Offer in Compromise

Doubt as to Collectibility: The Offer in Compromise Ground Explained (2026)

The short answer: doubt as to collectibility is the legal ground behind most IRS offers in compromise. It means your assets plus your future income — what the IRS calls your reasonable collection potential — add up to less than your full tax debt, so the IRS may accept a smaller amount because it could never collect more.

You've run your Schedule C numbers twice and the answer doesn't change: the balance the IRS says you owe isn't in the bank, and this year's receipts won't put it there. That gap between what you owe and what you could ever actually pay has a formal name in tax law — and it's the argument the IRS is legally allowed to accept. Here's exactly how the math works and how to make it.

Doubt as to collectibility (DATC) is one of three grounds you can select on Form 656, and it's the one used in the vast majority of offers. Further down, the image below shows you exactly what the offer paperwork looks like and where the doubt-as-to-collectibility election sits, so you can see what you'd actually be signing.

⏱ The clock that matters: there is no filing deadline for a doubt as to collectibility offer — but while you decide, the 0.5% monthly failure-to-pay penalty and daily-compounding interest keep growing the balance. One clock does run in your favor: once the IRS receives a processable offer, it is deemed accepted by law if the IRS doesn't decide within 2 years — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count.

What doubt as to collectibility actually means

Doubt as to collectibility exists when your reasonable collection potential — asset equity plus future income — is less than your full tax balance. It is not a hardship plea and not a negotiation. It's arithmetic: if the IRS's own formula says it can only ever collect $2,260 of a $6,200 debt, accepting $2,260 is a rational deal for the government.

That's what separates DATC from its two siblings on the offer menu. If you're arguing the debt itself is wrong — a bad audit, a substitute return, tax that isn't yours — that's an offer in compromise based on doubt as to liability, filed on a different form (656-L) with no application fee. If you could technically pay but doing so would create exceptional unfairness or hardship, that's an effective tax administration offer. DATC is for the situation most people are actually in: the number is right, and it's simply bigger than your life can produce.

