IRS Data Study

How Often Does the IRS Actually Seize Your Property? (Rarely) — 2026 Data Study

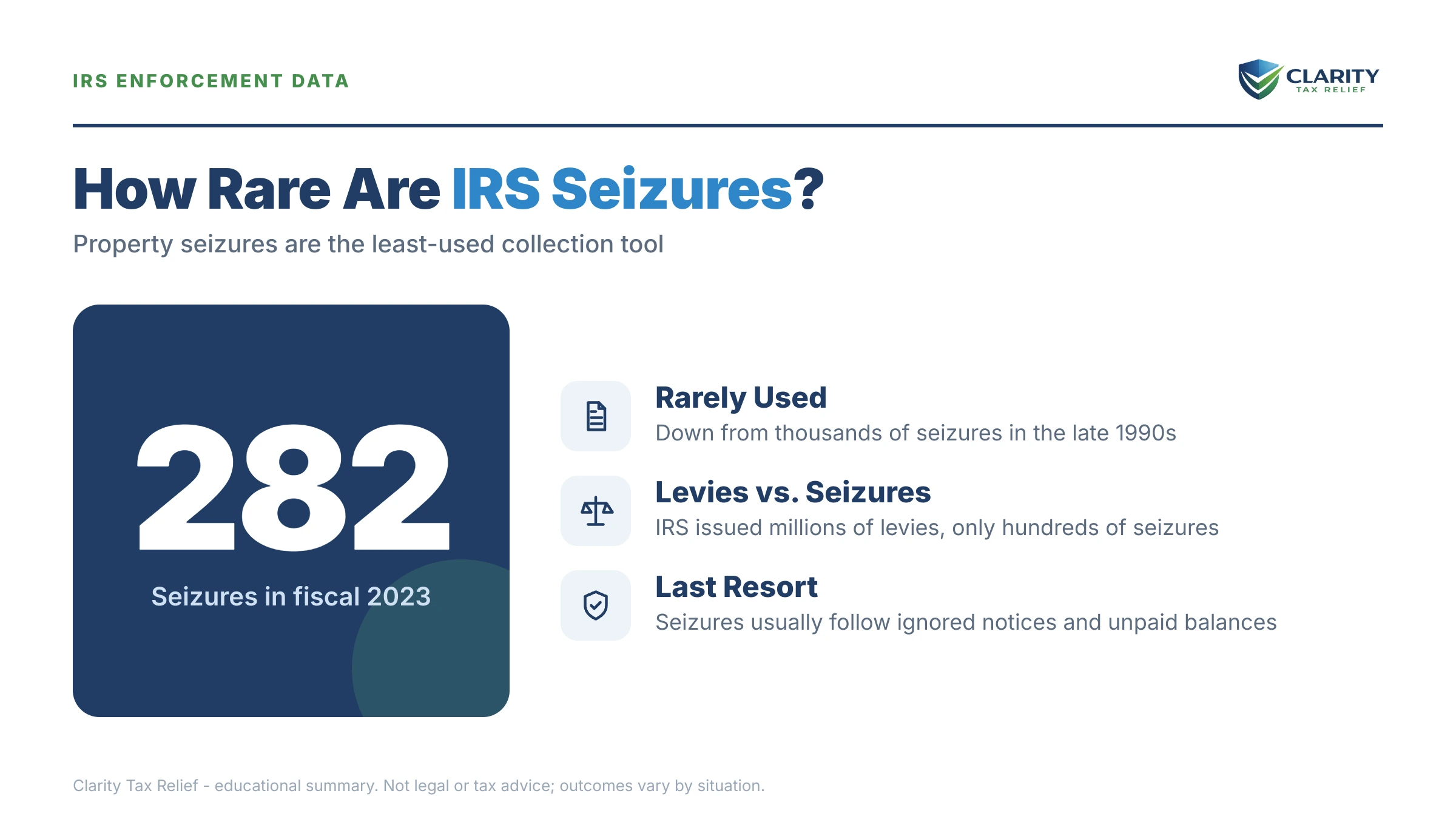

The short answer: almost never. So how often does the IRS seize property? According to the IRS Data Book, the IRS conducted just 50 property seizures nationwide in fiscal year 2025 — down from 71 the year before. By contrast, it filed about 214,099 tax liens and served about 339,137 levies. Physical seizure of your home or car is one of the rarest things the IRS does.

