Data Study

How Often Does the IRS Remove Penalties? The Abatement Numbers (2026)

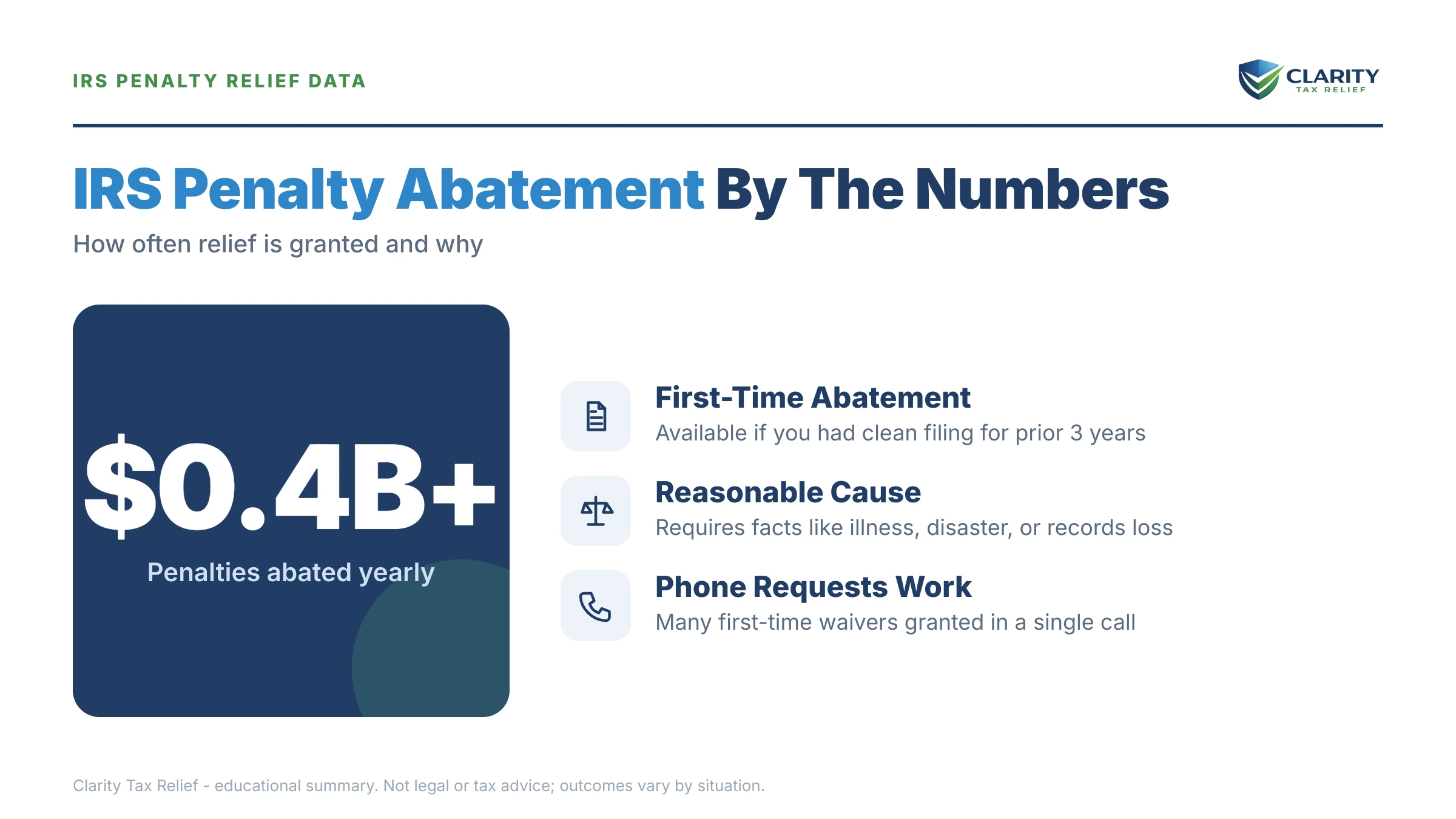

The short answer: how often does the IRS remove penalties? A lot — by dollar volume. In fiscal year 2024 the IRS assessed about $84.1 billion in civil penalties on individual, estate, and trust income tax returns and reduced or abated about $75.2 billion on those same returns. That is not a 90% approval rate for relief requests, but it shows penalties come off accounts often enough that it's worth asking.

Key findings

- In fiscal year 2024, the IRS assessed about $84.1 billion in civil penalties on individual, estate, and trust income tax returns.

