Tax Liens

Can I Refinance With an IRS Lien? Yes — Here's How (2026)

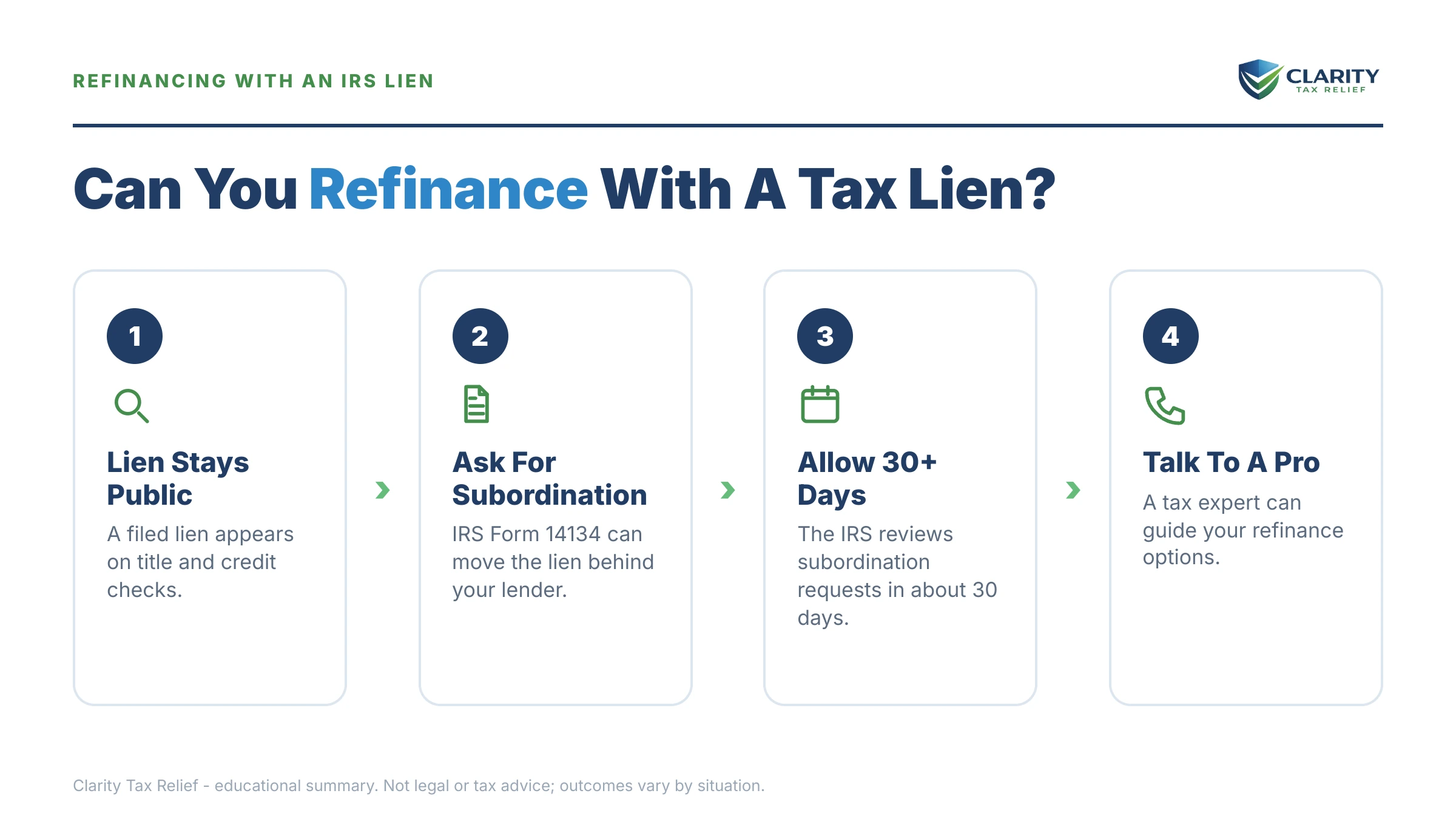

The short answer to "can I refinance with an IRS lien": yes. The lien must be handled before closing, and there are four established paths — pay it off from loan proceeds, subordinate it with Form 14134, get it withdrawn with Form 12277, or discharge the property with Form 14135. Subordination applications should reach the IRS at least 45 days before closing.

