Offer in Compromise

OIC Rejected — Now What? Your Appeal, Deadline, and Next Steps (2026)

OIC rejected — now what? You have 30 days from the date on your rejection letter to appeal using Form 13711, and that's usually your strongest move in 2026. You can also submit a new offer, set up a payment plan, or request hardship status. Your deposit and fee stay applied to your balance.

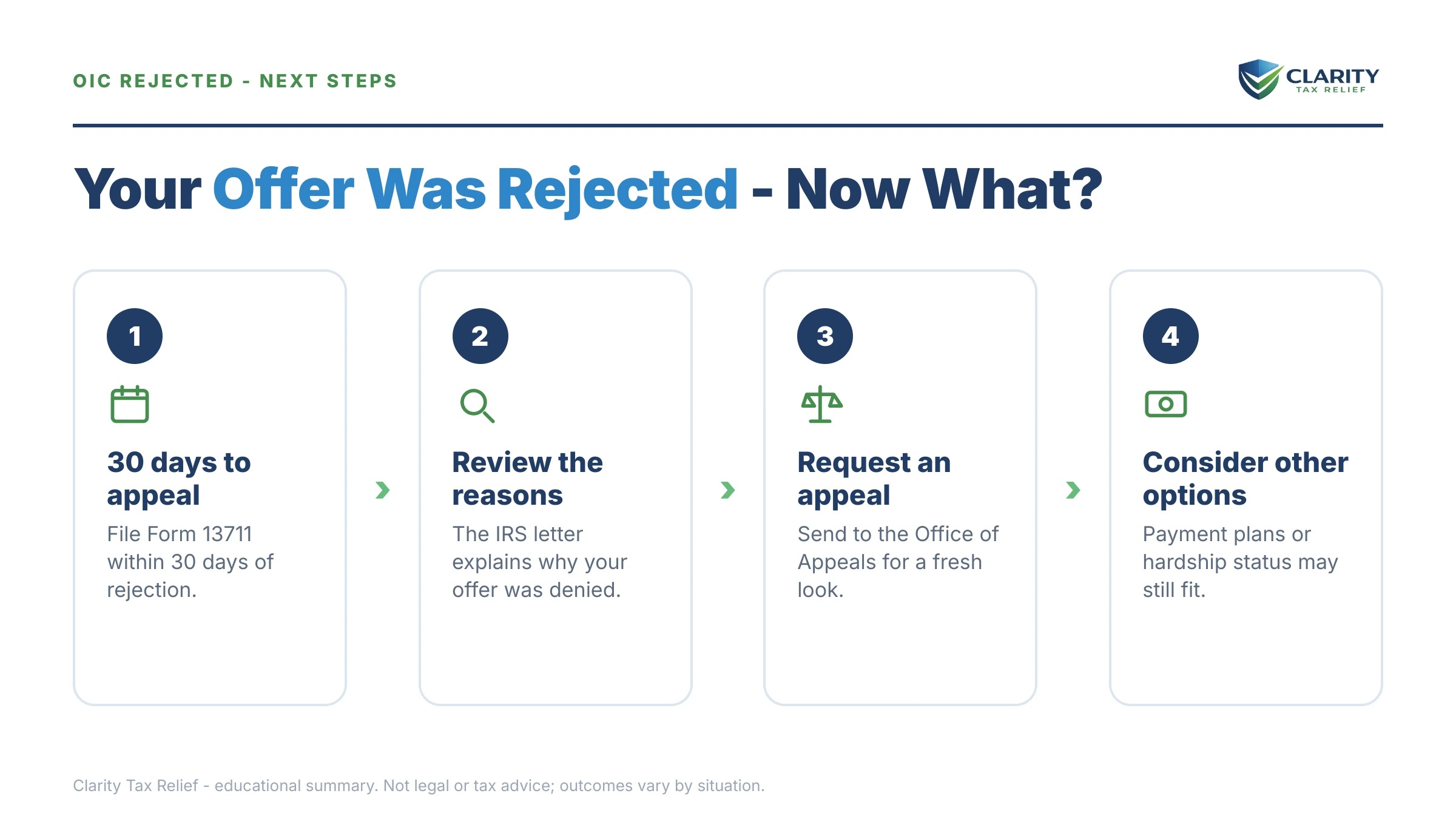

You opened the letter expecting relief and instead read the word "rejected." Your Offer in Compromise was reviewed and turned down — but this is not the end of the road, and it is not even close to the last word. A rejection comes with a clean, well-worn set of next steps, and the most important one runs on a clock.

