IRS Relief Programs

Separation of Liability Relief (Section 6015(c)): Splitting a Joint IRS Debt After Divorce in 2026

The short answer: separation of liability relief (IRC §6015(c)) splits extra tax assessed on a joint return between you and your ex-spouse, so you pay only the portion tied to your own income and deductions. You qualify if you're divorced, legally separated, widowed, or living apart 12 months — and you elect within 2 years of the IRS's first collection activity against you.

The marriage ended, the lease is in your name alone — and now the IRS is threatening to levy your paycheck for tax on income your ex earned. Because that return was signed jointly, the law currently lets the IRS collect every dollar from you. Separation of liability is the election Congress built to undo exactly that.

This guide covers who qualifies, how the IRS actually divides the bill item by item, and how to file the request. The image below shows exactly what the request paperwork looks like and where to look, so nothing on it catches you off guard.

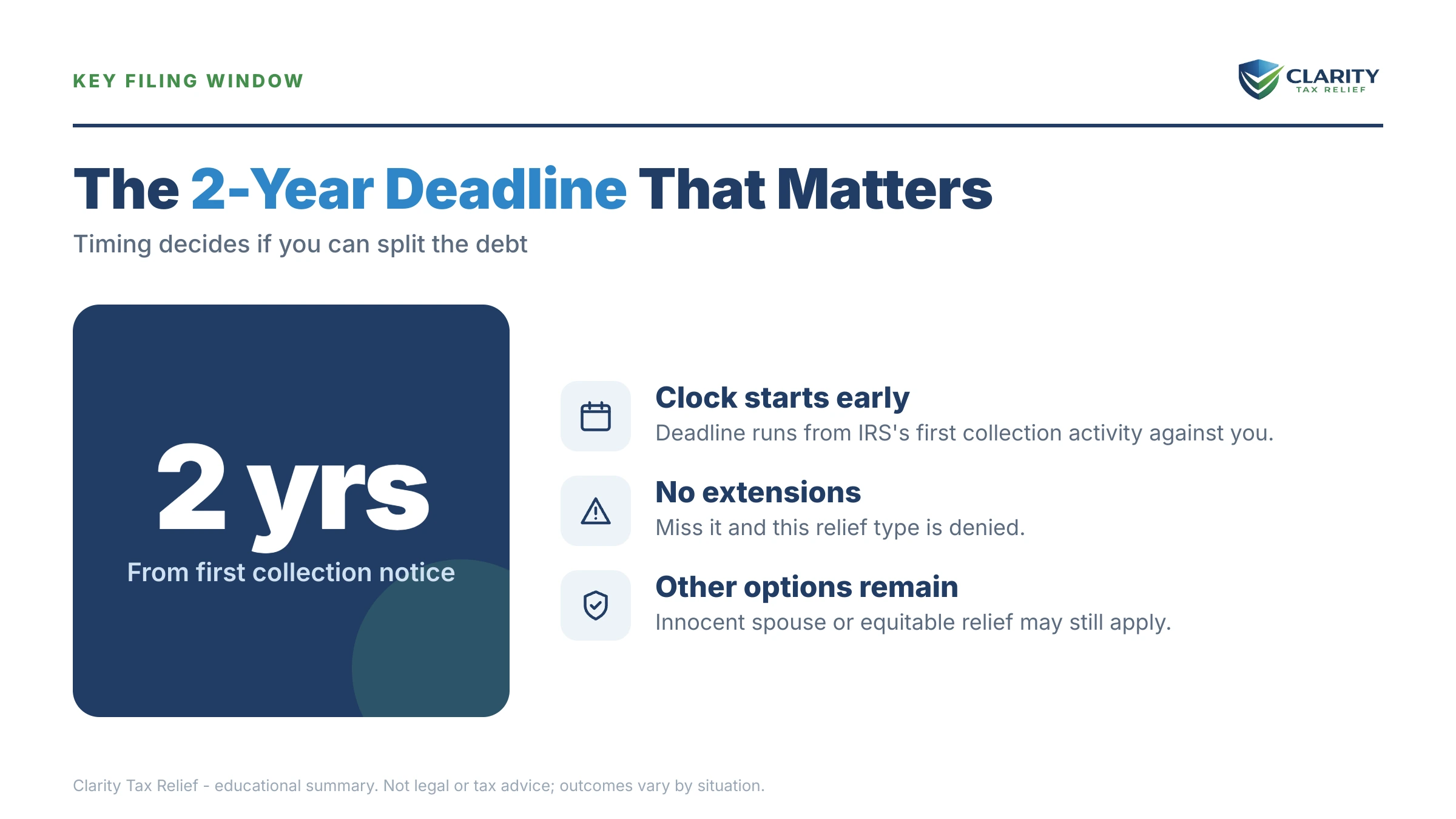

⏱ Your deadline: you have 2 years from the IRS's first collection activity against you to elect separation of liability relief. Collection activity means things like a levy notice with appeal rights or a refund offset — not a routine bill. Once the window closes, equitable relief is usually the only innocent-spouse path left.

What separation of liability relief is (and what it isn't)

Separation of liability relief under IRC §6015(c) reallocates a joint tax deficiency between two ex-spouses as if each had filed a separate return. Instead of arguing that you were completely blameless, you elect to have the extra tax divided item by item: tax generated by your ex's income becomes your ex's debt, and tax generated by your items stays yours.

The problem it solves is joint and several liability — the rule that both signers of a joint return each owe 100% of anything assessed on it. Your divorce decree assigning the IRS debt to your ex doesn't change that; the IRS wasn't a party to your divorce and isn't bound by it.

Three boundaries define this relief, and they trip people up constantly:

- It covers understatements only. That means additional tax the IRS assessed after the return was filed — typically from an audit or a CP2000 notice flagging unreported income. If the return was accurate but the balance was simply never paid, that's an underpayment, and only equitable relief can touch it.