Maybe your divorce decree gave you a deadline to refinance the house into your name alone, and the loan was moving — until the title search turned up a federal tax lien from a year you filed jointly, and your loan officer put everything on hold. That hold is removable. The IRS has a formal process built for exactly this moment, and your job now is picking the right path and starting the paperwork early enough.

Further down, the image shows you exactly what the recorded Notice of Federal Tax Lien looks like and where to find the three details your lender will ask about: the amount, the tax years covered, and the recording date.

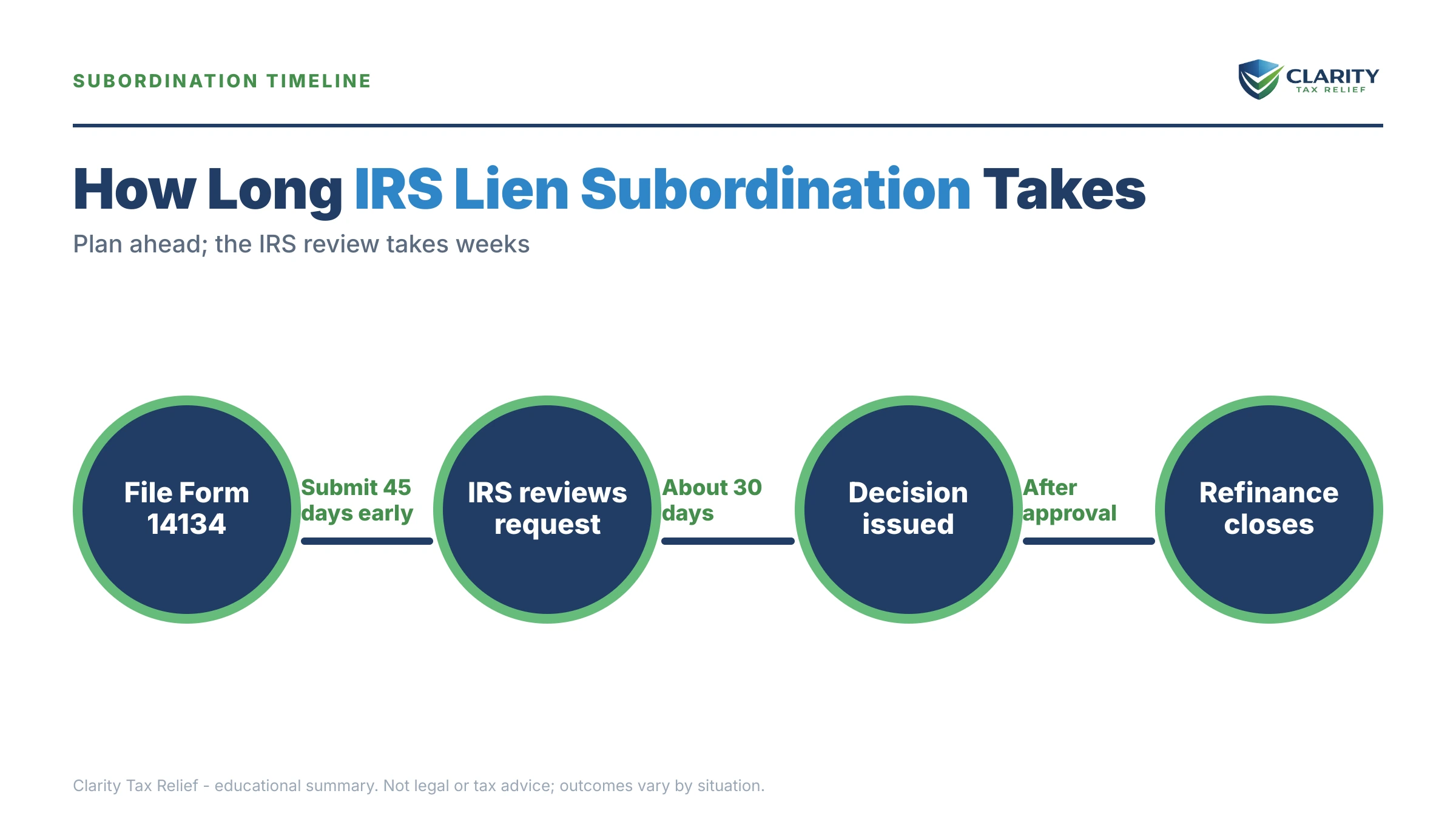

⏱ The clock that matters: the IRS asks for Form 14134 subordination applications at least 45 days before your loan settlement date. If your closing is already on the calendar, count backward from it today — a late or incomplete application is the most common reason a lien refinance falls apart.

