Data Study

IRS Offer in Compromise Acceptance Rate: The Real Odds by the Numbers (2026)

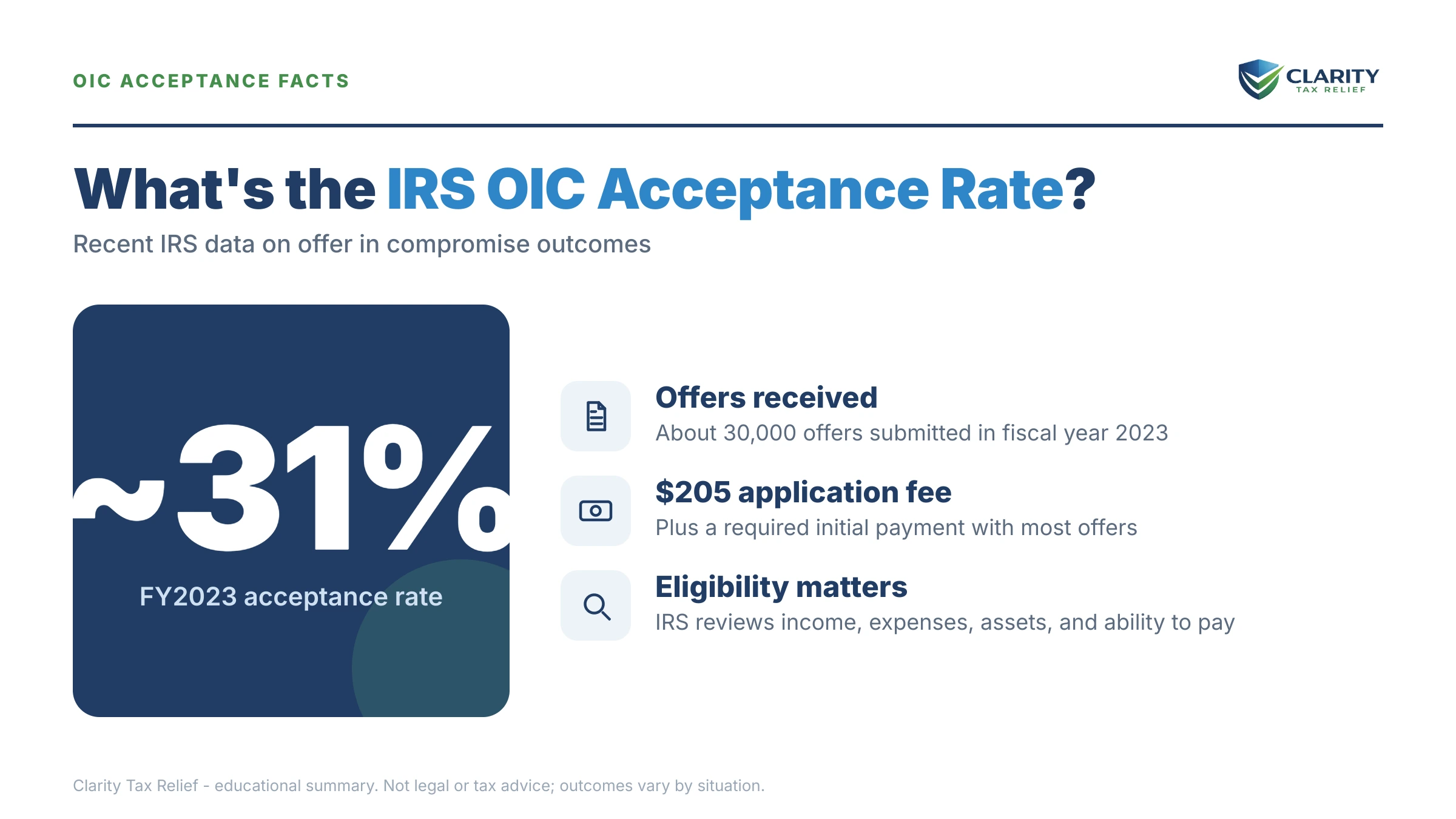

The headline number: the IRS offer in compromise acceptance rate was about 21% in fiscal year 2024 — the IRS received 33,591 offers and accepted 7,199 of them, roughly 1 in 5. Across the last decade (FY2015–FY2024), the IRS accepted about 37% of all offers, or roughly 1 in 3.

If you've searched for the IRS offer in compromise acceptance rate, you've probably also seen ads promising to settle your tax debt for "pennies on the dollar." This data study uses the IRS's own published figures to show what really happens to offers in compromise — an Offer in Compromise (OIC) is a formal agreement that lets you settle a tax debt for less than the full amount you owe. The numbers tell a more honest story than the ads do.