Here is the fact most people miss: an OIC rejection is appealable, and the appeal is often where offers finally get accepted. The rejection letter you're holding shows two things that control everything you do next — the reason the IRS gave, and a date. The image below shows exactly what this letter looks like and where to find both.

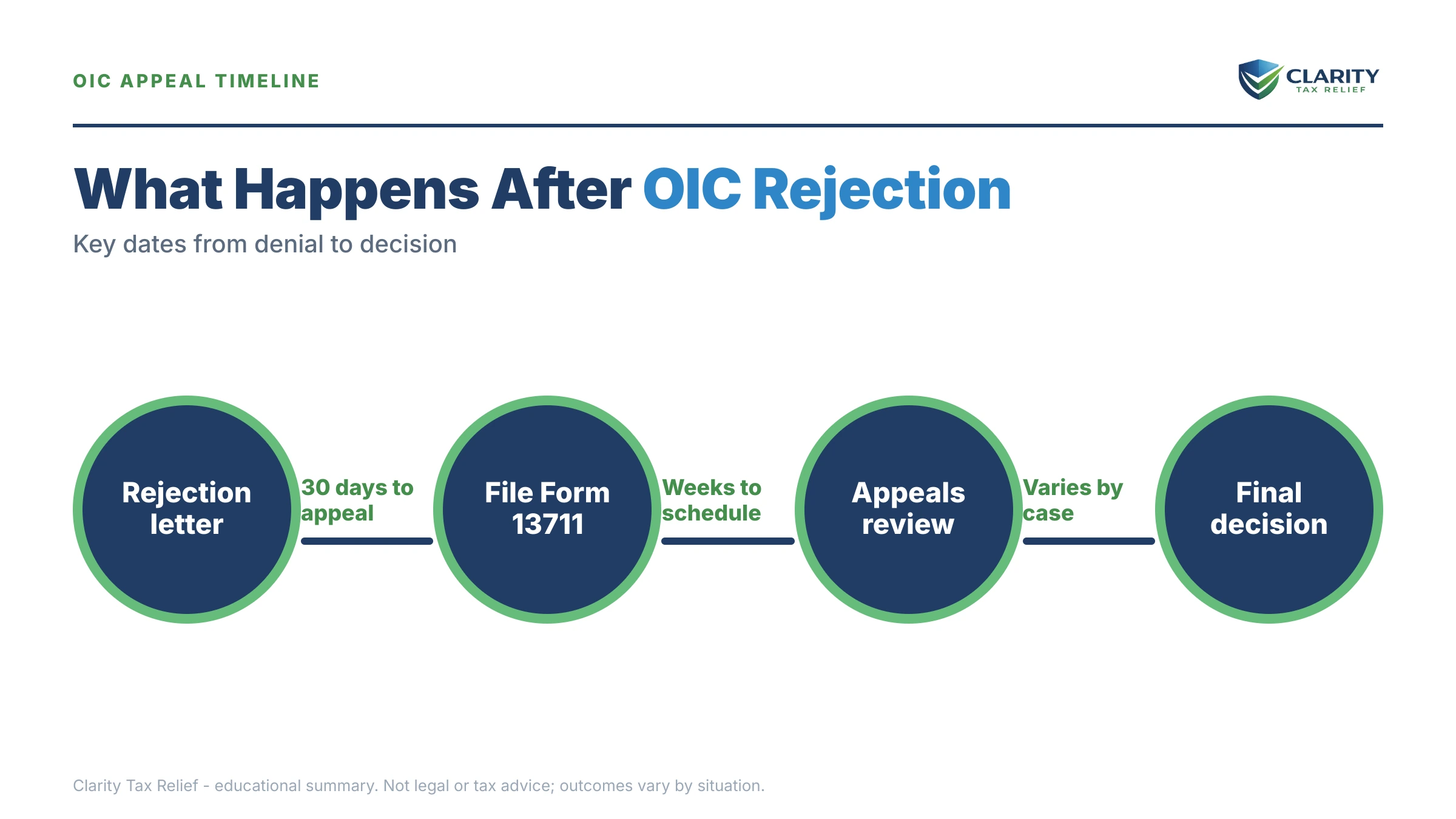

⏱ Your deadline: you have 30 days from the date printed on your OIC rejection letter to file Form 13711 and preserve your appeal rights. That's the date on the letter — not the day it arrived — so open the envelope and note it now.

