IRS Appeals & Relief Programs

Innocent Spouse Denied: How to Appeal the IRS's Decision (2026)

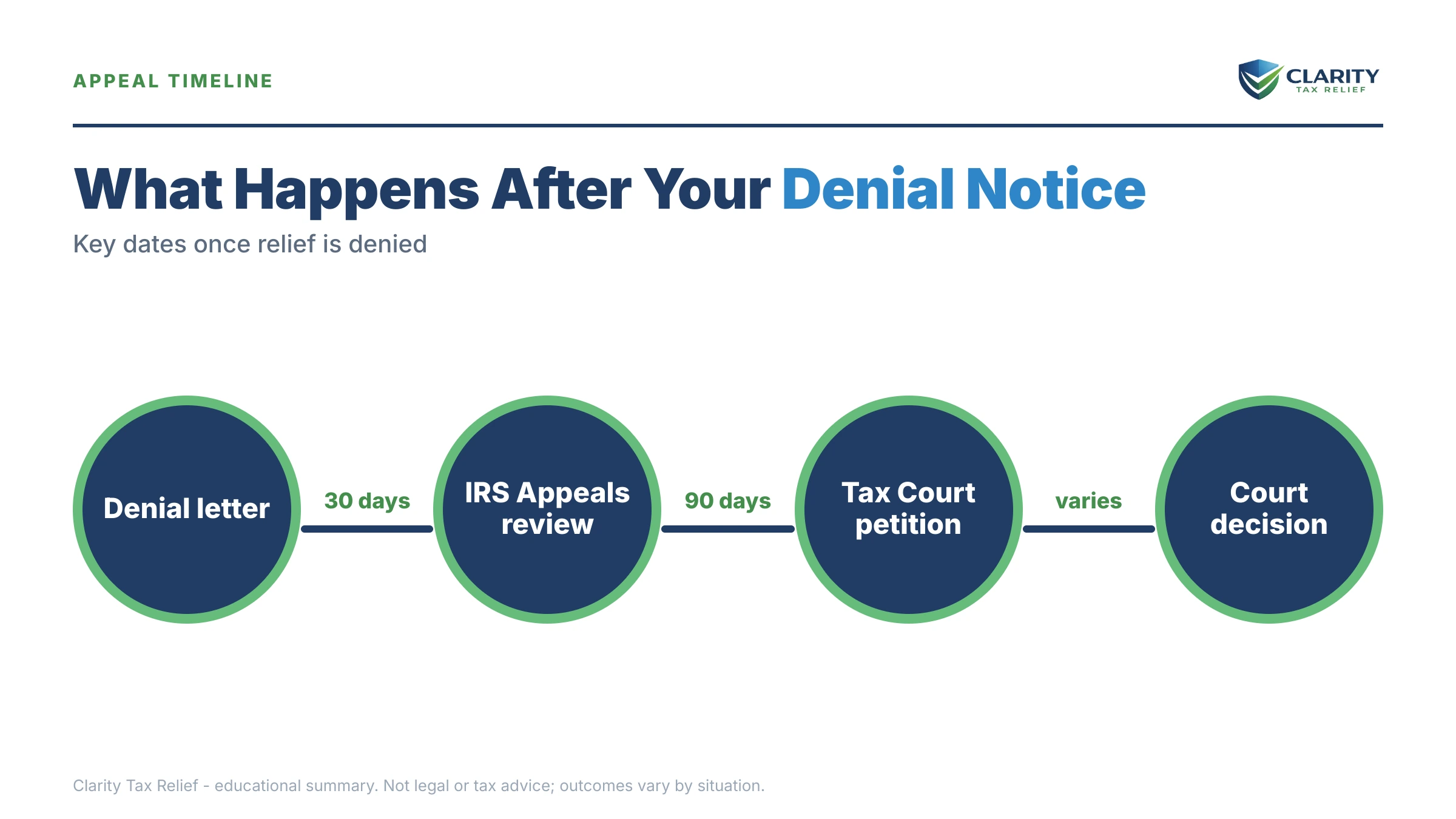

The short answer: if your innocent spouse relief was denied, you have two appeal windows. A preliminary determination gives you 30 days to request an IRS Appeals review with Form 12509. A final determination gives you 90 days to petition the U.S. Tax Court. Miss both, and the joint debt becomes fully collectible against you.

You spent months on Form 8857, laid out exactly what your spouse hid from you, and the IRS still checked the "denied" box. Now you're being told an "innocent spouse denied" letter makes you personally responsible for a debt someone else created. That decision is not final — but the appeal rights it triggers expire on a fixed schedule.

