Spouse & Family Tax Relief

Injured Spouse vs Innocent Spouse in 2026: Which Relief Do You Need?

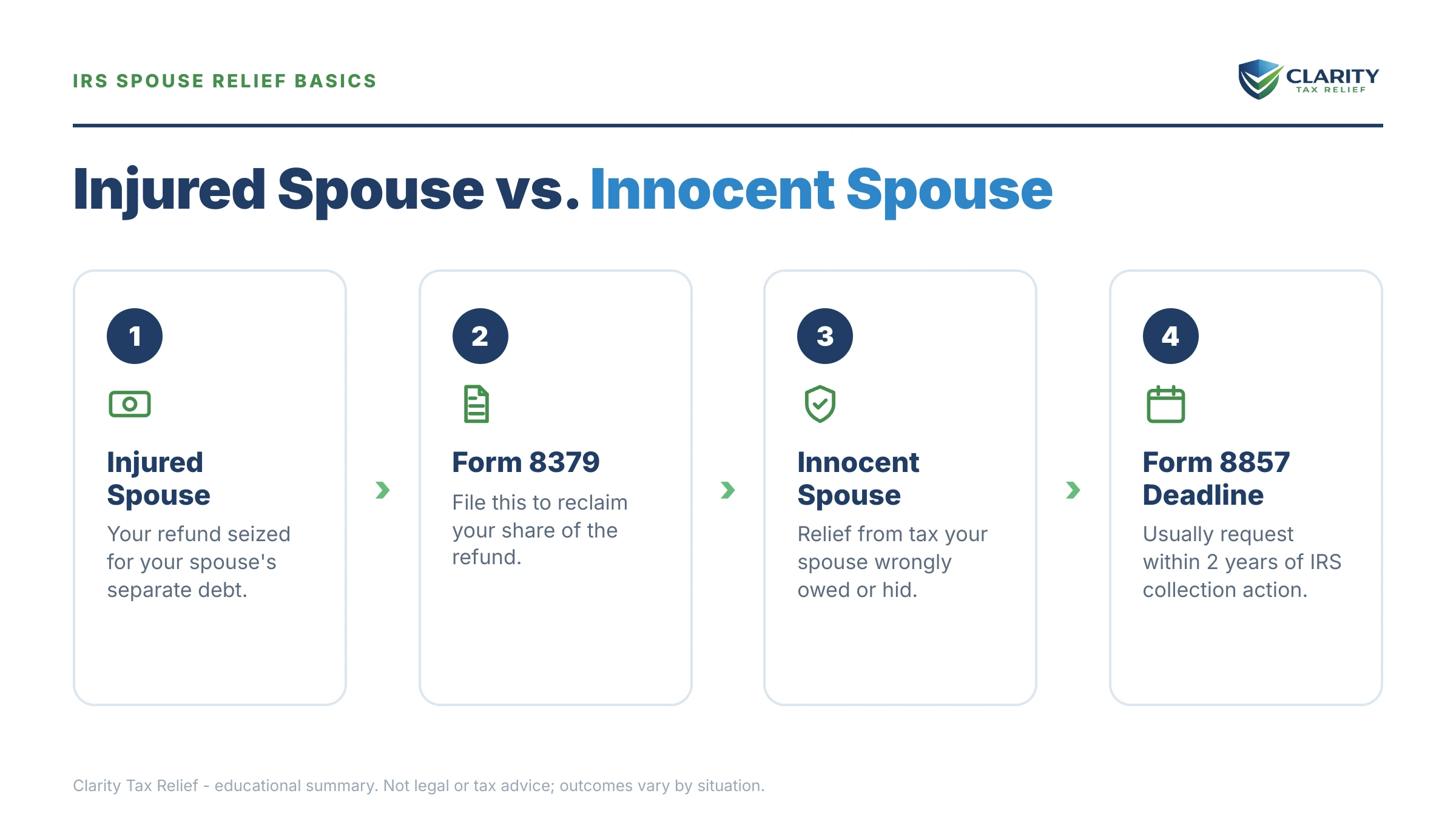

The short answer: injured spouse vs innocent spouse comes down to whose debt it is. Injured spouse relief (Form 8379) recovers your share of a joint refund taken for your spouse's separate debt. Innocent spouse relief (Form 8857) removes your liability for tax your spouse understated or left unpaid on a joint return.