Can I refinance with an IRS lien? What lenders actually check

You can refinance with an IRS lien because the IRS issues Certificates of Subordination — a document created specifically so refinances can close while a tax debt is still being paid. The lien is an obstacle with a procedure attached, not a dead end.

Here's what surprises most borrowers: tax liens have been off all three credit reports since 2018, so your credit score may be fine and your preapproval may sail through. The lien surfaces later, when the title company searches county records — where the Notice of Federal Tax Lien is a public filing. We cover why the score doesn't tell the whole story in tax lien on credit report.

So the question your lender is really asking isn't "does this person owe the IRS?" It's "will my new mortgage be in first position?" That's a priority question, and it's answerable — usually in one of four ways, each with its own form, cost, and timeline. You'll see all four compared in the table below.

Why a federal tax lien stalls a refinance

A refinance pays off your existing mortgage — and when that original mortgage is released, its first-lien position dies with it. Without IRS paperwork, the recorded tax lien would move up the line, and your new lender would be funding a loan that sits behind the IRS. No lender will do that voluntarily. The mechanics of who stands where are covered in tax lien vs mortgage priority.

This is why the lien blocks a refinance harder than it blocks staying put. Your current mortgage predates the lien and keeps its priority; the new loan wouldn't.

If you're recently divorced, two wrinkles matter. First, if the debt comes from a jointly filed return, both ex-spouses remain fully liable to the IRS regardless of what the decree says — the IRS was never a party to your divorce, a problem explained in why the IRS ignores the divorce decree. Second, if the lien is for your ex's separate debt but the house was jointly titled, the lien can still attach to their interest; see IRS lien on jointly owned property for how that plays out at closing.

What happens if you try to close without addressing the lien

A refinance application with an unaddressed federal tax lien doesn't get rejected on day one — it stalls in stages, and each stage costs you money:

- Application and preapproval — nothing flags. The lien isn't on your credit report, so the early stages feel normal.

- Title search — the Notice of Federal Tax Lien surfaces in county records. The title company reports it to the lender as a cloud on title.

- Underwriting condition — approval becomes conditional on resolving the lien. Your rate lock keeps ticking; extensions typically cost a fee or a worse rate.

- Closing postponed or the loan denied — if you arrive at the settlement date without a payoff letter or an IRS certificate in hand, the lender won't fund. You may have to restart the application, appraisal and all.

- The balance keeps growing the whole time — interest compounds daily and the 0.5%-per-month failure-to-pay penalty keeps posting, so the payoff quote next month is higher than this month's. The lien itself follows the debt until it's paid, withdrawn, or the collection statute runs out — and the IRS can refile before that happens.

None of this is a levy or a seizure — a lien is a claim, not a taking (the distinction is laid out in lien vs. levy). But for a refinance on a deadline, the lien is the single item most likely to blow the closing date.

Title search just turned up an IRS lien?

Get the lien, your payoff numbers, and your fastest path to closing reviewed free — before the 45-day subordination window eats your settlement date. An experienced tax professional will tell you whether payoff, subordination, or withdrawal fits your loan.

Your four ways to refinance around a federal tax lien

Every successful lien refinance uses one of four IRS procedures, and none of them carries an IRS application fee. Which one fits depends on your equity, your balance, and whether you're paying the debt off or keeping it on a plan:

| Option | Best when | IRS form & fee | What happens to the lien |

|---|---|---|---|

| Pay off at closing | Your equity covers the full payoff (cash-out or rate-and-term with funds to close) | Payoff request only — no form, no fee | Released — the IRS must issue a Certificate of Release within 30 days of full payment |

| Subordination | You're keeping the balance on a payment plan and just need the new lender in first position | Form 14134 — no IRS fee | Stays recorded, but the new mortgage moves ahead of it in priority |

| Withdrawal | You owe $25,000 or less and pay by direct-debit installment agreement | Form 12277 — no IRS fee | The public filing is pulled as if never recorded; the debt itself remains |

| Discharge | You need one specific property removed from the lien — mainly sales, occasionally divorce buyouts | Form 14135 — no IRS fee | Lifted from that property only; still attaches to everything else you own |

Payoff at closing is the cleanest path when the math works. The title company orders an official payoff figure from the IRS, writes it into the settlement statement, and pays the IRS directly from loan proceeds. You never touch the money, the lender's attorney watches it happen, and the release process starts automatically — getting a lien released after payment covers the certificate and how to speed up the county recording.

