Offer in Compromise

Offer in Compromise Doubt as to Liability: The 2026 Form 656-L Guide

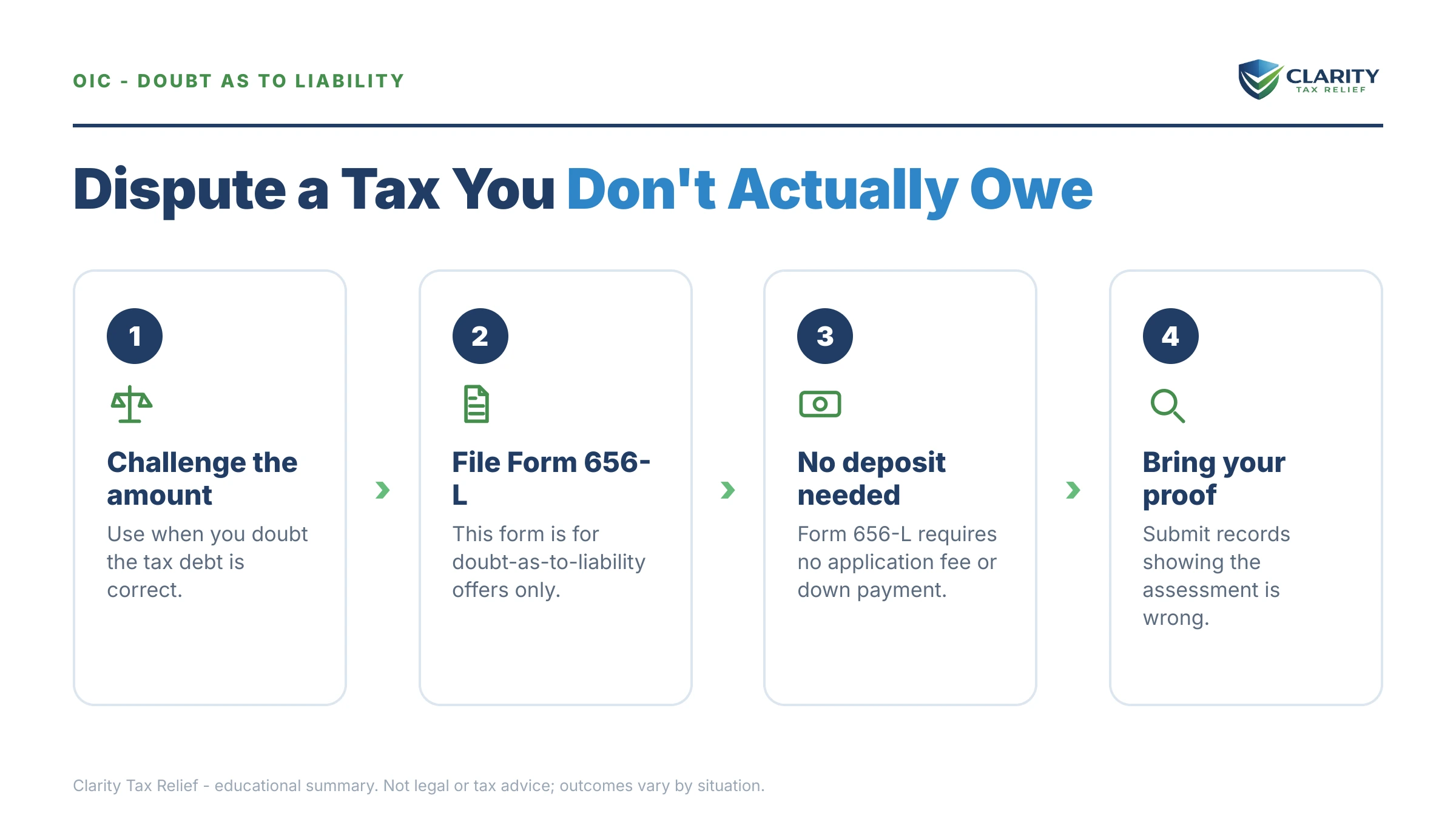

The short answer: an offer in compromise doubt as to liability (Form 656-L) asks the IRS to fix a tax that was wrongly assessed. There is no application fee, no down payment, and no financial disclosure. You offer the amount you actually owe — at least $1 — and prove the original number was wrong.

You've checked the numbers three times, and they still don't add up: the IRS says you owe money for income you never received, an audit you never knew happened, or a penalty for a business you didn't control. Arguing on the phone gets you nowhere, because to the collection system an assessed tax is an owed tax. The offer in compromise doubt as to liability route exists for exactly this — it's the IRS's formal process for saying "the assessment itself is wrong," and it runs on completely different rules than the settlement offers you see advertised.

