Hardship & Liens

Does CNC Stop a Tax Lien? Lien Filing During Hardship Status (2024)

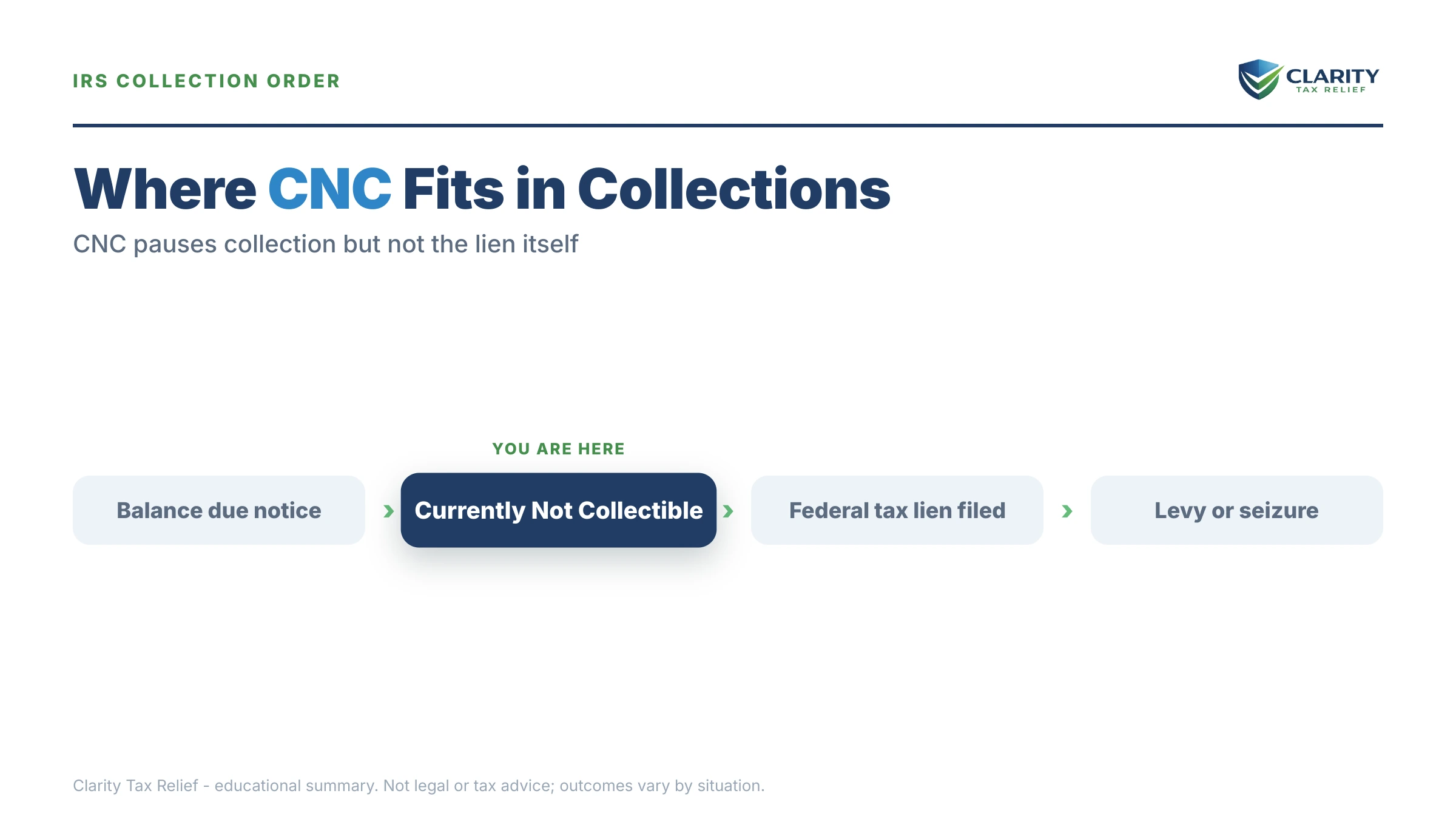

The short answer: does CNC stop a tax lien? No. Currently Not Collectible (CNC) status pauses active collection — wage garnishments and bank levies — but it does not stop the IRS from filing a Notice of Federal Tax Lien. On larger balances, the IRS often files a lien at the same time it approves hardship status.

Got a lien notice while in hardship status?

Send us a photo of the letter. An experienced tax professional will explain exactly where you stand, whether the lien can be withdrawn, and what your real options are — free, confidential, and no pressure.

⏱ Good to know: if the IRS does file a lien, you generally have 30 days from the date on the Letter 3172 to request a Collection Due Process hearing — your formal chance to challenge the filing. After a debt is fully resolved, the lien is normally released within 30 days.

What CNC status actually does — and doesn't do

Currently Not Collectible is the IRS's way of saying, "We agree you can't pay right now." When the IRS reviews your income and your allowable living expenses and finds there's nothing left over each month, it can place your account in CNC and stop trying to take money from you.