Subordination is for balances too big to pay at closing. The IRS agrees to stand behind your new lender because the refinance helps its own collection — a lower payment leaves you more able to pay the tax debt, or cash-out proceeds go partly to the IRS. The full application, attachment by attachment, is walked through in tax lien subordination (Form 14134).

Withdrawal is the underused one. Under the IRS's Fresh Start lien rules, a balance of $25,000 or less on a direct-debit installment agreement can qualify to have the notice withdrawn — typically after three consecutive direct-debit payments. Withdrawal erases the public filing entirely, which reads better to an underwriter than a release. See lien withdrawal (Form 12277) for the request itself.

Discharge mostly belongs to sales rather than refinances — if that's actually your situation, start with selling a house with an IRS lien and tax lien discharge (Form 14135). In a divorce, discharge occasionally appears when one spouse buys out the other and a lien attaches only to the departing spouse's interest.

A worked example: a $6,200 lien and a divorce-decree deadline

Say you're recently divorced and the decree requires you to refinance within twelve months — removing your ex from the mortgage and paying a $35,000 equity buyout. You owe the IRS $6,200 from a jointly filed year, and a Notice of Federal Tax Lien was recorded ten months ago. The numbers, all hypothetical:

- Home value: $310,000. Current mortgage balance: $198,000.

- Cash-out refinance at 80% loan-to-value → maximum new loan of $248,000.

- Payoff needs: $198,000 (old mortgage) + $35,000 (buyout) + roughly $6,000 in closing costs = $239,000 — leaving about $9,000 of room.

- IRS payoff: the lien says $6,200, but ten months of the 0.5%-per-month failure-to-pay penalty adds about $310, and interest adds several hundred more — call the actual payoff quote roughly $6,850.

The $9,000 of room covers the $6,850 payoff, so the cleanest move is a payoff at closing: the title company pays the IRS from proceeds, the loan closes in first position, and the Certificate of Release must issue within 30 days.

If the appraisal comes in low and the room disappears, the fallback still works. At $6,200, you're under the $10,000 ceiling for a guaranteed installment agreement — which is available to individuals only, for an income-tax balance of $10,000 or less excluding penalties and interest, and requires that all returns are filed, that you've filed and paid on time for the past 5 years with no installment agreement in that period, and that the balance is paid in full within 3 years. Paid over 36 months, that's about $173 a month ($6,200 ÷ 36, plus accruing interest). Set it up as direct debit, make the payments, request withdrawal on Form 12277 — or, if the closing can't wait, file Form 14134 for subordination so the loan closes while the plan runs.