Three of those rules matter before anything else. Form 656-L carries no application fee, no 20% deposit, and no Form 433 financial statement — because your finances are irrelevant. The only question is whether the tax is correct. The image below shows you exactly what Form 656-L looks like and where the offer amount and your written explanation go, so you can see how short the form itself really is; the work is in the evidence behind it.

⏱ The clocks that matter: there's no filing deadline for a doubt as to liability offer, but two real timers are running. Interest compounds daily on the disputed balance for as long as it stays assessed. And if a CP3219A Notice of Deficiency arrived within the last 90 days, your Tax Court window — a stronger forum — is still open. Check that date before anything else.

Why the IRS says you owe a tax you never actually owed

Most doubt as to liability offers trace back to an assessment the taxpayer never got a real chance to contest. The tax code lets the IRS assess first and hear your side later in several situations, and each one produces the same result: a legally binding balance built on numbers you dispute.

The common paths into this problem:

- A defaulted underreporter case. A CP2000 notice proposed tax on a 1099 mismatch — a wrong amount, a duplicate, or income reported under your SSN that wasn't yours. You moved, never saw it, and the proposal became a final assessment through a defaulted CP3219A Notice of Deficiency. This is the single most common route for 1099 contractors, whose income is reported by other people's bookkeepers.

- A substitute-for-return. You didn't file, so the IRS filed a substitute return for you — with every 1099 counted as pure profit, no business expenses, and the worst filing status. The resulting tax is almost always inflated.

- An audit that concluded without you. You missed the appointment, couldn't find receipts in time, or the mail went to an old address, and the examiner disallowed everything by default.

- A trust fund recovery penalty. The IRS assessed a business's unpaid payroll withholding against you personally as a "responsible person" — and you dispute that you had the authority or the willfulness the trust fund recovery penalty requires.

Notice what's not on that list: "the tax is right but I can't pay it." That's a different program with different math, covered next — and confusing the two is the fastest way to have an offer sent back unread.

Offer in compromise doubt as to liability vs. doubt as to collectibility

Doubt as to liability disputes whether the tax is correct; doubt as to collectibility concedes the tax and disputes whether it can ever be collected. The IRS keeps these on separate forms, separate rules, and separate review teams — and you cannot run both arguments on the same debt at the same time.

A collectibility offer on Form 656 is judged on your Reasonable Collection Potential — the equity in what you own plus a multiple of your monthly ability to pay. If your real problem is that the tax is correct but unpayable, that's the path to study (you can estimate a collectibility-based offer with our Offer in Compromise Calculator), and the mechanics live in our guide to how an offer in compromise actually works. A liability offer ignores your finances entirely.

| Feature | Doubt as to liability (Form 656-L) | Doubt as to collectibility (Form 656) |

|---|---|---|

| What you must prove | The assessed tax is wrong — a genuine dispute over the liability itself | The tax is right, but your assets and income can't cover it |

| Application fee | $0 | $205 (waived with low-income certification) |

| Down payment | None | 20% with a lump-sum offer (waived with low-income certification) |

| Financial disclosure | None — no Form 433 required | Full Form 433-A (OIC) or 433-B (OIC) |

| How the offer amount is set | The correct tax you actually owe — at least $1 | Reasonable Collection Potential (equity + future income) |

| Blocked when | The liability was finally decided by a court, or the same tax is in a pending court case | You can fully pay, or you're not current on filing |

The strategy point most pages miss: these can be run in sequence. Fix the liability first with a 656-L, then — if a correct but unpayable balance remains — pursue collectibility, a payment plan, or hardship status on the real number. Our comparison of cnc vs offer in compromise covers that second decision.

What happens if you do nothing about a wrong assessment

An assessment the IRS's computers consider final is collected exactly like a debt you agreed to — being right does not pause the machine. The sequence runs on autopilot, and each stage strips away options:

- The bill arrives. A CP14 gives you roughly 21 days (10 business days if the balance is $100,000 or more) before the reminder cycle starts, with failure-to-pay penalty and daily-compounding interest already attached to the disputed number.

- Reminders escalate. CP501 and CP503 follow, each adding another month of accruals to a balance you dispute.

- CP504 — intent to levy your state refund. The IRS can now take your state tax refund, and a federal tax lien becomes a live possibility on your credit, contracts, and clients.