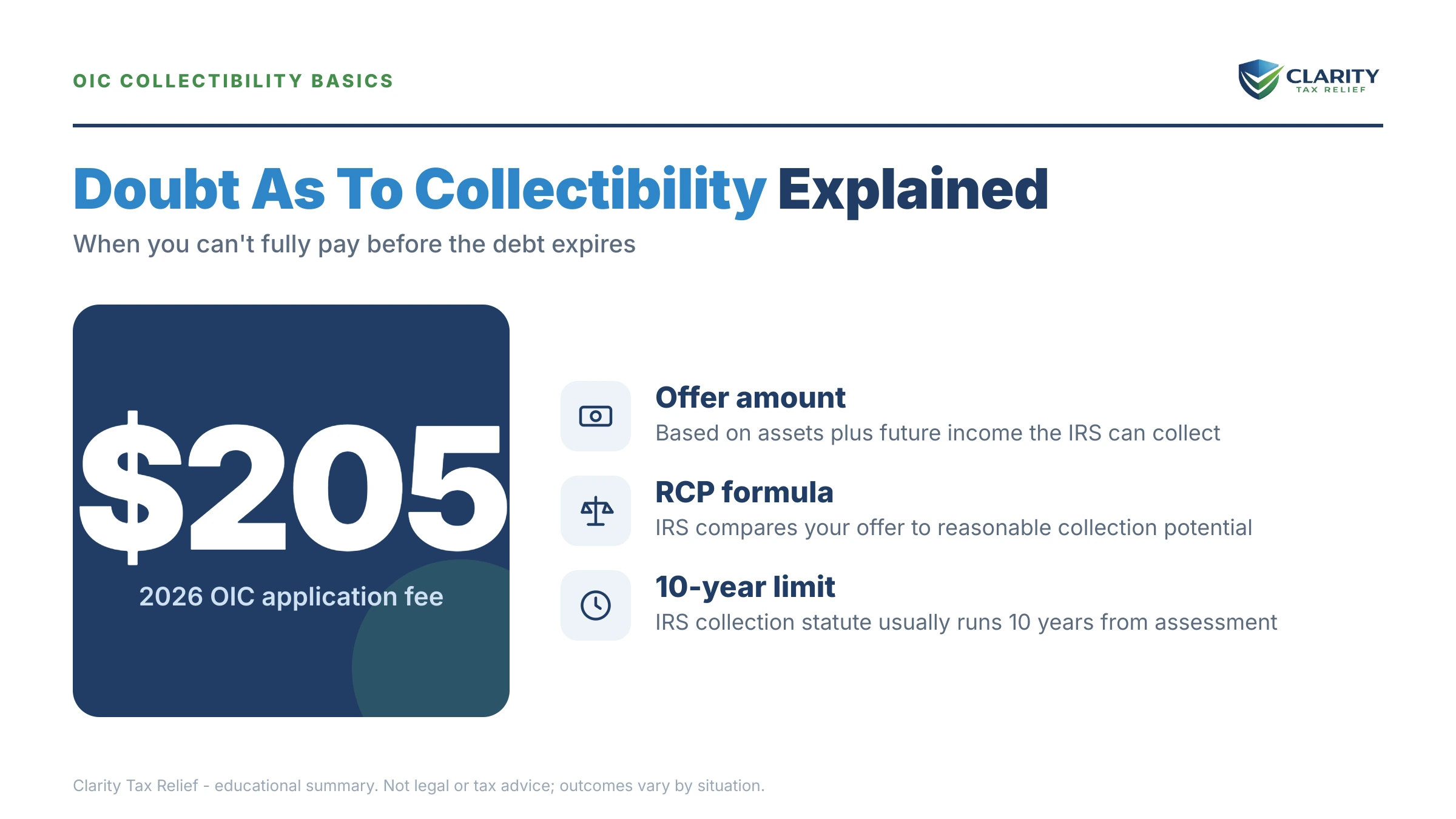

One honest calibration before the math: the IRS accepted roughly 1 in 5 offers in FY2024. Most rejections happen because the taxpayer's numbers don't survive the formula below — which is why you run it before you spend $205 finding out. Current-year figures and what they mean are in our offer in compromise acceptance rate 2026 breakdown, and the full program mechanics live in our guide to how an offer in compromise works.

How the IRS measures collectibility: the RCP formula

The IRS measures doubt as to collectibility with one formula — reasonable collection potential: net asset equity at quick-sale value, plus your monthly disposable income multiplied by 12 months for lump-sum offers or 24 months for periodic offers.

Each half has its own rules:

- Asset equity. The IRS values most assets at "quick-sale" value — typically 80% of market value — minus any loans against them. Small exclusions apply, like the first $1,000 in bank accounts, and equipment you genuinely need to earn a living is often excluded or heavily discounted.

- Future income. Your income minus IRS allowable living expenses — national and local standards, not your actual budget. Whatever's left is your monthly disposable income. The multiplier (12 or 24) is why lump-sum offers usually come out cheaper; the moving parts are covered in our guide to how the IRS calculates your future income for an offer.

If RCP comes out below your balance, doubt as to collectibility exists and an offer at your RCP fits the government's own math. If RCP comes out at or above the balance, the IRS will conclude you can full-pay and reject the offer. You can estimate your own number in a few minutes with our Offer in Compromise Calculator — it estimates, it doesn't decide, but it tells you whether this path is worth pursuing before any fee is paid.

A worked example: $6,200 owed, self-employed

Say you owe $6,200 in self-employment tax from a down year as a sole-proprietor handyman, and business hasn't recovered. Your net self-employment income now averages $3,850 a month, and the IRS allowable living expense standards for your household come to $3,690. Disposable income: $160 a month.

Now the assets. Checking account: $1,340, minus the $1,000 exclusion = $340 counted. Work van: worth $9,500 with an $8,200 loan — quick-sale value is 80% ($7,600), minus the loan = $0 equity. Tools you use daily to earn income: excluded. So:

- Lump-sum RCP: $340 + ($160 × 12) = $340 + $1,920 = $2,260

- Periodic RCP: $340 + ($160 × 24) = $340 + $3,840 = $4,180

Because $2,260 is less than $6,200, doubt as to collectibility exists, and a lump-sum offer around $2,260 matches the formula. Filing it costs the $205 application fee plus 20% down — $452 here, which is applied to your debt whether or not the offer is accepted (see is the OIC down payment refundable before you send it). If your AGI falls at or below 250% of the federal poverty level for your household size, the OIC low-income certification waives the fee, the down payment, and payments during review entirely.

The reality check: at this income level, the offer examiner will average several months of your gross receipts, pull bank statements, and probe whether $3,850 is your real run rate or a temporary dip. Self-employed offers get more scrutiny than W-2 offers — the specific traps are in our guide to the OIC for the self-employed. This example is hypothetical, and your numbers will differ; the formula won't.

What happens to the balance if you do nothing

An unpaid IRS balance moves through an automated notice sequence that ends in levies — whether or not a human ever reviews your file. In 2026, with the IRS workforce down roughly 27%, humans are harder to reach than ever, but the notice machine never stopped. The stages, in order:

- CP14 — the first bill for the balance, penalties, and interest.