Which schedule depends entirely on which letter you're holding. A preliminary determination and a final determination look similar and carry completely different clocks — the image below shows you exactly what these determination letters look like and where the date that starts your countdown sits.

⏱ Your deadline: You have 90 days from the date on a final IRS determination letter to petition the U.S. Tax Court — a statutory deadline under Section 6015(e) that cannot be extended. If your letter is a preliminary determination, you have 30 days to appeal within the IRS using Form 12509.

Why innocent spouse relief gets denied

The IRS denies innocent spouse requests most often for one of four reasons: knowledge, benefit, a blown deadline, or thin documentation. Your denial letter names which factors went against you, and that list is the blueprint for your appeal — argue those specific points, not the whole story over again.

Knowledge or "reason to know." This kills more requests than everything else combined. If you signed the return, had access to the accounts, or lived a lifestyle the reported income couldn't support, the reviewer likely concluded you knew — or should have known — about the understatement. The appeal has to show what you actually saw at the time, not what you learned later.

Significant benefit. If the unpaid tax funded things you shared — a house, vacations, money moved into a business you own — the IRS treats that as benefiting from the underpayment, even if you never touched the hidden income directly.

The two-year rule. Relief under Sections 6015(b) and 6015(c) must be requested within two years of the IRS's first collection activity against you. Miss it and those two paths close — though equitable relief under Section 6015(f) has no two-year deadline and may still be open.

Documentation gaps. Innocent spouse reviewers can't take your word for what happened inside a marriage. Requests built on a narrative with no bank records, no correspondence, and no third-party corroboration get denied even when the story is true. If your original request was thin, our guide on building the case when your spouse hid income from me shows what evidence actually moves these decisions.

One more denial reason worth naming because it surprises people: the type of tax. Section 6015 covers only jointly filed income tax returns. If any of the balance is payroll tax, a trust fund penalty, or business tax, that portion was never eligible — no appeal changes that (more on this in the worked example below).

Which letter you're holding decides your deadline

An innocent spouse denial arrives in two stages, and each stage carries a different appeal right with a different clock. Compare your letter against the image on this page, then find your row:

| What you received | Your window | Your appeal right |

|---|---|---|

| Preliminary determination (proposed denial) | 30 days from the letter date | Independent Office of Appeals review via Form 12509 |

| Final determination (after Appeals, or after the 30 days lapsed) | 90 days from the mailing date | Petition the U.S. Tax Court under Section 6015(e) |

| No determination at all, 6+ months after filing Form 8857 | Any time after the 6-month mark | Petition the Tax Court without waiting for a letter |

| Both windows already missed | No appeal window remains | Collection alternatives, equitable relief if never considered, or a spouse defense at a CDP hearing |

The 30-day Appeals stage matters more than it looks. Since the Taxpayer First Act, the Tax Court generally decides equitable relief cases on the administrative record — the file you built with the IRS — plus only evidence that is newly discovered or was previously unavailable. Documents you never gave the IRS may be hard to introduce later. The Appeals review is your chance to get everything into that record while the door is wide open.

What happens if you ignore an innocent spouse denial

Once your appeal windows lapse, the denial becomes final and the IRS can pursue you personally for the entire joint balance — not your "share," all of it. Joint-and-several liability means each spouse owes 100%, and the IRS collects from whoever is easier to reach. Here is the sequence:

- The 30-day window lapses. Your preliminary denial converts to a final determination without an independent Appeals review — and without your best evidence in the record.

- The 90-day window lapses. The Tax Court door closes permanently for this determination. No judge will ever review the IRS's decision.

- The collection freeze lifts. The levy suspension that protected you while the case was pending ends, and the automated balance-due notice sequence resumes against you.

- Refund offsets begin. Every federal refund you're owed — including refunds generated by your business's estimated payments — gets swept into the joint balance.

- A final notice of intent to levy arrives. After its 30-day window, the IRS can garnish your pay, levy your bank accounts, and file a federal tax lien that attaches to your home and business assets.

One quiet cost of doing nothing: the 10-year collection statute was paused the entire time your innocent spouse case was pending, and that time gets added back to the end. Walking away from a denied case doesn't run out the clock — it lengthens it. Our guide to how long the IRS can collect back taxes explains the CSED, and you can estimate your own expiration date with our CSED Calculator.

In 2026, don't count on the shrunken IRS losing your file. The workforce is down roughly 27%, but determination letters, offsets, and levy notices are generated by automated systems that never stopped running.

