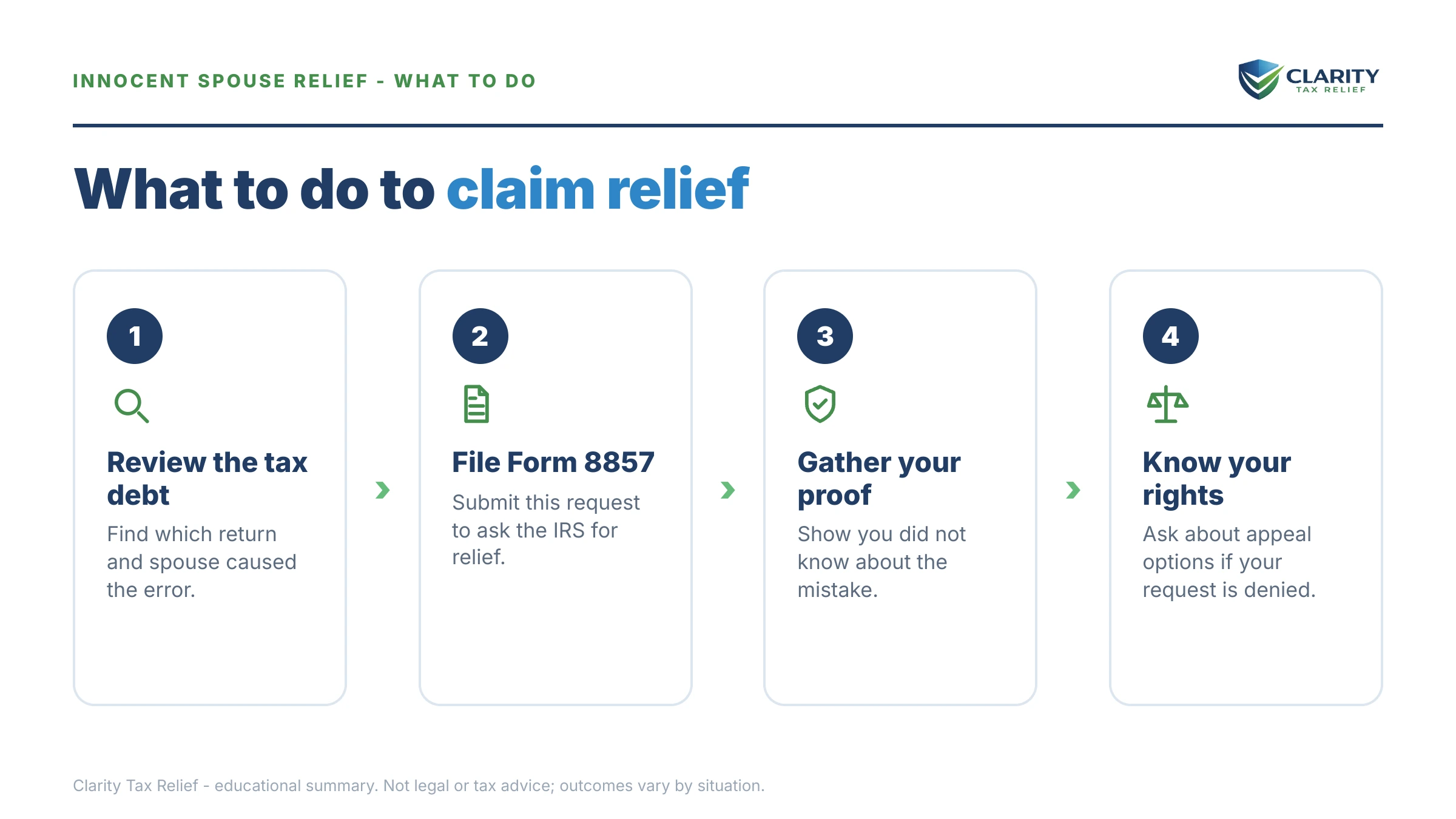

How to request innocent spouse relief, step by step

- Pull your IRS records. Get account transcripts for every year of the joint debt so you can see what was assessed, when the IRS first tried to collect from you, and how much collection time remains — your 2-year window runs from the IRS's first collection activity, not from your divorce.