Maybe the refund you were counting on this month never arrived, and a letter says it went to a debt you never knew existed. Or maybe the IRS says you owe tens of thousands for tax years your spouse — or your late husband, or your ex — always handled alone. That sinking feeling is real, but both problems have a specific legal fix, and this guide sorts out which one is yours.

The two remedies sound nearly identical and get mixed up constantly — even by preparers. They use different forms, go to different IRS units, and run on completely different clocks. Filing the wrong one doesn't just fail; it burns months you may not have. The image below shows exactly how the two paths split and where your situation fits.

⏱ Your deadlines: You have 2 years from the IRS's first collection action against you to request innocent spouse relief under sections 6015(b) and 6015(c). Injured spouse claims generally must be filed within 3 years of filing the joint return (or 2 years from when the tax was paid). Equitable relief stays open as long as the IRS can still legally collect the debt.

Injured spouse vs innocent spouse: the difference in one table

Injured spouse relief recovers a refund the government took for a debt that was never yours; innocent spouse relief removes your name from a tax debt the law currently says you share. The first is about getting money back. The second is about not owing money at all.

Here is the fastest way to tell them apart: ask "was this ever my debt?" If the debt belongs only to your spouse — child support from a prior relationship, defaulted student loans, their own back taxes from before you married — and the government grabbed your joint refund to pay it, you are an injured spouse. If the debt sits on a joint return you both signed, but it exists because of your spouse's hidden income, inflated deductions, or unpaid balance, you may be an innocent spouse.

| Question | Injured spouse (Form 8379) | Innocent spouse (Form 8857) |

|---|---|---|

| Whose debt is it? | Your spouse's separate debt (child support, student loans, state tax, their old IRS balance) | A joint IRS debt from a return you both signed |

| What went wrong? | Your joint refund was offset to pay that separate debt | Your spouse understated the tax or never paid it |

| What you get | Your share of the taken refund back | Removal of some or all of your liability, penalties, and interest |

| Filing deadline | Generally 3 years from filing the return, or 2 years from payment | 2 years from first collection activity for most types; longer for equitable relief |

| Typical wait | Roughly 8–14 weeks | Often 6 months or more |

| Marriage status | Usually still married and filing jointly | Often divorced, separated, or widowed — but none of those is required |

Why you're facing this: how each problem starts

Both problems trace back to the same legal fact: a joint return merges two people into one taxpayer in the government's eyes. What happens next depends on which direction the money flowed.