- LT11 / Letter 1058 — final notice. A 30-day clock starts on levy action. This notice also carries Collection Due Process rights via Form 12153 and a CDP hearing — and if you never had a prior chance to dispute the tax, a CDP hearing is one of the few other places the liability itself can be raised.

- Enforcement. A bank levy freezes funds for 21 days before they're sent; a levy on your business clients grabs contractor pay; every federal refund you're ever due is offset against the balance. If the debt grows past $66,000 (the 2026 threshold), passport certification enters the picture.

In 2026 there's a cruel asymmetry here: the IRS workforce was cut roughly 27% in 2025, so reaching a human to explain the error is harder than ever — but the notices, liens, and levies are generated automatically and never slowed down. The dispute doesn't get heard unless you file something that legally requires the IRS to hear it.

Assessed for a tax you don't believe you owe?

Send us the notice and your side of the story. An experienced tax professional will check whether a doubt as to liability offer — or a faster, free remedy — fits your facts, before interest builds any further on a number that may be wrong. Free and confidential.

Every way to challenge a tax you don't owe — costs and timelines

A doubt as to liability offer is one of six tools for attacking a wrong assessment, and it's rarely the cheapest or fastest — it's the most formal. Check the free remedies first; a 656-L is strongest when the informal doors have closed or when you need a binding written resolution.

| Option | Out-of-pocket cost | Typical timeline | Best when |

|---|---|---|---|

| Doubt as to liability offer (Form 656-L) | $0 to file | Several months to a year+; deemed accepted if no decision in 2 years | Informal fixes failed, or you want a binding resolution with appeal rights |

| Audit reconsideration | $0 | Months; varies by campus workload | You have new documents the IRS never saw (post-audit, SFR, defaulted CP2000) |

| File your original return (replaces an SFR) | $0 | Months to process | The balance came from a substitute-for-return — this is usually the first move |

| CDP hearing (Form 12153) | $0 | Must request within 30 days of an LT11/Letter 1058 | A final levy notice just arrived and you had no prior chance to dispute the tax |

| Tax Court petition | $60 filing fee | Must file within 90 days of a Notice of Deficiency | The CP3219A window is still open — the strongest prepayment forum there is |

| Pay in full, then claim a refund | The entire assessed balance up front | Often a year or more | You can afford to pay first and want the dispute out of collections entirely |

Which fix fits your situation

The right remedy depends on how the wrong number got assessed, not on how wrong it is. Match your entry point to the tool built for it:

| Your situation | Usually the best first move | Why |

|---|---|---|

| CP2000 assessed by default — you never responded | Audit reconsideration, then Form 656-L if denied | Both reopen the assessment; reconsideration is free and less formal |

| IRS filed a substitute return (SFR) | File your actual original return | The IRS generally adjusts the assessment to your real numbers |

| Audit finished; you've since found the missing records | Audit reconsideration | It exists precisely for new evidence the examiner never saw |

| Reconsideration already denied, dispute still genuine | Doubt as to liability offer | A binding second look, with Appeals rights if rejected |

| Trust fund recovery penalty assessed; you missed the Letter 1153 protest | Doubt as to liability offer | The recognized post-assessment challenge to responsible-person status |

| The tax is correct — you just can't pay it | Collectibility offer, payment plan, or CNC | Liability isn't in doubt; that's a finances question, not an accuracy one |

| CP3219A arrived within the last 90 days | Tax Court petition | A prepayment forum with an independent judge — don't let it lapse |

One boundary case worth naming: if the disputed debt is a business's payroll tax rather than the penalty assessed against you personally, the offer rules change substantially — see our guide to a business offer in compromise payroll situation. And state assessments follow entirely separate programs; California, for example, runs its own FTB offer in compromise with its own forms and standards.

A worked example: $23,800 assessed, roughly $650 actually owed

Say you're a 1099 contractor and a former client's bookkeeper issued a 1099-NEC for $54,000 — the full contract value — when the client actually paid you $12,000 before the project was cancelled. You reported the $12,000. The IRS computer saw a $42,000 gap, mailed a CP2000 to the apartment you'd left, defaulted the case, and assessed. Here's how a hypothetical balance like that gets built:

- Additional income tax on $42,000 of phantom income (22% bracket): $9,240

- Additional self-employment tax: $42,000 × 92.35% × 15.3% ≈ $5,934

- 20% accuracy-related penalty on $15,174 of added tax: $3,035

- Failure-to-pay penalty and compounding interest since assessment: ≈ $5,591

- Total assessed: ≈ $23,800 — on income that never hit your bank account.