Why your OIC was rejected

The single most common reason the IRS rejects an offer is that your offer was less than your Reasonable Collection Potential (RCP) — the total the IRS believes it can collect from your assets plus your future income over the collection window. If the number you offered comes in below the IRS's RCP math, the offer examiner is required to reject it. (For the full walkthrough of how an offer is supposed to work, see our hub guide on how an offer in compromise actually works.)

Your rejection letter names the reason. In practice, rejections cluster into a handful of causes:

- Offer below RCP — the headline reason. The IRS valued your equity or future income higher than you did.

- Asset equity understated — a vehicle, retirement account, home, or business interest the IRS valued differently. Learn how the number is built in our guide to reasonable collection potential.

- Disposable income miscalculated — the IRS allowed fewer living expenses than you claimed, pushing monthly disposable income up.

- Dissipated assets added back — money or property you spent before or during the offer that the IRS counts as still collectible. See dissipated assets oic.

- Compliance gap — a missing return or unpaid estimated payment. This often gets an offer returned rather than rejected (more on that difference below).

Rejection is common, not a personal failure. The IRS accepted roughly 1 in 5 offers in FY2024 — see the current numbers in our breakdown of the IRS offer in compromise acceptance rate and what's shifting in the offer in compromise acceptance rate 2026.

Rejected vs. returned: they are not the same

A rejected offer was evaluated and denied — and it carries formal appeal rights. A returned offer was never fully reviewed, usually because you had an unfiled return, a missing estimated payment, an open bankruptcy, or you didn't respond to a request for information. A return has no appeal rights.

The distinction matters because the fix is different. If your offer was returned, you cannot file Form 13711 — instead you cure the problem (file the return, make the payment) and resubmit a fresh offer. If it was rejected, the 30-day appeal clock is live and you should use it. Check the letter's language and your transcript: code 481 transcript confirms a rejection posted to your account.

What happens if you do nothing

If you let the 30-day window pass without appealing or choosing another path, the IRS collection machine restarts where it left off. Collection was paused while your offer was pending and during the appeal window; once that protection lapses, the automated sequence resumes — and interest and the failure-to-pay penalty never stopped accruing in the first place.

- Rejection letter — your 30-day appeal clock starts. Collection hold still in place.

- Appeal window closes — no timely Form 13711 means the collection hold lifts.

- Reminder / balance-due notices — the IRS re-bills the full balance plus accrued penalties and interest.

- CP504 — Notice of Intent to Levy — the IRS can move to seize your state tax refund. Read the CP504 guide.

- LT11 / Letter 1058 — Final Notice — a 30-day clock plus Collection Due Process rights, then wage and bank levies become possible. See the LT11 guide.

In 2026, this sequence runs on autopilot. IRS headcount fell sharply in 2025, but the notices, liens, and levies are generated by automated systems — the machine keeps escalating whether or not a human ever reopens your file. Acting inside the 30 days is how you stay in front of it.

OIC rejected? Don't let the 30-day appeal window close.

Send us your rejection letter. An experienced tax professional will read the IRS's reason, check whether the RCP math is wrong, and tell you whether to appeal with Form 13711 or reapply — free, confidential, no pressure.

Your options after an OIC rejection

You have four realistic paths after a rejection, and the right one depends on why you were rejected. The table below lays out what each costs, how long it takes, and when it fits.

| Option | Cost | Timeline | Best when |

|---|---|---|---|

| Appeal (Form 13711) | No new fee | Weeks to months in Appeals | The IRS got a value or income number wrong |

| New offer (Form 656) | $205 fee + 20% down (waived if low-income) | Several months for a fresh review | Your first number was too low, or finances changed |

| Installment agreement | $0–$130 setup (waived/reduced if low-income) | Often approved online same day | You can pay over time but not in full |

| Currently Not Collectible | No fee | Set up once financials are verified | Paying anything now creates genuine hardship |

A few notes that change the decision:

- Appeal costs nothing extra and often improves the result — the Form 13711 OIC appeal goes to the Independent Office of Appeals, which can weigh "hazards of litigation" the offer examiner cannot.