The injured spouse problem: your refund paid someone else's bill

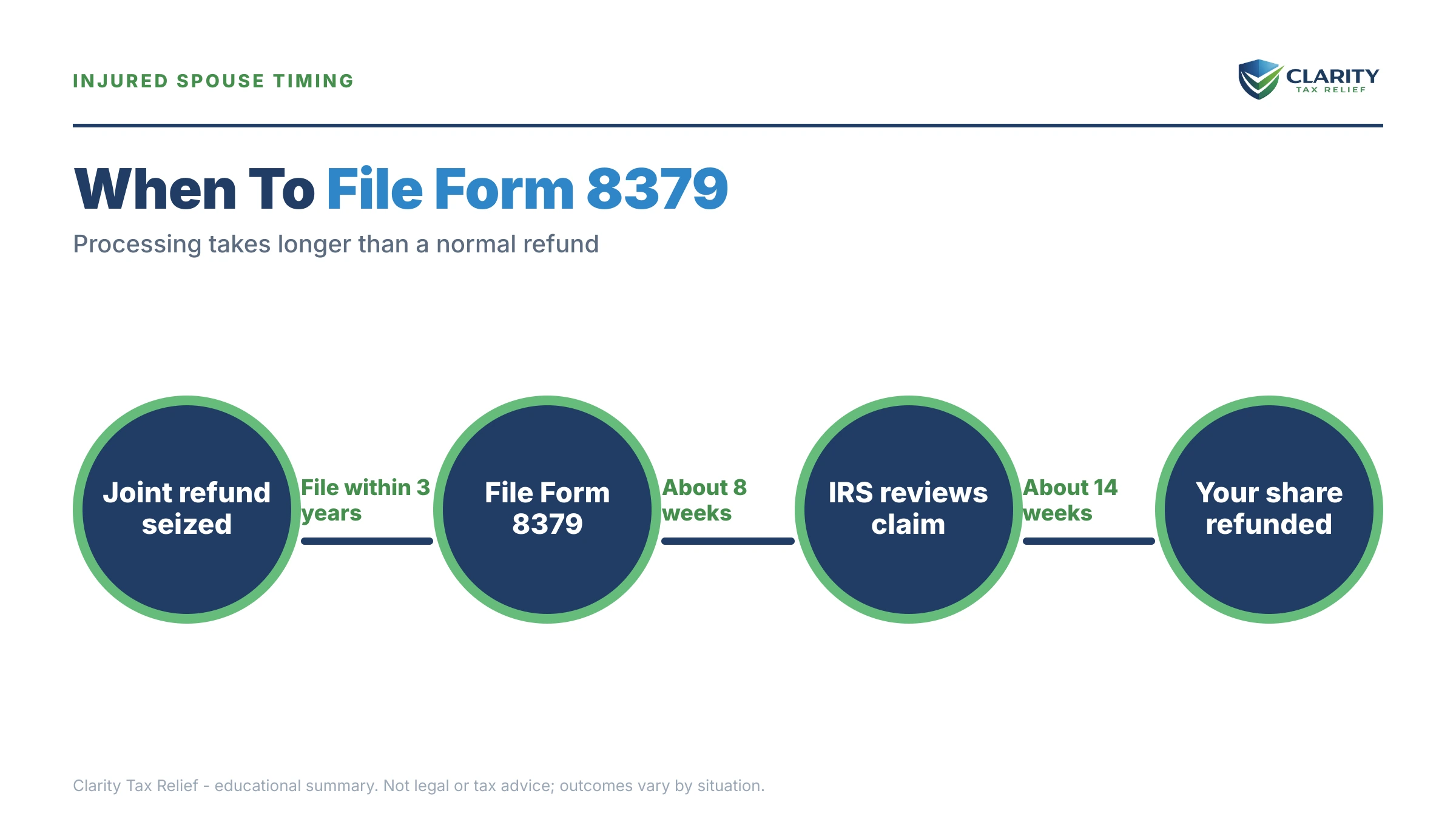

Every federal refund passes through the Treasury Offset Program before it reaches you. If either name on the return is flagged for past-due child support, defaulted federal student loans, state income tax, an unemployment overpayment, or an old IRS balance from before the marriage, the Bureau of the Fiscal Service intercepts the whole joint refund — including the portion generated by your income and your withholding. Form 8379 tells the IRS how to split the refund and return your share. Our Form 8379 walkthrough covers the allocation line by line.

The innocent spouse problem: a joint debt you didn't create

When you sign a joint return, IRC §6013 makes you jointly and severally liable — the IRS can collect 100% of the balance from either spouse, in any proportion, for the life of the debt. It does not matter whose income caused it, who kept the books, or what a divorce decree says. If your spouse ran unreported side income, invented deductions, or simply never paid what the return showed, Section 6015 gives you three ways out, all requested on Form 8857. If you're piecing together evidence that your spouse hid income from you, that evidence becomes the backbone of the claim.

One distinction inside the innocent spouse world matters enormously: an understatement (the return was wrong) opens all three relief types, while an underpayment (the return was right but the tax was never paid) can only be fixed through equitable relief. Widowed readers, take note: you can request innocent spouse relief for years filed with a deceased spouse — death does not erase the joint liability, but it doesn't erase your relief rights either.

Form 8379 or Form 8857? The notices and codes that tell you

The letter or transcript entry that alerted you almost always identifies which relief you need. Match yours below:

| What you received | What it means | Which relief fits |

|---|---|---|

| Bureau of the Fiscal Service offset letter | Your refund went to another agency's debt — child support, student loans, state tax | Injured spouse — Form 8379 |

| CP39 or CP42 notice | The IRS applied your refund or overpayment to your spouse's tax debt | Injured spouse — Form 8379 |

| Transcript code 898 | A refund offset to a non-IRS debt through the Treasury Offset Program | Injured spouse — Form 8379 (if the debt is your spouse's alone) |

| CP2000, CP22A, or CP3219A on a joint year | The IRS changed a joint return and assessed more tax | Innocent spouse — Form 8857, if the errors were your spouse's |

| CP14, CP71, CP504, or LT11 on a joint balance | The IRS is actively collecting a joint debt from both names | Innocent spouse — Form 8857; an LT11 typically starts your 2-year window |

What happens if you do nothing

Doing nothing costs the two paths differently: the injured spouse quietly loses money, while the would-be innocent spouse loses legal rights. On the joint-debt side, the sequence is automated and runs in this order:

- Assessment and first bills. The joint balance posts and CP14, then reminder notices, arrive addressed to both of you. Penalties and interest compound monthly from here forward.