- CP501 / CP503 — reminders. Still just bills, but the 0.5% monthly penalty and interest are compounding.

- CP504 — intent to levy your state tax refund; a federal tax lien becomes a live possibility.

- LT11 / Letter 1058 — final notice of intent to levy, starting a 30-day clock and your Collection Due Process rights.

- Levy. Bank accounts (funds are held 21 days before they leave), and — this is the part that stings for a sole proprietor — levies mailed directly to your 1099 clients, ordering them to send your invoiced payments to the IRS instead of you.

That client-levy stage is why self-employed taxpayers shouldn't ride the sequence out. There's no employer to garnish, so the IRS goes to your bank and your customers — and a levy notice landing on a client's desk can cost you the relationship, not just the check. A pending, processable offer generally suspends levy action while the IRS reviews it, which is one of the quieter benefits of filing.

Self-employed with a balance the math says you can't pay?

Before you spend $205 finding out, have an experienced tax professional run the same RCP math the IRS will — and tell you honestly whether doubt as to collectibility, a payment plan, or hardship status fits your numbers. Free, confidential, no pressure — and every month of waiting adds penalties and interest.

DATC offer vs. your other options: costs and timelines

A doubt as to collectibility offer costs $205 up front and typically takes many months to resolve; a payment plan can be set up in an afternoon. Which trade-off makes sense depends on how far your RCP sits below your balance:

| Path | Upfront cost | Typical timeline | Keep in mind |

|---|---|---|---|

| DATC offer in compromise | $205 fee + 20% down (both waived with low-income certification) | Commonly 6–12+ months; deemed accepted if no decision in 2 years, with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count | CSED pauses during review; 5 years of perfect compliance required after acceptance |

| Doubt as to liability offer (Form 656-L) | No application fee | Several months | Argues the debt is wrong, not unpayable — no financial disclosure |

| Installment agreement | Setup fee varies by method; reduced or waived for low income | Set up online same day; up to 72 months (balances ≤ $50,000) | Full balance paid over time; interest and penalties continue |

| Currently not collectible | $0 | Weeks to establish; reviewed as income changes | Pauses collection but the debt and interest remain; CSED keeps running |

| Short-term full pay | $0 setup | Up to 180 days | Cheapest exit if the money is realistically reachable |

Notice the strategic tension in that table: an offer pauses the 10-year collection statute while it's pending, so a failed offer hands the IRS extra time to collect. Currently-not-collectible status does the opposite — the clock keeps running toward expiration. When RCP is close to your balance, that difference can matter more than the offer itself.

How much you owe changes the calculus

The smaller your balance, the harder a doubt as to collectibility offer has to work to beat a simple payment plan. Here's how the realistic paths shift by amount band:

| Balance owed | Realistic paths | DATC offer reality check |

|---|---|---|

| Under $10,000 | Guaranteed installment agreement; 180-day full pay; CNC if genuine hardship | Only worth pursuing when RCP is far below the balance and income won't recover — otherwise the fee and 6–12 month wait beat nothing |

| $10,000–$25,000 | Streamlined plan; CNC; DATC offer | Viable when disposable income is near zero and assets are thin |

| $25,000–$50,000 | Streamlined plan (direct debit at the top of the band); DATC offer | The offer-vs-plan math starts genuinely favoring offers for low-RCP taxpayers |

| Over $50,000 | Financial-disclosure installment agreement; partial-pay plan; DATC offer | This is where most accepted DATC offers live — full disclosure is required either way, so the offer costs little extra effort |

In our $6,200 example, that first row is the honest tension: a guaranteed installment agreement at roughly $86–$100 a month would also stop enforcement, with no fee and no financial disclosure. The offer wins only because $2,260 once beats roughly $7,000+ paid over six years with accruing interest — and only if the low income is real and durable. That's exactly the judgment call worth getting a second opinion on.