- It never produces a refund. Section 6015(c) wipes out your share of what's still unpaid, but it can't return money you already paid or refunds already offset. If you've paid anything, request the other relief types on the same form.

- It's an election, not a plea for mercy. If you meet the tests, the statute says the IRS shall allocate the deficiency. The main way the IRS blocks an item is proving — with the burden on the IRS — that you had actual knowledge of it.

One more distinction: if your refund was taken for a debt that was solely your spouse's from before the marriage — old student loans, their pre-marriage tax bill — that's injured spouse territory, a different form with different rules. The injured spouse vs. innocent spouse comparison sorts out which one you actually need.

Who qualifies for separation of liability in 2026

You can elect separation of liability if you are divorced, legally separated, widowed, or have not shared a household with your spouse at any time during the 12 months before you file the election. This marital-status test is what separates §6015(c) from the other innocent-spouse programs — it's built specifically for people whose marriage is over.

Watch the household detail: a spouse who is temporarily away — deployment, school, even incarceration — but expected to return is still treated as a member of your household. "Living apart" means genuinely separate lives, and separate leases, utility bills, or a legal separation agreement are the proof the IRS wants to see.

Two things disqualify an otherwise eligible person:

- Actual knowledge. If the IRS can prove you actually knew about the specific item that caused the deficiency — the unreported income itself, or the facts that made a deduction bogus — that item stays joint. Suspicion isn't enough, and neither is merely signing the return. The burden of proof sits on the IRS, which is why this election often succeeds where a §6015(b) claim would fail. If you signed under duress or abuse, knowledge may not be held against you at all.

- Asset games. If assets were shuffled between you and your spouse as part of a fraudulent scheme, the election is off the table entirely. If your spouse transferred assets to you mainly to dodge tax, your relief is reduced by the value of what you received.