Key findings

- About 1 in 5 offers were accepted in FY2024. The IRS received 33,591 offers in compromise and accepted 7,199 — an acceptance rate of roughly 21%.

- The dollars accepted were modest at the program level. Accepted offers in FY2024 totaled about $163.4 million across all 7,199 deals.

- The rate swings year to year. The prior fiscal year, the IRS accepted about 42% of offers — twice the FY2024 share.

- Over the long run, about 1 in 3 offers are accepted. Across FY2015–FY2024, taxpayers submitted nearly 500,000 offers and the IRS accepted about 37% overall.

- "Pennies on the dollar" is a slogan, not a statistic. The amount the IRS accepts is set by a formula tied to your assets and income — not by negotiation theater.

The IRS offer in compromise acceptance rate, by the numbers

Here are the verified figures from the IRS Data Book. We've rounded acceptance rates to whole percentages and left the underlying counts exact.

| Measure | Figure |

|---|---|

| Offers in compromise received (FY2024) | 33,591 |

| Offers in compromise accepted (FY2024) | 7,199 |

| Acceptance rate (FY2024) | ~21% (about 1 in 5) |

| Dollar value of accepted offers (FY2024) | ~$163.4 million |

| Acceptance rate (prior fiscal year) | ~42% |

| Offers submitted (FY2015–FY2024) | nearly 500,000 |

| Acceptance rate (FY2015–FY2024) | ~37% (about 1 in 3) |

What this means in plain English

Two things jump out of these numbers.