- Annual reminders and lien exposure. CP71 notices restate the growing balance each year, and a federal tax lien against both names becomes possible.

- CP504, then LT11 — and your clock starts. The final notice of intent to levy is "collection activity." The 2-year window for the two strongest innocent spouse relief types starts with the first real collection action against you — a levy notice, or your own refund seized and applied to the joint debt — not with the first bill.

- Levy. Bank accounts, wages, and — for retirees — up to 15% of every Social Security check through the Federal Payment Levy Program, continuously, until the balance is resolved. Every future refund is offset too.

- Rights narrow. Once the 2-year window closes, sections 6015(b) and (c) are gone. Only equitable relief remains, and it is the most discretionary of the three.

On the refund side, the loss is quieter but just as final. The offset repeats every filing season until your spouse's debt is paid, and each year's claim has its own refund-statute deadline — generally 3 years from filing. Money you don't claim in time is gone permanently, and with the IRS workforce down roughly 27% since 2025, nobody at the agency is going to flag it for you.

A refund taken — or a levy notice on a joint debt?

One of these clocks may already be running on you. Get your notice reviewed free before the 2-year innocent spouse window closes or this year's refund claim expires — an experienced tax professional will tell you which form fits and what it can realistically recover.

Your relief options: eligibility and deadlines compared

Four distinct remedies cover the injured spouse and innocent spouse landscape, and each has its own eligibility test. If none of them fully removes you from the debt, the general resolution toolbox — payment plans, hardship status, settlement — is covered in our guide to how to settle tax debt yourself.

| Relief option | Core eligibility | Filing deadline | What it can do |

|---|---|---|---|

| Injured spouse allocation (Form 8379) | You filed jointly, contributed income, withholding, or credits of your own, and the refund went to your spouse's separate debt | Generally 3 years from filing, or 2 years from payment | Returns your allocated share of the offset refund |

| Innocent spouse relief — §6015(b) | Understatement from your spouse's erroneous items; you didn't know and had no reason to know; holding you liable would be unfair | 2 years from first collection activity | Removes the tax, penalties, and interest tied to the understatement |

| Separation of liability — §6015(c) | Divorced, legally separated, widowed, or living apart 12+ months; no actual knowledge of the erroneous items | 2 years from first collection activity | Splits the deficiency — you pay only your allocated share (no refunds of amounts already paid) |

| Equitable relief — §6015(f) | Unfair to hold you liable, but you miss the (b) or (c) tests; the only route for correct-but-unpaid returns | While the IRS can still collect — generally 10 years from assessment — or within the refund statute for refunds | Can remove understatements or unpaid balances based on a fairness-factor review |

A few specifics the table can't hold. Under the 8379 allocation, the IRS divides the refund based on each spouse's income, withholding, estimated payments, and credits — so a spouse with no income of their own may recover little, while a spouse whose withholding produced the refund can recover nearly all of it. Full qualification detail for the 6015(b) knowledge test lives in our guide to how to qualify for innocent spouse relief.

Separation of liability is usually the strongest play after divorce or a spouse's death, because it doesn't require proving you were blameless — only that you lacked actual knowledge of the specific items and that the items are allocable to the other spouse. Its trade-off: it can zero out what you still owe, but it can't refund what you already paid.

Equitable relief is the safety net, and the only path when the return was accurate but the tax went unpaid — the classic "my spouse said they mailed the check" scenario. Because it stays open as long as the IRS can still collect, knowing how much time remains on the 10-year clock matters; you can estimate your remaining collection window with our CSED Calculator. Be aware that filing Form 8857 pauses collection against you while the IRS decides, but it also extends that 10-year clock, and interest keeps accruing throughout.