- A new offer makes sense when your original number was genuinely too low. Read oic rejected can i reapply before you refile, and how to get oic accepted to avoid a second rejection.

- An installment agreement stops the escalation immediately — a streamlined installment agreement covers balances under $50,000 without detailed financials. You can even move to one while keeping an OIC in play later.

- Currently Not Collectible pauses collection entirely when you can't pay. Compare the two in cnc vs offer in compromise.

Should you appeal or reapply?

Appeal when the rejection came from a disagreement — an inflated asset value, disposable income calculated too high, or dissipated assets added back unfairly. Those are arguable, and Appeals is where you argue them, at no extra cost. Reapply when the rejection was simply correct — your offer was below RCP and there's no realistic argument the number was wrong.

Before you decide, estimate your own number with our Offer in Compromise Calculator. If your honest RCP lands near what the IRS said, appealing the same number wastes 30 days — a new, better-supported offer is the move. If your RCP is genuinely lower than the IRS's figure, that gap is exactly what the appeal is for.

Worked example: a rejected $7,400 offer

Here's a clearly hypothetical case to show the math. Say you're a 1099 contractor who owes $7,400 in back taxes and offered the IRS a $1,500 lump sum. The IRS rejected it and the letter cites "offer less than Reasonable Collection Potential."

Working backward from the letter, the IRS built your RCP like this:

- Equity in your work truck: quick-sale value $9,000 − loan balance $5,000 = $4,000

- Bank + tools: $800

- Future income: $150/month disposable × 12 (lump-sum multiplier) = $1,800

- Total RCP: $4,000 + $800 + $1,800 = $6,600

Your $1,500 offer sat far below the IRS's $6,600 RCP, so it had to be rejected. Now you have two smart moves. If the truck's true quick-sale value is closer to $6,000 (making equity $1,000, not $4,000), that's a $3,000 valuation error worth appealing — a corrected RCP of about $3,600 changes the whole picture. If the IRS's numbers are right, a new offer near $6,600 has a real shot, while $6,600 spread over a 72-month installment agreement is roughly $103/month before interest. Meanwhile, your original 20% deposit isn't gone — it already reduced the $7,400 balance.