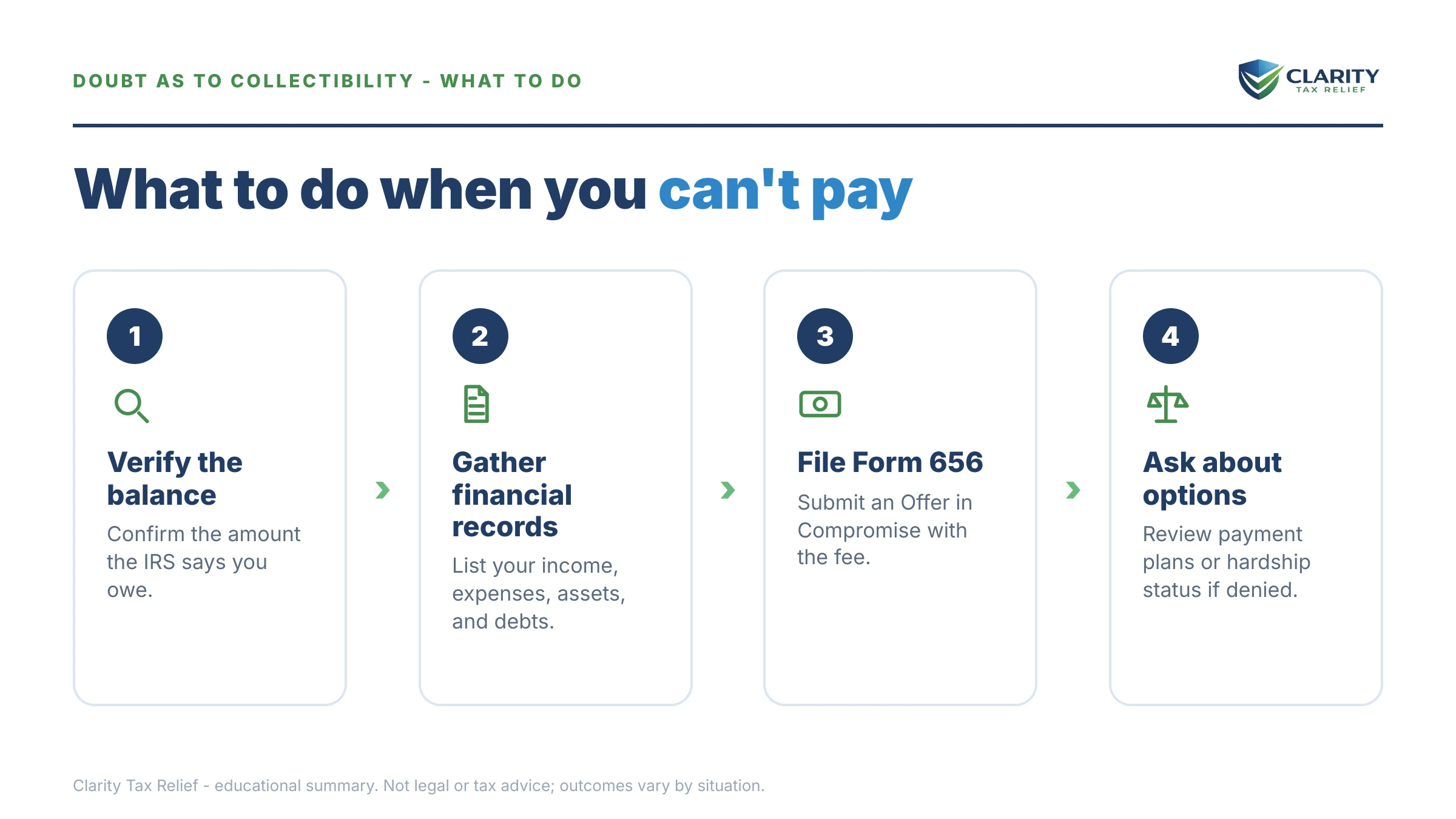

How to build a doubt as to collectibility offer, step by step

- Get compliant first. File every required return and get current on this year's estimated tax payments — the IRS returns offers from non-compliant taxpayers without reviewing them.

- Run your RCP math. Add net asset equity at quick-sale value to 12 (lump-sum) or 24 (periodic) months of disposable income, using IRS allowable expense standards.

- Choose your payment terms. Pick lump-sum (5 or fewer payments, 12-month multiplier) or periodic (monthly payments, 24-month multiplier) — lump-sum usually produces the lower offer.

- Complete the paperwork. Fill out Form 433-A's OIC version with three months of documentation, then check "Doubt as to Collectibility" on Form 656 and state your offer amount.

- Submit with payment. Mail the package with the $205 fee and 20% down (lump-sum) or your first monthly payment (periodic) — or the low-income certification that waives both.

- Stay compliant while it's pending. Keep filing, keep making estimated payments, and answer every IRS document request quickly — non-compliance during review gets the offer returned.

If the IRS says no, you're not done: you generally have 30 days to appeal the rejection with Form 13711, and Appeals reverses examiner math more often than people expect. And remember the back end of acceptance: five years of on-time filing and paying afterward, or the compromised debt comes back in full.

When you can handle this yourself — and when help changes the outcome

You do not need professional help to set up a payment plan on a balance you agree with — and if your RCP comes out above your debt, that plan is your answer, and anyone selling you an offer anyway is selling you a rejection. You can also reasonably DIY a DATC offer when your finances are simple: steady W-2 income, no business, no real assets, and a pre-qualifier result that clearly favors you.