That protection is real and important. While you're in CNC, the IRS won't garnish your paycheck, won't levy your bank account, and won't seize your Social Security. If you're in a true financial crisis, this is the breathing room that keeps the lights on.

But CNC has clear limits. It does not:

- Erase or reduce the tax you owe.

- Stop penalties and interest from continuing to add up.

- Prevent the IRS from filing a federal tax lien.

That last point catches a lot of people off guard. You can do everything right, get approved for hardship status, and still open the mailbox to find a lien notice. It feels like a contradiction — but to the IRS, it isn't. For a deeper look at how the program works, see our honest guide to Currently Not Collectible status.

Why the IRS files a lien during hardship status

A federal tax lien isn't a seizure. It's a legal claim — a public notice that says the government has a stake in your property if you sell it or come into money. A levy takes; a lien just marks. If the difference is fuzzy, our breakdown of lien vs. levy spells it out plainly.

From the IRS's point of view, that's exactly why a lien fits with CNC. Collection is paused, so the IRS isn't going to take anything from you today. But your debt is still on the books, and the IRS wants to protect its position in case your finances improve, you sell a house, or you inherit money down the road. The lien holds its place in line.

The biggest factor is how much you owe. The IRS uses an internal dollar threshold for automatic lien filing. Balances below that line frequently go into CNC with no lien at all. Larger balances usually trigger a lien — and being in hardship status doesn't change that math. You can read the IRS's own overview at Understanding a Federal Tax Lien.

What a lien means while you're in CNC

If a lien gets filed, here's what actually changes in your life — and what doesn't:

- Your income is still safe. CNC keeps the levies and garnishments off the table. The lien doesn't reach into your paycheck.

- Your credit isn't directly hit anymore. The major credit bureaus stopped including tax liens on consumer credit reports — but lenders can still find a lien in public records when you apply for a mortgage. See how IRS debt affects your credit for the full picture.

- Selling or borrowing gets harder. A lien attaches to property you own, including your home. If you try to sell or refinance, the lien usually has to be dealt with first.

- The debt still expires on schedule. The IRS generally has 10 years from assessment to collect (the Collection Statute Expiration Date, or CSED). That clock keeps running in CNC, and a lien on file does not extend it.

If a lien arrives, you'll likely get the official notice on a Letter 3172, the Notice of Federal Tax Lien. Don't ignore it — that letter starts your 30-day window to request a hearing.