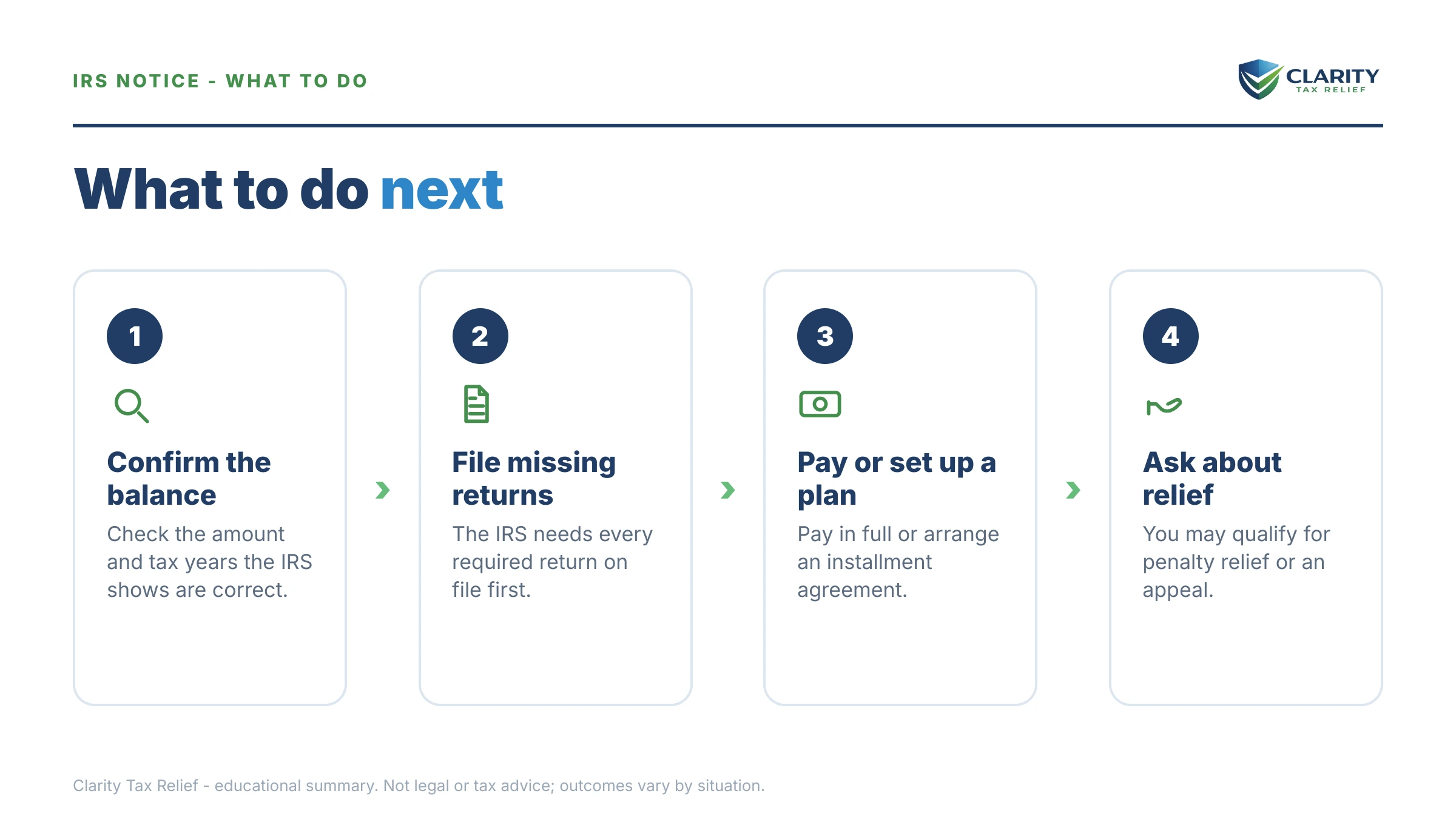

First, an offer in compromise is real — but it is not common, and it is not automatic. Roughly 4 out of 5 offers in FY2024 were not accepted. That's not because the IRS is heartless. It's because an offer only gets accepted when it meets the agency's math. The IRS measures something called your Reasonable Collection Potential (RCP) — basically, the most it believes it could collect from your assets plus your future income over a set period. If your offer is less than that number, it usually gets rejected. If you can full-pay through a monthly plan, you generally won't qualify at all.

Because the offer amount comes down to that formula, it helps to run your own figures before you ever file. You can estimate your own offer with our Offer in Compromise Calculator, which estimates the lowest amount the IRS may accept based on your finances — no promise of a specific result, just a realistic starting number.

Second, the year-to-year swing matters. The acceptance rate was about 42% one year and about 21% the next. A single year's rate doesn't decide your odds. What decides your odds is whether your finances genuinely fit the program. Someone with few assets, low income, and full compliance has a very different outlook than someone offering a lowball number while still earning enough to pay over time.

So here's the honest takeaway on "pennies on the dollar": the IRS did accept about $163.4 million across 7,199 offers in FY2024, which means many people legitimately settled for less than they owed. But the discount is driven by a formula, not a sales pitch. Anyone promising to settle your debt for pennies on the dollar before reviewing your finances is selling you something. The right question isn't "how low can we go?" — it's "what does my Reasonable Collection Potential actually come out to?"

Want to know your real odds — before you spend a dime?

The fastest way to know whether an Offer in Compromise fits is to run your numbers with an experienced tax professional. We'll review your assets, income, and balance and tell you honestly whether you may qualify — free, confidential, no pressure. Learn more about how an Offer in Compromise works, then talk it through with us.

Methodology & source

All figures in this study come from the IRS Data Book, Offers in Compromise table, published each year by the Internal Revenue Service. You can review the source data directly at the SOI Tax Stats — All Years IRS Data Book page on IRS.gov.

The acceptance rate is calculated as offers accepted divided by offers received within a federal fiscal year (October 1 through September 30). Because the IRS reports figures by fiscal year and offers can be received in one year and decided in the next, single-year rates are best read as a snapshot rather than a precise per-applicant probability. Dollar totals reflect the value of accepted offers, not the amount of debt forgiven. We rounded acceptance rates to whole percentages and left counts and dollar figures as reported. No figures were estimated or modeled.

Cite this study

You're welcome to cite or quote these figures. Please use this attribution and link back:

"IRS Offer in Compromise Acceptance Rate: The Real Odds by the Numbers," Clarity Tax Relief IRS Help Center, analysis of the IRS Data Book. Available at https://claritytaxrelief.com/blog/irs-oic-acceptance-rate/.

Frequently asked questions

What is the IRS offer in compromise acceptance rate?

In fiscal year 2024 the IRS received 33,591 offers in compromise and accepted 7,199 of them — about a 21% acceptance rate, or roughly 1 in 5. The rate moves from year to year; the prior fiscal year it was about 42%. Across fiscal years 2015 through 2024, the IRS accepted about 37% of all offers, or roughly 1 in 3.

Why is the offer in compromise acceptance rate so low?

Most rejected offers come from people who didn't actually qualify or who offered far less than the IRS formula would accept. The IRS only accepts an offer when it equals or beats your Reasonable Collection Potential — what it could collect from your assets and future income. Offers that ignore that math, or that come from people who can full-pay over time, get rejected.

Can the IRS really settle tax debt for pennies on the dollar?

Not as a rule. "Pennies on the dollar" is a marketing slogan, not a program. The IRS accepted about 1 in 5 offers in FY2024, and the amount it accepts is tied to a strict formula based on your assets and income. Anyone promising to settle your debt for pennies on the dollar before reviewing your finances is selling you something.

How can I improve my chances of an offer being accepted?

File all required tax returns first, stay current on this year's taxes, and offer at least what the IRS formula expects based on your assets and income. Submitting a complete, accurate Form 656 and Form 433-A(OIC) with full documentation matters. An experienced tax professional can run the numbers before you apply so you don't waste the application fee on an offer that can't be accepted.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.