Worried about a lien or levy?

Seizures are rare — but liens and levies are common, and they move fast once they start. Send us your notice and an experienced tax professional will explain exactly where you stand and what your options are. Free, confidential, no pressure.

Key findings

- The IRS conducted only 50 property seizures in fiscal year 2025 (FY2025), down from 71 in fiscal year 2024 (FY2024) — a drop of about 30%.

- That works out to roughly one physical seizure per week for the entire United States.

- In FY2025, the IRS filed about 214,099 Notices of Federal Tax Lien — roughly 4,280 times more often than it seized property.

- In FY2025, the IRS served about 339,137 notices of levy on third parties such as banks and employers — roughly 6,780 times more often than it seized property.

- Takeaway: the realistic risk for most taxpayers is a lien or a bank/wage levy — not the IRS showing up to take a house or car.

The numbers: IRS property seizures vs. liens and levies

Here is how the major IRS collection actions compare, using figures from the IRS Data Book. Seizure counts are shown for both years; lien and levy figures reflect FY2025.

| IRS collection action (FY2025) | Figure |

|---|---|

| Physical property seizures | 50 |

| Notices of Federal Tax Lien filed | ~214,099 |

| Notices of levy served on third parties (banks, employers) | ~339,137 |

Source: IRS Data Book FY2025, Table 4-1. Lien and levy figures are rounded as reported by the IRS; "—" indicates a figure not used in this study.

What this means in plain English

The fear most people feel when they owe the IRS is the same one: agents at the door, the house sold, the car towed. The data shows that picture is almost never reality. With only 50 seizures in all of FY2025, a physical seizure is among the rarest actions the IRS takes — it usually comes only after years of ignored notices, in cases involving large balances and no cooperation.

That doesn't mean a tax debt is harmless. It means the real risk is different from the one people imagine. The IRS filed roughly 214,099 federal tax liens and served about 339,137 levies in the same year. A lien is a public legal claim that can wreck your credit and follow you when you sell property. A levy actually takes money — from your paycheck or straight out of your bank account.