- Over the same period, the IRS reduced or abated about $75.2 billion in penalties on those same return types.

- The "reduced or abated" figure includes routine corrections, recomputations, and several forms of relief — it is not a count of granted abatement requests, and it does not mean ~90% of penalties are "forgiven."

- The takeaway is practical: a very large dollar volume of penalties is removed every year, which is exactly why it is worth requesting relief such as First-Time Abatement or reasonable cause.

- The IRS rarely removes a penalty automatically. In most cases, you have to ask — and back it up with the facts.

The numbers: penalties assessed vs. reduced or abated

Here are the figures for individual, estate, and trust income tax returns in fiscal year 2024, straight from the IRS Data Book.

| Measure (FY 2024) | Amount |

|---|---|

| Civil penalties assessed (individual, estate & trust income tax returns) | ~$84.1 billion |

| Civil penalties reduced or abated (same return types) | ~$75.2 billion |

Source: IRS Data Book, Civil Penalties Assessed and Abated (Table 28). Figures are rounded.

What this means in plain English

It's tempting to divide $75.2 billion by $84.1 billion, get about 90%, and conclude the IRS wipes out nearly every penalty. Please don't. That math is misleading, and acting on it could cost you.

Here's why. The "reduced or abated" total mixes together several very different things:

- Routine corrections — the IRS catches its own posting errors and backs out penalties that should never have been charged.

- Recomputations — when a return is amended or a balance changes, the related penalty is recalculated, often downward.

- Granted relief — First-Time Abatement and reasonable-cause requests that taxpayers actually filed and the IRS approved.

Only that last bucket reflects relief that someone asked for and won. The Data Book does not break the $75.2 billion into those pieces, so nobody can honestly say "the IRS approves 90% of abatement requests." Anyone who tells you that is guessing.