Then there's timing. The 2-year clock starts at the IRS's first collection activity against you — commonly a levy notice that includes your spousal-relief rights, a refund of yours seized and applied to the joint debt, or a collection lawsuit. Ordinary balance-due letters generally don't start it, but the safest reading of any notice in your mailbox is "the clock may already be running."

| Trigger event | Your window | What you lose if it passes |

|---|---|---|

| IRS's first collection activity against you | 2 years to elect §6015(c) on Form 8857 | The election itself — only equitable relief remains |

| LT11 / Letter 1058 final notice of intent to levy | 30 days to request a CDP hearing (Form 12153) | The pre-levy hearing where spousal relief can be raised |

| Final determination denying your relief | 90 days to petition the U.S. Tax Court | Independent court review — the denial becomes final |

How the IRS splits the bill: the allocation, with real math

Under separation of liability, each item that caused the deficiency is allocated to the spouse whose income or deduction generated it — as if you had filed married-filing-separately. Interest and penalties follow the tax they're attached to, so shedding an item sheds its baggage too.

Say you owe $4,800 — a hypothetical, but a common shape. The IRS audited your final joint return two years after the divorce and assessed a $4,800 deficiency: $4,100 traces to rideshare income your ex never reported, and $700 to an education credit disallowed because the expenses on your side didn't qualify. You rent, you're on a W-2, and the IRS is now threatening your paycheck for the full $4,800 because you're easier to find than your ex.

Elect separation of liability and the math changes completely:

| Item that caused the deficiency | Extra tax | Allocated to |

|---|---|---|

| Ex-spouse's unreported rideshare income (their 1099) | $4,100 | Your ex-spouse |

| Disallowed education credit (your expenses) | $700 | You |

| Total joint deficiency | $4,800 | You pay $700 + its interest; your ex owes $4,100 |

Your exposure drops from $4,800 to $700 plus the interest attached to that $700 — an amount most people can simply pay off and be done with. Two caveats keep the allocation honest: if the IRS proves you actually knew about the rideshare income, that $4,100 stays joint; and an item normally allocable to your ex can shift back to you to the extent you received a direct tax benefit from it.

Notice what the election doesn't do: it doesn't erase the $4,100. The IRS keeps collecting it — from your ex. That's the whole point of the program, and it's why the IRS is required to contact your ex before deciding.

What happens if you ignore the joint debt

Until relief is granted, joint and several liability lets the IRS collect the entire deficiency from whichever ex-spouse is easier to reach — and a W-2 renter with a bank account is usually the easier one. There's no home for a lien to quietly sit against, so the IRS reaches renters through paychecks, accounts, and refunds. The sequence runs on autopilot:

- Balance-due notices arrive in your name. Interest and the 0.5%-per-month failure-to-pay penalty keep compounding on the full joint amount, not your "fair share."

- CP504 stage. The IRS can now seize your state tax refund and apply it to the joint debt.

- LT11 / Letter 1058 final notice. A 30-day clock starts. After it runs, the IRS can levy wages and bank accounts. This notice also carries your Collection Due Process rights — one of the venues where spousal relief can be raised.

- Levy. A wage levy is continuous until released; a bank levy freezes funds for 21 days before they're sent to the IRS. You can estimate what a wage levy would leave you with using our IRS Wage Garnishment Calculator.

- Every refund, every year gets offset to the joint balance — and somewhere along this timeline, your 2-year election window quietly closes.

Filing Form 8857 changes this picture almost immediately: the law generally suspends levies and other collection against the requesting spouse while the claim is pending. The trade-off is that the 10-year collection statute pauses too, so the IRS recovers that time on the back end if relief is denied.

Being collected for your ex's tax bill?

Send us the notice. An experienced tax professional will map whether separation of liability fits your facts, what your allocated share would actually be, and how to pause collection while the request is pending — free, before your 2-year election window closes.