Holding an innocent spouse denial right now?

Get your determination letter reviewed free before your 30-day Appeals window or 90-day Tax Court window closes. An experienced tax professional will tell you which clock you're on, whether an appeal is winnable, and what your fallback should be — no pressure, no obligation.

Innocent spouse denied: your options now

A denial closes one door, but it leaves at least six others open — some that re-fight the liability, some that manage it. Which ones fit depends on the letter, the calendar, and your finances:

| Option | Deadline / eligibility | Who it fits |

|---|---|---|

| Form 12509 Appeals review | 30 days from a preliminary determination; free | Anyone at the preliminary stage — always worth taking to build the record |

| Tax Court petition | 90 days from a final determination; $60 fee (waivable) | Strong facts the IRS weighed wrongly; independent judge decides |

| Equitable relief request (§6015(f)) | Open while the collection statute runs; no two-year rule | Denials under (b)/(c) for the two-year deadline, or where hardship and abuse factors were never weighed |

| Reconsideration with new information | No fixed deadline; requires facts the original reviewer never saw | You've since found bank records, court filings, or witness statements |

| Offer in Compromise — Doubt as to Liability | No fee for this OIC type; must dispute that you owe the tax | The assessment itself is wrong, separate from the spouse question |

| Payment plan / CNC / standard OIC | Means-tested; plans up to 72 months online for balances ≤ $50,000 | Appeal odds are weak, or you want the exposure capped while you fight |

| CDP hearing spouse defense | 30 days from a final levy notice, via Form 12153 | Both appeal windows missed and the relief question was never litigated |

Three of these deserve a closer look.

The equitable relief pivot. If your denial rested on the two-year deadline, you may not need to appeal at all — equitable relief under Section 6015(f) has no two-year rule and weighs factors like economic hardship, abuse, and poor health that the stricter tests ignore. Similarly, if the IRS analyzed you only under 6015(b) when you're divorced or legally separated, separation of liability relief under Section 6015(c) may allocate the deficiency to your ex on different, sometimes easier terms.

The doubt-as-to-liability route. Innocent spouse relief argues "the debt is real, but it isn't mine." An offer in compromise based on doubt as to liability argues "the debt itself is wrong" — useful when the underlying assessment came from an exam or underreporter notice your spouse never answered. It's a different legal theory, so a spouse-relief denial doesn't foreclose it.

The containment play. Sometimes the smart move is managing the balance while you fight — or instead of fighting. Payment plans, hardship status, and settlement offers all remain available after a denial; the shared mechanics live in our guide to how to settle tax debt yourself. And remember one asymmetry: if your spouse also requested relief and won, or simply pays, your exposure shrinks — the IRS can only collect the debt once.

A worked example: say the denied balance is $4,800

Say you run a small business with two employees, and the IRS denied your innocent spouse request on a $4,800 joint liability from a year your ex-spouse left 1099 income off the return you both signed. This is hypothetical, but the math is real:

- Cost of doing nothing: the failure-to-pay penalty runs 0.5% per month — $24 a month on $4,800 — plus compounding interest on top. A year of ignoring it adds roughly $290 in penalty alone before interest, and it ends in a levy notice.

- Cost of appealing: Form 12509 to Appeals is free. A Tax Court petition costs $60, waivable if you can't afford it. If you win under separation of liability, the full $4,800 — all of it attributable to your ex's unreported income — comes off your account.

- Cost of containing it: at $4,800 you're under the $10,000 ceiling for a guaranteed installment agreement, which requires full payment within three years — roughly $133/month, with interest and the 0.5% penalty still accruing until paid. A standard 72-month online plan runs closer to $67/month but costs more in accruals over time.

Now the trap specific to business owners: your company's payroll account is a separate universe. If your business also owes on its 941s, no innocent spouse outcome touches payroll tax — Section 6015 covers only joint 1040 liability. Winning your appeal on the $4,800 while ignoring a payroll balance leaves the more dangerous debt untouched, because trust-fund payroll debt can become personal through its own mechanism. Keep the two tracks separate in your planning, and see our guide to 941 back taxes if that's part of your picture.

The honest read at this dollar level: with strong facts, the free Appeals review is nearly always worth 30 days of effort. With weak facts, $133/month for three years may cost less than professional representation — and either way, the worst option is the one where the deadline passes unused.