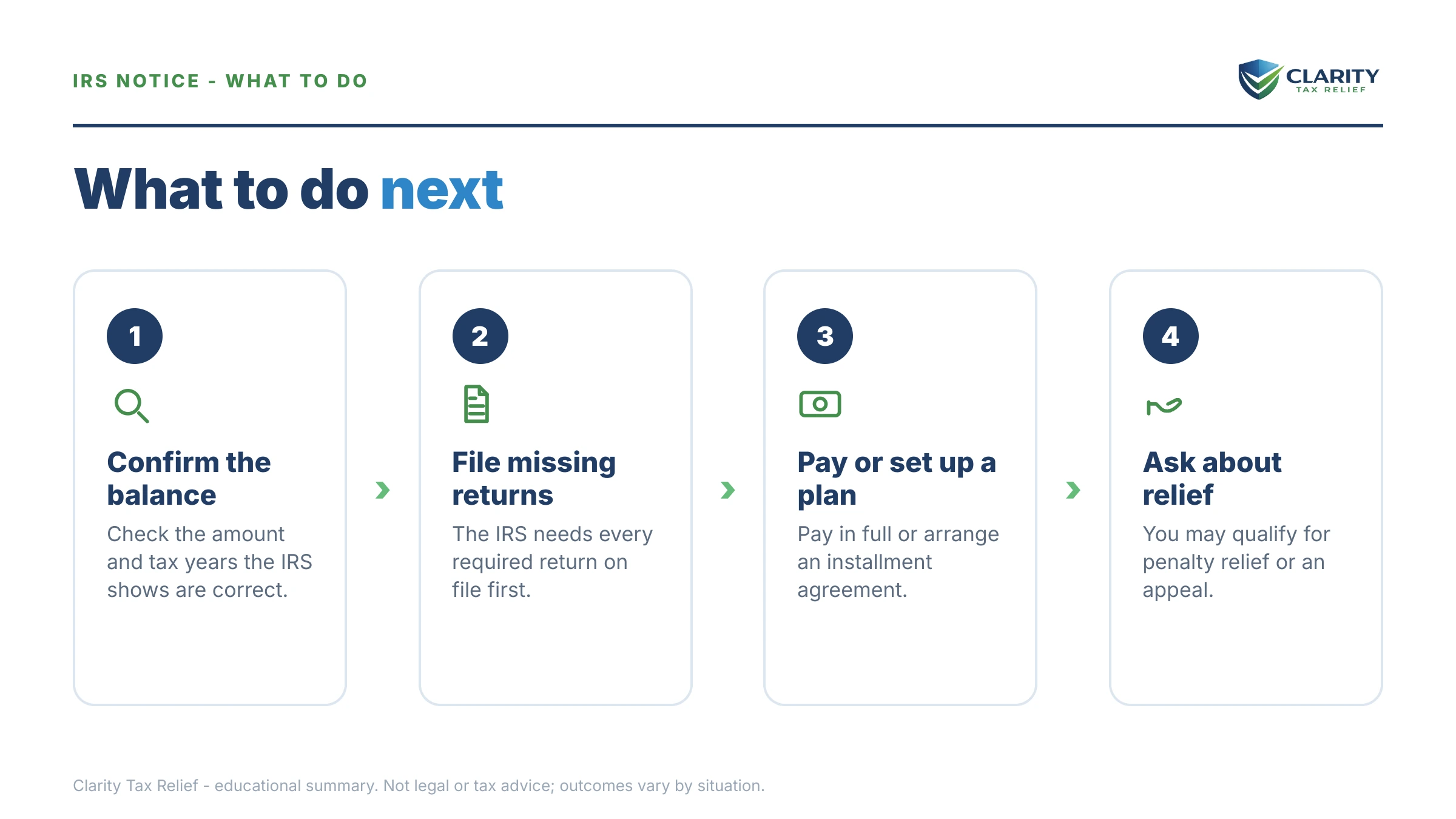

The honest, useful read is this: the IRS removes an enormous dollar volume of penalties every year. Penalties are not permanent. Under the right circumstances they come off — but you generally have to request it, and you have to show why you qualify. That is the whole reason to file a clear, well-supported request rather than just paying a penalty you might not owe.

The two most common paths are First-Time Abatement (FTA) — for taxpayers with a clean recent compliance history — and reasonable-cause relief, for circumstances beyond your control such as serious illness, a death in the family, a natural disaster, or relying on wrong advice. The IRS explains both on its penalty relief page. If you want to see exactly how a penalty was calculated before you challenge it, our IRS penalty and interest calculator can help you understand the running total.

Think a penalty might come off your account?

Send us your notice. An experienced tax professional will review whether you may qualify for First-Time Abatement or reasonable-cause relief — free, confidential, and no pressure. Eligibility always depends on your specific facts.

Methodology & source

This study uses published, official figures only. No estimates were created. The data comes from the IRS Data Book, the annual statistical report the IRS issues on its own operations.

- Source: IRS Data Book — Civil Penalties Assessed and Abated by Type of Tax and Type of Penalty (Table 28).

- Period: Fiscal year 2024.

- Scope: Civil penalties on individual, estate, and trust income tax returns.

- Rounding: Dollar figures are rounded to the nearest tenth of a billion.

- Important limitation: "Reduced or abated" dollars include routine corrections, recomputations, and relief combined. The figure cannot be read as an approval rate for abatement requests.

For background on how the IRS corrects return amounts (another driver of penalty changes), see our related study on IRS math error notice statistics.

Cite this study

Researchers, journalists, and tax pros are welcome to cite these figures. Please credit the original IRS source and link back to this page.

Clarity Tax Relief. "How Often Does the IRS Remove Penalties? The Abatement Numbers (2026)." https://claritytaxrelief.com/blog/irs-penalty-abatement-statistics/. Data: IRS Data Book, Civil Penalties Assessed and Abated (Table 28), FY2024.

Penalty abatement, answered

Does the IRS really remove about 90% of penalties?

No — that is a misreading of the numbers. The dollars the IRS reduces or abates each year include routine corrections, recomputations, and several kinds of relief, not just granted abatement requests. So while a very large dollar volume of penalties is removed annually, you cannot read it as a 90% approval rate for relief requests. Your own outcome depends on your facts.

How much in penalties did the IRS remove in 2024?

According to the IRS Data Book, in fiscal year 2024 the IRS reduced or abated about $75.2 billion in civil penalties on individual, estate, and trust income tax returns. Over the same period it assessed about $84.1 billion in penalties on those same return types.

If so many penalties are removed, is it worth requesting abatement?

Yes. The sheer dollar volume of penalties reduced or removed each year shows the IRS does take penalties off accounts under the right circumstances. First-time abatement and reasonable-cause relief are real programs with published rules. You generally have to ask — the IRS does not automatically remove a penalty just because you qualify.

What types of penalty relief does the IRS offer?

The most common are First-Time Abatement, for taxpayers with a clean recent compliance history, and reasonable-cause relief, for events outside your control such as serious illness, a natural disaster, or reliance on incorrect advice. The IRS may also correct or recompute penalties when its own records or the law require it.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.