Separation of liability vs. innocent spouse relief vs. equitable relief

Form 8857 covers three distinct programs, and you don't have to pick just one — the form lets the IRS consider every type of relief you might qualify for, and it should. Each has a different job:

| Relief type | What it covers | Key eligibility test | Deadline |

|---|---|---|---|

| Innocent spouse relief — §6015(b) | Understatements (audit / CP2000 tax) | You didn't know and had no reason to know of the error, and holding you liable would be unfair | 2 years from first collection activity |

| Separation of liability — §6015(c) | Understatements only | Divorced, legally separated, widowed, or apart 12 months; IRS must prove your actual knowledge to block an item | 2 years from first collection activity |

| Equitable relief — §6015(f) | Understatements and underpayments | Unfair to hold you liable considering all facts and circumstances | While the collection statute (or refund statute) is open |

The practical pecking order for someone divorced: §6015(c) is usually the strongest opening move, because the IRS carries the knowledge burden and your marital status already satisfies the threshold test. Full innocent spouse relief under (b) is worth requesting alongside it when you genuinely had no idea — it can erase your share entirely and support a refund. Equitable relief under (f) is the catch-all: the only route for unpaid-but-accurately-reported balances, and the fallback if the 2-year window has already closed.

Two situation-specific wrinkles. If you live in a community property state, allocation gets more complicated because half of each spouse's income may legally belong to the other — community property tax relief under §66 has its own rules. And state tax agencies run their own separate programs with their own forms and windows; California's, for example, is covered in our FTB innocent spouse guide. Never assume a federal grant of relief automatically fixes the state bill.

If none of the three fits — say the debt really is half yours — the standard toolbox of payment plans, hardship status, and settlement still applies to your share; our guide on how to settle tax debt yourself walks through all of it.