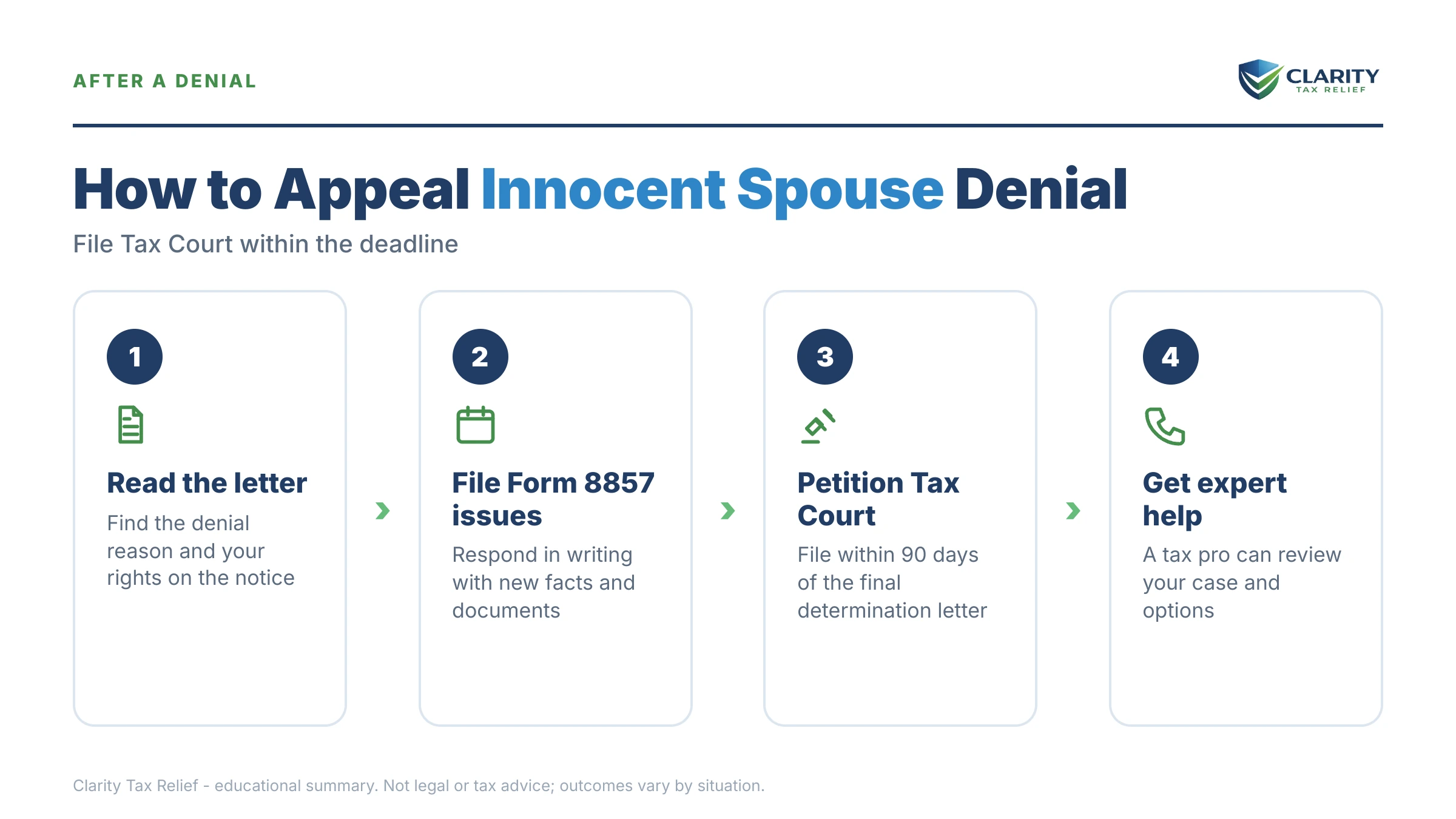

How to respond to an innocent spouse denial, step by step

- Identify your letter — find whether it says preliminary determination or final determination, because the date printed on it starts a 30-day or a 90-day clock.

- Calendar the deadline — 30 days from a preliminary determination to file Form 12509, or 90 days from a final determination to petition the Tax Court, and build in mailing time.

- Decode the denial reasons — list every factor the IRS cited against you (knowledge, benefit, deadline, documentation), because each one needs a specific answer.

- Gather targeted evidence — bank statements showing who controlled the money, proof of separate finances, records of abuse or deception, and anything the original reviewer never saw.

- File the right response — Form 12509 to the Independent Office of Appeals for a preliminary denial, or a petition through the U.S. Tax Court's website for a final determination.