How to respond, step by step

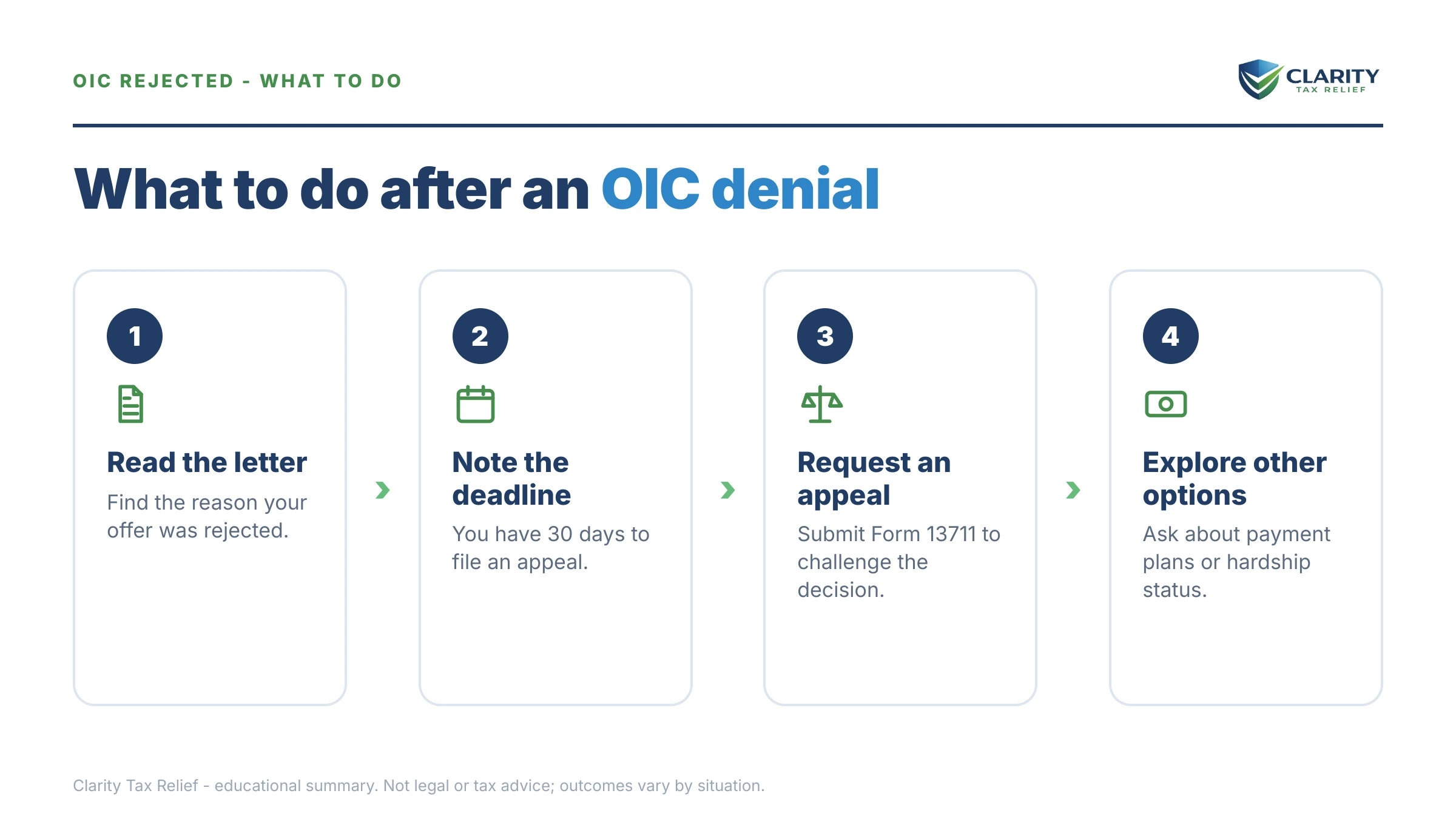

- Find the date and the reason on your rejection letter — the date starts your 30-day clock; the reason tells you whether to appeal or reapply.

- Confirm it's a rejection, not a return — only a rejection is appealable. Check the letter's wording and your transcript for code 481.

- Recalculate your RCP — compare the IRS's asset values and disposable income to your own honest numbers to spot any error.

- File Form 13711 within 30 days if you're appealing — state each disputed item and attach your supporting proof.

- Or submit a new Form 656 if your number was genuinely too low, with a fresh fee and 20% down (both waived if you qualify as low-income).

- Protect yourself in the meantime — if you won't appeal or reapply, set up an installment agreement or request CNC before collection restarts.

Not sure whether your rejection reason is arguable? A quick review can tell you in one call whether to appeal, reapply, or pivot to a payment plan before the window closes.

What happens to your deposit and fee

Neither your $205 application fee nor your payments come back after a rejection — but the payments aren't lost. The $205 fee is retained by the IRS, while any 20% down payment or periodic payments you made are applied to your tax balance, lowering what you owe. You can direct in writing how the IRS applies that money to a specific tax period; otherwise the IRS applies it in the government's best interest. For the full breakdown, see oic down payment refundable.

| Stage | Your window | What you can still do |

|---|---|---|

| Rejection letter received | 30 days to appeal | File Form 13711 or plan a new offer |

| Appeal filed timely | Collection stays paused | Argue valuation / income in Appeals |

| Window closed, no action | Collection resumes | Set up an installment agreement or CNC now |

| Notice of Intent to Levy (CP504) | Before levy on state refund | Resolve balance or request a hold |

| Final Notice (LT11) | 30 days + CDP rights | Request a CDP hearing to stop levies |

When you can handle this yourself — and when help changes the outcome

You can handle the aftermath alone when the situation is simple: the rejection was correct, your balance is modest, and you just need to set up a streamlined installment agreement online. If you agree the offer was too low and don't want to keep chasing a settlement, a payment plan or CNC is a clean self-serve fix.

Experienced help changes the math when the rejection is arguable. If the IRS overvalued an asset, miscounted your allowable living expenses, added back dissipated assets, or you're a self-employed filer whose future income was projected too high, a Form 13711 appeal built on the right documentation is where those disputes get won. The same is true if you have multiple years in play, business income complicating the RCP, or a levy already looming — those are the cases where the order you fix things in decides what you ultimately pay.