How to refinance with an IRS lien, step by step

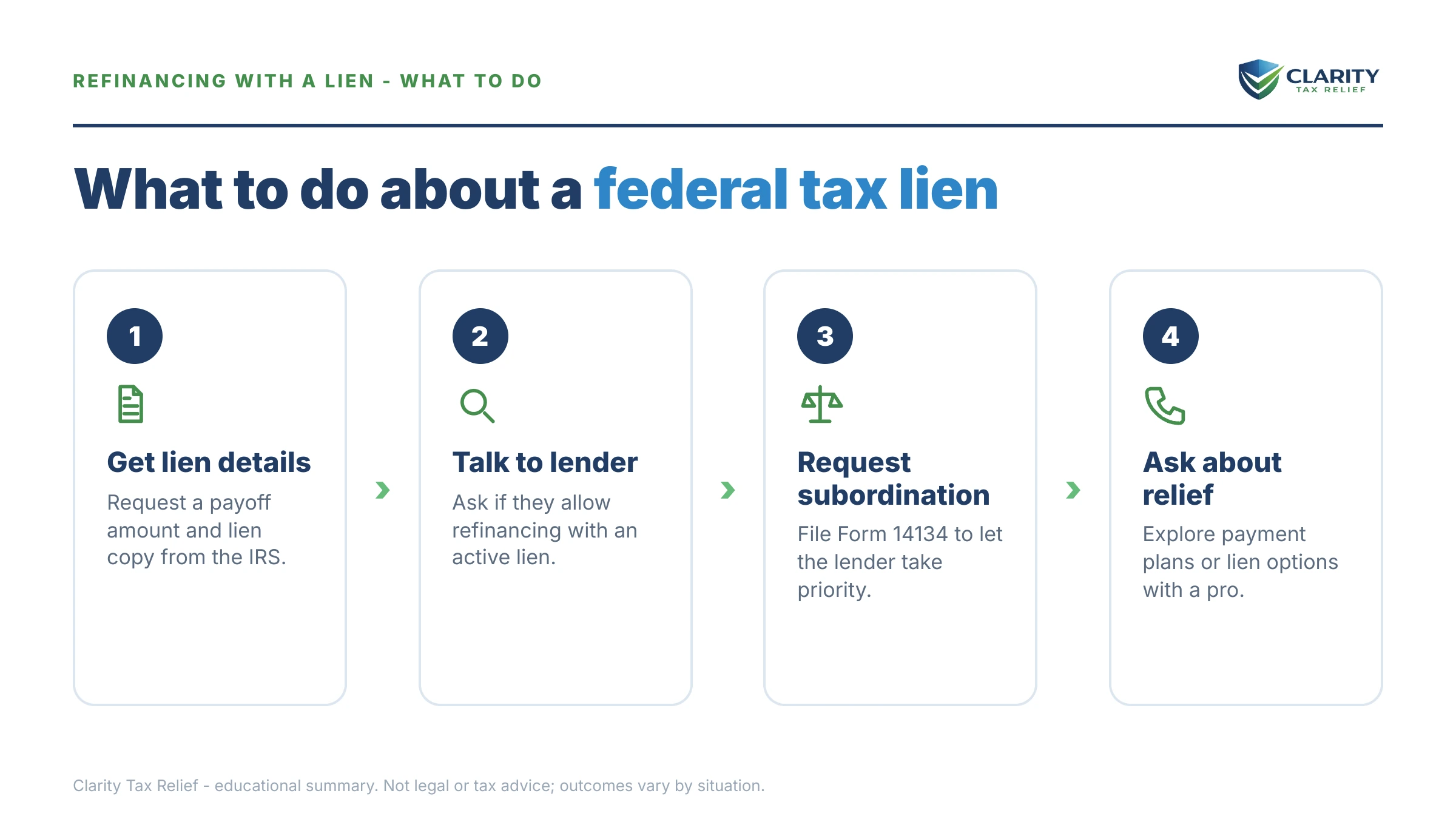

- Pull the recorded lien and a current payoff. Get the Notice of Federal Tax Lien from your title report or county recorder and request an up-to-date payoff amount through your IRS online account — the recorded figure is stale the day it's printed.

- Tell your loan officer before underwriting finds it. Disclose the lien now and pick the path together: payoff at closing if your equity covers it, subordination if you're keeping the balance on a payment plan.

- Order the official payoff letter (payoff path). Have the title or escrow company request an IRS payoff figure good through your closing date and write the payment into the settlement statement so it's paid directly from loan proceeds.

- File Form 14134 early (subordination path). Send the complete application — appraisal, loan estimate, and title report included — to the IRS at least 45 days before your settlement date.

- Confirm the certificate after closing. Verify the Certificate of Release or Subordination is issued and recorded with the county, and check your account transcript for code 583 if the lien was released or withdrawn.

The IRS's own subordination instructions and Publication 784 are linked from the Form 14134 page at IRS.gov.

Check your transcript before you apply: the lien codes that matter

Your IRS account transcript tells you the lien's official status before the title company does — and catching a stale or already-resolved lien early can save your closing date.

| Transcript code | What it means | What to do before you apply |

|---|---|---|

| Code 582 | A lien indicator is on your account — a Notice of Federal Tax Lien was filed | Pull the recorded notice from county records and request a current payoff; choose your path before underwriting flags it |

| Code 583 | The lien was released or withdrawn | Get the certificate and hand a copy to your title company — county records sometimes lag behind the IRS |

| Code 971 | A notice was issued — often Letter 3172, telling you the lien was filed | Match the date to the lien filing; if it's recent, ask an experienced tax professional whether appeal rights are still open |

| Code 530 | Your account is in currently-not-collectible (hardship) status | Collection is paused, but the recorded lien usually stays — it still must be paid or subordinated to close |

When you can handle this yourself — and when help changes the outcome

Plenty of lien refinances close without professional help. If your equity covers the payoff, the paying-at-closing path is mostly the title company's job: they order the payoff letter, they disburse, the release follows automatically. A single-year lien with an accurate balance and a cooperative closing timeline is a DIY situation.