- Identify your relief type and deadline. Match your facts to traditional relief, separation of liability, or equitable relief. If you're divorced, legally separated, or have lived apart 12 months and the debt came from an audit or CP2000, separation of liability is usually the strongest starting point.

- Gather your evidence. Collect the joint returns, divorce or separation records, and proof of what you knew — bank statements, account access records, emails, and anything showing your spouse controlled the finances or concealed the income.

- Complete and file Form 8857. One Form 8857 can cover multiple tax years. Answer the financial-involvement and knowledge questions carefully, attach documents instead of bare explanations, and mail or fax it to the address in the form instructions.

- Respond to every IRS follow-up. The IRS will contact your ex-spouse and may send you questionnaires; a missed response is a common reason otherwise-solid requests fail. Expect the review to take months, often six or more.

- Appeal a denial on time. Appeal a preliminary denial to the IRS Independent Office of Appeals, and if the final determination still denies relief, petition the U.S. Tax Court within 90 days of the determination letter.

For a line-by-line walkthrough of Form 8857 — including the knowledge and abuse questions that trip people up — see our Form 8857 walkthrough.

When you can handle this yourself — and when help changes the outcome

Plenty of innocent spouse requests succeed without professional help. You're a good DIY candidate when the facts are clean: you're divorced, the hidden income is documented in the IRS's own audit file, it's a single tax year, there's no abuse dimension to present, and you're comfortably inside the 2-year window. File Form 8857 carefully, attach your documents, and answer the follow-ups on time.

Experienced help tends to change outcomes in specific situations: when the knowledge fight is real (especially if you're a business owner facing the sophistication presumption), when abuse or financial control needs to be documented and presented, when multiple years or a mix of understatements and unpaid balances require different relief types per year, when a levy is already in motion and collection needs to be paused fast, or when a denial is headed to Appeals or Tax Court. And if only part of the debt is relieved — like the $14,800 remainder in the example above — the leftover balance still needs a resolution strategy; the full toolkit is in how to settle tax debt yourself, and if you do hire someone, vet them against the checklist in how to choose a tax relief company.

If any of those harder scenarios sounds like yours, get your innocent spouse case reviewed free before more of the 2-year window burns — call (888) 825-7779 or use the 2-minute form.

Terms on Form 8857 and your notices, decoded

- Joint and several liability — each spouse on a joint return owes 100% of the bill; the IRS can collect all of it from either one.

- Understatement vs. underpayment — an understatement is tax the return never showed (audit/CP2000 additions); an underpayment is a correct return whose balance went unpaid. Only equitable relief covers underpayments.

- Erroneous item — the specific mistake creating the debt: unreported income, a bogus deduction, an improper credit. Relief is decided item by item.

- Nonrequesting spouse — the other person on the return. The IRS must notify them and let them tell their side, usually via Form 12508.

- Actual knowledge vs. reason to know — actual knowledge means you knew of the item itself; reason to know means a reasonable person in your shoes would have. Different relief types use different standards.

- CSED — the Collection Statute Expiration Date, when the IRS's 10-year collection window closes. A pending Form 8857 pauses and extends it.

Innocent spouse relief questions, answered

What qualifies you for innocent spouse relief?

Three things, at minimum: you filed a joint return, the tax problem is attributable to your spouse's or ex-spouse's erroneous items or unpaid balance, and holding you liable would be unfair given what you knew and how you benefited. Each of the three relief types adds its own tests — traditional relief requires that you had no reason to know of the error, separation of liability requires a divorce, legal separation, or 12 months living apart, and equitable relief weighs a list of fairness factors.

How long do you have to file for innocent spouse relief?

You have 2 years from the IRS's first collection activity against you — a refund offset, a levy notice, or a collection suit — for traditional relief and separation of liability. Equitable relief can be requested as long as the IRS can still collect, generally 10 years from assessment, or within the refund statute if you're asking for money back. The clock runs from IRS action, not from your divorce or when you discovered the debt.