Terms on your rejection letter, decoded

- Reasonable Collection Potential (RCP): the IRS's estimate of everything it could collect from your assets plus future income — the number your offer must meet or beat.

- Form 13711: the Request for Appeal of Offer in Compromise; your tool to challenge a rejection within 30 days.

- Rejected vs. returned: a rejection was evaluated and is appealable; a return was never fully reviewed and is not.

- Dissipated assets: money or property you spent that the IRS adds back into RCP as if you still had it.

- Code 481: the transcript entry that confirms your offer was officially rejected.

- Independent Office of Appeals: the separate IRS unit that hears your Form 13711 appeal and can weigh litigation risk.

OIC rejection questions, answered

What's the difference between an OIC being rejected and being returned?

A rejected offer was reviewed on its merits and turned down — and it carries a 30-day right to appeal with Form 13711. A returned offer was never fully evaluated, usually because a return is unfiled, an estimated payment is missing, or you're in an open bankruptcy. A return has no appeal rights, but you can fix the problem and resubmit right away with a fresh application.

How long do I have to appeal an OIC rejection?

You have 30 days from the date printed on the rejection letter to file Form 13711, Request for Appeal of Offer in Compromise. That date is the date on the letter, not the day it arrives, so open the envelope immediately. Miss the window and you lose the automatic appeal — you'd have to start over with a brand-new offer instead.

Can I submit a new offer after being rejected?

Yes. You can file a new Form 656 with a fresh $205 fee and 20% down (both waived if you qualify as low-income) whenever your financial picture supports a higher, realistic number. A new offer makes sense when your finances have changed or your first offer was simply too low for your Reasonable Collection Potential. If the rejection was a math or valuation error, appealing is usually faster and cheaper than reapplying.

Do I get my OIC deposit and application fee back if I'm rejected?

No. The $205 application fee is not refunded, and any 20% down payment or periodic payments you made are applied to your tax balance rather than returned. That is not lost money — it directly reduces what you owe. You can tell the IRS in writing how to apply the payment to a specific tax period; otherwise the IRS applies it in the government's best interest.

What are the most common reasons the IRS rejects an OIC?

The number-one reason is that your offer is less than your Reasonable Collection Potential — the IRS believes it can collect more from your assets and future income than you offered. Other frequent causes are missing or understated asset equity, disposable income the IRS calculates higher than you did, dissipated assets added back in, or a compliance gap like an unfiled year. The IRS accepted roughly 1 in 5 offers in FY2024, so rejection is common — and often fixable.

Does IRS collection resume after my OIC is rejected?

Yes, but not instantly. Collection is paused while an offer is pending and during the 30-day appeal window, and it stays paused if you file a timely Form 13711 appeal. Once the appeal is exhausted or the window closes, the IRS restarts its collection sequence — reminder notices, then a Notice of Intent to Levy, then a final notice. Interest and the failure-to-pay penalty accrue the entire time.

Should I appeal my OIC rejection or just reapply?

Appeal when the rejection came from a disagreement the IRS got wrong — an inflated asset value, disposable income miscalculated, or dissipated assets added back unfairly. Reapply when your numbers were genuinely too low or your finances have changed since you filed. Appeals often improve the outcome because the Independent Office of Appeals can weigh hazards of litigation the offer examiner cannot, and it does not cost another fee.

What does code 481 on my transcript mean after an OIC?

Transaction Code 481 means your Offer in Compromise was rejected and posted to your account. It typically replaces Code 480, which shows an offer is pending. Seeing 481 confirms the rejection is official and your collection hold is winding down — so it's your cue to file Form 13711 within 30 days or move to another resolution before enforcement restarts.

Your next 24 hours

- Find the date on your rejection letter. That single date starts your 30-day clock to file Form 13711 — write it down before you do anything else.

- Gather your offer paperwork. Pull your Form 656, your 433-A (OIC), and the asset values you reported so you can compare them to the IRS's numbers and spot any error.

- Get a free case review. Use the 2-minute form or call (888) 825-7779 — we'll tell you whether to appeal or reapply while the 30-day window is still open.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.

Primary sources: IRS — Offer in Compromise, IRS Independent Office of Appeals, and the Taxpayer Advocate Service.