Now the doubt as to liability math. Your bank statements and invoices show exactly $12,000 received from that client — already reported. Digging through the year, you find one honest omission: an $1,800 side job you forgot. The correct additional liability is roughly $254 of SE tax plus about $396 of income tax — call it $650.

So the Form 656-L offer is $650: the amount you genuinely owe, documented line by line. You attach the bank statements, the invoices, the cancelled contract, and — ideally — a corrected 1099 from the client. If the IRS agrees the evidence shows the assessment was wrong, accepting the offer corrects the whole $23,800, because the penalties and interest built on the phantom income collapse along with it. Nothing about that outcome is automatic or guaranteed — it rises and falls entirely on the paper trail — but notice what never came up: your income, your savings, what you could afford. In a liability offer, only the truth of the number matters.

How to file an offer in compromise doubt as to liability, step by step

- Rule out a simpler fix first. Check whether audit reconsideration, an original return (for an SFR), a CDP hearing, or a penalty abatement request solves the problem faster and for free.

- Pull your IRS transcripts and records. Order account and wage-and-income transcripts for the disputed years so you can see exactly what was assessed, when, and from which documents.

- Recalculate the correct liability and set your offer. Rebuild the year with your real numbers — bank deposits, invoices, corrected 1099s — and offer that corrected amount, at least $1, on the form.

- Complete Form 656-L with a written statement and evidence. Explain in plain terms why the assessment is wrong, attach every supporting document, and never mention ability to pay — that argument belongs on a different form.

- Mail the package and confirm it's pending. Send it to the address in the current Form 656-L instructions via certified mail, then watch your transcript for code 480 showing the offer is under review.

- Respond to every IRS request and appeal a rejection within 30 days. Missed document requests get offers returned without appeal rights; a rejection can be appealed with Form 13711 inside the 30-day window.

The written statement is where offers are won. Structure it like a story a stranger can follow in five minutes: what the IRS assessed and why, what actually happened, and which attached exhibit proves each point. Vague indignation loses; a numbered exhibit list wins. The form itself — as the image shows — leaves only a small box for your explanation, which is why the statement and exhibits ride along as attachments.

What happens after you file Form 656-L

A pending doubt as to liability offer generally suspends IRS levy action while it's reviewed. On your transcript, that status shows up as code 480 — offer-in-compromise pending. Unlike collectibility offers, liability offers are routed to examination-side reviewers who re-work the tax question itself, so expect requests for specific documents rather than bank statements and pay stubs.

Three things to understand while you wait:

- The collection statute pauses. The 10-year clock stops while the offer is pending (plus 30 days after a rejection). If your offer fails, the IRS gets that time back on the far end — a real cost of filing a weak offer.

- The 2-year rule protects you. By law, an offer the IRS doesn't decide within 2 years of receipt is deemed accepted. With post-2025 staffing levels, that rule has teeth.

- Returned is worse than rejected. A returned offer (missing signature, unanswered document request, ability-to-pay arguments on the wrong form) carries no appeal rights. A rejected offer can go to the Independent Office of Appeals — see appealing an OIC rejection (Form 13711) — where officers weigh the hazards of litigation and frequently split the difference on well-documented files.

- Acceptance ends it. You pay the offered amount, the assessment is corrected, and the erroneous penalties and interest fall away with the tax they were built on.

If a levy notice lands while you're still assembling your package, don't wait to finish it — get the file reviewed now or call (888) 825-7779, because the pending-offer collection hold only protects you once the offer is actually in the IRS's hands.

When you can handle a doubt as to liability offer yourself

Plenty of 656-L cases are genuinely DIY-able, because the form is free and the IRS is required to consider it. You can reasonably self-file when the dispute is a single year, the proof is clean and third-party (a corrected 1099, bank statements, a canceled contract), and you can write a clear two-page timeline connecting each document to each wrong number. The worked example above is exactly that kind of case.

Experienced help changes outcomes in a narrower set of situations: trust fund recovery penalty disputes, where "responsible person" and "willfulness" are legal arguments the IRS litigates hard; income that has to be reconstructed rather than simply documented (cash-heavy years, missing records, bank-deposit analysis); multiple assessed years with different procedural histories; an offer already rejected and headed to Appeals; or a levy already in motion, where sequencing the collection hold matters as much as the merits. In those cases the question isn't filling out the form — it's building a file an Appeals officer can say yes to.

Terms on Form 656-L, decoded

- Assessment — the formal recording of a tax debt on the IRS's books; once assessed, the collection machinery treats it as owed regardless of accuracy.

- Doubt as to liability — a genuine dispute over whether the assessed tax is correct, the legal basis for a Form 656-L offer under IRC §7122.