Experienced help changes outcomes in the situations offer examiners push back hardest on: self-employed income that has to be averaged and defended month by month, business assets and tools that need to be valued (or excluded) correctly, recently spent or transferred assets the IRS may add back into your RCP as "dissipated," multiple tax years stacked together, or an offer that's already been rejected once. In those cases the difference between an accepted offer and a rejected one is usually how the 433-A (OIC) is built — not the form itself.

Whatever you decide, verify everything against the primary sources: the IRS's own Offer in Compromise page, its OIC Pre-Qualifier tool, and — if your case stalls or the IRS mishandles it — the Taxpayer Advocate Service.

Terms on the offer paperwork, decoded

- Reasonable collection potential (RCP): the IRS's calculation of the most it could ever collect from you — asset equity plus 12 or 24 months of disposable income. Your offer competes against this number.

- Quick-sale value: what an asset would fetch in a fast sale — typically 80% of fair market value — used instead of full value when counting your equity.

- Allowable living expenses: the national and local expense standards the IRS uses in place of your actual budget when computing disposable income.

- Monthly disposable income: your income minus allowable expenses — the figure that gets multiplied by 12 or 24 in the RCP formula.

- Dissipated assets: money or property you spent or transferred while the debt existed that the IRS may add back into your RCP as if you still had it.

- CSED: the collection statute expiration date — 10 years from assessment, paused while an offer is pending.

Doubt as to collectibility: your questions answered

What does doubt as to collectibility mean on Form 656?

It's the checkbox that tells the IRS you can't pay your full tax debt before the collection statute runs out. Checking it means you're asking the IRS to accept your reasonable collection potential — net asset equity plus 12 or 24 months of disposable income — instead of the full balance. It's the ground behind the vast majority of offers, and it requires full financial disclosure on Form 433-A (OIC).

How does the IRS decide how much I can pay?

Through a formula called reasonable collection potential: the quick-sale value of your assets minus what you owe on them, plus your monthly disposable income multiplied by 12 for lump-sum offers or 24 for periodic offers. Disposable income is your actual income minus IRS allowable living expense standards — not your real budget. If your RCP is less than your debt, doubt as to collectibility exists.

What is the difference between doubt as to collectibility and doubt as to liability?

Doubt as to collectibility says the debt is correct but you can't pay it; doubt as to liability says the debt itself is wrong. They use different forms — Form 656 for collectibility, Form 656-L for liability — and a liability offer has no application fee. You can't argue both in the same offer, so pick the ground that matches your real dispute.

How much should I offer in a doubt as to collectibility offer?

Offer your reasonable collection potential — no less, and usually no more. Offers below the RCP the IRS calculates get rejected, and offering meaningfully more than RCP wastes money. Run the math first: asset equity at quick-sale value plus 12 months of disposable income for a lump-sum offer. If your number comes out at or above your full balance, an offer isn't your path — a payment plan is.

Does filing a doubt as to collectibility offer stop IRS collection?

Generally yes — the IRS typically suspends levy action while a processable offer is pending, plus 30 days after any rejection and during a timely appeal. But two things keep running: interest continues to accrue on the balance, and the 10-year collection statute pauses while the offer is under review, giving the IRS more time to collect if the offer fails.

Can I qualify for a doubt as to collectibility offer if I'm self-employed?

Yes — self-employed taxpayers file the same Form 656 with Form 433-A (OIC), which has dedicated sections for business income and expenses. Expect closer scrutiny: the IRS averages several months of gross receipts, questions dips in income, and requires you to be current on this year's estimated tax payments before it will even process the offer.

What happens if my doubt as to collectibility offer is rejected?

You have 30 days from the rejection letter to appeal using Form 13711, which sends the case to the IRS Independent Office of Appeals — a fresh set of eyes that regularly reverses examiner math. You can also fix the problem the examiner cited and reapply, or pivot to an installment agreement or currently-not-collectible status. Payments already made are kept and applied to your debt.

Your next 24 hours

- Pull your real balance. Log into your IRS online account and note the total across every tax year — penalties and interest included. Your offer must cover all of it, and the RCP math starts from that number.

- Gather the RCP inputs. Your last filed return, three months of bank statements, current business income and expense figures, and loan balances on your vehicle and any other assets.

- Get the math checked before you pay to file. Send your numbers through the form at the free case review or call (888) 825-7779 — an experienced tax professional will tell you whether doubt as to collectibility fits your finances or whether a cheaper path gets you out faster, while penalties and interest are still small.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.