A worked example: $48,300 of joint tax debt on a Social Security income

Say you're 68, retired, living on $1,860 a month in Social Security. The IRS audited your 2022 and 2023 joint returns and assessed $48,300 — all of it traced to consulting income your ex-husband earned and never mentioned. You divorced in 2024, and the LT11 just arrived. This is hypothetical, but the math is exactly what you'd face:

- Do nothing: the Federal Payment Levy Program can take 15% of your benefit — $1,860 × 0.15 = $279 a month, every month. Meanwhile the failure-to-pay penalty alone runs 0.5% a month — about $241 on a $48,300 balance — before interest. The levy would barely outpace the charges; the debt could follow you for the rest of the collection statute.

- Payment plan: at $48,300 you're under the $50,000 online threshold, so a 72-month plan is available — but $48,300 ÷ 72 ≈ $671 a month, more than a third of your entire income. Not survivable, and not necessary.

- Separation of liability: you're divorced, so §6015(c) is open. The deficiency is allocated between spouses by whose items caused it. The unreported consulting income was 100% his, and you had no actual knowledge of it — so your allocated share of the $48,300 could be $0. If the IRS shows you knew about part of the income, only that part stays with you.

- Backup positions: if knowledge is disputed, §6015(b) and equitable relief run as fallback arguments on the same Form 8857 — the IRS must consider all three.

That's the real stakes of this comparison: the difference between $671 a month you can't pay and a correctly filed claim that removes the debt from your name entirely.