- Line up a fallback — price out a payment plan, hardship status, or an equitable relief request now, so collection can't blindside you if the appeal fails.

Taking an innocent spouse denial to Tax Court: what to expect

The Tax Court is the only forum where someone outside the IRS reviews your innocent spouse denial, and you don't need a lawyer to get in the door. The petition costs $60, the fee can be waived, and cases with $50,000 or less at stake per year can elect the simplified small-case ("S case") procedures with relaxed rules of evidence.

Four things to know before you file:

- The record rule. In equitable relief cases the court generally works from the administrative record you built with the IRS, plus evidence that is newly discovered or was previously unavailable. This is why skipping the Form 12509 stage to "save it for court" backfires — thin record in, thin record out.

- Your ex can join. The non-requesting spouse has a legal right to intervene and argue against your relief. Plan for the possibility that you're litigating against both the IRS and your ex.

- Most cases never see trial. After you file, the case typically routes to IRS Appeals or Chief Counsel for settlement talks. A well-documented petition often gets resolved by concession or compromise months before a trial date.

- Free help exists. If your income is modest, a Low Income Taxpayer Clinic can represent you in Tax Court at no charge — see our guide to the Low Income Taxpayer Clinic program.

Note what the 90-day letter here is not: it's a Section 6015(e) determination, not a notice of deficiency. If you received a CP3219A proposing new tax instead, that's a different 90-day track — see the 90-day letter and Tax Court petition basics.

If the denial sticks: realistic paths by balance

If the appeal fails or the windows have closed, the joint debt is yours to manage, and the right containment strategy tracks the size of the balance:

| Balance you're left holding | Realistic paths | What to know |

|---|---|---|

| Under $10,000 | Pay in full, 180-day short-term plan, or guaranteed installment agreement | Guaranteed IA requires payoff within 3 years; $0 setup fee on the 180-day option |

| $10,000 – $25,000 | Streamlined installment agreement, up to 72 months online | No financial disclosure needed; liens usually avoidable if you stay current |

| $25,000 – $50,000 | Streamlined plan (direct debit typically required above $25k), or OIC if the math works | Direct debit lowers default risk and setup fees |

| Over $50,000 | Full financial disclosure plan, CNC, or offer in compromise | At $66,000+ the IRS can certify your passport for denial; the IRS accepted roughly 1 in 5 offers in FY2024 — an OIC is real but never guaranteed |

When you can handle this yourself — and when help changes the outcome

The 30-day Form 12509 appeal is genuinely DIY-able if your denial turns on one or two factual points and you hold the documents that answer them. Writing a focused disagreement — this factor, this evidence, this conclusion — costs you nothing but time. Likewise, if the balance is small and your facts are honestly weak, setting up a payment plan yourself and moving on is a legitimate, rational choice, not a defeat.

Experienced help tends to change outcomes in four situations: a Tax Court deadline is running and the administrative-record rule means your filing strategy now determines what evidence a judge ever sees; the case involves abuse or financial control, where framing the knowledge factors correctly is the whole case; your ex has hired counsel to intervene; or you're a business owner juggling this alongside payroll or multi-year debt, where sequencing the two tracks wrong gets expensive. If your denial has a 90-day clock on it, get the letter in front of an experienced tax professional this week — a free case review will tell you in one conversation whether the appeal is worth fighting.

Situations that change your appeal

Community property states. In the nine community property states, income your spouse earned may be half "yours" by operation of state law, which changes both the liability math and the relief rules — Section 66 has its own relief provisions, covered in our guide to community property tax relief.

State tax runs on separate rails. Winning or losing with the IRS does not decide your state case. California, for example, has its own innocent spouse program with its own forms and windows through the Franchise Tax Board — see FTB innocent spouse relief. Never assume a federal deadline or threshold applies to a state agency.

Your divorce decree doesn't bind the IRS. A decree ordering your ex to pay the taxes is enforceable against your ex in state court — but the IRS wasn't a party to your divorce and can still collect the joint debt from you. Details in why the IRS ignores the divorce decree.

Wrong form entirely? If your complaint is that your refund was seized for a debt that was never jointly yours — your spouse's child support, student loans, or pre-marriage taxes — you need Form 8379, not an innocent spouse appeal. The distinction is spelled out in injured spouse vs. innocent spouse.

Terms on your denial letter, decoded

- Preliminary determination: the IRS's proposed decision — not final, and appealable within the agency for 30 days.