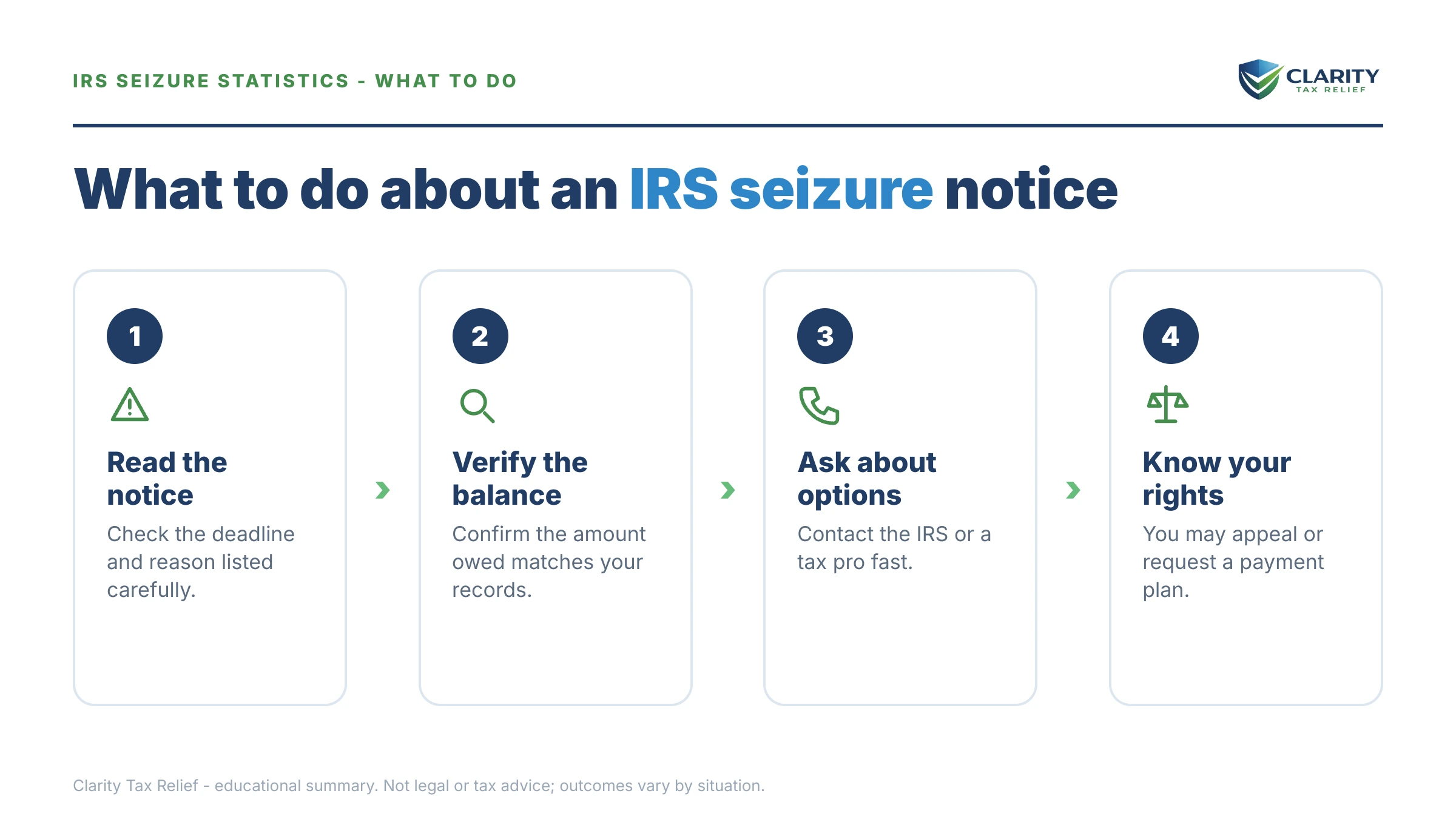

So the lesson isn't "relax." It's "aim at the right target." You probably won't lose your home. But a bank account frozen on payday, or a chunk of every check garnished, is a common and disruptive outcome — and it's the one worth preventing. Both happen through an automated notice sequence, which means you almost always get warning and time to act before money moves.

If a levy has already hit, fast action can stop it — see how a bank levy release works and what to do about a federal tax lien. The earlier you respond to IRS notices, the more options you keep.

Methodology & source

This study uses published figures from the Internal Revenue Service Data Book, Table 4-1 ("Delinquent Collection Activities"). The seizure counts, Notices of Federal Tax Lien filed, and notices of levy served on third parties are reported directly by the IRS for the fiscal years shown. We rounded lien and levy figures as the IRS reports them and calculated the year-over-year change and the seizure-to-lien and seizure-to-levy ratios from those published numbers. No figures were estimated or modeled.

Primary source: IRS Data Book, Table 4-1 — Delinquent Collection Activities. For broader context on enforcement and taxpayer protections, see the Taxpayer Advocate Service.

Cite this study

Researchers, journalists, and bloggers are welcome to cite these figures. Please use the attribution line below and link back to this page:

"The IRS conducted just 50 property seizures in fiscal year 2025, compared with about 214,099 tax liens filed and 339,137 levies served — making physical seizure one of its rarest collection actions." — Clarity Tax Relief, How Often Does the IRS Actually Seize Your Property? (2026), analysis of IRS Data Book FY2025, Table 4-1.

IRS seizure statistics: frequently asked questions

How often does the IRS actually seize property?

Very rarely. According to the IRS Data Book, the IRS conducted just 50 property seizures nationwide in fiscal year 2025, down from 71 in fiscal year 2024. A physical seizure of a home, car, or business asset is one of the rarest collection actions the IRS takes.

Is the IRS more likely to levy my bank account than seize my house?

Yes, by a wide margin. In fiscal year 2025 the IRS served about 339,137 notices of levy on third parties such as banks and employers, compared with only 50 physical property seizures. A bank or wage levy is thousands of times more common than the IRS taking your home or car.

What is the difference between a levy, a lien, and a seizure?

A lien is a legal claim against your property that protects the government's interest — the IRS filed about 214,099 Notices of Federal Tax Lien in fiscal year 2025. A levy actually takes funds, such as money from a bank account or wages. A seizure is the IRS taking and selling physical property like a house or car, which happened only 50 times in fiscal year 2025.

What should I do if I am worried about an IRS seizure?

Act before the collection process escalates. Seizures are rare, but liens and levies are common and can disrupt your finances. Responding early to IRS notices, setting up a payment plan, or requesting a collection alternative reduces the risk. A free consultation with an experienced tax professional can map out your options.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.