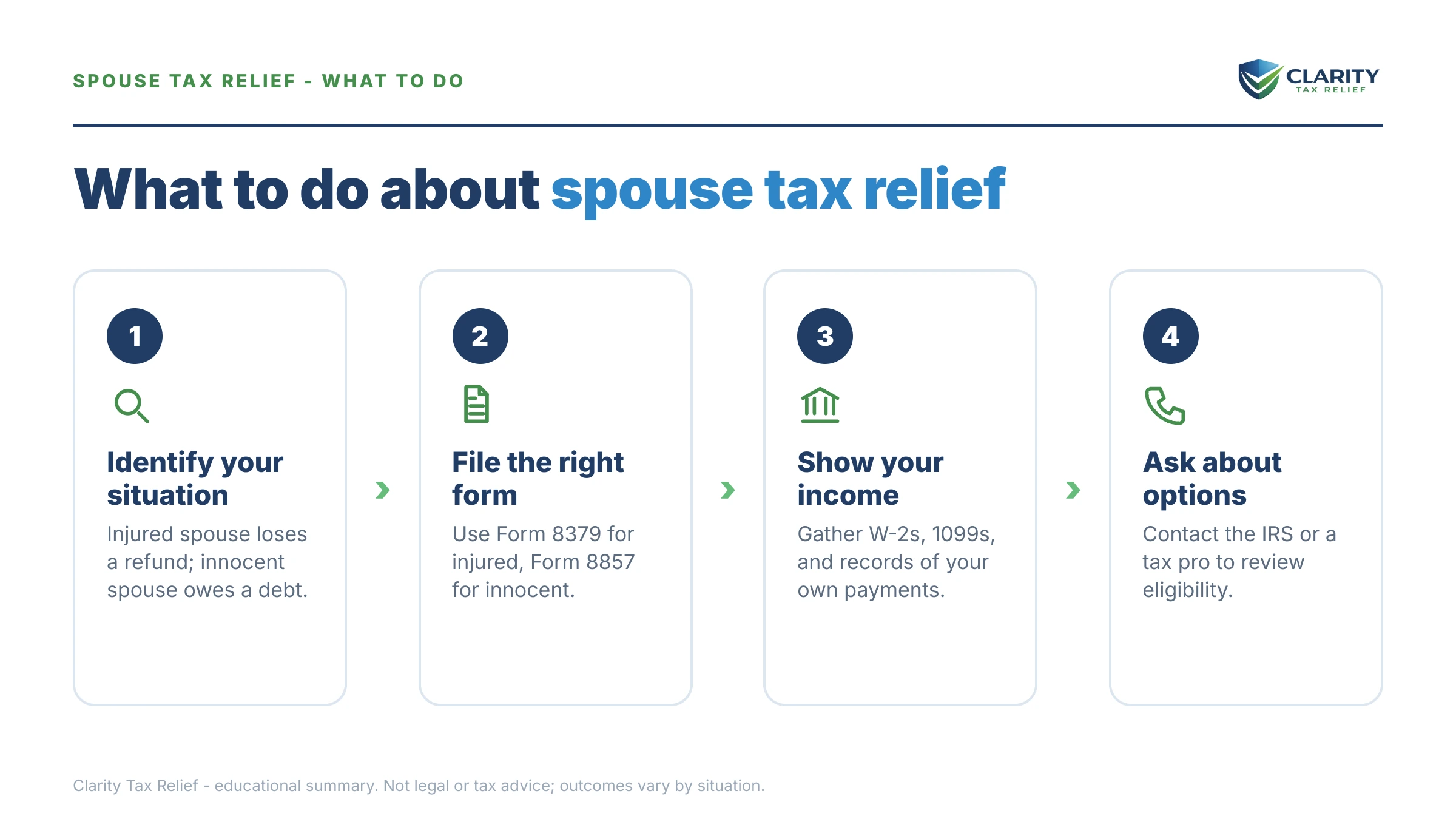

How to respond, step by step

- Diagnose which problem you have. A taken refund for a debt that was never yours means injured spouse (Form 8379); a bill on a joint return caused by your spouse's errors means innocent spouse (Form 8857).

- Confirm whose debt it is. Check your IRS online account for joint balances, and call the Treasury Offset Program at 800-304-3107 to hear exactly which agency took your refund.

- Gather your paper trail. Pull the notice, the joint returns at issue, your own income and withholding records (W-2s, 1099s, SSA-1099), and any divorce decree or death certificate.

- File the correct form. Send Form 8379 with your return or by itself after an offset; send Form 8857 as soon as you learn of the debt — one form can cover multiple tax years.

- Answer every IRS follow-up by its printed date. Both units send questionnaires, and on Form 8857 the IRS must also contact the other spouse — missing a response window can sink an otherwise strong claim.

- Appeal a denial. Protest the preliminary determination to the IRS Independent Office of Appeals, and if the final determination still denies relief, petition the U.S. Tax Court within 90 days.

If you're already at the denial stage, our guide to an innocent spouse relief denial and appeal walks through the protest letter and the Tax Court petition in detail, and the Form 8857 walkthrough covers the questionnaire itself.

When you can handle this yourself — and when help changes the outcome

Most injured spouse claims are genuinely do-it-yourself. If your situation is a straightforward offset — your W-2 or SSA income, your withholding, your spouse's clearly separate debt — attaching Form 8379 to each year's return is checkbox-level work. The official instructions at the IRS's About Form 8379 page cover it, and the agency's innocent spouse relief overview explains the 8857 side. Low-income filers can also get free representation through Low Income Taxpayer Clinics and case help from the Taxpayer Advocate Service.

Innocent spouse claims are a different animal. The IRS grants them based on evidence about knowledge, benefit, and fairness — not sympathy — and the facts have to be assembled deliberately. Experienced help tends to change outcomes when: a levy is already hitting your Social Security or bank account; the return-signing spouse is deceased and records are scattered; multiple audited years are involved; the IRS argues you "had reason to know"; your claim was already denied once; or you live in a community property state where the allocation rules invert. In those cases, how the Form 8857 narrative and exhibits are built is frequently the difference between relief and a denial you then have to appeal.

If your case touches any of those harder scenarios, a free case review — the 2-minute form or (888) 825-7779 — can tell you which Section 6015 path fits your facts before you file anything.

Community property states and state tax agencies play by different rules

In the nine community property states, half of each spouse's income legally belongs to the other — which reshapes both remedies. Injured spouse allocations follow state community property law rather than a simple "whose W-2 is it" split, and a separate relief provision under IRC §66 exists for spouses who filed separate returns but got taxed on a partner's community income. The full rules are in our guide to community property tax relief.

State income tax debts are their own universe. Federal innocent spouse approval does not automatically bind your state, and each agency runs its own program on its own forms and timelines. California's Franchise Tax Board, for example, has a distinct process covered in our FTB innocent spouse guide — and remember that the FTB can collect for 20 years, twice the IRS window, so resolving the state side matters just as much.

Terms on your notice, decoded

- Joint and several liability — the rule that lets the IRS collect 100% of a joint-return debt from either spouse, in any mix.

- Understatement vs. underpayment — an understatement means the return itself was wrong; an underpayment means the return was right but the tax was never paid. Only equitable relief covers underpayments.

- Offset — the government applying your refund to another debt through the Treasury Offset Program before you ever see it.

- Collection activity — the IRS action (a levy notice, a suit, or your refund applied to the joint debt) that starts the 2-year clock for §6015(b) and (c) claims.