- Final determination: the IRS's last word administratively; it starts the one-time 90-day Tax Court window.

- Form 12509: the Innocent Spouse Statement of Disagreement — the form that routes your case to the Independent Office of Appeals.

- Actual knowledge vs. reason to know: what you truly knew versus what a reasonable person in your position would have noticed — the factor most denials turn on.

- Non-requesting spouse: the other person on the joint return, who must be notified of your case and may argue against your relief.

- Administrative record: the complete file you built with the IRS — generally the evidence pool a Tax Court judge works from in equitable relief cases.

Innocent spouse denial questions, answered

Why did the IRS deny my innocent spouse relief request?

The most common reasons are that the IRS decided you knew or had reason to know about the understated income, that you significantly benefited from the unpaid tax, or that you missed the two-year deadline for relief under Sections 6015(b) or (c). Thin documentation sinks many requests — the IRS won't take your word for what happened inside your marriage. Your denial letter lists the specific factors it weighed, and that list is the blueprint for your appeal.

Can I appeal an innocent spouse denial?

Yes — twice. If you received a preliminary determination, you have 30 days to request a review by the IRS Independent Office of Appeals using Form 12509. If you received a final determination, you have 90 days to petition the U.S. Tax Court, where a judge — not the IRS — decides your case. Miss both windows and the denial becomes final.

How long do I have to petition the Tax Court after an innocent spouse denial?

90 days from the date the IRS mails your final determination letter, under Section 6015(e). That deadline is set by statute and cannot be extended, and the filing fee is $60 (waivable if you can't afford it). If the IRS has simply sat on your Form 8857 for more than six months without issuing any determination, you can petition the Tax Court without waiting for a letter.

Will the IRS collect from me while my innocent spouse appeal is pending?

Generally no — the IRS is barred from levying you for the joint liability while your Form 8857, your Appeals review, and any timely Tax Court case are pending. But the 10-year collection statute pauses during that same period, so the IRS gets that time back later. Refund offsets can still happen in some situations, so don't treat a pending appeal as complete protection.

Can I reapply for innocent spouse relief after being denied?

You can't simply refile the same request with the same facts — the IRS will deny it as a duplicate. But you can submit new information the original reviewer never saw, and if you were denied under Sections 6015(b) or (c), you may still request equitable relief under Section 6015(f), which uses a broader, more forgiving set of factors and has no two-year deadline.

Will my ex-spouse know I'm appealing?

Yes. The law requires the IRS to notify the other person on the joint return and let them participate at every stage, including intervening in your Tax Court case. If there's a history of abuse, tell the IRS — it will withhold your current address and other personal details, but it cannot keep the existence of the case itself secret.

Does innocent spouse relief cover business or payroll taxes?

No. Innocent spouse relief applies only to income tax from a jointly filed Form 1040. Payroll taxes (Form 941), trust fund recovery penalties, and business entity taxes are outside Section 6015 entirely — if you owe those, they need their own resolution track, such as a payment plan or penalty abatement, regardless of how your innocent spouse case ends.

What happens if I miss the 90-day Tax Court deadline?

The denial becomes final and the IRS can resume collecting the joint debt from you — the notice sequence restarts and levies become possible. You still have moves: you may be able to raise a spouse defense at a Collection Due Process hearing if you get a levy notice, request equitable relief if it was never considered, or shift to collection alternatives like a payment plan, hardship status, or an offer in compromise.

What is the difference between injured spouse and innocent spouse relief?

Innocent spouse relief (Form 8857) removes your responsibility for a joint tax debt caused by your spouse's errors. Injured spouse relief (Form 8379) recovers your share of a refund that was seized for your spouse's separate debt, like back child support or defaulted student loans. If your refund was taken but you don't owe the underlying debt jointly, you likely need the injured spouse form instead.

Your next 24 hours

- Find the determination date on your letter. The date printed near the top starts your 30-day or 90-day clock — write the actual deadline on your calendar today, not "soon."

- Pull the file together. Your denial letter, your original Form 8857 packet, the joint return for the year in question, and any bank or account records showing who controlled the money.

- Get the denial reviewed free before the window closes. Send it through the 2-minute form or call (888) 825-7779 — an experienced tax professional will map your appeal odds and your fallback in one conversation.

For primary sources: the IRS's official overview of the program and its appeal rights is at IRS.gov — Innocent Spouse Relief; petitions are filed through the United States Tax Court; and if IRS delays or process failures are hurting your case, the independent Taxpayer Advocate Service can intervene at no cost.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.