Experienced help changes the outcome when the file is messier: a closing date inside the 45-day subordination window, where the application has to be complete and correct the first time; multiple tax years or multiple recorded liens; a balance you dispute or believe was already paid; divorce-entangled joint liability where innocent spouse relief might remove your share entirely; or self-employment income that complicates both the new loan and the IRS financial picture at once. In those cases the sequencing — which certificate to request, what to pay first, what to document — determines whether the loan closes on schedule.

The IRS's plain-language overview of how liens work, including payoff and certificate requests, is at Understanding a federal tax lien, and payment-plan setup lives at IRS payment plans.

Terms on your lien paperwork, decoded

- Notice of Federal Tax Lien (NFTL): the public document (Form 668(Y)) the IRS records at your county — the filing your title search found.

- Release: the IRS's confirmation the lien is satisfied, issued within 30 days of full payment.

- Withdrawal: stronger than a release — the public filing is pulled as though it never existed, even though the debt may remain.

- Subordination: the IRS agrees to stand behind a specific new lender in line; the lien stays recorded but stops blocking the loan.

- Discharge: one specific property is removed from the lien's reach; the lien survives against everything else.

- Payoff letter: the official IRS figure, good through a stated date, that a title company needs — always higher than the recorded lien amount.

- CSED: the 10-year collection deadline; a lien self-releases when it expires unless refiled, though waiting it out rarely fits a refinance timeline — you can estimate your date with our CSED Calculator.

Refinancing with a tax lien: your questions, answered

Does an IRS tax lien show up on my credit report when I refinance?

No — the three credit bureaus removed all tax liens from credit reports in 2018, so the lien is not hurting your score. Lenders find it anyway: every refinance includes a title search of county records, where the Notice of Federal Tax Lien is recorded. Expect the underwriter to condition your approval on resolving it, even with excellent credit.

How long does IRS lien subordination take?

Plan on 30 to 45 days from a complete Form 14134 application to a decision, which is why the IRS asks you to apply at least 45 days before your settlement date. Incomplete applications — missing the appraisal, the loan estimate, or the title report — are the most common cause of delay. There is no IRS fee for the application.

Can I pay off an IRS lien with cash-out refinance money at closing?

Yes, and it is often the cleanest path when your equity covers the balance. The title company requests an official payoff amount from the IRS, pays it directly from loan proceeds at settlement, and the IRS must issue a Certificate of Release within 30 days of full payment. Order the payoff quote early — the recorded lien amount understates what you owe once interest and penalties are added.

Will the IRS remove the lien if I just set up a payment plan?

Not automatically. A payment plan stops enforcement but leaves the recorded lien in place. If you owe $25,000 or less and convert to a direct-debit installment agreement, you can request lien withdrawal on Form 12277, typically after three consecutive direct-debit payments. Withdrawal pulls the public filing entirely, which is stronger than a release for a lender reviewing your title.

What is the difference between lien subordination and lien discharge?

Subordination (Form 14134) keeps the lien on your property but moves the new lender ahead of the IRS in priority — it exists specifically for refinances. Discharge (Form 14135) removes one property from the lien entirely and is mainly used when selling. For a refinance where you keep the home and the debt, subordination is almost always the right application.

Can I refinance with an FHA or VA loan if I have an IRS lien?

Often yes, if the debt is under control. Government-backed programs generally accept an active IRS payment agreement with a documented history of on-time payments, though individual lenders can add stricter overlays. Conventional lenders vary more widely. Either way, the recorded lien itself still has to be paid, subordinated, or withdrawn before the new loan can take first position.

My divorce decree says my ex pays the tax debt — why is the lien still on my house?

Because the IRS is not bound by your divorce decree. If the debt comes from a jointly filed return, both spouses remain fully liable to the IRS, and the lien attaches to property either of you owns. Your decree gives you a claim against your ex, not against the lien. Innocent spouse relief may help in some cases, but the lien must still be addressed to close your refinance.

Your next 24 hours

- Find the recorded lien. Pull the Notice of Federal Tax Lien from your title report (or the county recorder) and note the amount, tax years, and recording date — then request a current payoff figure through your IRS online account, because the recorded number is already out of date.

- Gather your file. Your loan estimate, most recent mortgage statement, last filed tax return, and — if you're divorced — the pages of your decree covering the house and the tax debt.

- Get a free lien review. If your closing is anywhere near the 45-day subordination window, don't guess at the right path — call (888) 825-7779 or use the 2-minute form at the top of this page and an experienced tax professional will map payoff vs. subordination vs. withdrawal against your actual closing date.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.