- Non-requesting spouse — the other person on the joint return, whom the IRS must notify and allow to weigh in on an innocent spouse claim.

- CSED — the Collection Statute Expiration Date, generally 10 years from assessment; equitable relief remains available while it's open, and filing Form 8857 extends it.

Injured spouse vs innocent spouse: your questions answered

What is the difference between injured spouse and innocent spouse relief?

Injured spouse relief (Form 8379) recovers your share of a joint tax refund the government took to pay your spouse's separate debt, such as child support or defaulted student loans. Innocent spouse relief (Form 8857) removes your legal responsibility for tax owed on a joint return because of your spouse's errors. One recovers money that was already yours; the other erases a liability the law says you share.

How long does injured spouse relief take?

The IRS typically takes about 8 weeks to process Form 8379 when you file it by itself, and roughly 11 to 14 weeks when you attach it to your joint return. With IRS staffing down sharply in 2026, plan for the longer end of those ranges. Filing the form with your return each year is faster than chasing a refund after it has been offset.

Can I file Form 8379 after the IRS already took my refund?

Yes. You can file Form 8379 by itself after an offset, and you can file one for each year a refund was taken. The claim generally must be filed within 3 years of the date the joint return was filed or 2 years from the date the tax was paid, whichever is later. Past those windows, the money is usually gone for good.

What is the deadline for innocent spouse relief?

For classic innocent spouse relief and separation of liability, you must file Form 8857 within 2 years of the IRS's first collection activity against you, such as a levy or a refund offset applied to the joint debt. Equitable relief has a longer window: you can request it any time the IRS can still collect the debt, generally 10 years from assessment, or within the refund statute if you are seeking money back.

Do I qualify for innocent spouse relief if I signed the joint return?

Signing the return does not disqualify you — nearly every innocent spouse claimant signed the return in question. The test is whether you knew or had reason to know about the understatement when you signed, and whether it would be unfair to hold you responsible. Factors like deception by your spouse, abuse, financial control, and whether you benefited from the unpaid tax all matter.

Will the IRS contact my ex-spouse if I file Form 8857?

Yes. The law requires the IRS to notify the other person on the joint return and give them a chance to participate in the decision. The IRS does not share your current address, phone number, or employer information with them. If you are a survivor of domestic violence, say so on the form — the IRS weighs abuse heavily and handles those cases with added care.

Does my divorce decree protect me if it says my ex pays the taxes?

No. A divorce decree binds you and your ex — it does not bind the IRS. Joint and several liability means the IRS can collect the entire joint balance from either name on the return, regardless of what a state court ordered. To actually remove yourself from the debt, you need relief under Section 6015, most often separation of liability after a divorce.

Can the IRS take my Social Security for my spouse's tax debt?

If the debt is on a joint return, yes — the Federal Payment Levy Program can take up to 15% of your Social Security benefit continuously until the balance is resolved. If the debt is your spouse's separate liability that you never signed onto, your benefits should not be levied for it. Innocent spouse relief, hardship status, or a levy release can stop a Social Security levy on a joint debt.

Can I file both injured spouse and innocent spouse relief?

Yes, because they solve different problems and can both apply to the same marriage. For example, you might file Form 8857 to remove yourself from a joint balance your spouse created, and file Form 8379 this year so your current refund is not offset against that same balance while the innocent spouse claim is pending. Each form is evaluated on its own rules and timeline.

What happens if my innocent spouse claim is denied?

You can appeal. The IRS issues a preliminary determination first, which you can protest to the IRS Independent Office of Appeals. If the final determination still denies relief, you have 90 days to petition the U.S. Tax Court, where a judge reviews the case fresh. Many claims denied on paper succeed on appeal once the knowledge and fairness factors are properly documented.

Your next 24 hours

- Find the debt on your letter. A Bureau of the Fiscal Service offset letter names the agency that got your money; an IRS collection notice names the joint tax year and the balance. That one detail tells you which form you need.

- Gather three things: the joint returns for the years in question, your own income and withholding records (SSA-1099, W-2s, 1099s), and any divorce decree or death certificate that changes your eligibility.

- Get your free case review — the 2-minute form or (888) 825-7779. If a levy notice has arrived, your 2-year innocent spouse window is already running; if a refund was taken, each year's claim has its own expiration. An experienced tax professional will map both clocks before either closes.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.