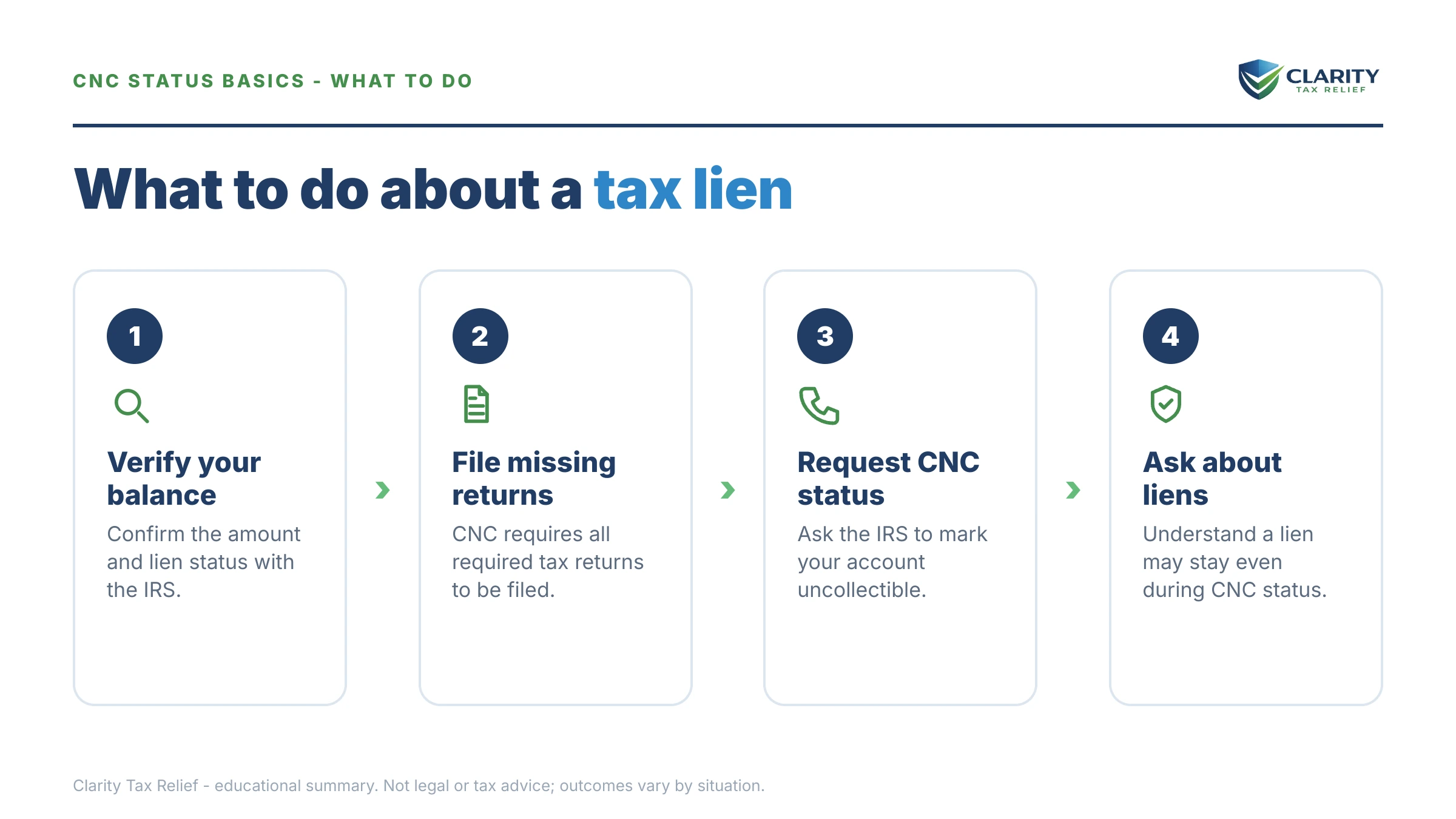

How to respond when a lien shows up during CNC

- Confirm the status of your account. Log into your IRS online account and check that CNC is in place and the lien is tied to the right years and amounts.

- Mind the 30-day deadline. If you want to challenge the lien filing, request a Collection Due Process hearing within 30 days of the Letter 3172 date.

- Ask whether a withdrawal fits. In limited situations, the IRS will withdraw a lien notice — for example, if you enter a direct-debit installment agreement on a qualifying balance. Our walkthrough of the lien withdrawal request on Form 12277 explains who qualifies.

- Plan for a sale or refinance. If you need to sell or borrow against property, the IRS offers a lien discharge or subordination so a deal can close. These are separate requests from CNC.

- Stay compliant going forward. File every return on time and stay current on new taxes. A new balance can knock you out of CNC and re-start collection.

Is there any way to keep a lien off your record?

There's no guaranteed way to block a lien — and you should be cautious of anyone who promises one. Anyone telling you they can "settle for pennies on the dollar" or "guarantee no lien" before reviewing your finances is selling you something, not helping you.

That said, a few honest moves can lower your odds, depending on your situation:

- Keep the balance down. Paying a balance below the IRS lien-filing threshold sometimes avoids a lien entirely. If you owe a large amount, see our guide to the "IRS hardship program," explained honestly.

- Ask the IRS not to file. When you set up your account, you or your representative can sometimes make the case that a lien isn't needed to protect the government's interest. It's not guaranteed, but it's worth raising.

- Use a direct-debit installment agreement instead of CNC when you can afford a small payment — that path can open the door to a later lien withdrawal that pure CNC does not.

- Wait out the statute. If your hardship is long-term and the CSED is approaching, the debt — and the lien with it — can expire without you paying it in full.

If the lien is causing real harm the IRS won't fix, the independent Taxpayer Advocate Service can sometimes step in. You can also read more about how the IRS can temporarily delay the collection process on its own site.

The bottom line

CNC and a tax lien do two different jobs. CNC protects your income today. A lien protects the government's claim for tomorrow. They can — and often do — exist at the same time. So if you're hoping hardship status will keep a lien off your record, plan for the possibility that it won't, and focus your energy on the moves that actually matter: protecting your paycheck, staying compliant, and watching the 10-year clock run down.

CNC and tax lien questions, answered

Does CNC status stop the IRS from filing a tax lien?

No. Currently Not Collectible status pauses active collection — wage garnishments and bank levies — but it does not stop the IRS from filing a Notice of Federal Tax Lien. In fact, the IRS often files a lien when it places larger balances into CNC, to protect its claim while collection is paused.

What does CNC actually protect me from?

CNC stops the IRS from taking your paycheck, your bank account, your Social Security, and other income while the status is in place. It does not erase the debt, stop penalties and interest from adding up, or prevent a federal tax lien. It buys breathing room, not forgiveness.

Can I be in CNC and still avoid a tax lien?

Sometimes. Whether the IRS files a lien depends largely on how much you owe — balances under the lien-filing threshold often see no lien, while larger balances usually do. There's no guaranteed way to block a lien, but keeping the balance lower, staying compliant, and asking the IRS not to file can help in some cases.

Does the 10-year collection clock keep running in CNC?

Yes. The IRS generally has 10 years from assessment to collect a debt (the CSED). That clock keeps running while you're in CNC, so time in hardship status counts toward the deadline. If your finances never recover, the debt can expire when the 10 years run out — a lien on file does not extend that clock.

How do I get the lien removed after I'm in CNC?

A lien is normally released within 30 days after the debt is paid, settled, or expires under the 10-year statute. While you still owe, you may be able to request a lien withdrawal using Form 12277 in limited situations, or a discharge or subordination if you need to sell or refinance. CNC alone does not remove a lien.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.