- Doubt as to collectibility — the other offer basis: the tax is right, but your assets and income can't cover it before the collection statute runs out.

- Deemed acceptance — the rule that an offer the IRS fails to decide within 2 years is automatically accepted.

- Transaction code 480 — the transcript entry showing your offer is pending and the account is flagged accordingly.

- Audit reconsideration — the free, informal process for reopening an assessment when you have evidence the IRS never considered; the main alternative to a 656-L.

Offer in compromise doubt as to liability: your questions, answered

What is an offer in compromise based on doubt as to liability?

It's an offer that asks the IRS to correct a tax that was wrongly assessed, filed on Form 656-L. Instead of proving you can't pay, you prove the underlying liability is wrong — and you offer the amount you believe you actually owe, supported by documents. If the IRS agrees the assessment is incorrect, it accepts your offer and adjusts the balance, including the penalties and interest built on the erroneous tax.

Does Form 656-L have an application fee or down payment?

No. A doubt as to liability offer requires no application fee, no initial payment, and no monthly payments while the IRS reviews it. That's different from a doubt as to collectibility offer on Form 656, which carries a $205 fee and a 20% down payment on lump-sum offers unless you meet the low-income certification. You also don't file a financial statement with Form 656-L.

How much should I offer on a doubt as to liability offer?

Offer the amount you believe is the correct tax for the disputed years — it must be more than $0, so at least $1 even if you think you owe nothing. Don't discount for what you can afford; ability to pay is irrelevant in a liability offer and raising it can get the offer sent back. Tie the number directly to your recalculation and evidence.

Can I file doubt as to liability and doubt as to collectibility at the same time?

No — the IRS won't consider both offer types on the same tax debt at the same time. You choose the argument that fits: liability if the assessment itself is wrong, collectibility if the tax is correct but your assets and income can't cover it. Many people resolve the liability question first, then pursue a collectibility offer or payment plan on whatever balance genuinely remains.

Does a doubt as to liability offer stop IRS collection?

Generally yes — the IRS suspends levy action while an offer in compromise is pending, and for 30 days after a rejection while you can appeal. Know the trade-off: the 10-year collection statute is paused during that same period, so a pending offer extends the IRS's time to collect if the offer fails. Refund offsets and an already-filed lien can still remain in place.

How long does a doubt as to liability offer take?

Expect several months to a year or more, depending on how complex the dispute is and IRS staffing — reviews have slowed since the 2025 workforce cuts. By law, if the IRS doesn't make a decision within 2 years of receiving your offer, it's deemed accepted. Track its status through transcript code 480, which posts when the offer is officially pending.

What happens if my doubt as to liability offer is rejected?

You have 30 days from the rejection letter to appeal to the IRS Independent Office of Appeals, typically using Form 13711. Appeals officers settle cases based on the hazards of litigation, so a well-documented file often does better there. If the appeal fails, alternatives like audit reconsideration, paying and filing a refund claim, or resolving the balance through a payment plan remain available.

Can I use doubt as to liability for the trust fund recovery penalty?

Yes — Form 656-L is a recognized way to contest a trust fund recovery penalty after it's been assessed, arguing you weren't a responsible person or didn't willfully fail to pay. It's often the last practical door for someone who missed the 60-day window to protest Letter 1153. Expect the IRS to scrutinize check-signing authority, titles, and who actually controlled payments.

Should I use audit reconsideration instead of a doubt as to liability offer?

Often, yes — audit reconsideration is free, less formal, and works well when you have new documents the IRS never saw, especially after a substitute-for-return or a defaulted audit. A liability offer is the better tool when reconsideration already failed, when you want a binding written resolution, or when the dispute turns on judgment calls rather than missing paperwork.

Your next 24 hours

- Find the source of the assessment. Pull the notice (or your account transcript) and write down the tax year, the assessed amount, and how it was created — CP2000 default, substitute return, audit, or trust fund penalty. That one fact decides which remedy fits.

- Gather the proof. Bank statements for the disputed year, invoices or contracts, the 1099s involved (and a corrected one if you can get it), and the return you actually filed. Your case is only as strong as this stack.

- Get a free case review. Use the 2-minute form or call (888) 825-7779. An experienced tax professional will confirm whether a doubt as to liability offer or a faster free remedy fits your facts — while interest is still compounding on a number that may simply be wrong.

Primary sources: the IRS's official pages for Form 656-L, Offer in Compromise (Doubt as to Liability) and the Offer in Compromise program. If the IRS system itself is causing hardship or delay in your case, the Taxpayer Advocate Service is an independent avenue for help.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.