Will my ex-spouse be notified if I file Form 8857?

Yes. The law requires the IRS to contact the other person on the joint return and let them participate — there is no exception, even in abuse cases. What the IRS will not do is disclose your current name, address, phone number, or employer. If you fear retaliation, explain your safety concerns on Form 8857; a history of abuse or financial control is also a factor that strengthens an equitable relief claim.

What is the difference between injured spouse and innocent spouse relief?

Injured spouse relief (Form 8379) recovers your share of a joint refund that was seized for your spouse's separate debt — their old taxes, child support, or student loans. Innocent spouse relief (Form 8857) removes your liability for a joint tax debt itself. If the debt comes from a jointly filed return, you need innocent spouse relief; if a refund was taken for a debt that was never yours, you need injured spouse relief.

Does the IRS stop collecting while my innocent spouse request is pending?

Generally yes — filing Form 8857 suspends levies and most collection against you for the years in your request while the IRS reviews it. Two caveats: interest keeps accruing on any part of the debt you ultimately owe, and the 10-year collection statute is paused and extended while the request is pending, plus 60 days. Refund offsets can still happen in some situations, so don't count on a refund arriving while the case is open.

Can I get innocent spouse relief if I am still married?

Yes, for two of the three types. Traditional relief and equitable relief have no marital-status requirement — you can request them while married and living together. Separation of liability is the exception: it requires that you be divorced, legally separated, widowed, or living apart from your spouse for the 12 months before you file. Staying married does affect the equitable analysis, since being divorced or separated weighs in favor of relief.

My divorce decree says my ex is responsible for the tax debt. Doesn't that protect me?

Not from the IRS. A divorce decree is an agreement between you and your ex that state courts enforce — the IRS wasn't a party to it and isn't bound by it, so it can still collect the entire joint debt from you. The decree does help in two ways: it's a positive factor in an equitable relief analysis, and you may be able to pursue your ex in state court for amounts the IRS collects from you.

Can I get back money I already paid toward my spouse's tax debt?

Sometimes, depending on the relief type. Traditional innocent spouse relief and equitable relief can produce refunds of payments you made, generally limited to amounts paid within 3 years of filing the return or 2 years of the payment. Separation of liability relief never generates a refund — it only removes the unpaid portion allocated to your ex-spouse. List your payments on Form 8857 so the refund question is in front of the IRS from day one.

Does signing the return without reading it hurt my case?

By itself, signing without reading is not a defense — the law treats you as knowing what a reasonable review of the return would have shown. What matters is whether you had reason to know of the specific error: a brokerage account you never saw is a different case than a business loss you helped calculate. The major exception is abuse or financial control — if you signed under duress or your spouse controlled all financial information, the knowledge bar shifts.

What happens if my innocent spouse relief request is denied?

You get two more chances. First, you can appeal the preliminary determination to the IRS Independent Office of Appeals, where a new reviewer weighs the factors. If the final determination still denies relief, you have 90 days from that letter to petition the U.S. Tax Court. Many denials turn on thin documentation rather than bad facts, so an appeal built on better evidence is often worth pursuing.

Primary sources worth bookmarking: the IRS's official overview at IRS.gov — Innocent Spouse Relief, the form itself at About Form 8857, and — if your request stalls or a levy hits while it's pending — the Taxpayer Advocate Service, an independent office inside the IRS that helps for free.

Your next 24 hours

- Find the IRS's first collection action against you. Dig out the earliest notice, offset letter, or transcript entry showing collection — that date, not your divorce date, started your 2-year window for two of the three relief types.

- Gather your core file: the joint returns at issue, your divorce decree or proof of living apart, and anything showing what you did and didn't know — statements, account access records, emails.

- Get a free case review. Call (888) 825-7779 or use the 2-minute form — an experienced tax professional will map your facts to the right relief type before more of the 2-year window closes.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.