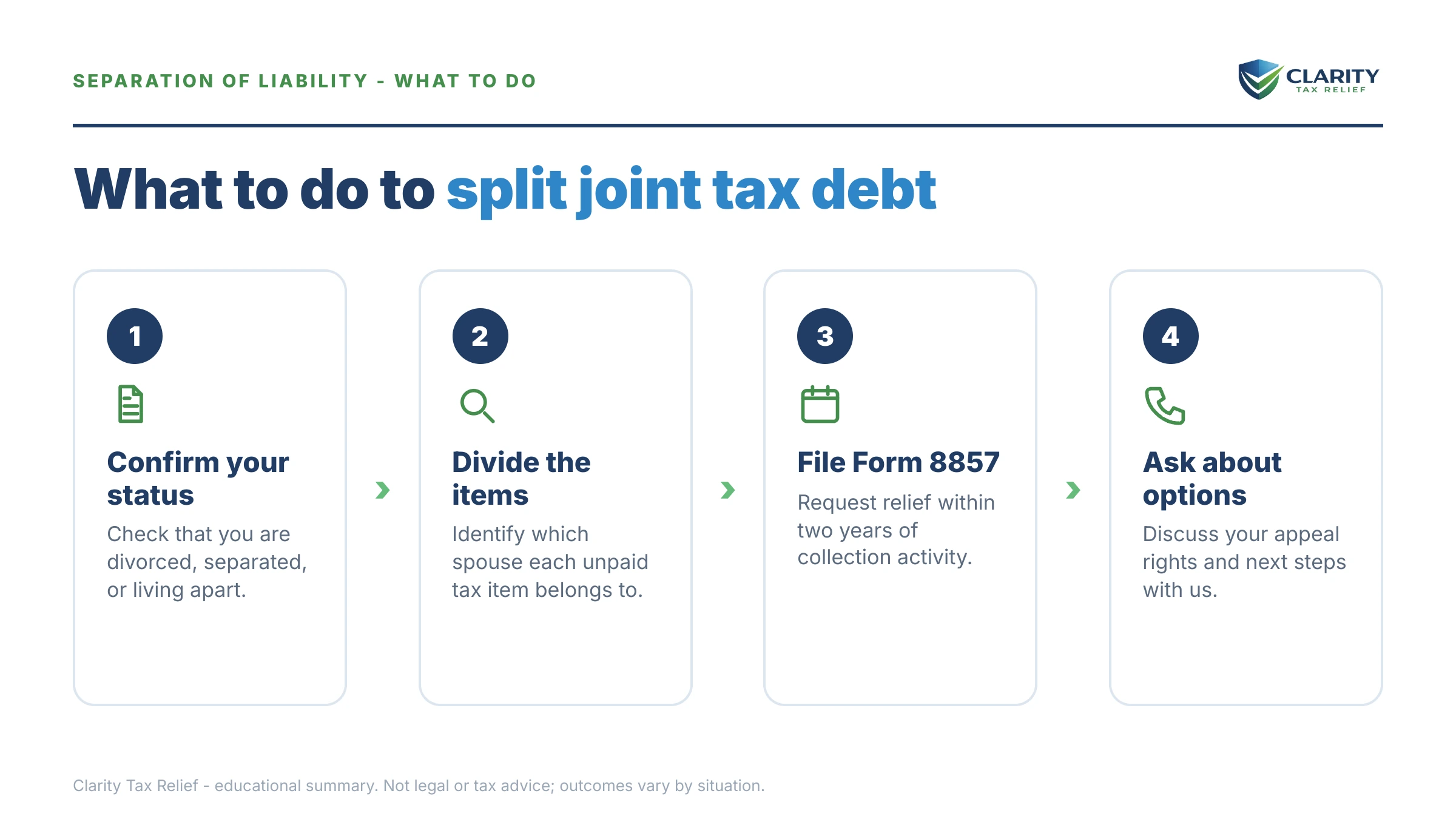

How to request separation of liability relief, step by step

- Confirm your marital-status window. Verify that you're divorced, legally separated, widowed, or have lived apart from your spouse for the entire 12 months before you file. A signed divorce decree — or separate leases and utility bills — is the cleanest proof.

- Pin down the 2-year clock. Find the date of the IRS's first collection activity against you — a levy notice with appeal rights, a refund offset, or a collection suit — and confirm you're still inside the 2-year election window.

- Gather the paper trail. Pull the joint return, the audit report or CP2000 that created the deficiency, and the documents showing whose item caused it: your ex's 1099s, business records, or account statements.

- File Form 8857. Complete Form 8857, Request for Innocent Spouse Relief, and ask the IRS to consider every type of relief you may qualify for — one form covers §6015(b), (c), and (f). Mail or fax it to the address in the instructions and keep a copy of everything.

- Respond fast and expect your ex to be contacted. The IRS must notify your ex-spouse, who gets Form 12508 to tell their side. Answer any IRS questionnaire quickly — silence is the most common reason strong claims stall or fail.

- Appeal a denial within 90 days. If the final determination denies relief, you can petition the U.S. Tax Court within 90 days. Missing that window makes the denial final, so calendar the date the determination letter arrives.

Our line-by-line Form 8857 walkthrough covers the form itself, including how to describe abuse or financial control safely — the IRS is required to keep your current address, phone, and employer from your ex. And if you've already been denied once, the innocent spouse denied guide maps the appeal and Tax Court route in detail.

When you can handle this yourself — and when help changes the outcome

There is no fee to file Form 8857, and a clean case is genuinely a DIY project. If the entire deficiency traces to one item that's unmistakably your ex's — their 1099, their business, their brokerage account — your divorce is documented, and no levy is in motion, you can reasonably file the form yourself and answer the follow-up questionnaire honestly.

Experienced help earns its cost in four situations: a levy is already in motion (the collection hold needs to be asserted and confirmed, not assumed); the IRS is arguing you had actual knowledge (this becomes an evidence fight, and how your statement is worded matters); the deficiency mixes items across both spouses or multiple years (the allocation math and tax-benefit exceptions get technical fast); or you're headed to Appeals or Tax Court after a denial. If money is tight, the Taxpayer Advocate Service and low-income taxpayer clinics can also assist at no charge.

Terms on your notice, decoded

- Joint and several liability — the rule that each signer of a joint return owes 100% of the tax, so the IRS can collect it all from either of you.

- Deficiency / understatement — extra tax the IRS assessed after your return was filed, usually from an audit or document-matching; the only kind of debt §6015(c) can split.

- Underpayment — tax your return correctly reported but that was never paid; separation of liability can't touch it, only equitable relief can.

- Actual knowledge — knowing about the specific item itself (not just suspecting something was off); the IRS must prove it to keep an item on your side of the ledger.

- Non-requesting spouse — your ex, who the IRS must notify and allow to participate in the decision and any appeal.

- Final determination — the IRS letter granting or denying relief; it starts your 90-day window to petition the Tax Court.

The IRS's own overview of all three programs is at Innocent Spouse Relief on IRS.gov, and the current form and instructions are at About Form 8857.

Separation of liability questions, answered

What's the difference between innocent spouse relief and separation of liability?

Traditional innocent spouse relief under §6015(b) erases your share of a joint understatement entirely, but you must show you didn't know and had no reason to know about the error. Separation of liability under §6015(c) only splits the bill — yet it's often easier to win, because the IRS carries the burden of proving you had actual knowledge. Form 8857 lets the IRS consider both on one request.

Can I get a refund through separation of liability relief?

No. Section 6015(c) relieves you of unpaid liability going forward, but it does not authorize the IRS to refund amounts you already paid toward the deficiency. If you've made payments — or your refunds were offset — ask for §6015(b) or equitable relief on the same Form 8857, since both of those can support a refund when their tests are met and the refund statute is still open.

What is the deadline to request separation of liability relief?

You must elect within 2 years of the IRS's first collection activity against you — for example, a levy notice with spousal-relief rights, a refund offset applied to the joint debt, or a collection lawsuit. Routine bills generally don't start the clock, but don't cut it close: if the window closes, equitable relief under §6015(f) is usually your only remaining path.

Will my ex-spouse find out if I file Form 8857?

Yes. The law requires the IRS to notify your ex (the "non-requesting spouse"), let them submit information, and let them participate in any appeal. The IRS will not share your current address, phone number, or employer with them. If you're a survivor of domestic abuse, say so on the form — the IRS factors abuse into how it handles the claim.

What if I knew my ex wasn't reporting the income?

Actual knowledge of the specific item defeats the election for that item — but the burden is on the IRS to prove you actually knew, not just that you should have suspected. Signing the return, or knowing your ex had a side business in general, isn't enough by itself. One exception: if you signed under duress or abuse, that knowledge may not be held against you.

Does separation of liability apply to tax we reported but never paid?

No. Section 6015(c) covers only understatements — extra tax the IRS assessed after the return was filed, usually through an audit or a CP2000. If your joint return showed the right tax but the balance was never paid, that's an underpayment, and equitable relief under §6015(f) is the only innocent-spouse route that can address it.

My divorce decree says my ex pays the taxes — doesn't that settle it?

Not with the IRS. A divorce decree binds you and your ex to each other, but the IRS is not a party to it and can still collect the full joint liability from either of you. Separation of liability is the federal mechanism that actually reassigns the debt. The decree still helps — as evidence of who was responsible, and as a basis to pursue your ex in state court if they don't pay their share.

Can the IRS levy my wages while my Form 8857 is pending?

Generally no. Filing a §6015 request suspends most collection against you — levies included — while the IRS considers the claim and, if you petition, while the Tax Court case is pending. Two caveats: the suspension protects only the requesting spouse, and the 10-year collection statute is paused during the request, so the IRS gets that time back later.

Your next 24 hours

- Find the trigger date. Pull every IRS letter you've received and note the date of the earliest levy notice or refund offset in your name — that's what likely started your 2-year election clock, and it tells you how much runway you have.

- Gather three documents. Your divorce decree (or proof you've lived apart 12 months), the joint return in question, and the audit report or CP2000 showing what the extra tax came from and whose item caused it.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form. We'll confirm whether separation of liability fits, calculate what your allocated share would actually be, and get the request moving before the election window closes.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.