IRS Relief Programs

IRS Hardship Program in 2026: What It Really Is and Who Actually Qualifies

The short answer: the IRS hardship program is the everyday name for Currently Not Collectible (CNC) status — a real IRS designation that pauses levies, garnishments, and collection when paying would leave you unable to cover basic living expenses. It doesn't erase the debt: interest keeps accruing, and the IRS rechecks your income.

You owe about $8,900, a refinance is on the calendar, and somewhere between the collection notices and the ads you heard there's an "IRS hardship program" that makes it all stop. The program is real — it's just not called that. And for a homeowner about to face a mortgage underwriter, it can help you or quietly work against you, depending on how it's used.

This guide covers what the hardship program actually is, the expense test the IRS uses to grant it, and the honest math on when it's the right tool. You'll also see what hardship status looks like on a real IRS account transcript — the image below shows exactly where the marker appears on your own.

⏱ The real clock: there is no application deadline for the IRS hardship program — but interest compounds daily and the 0.5% monthly failure-to-pay penalty is adding to your balance right now. The automated notice sequence keeps escalating until you pay, arrange payments, or are approved for hardship status.

What the IRS hardship program actually is

The "IRS hardship program" is the marketing name for Currently Not Collectible status — internally, the IRS calls it status 53, and it appears on your account transcript as code 530. There is no application form labeled "hardship program," no enrollment window, and no fee. It is a determination the IRS makes about your account after looking at your finances.

When the IRS grants it, active collection stops: no wage garnishment, no bank levy, no threatening letter cycle. The debt itself stays on the books and keeps growing with interest and penalties. Our guide to IRS Currently Not Collectible status covers the status itself in full detail.

"Hardship" at the IRS actually maps to three different mechanisms, and knowing which one you need matters:

- CNC status — the ongoing pause most people mean when they search "IRS hardship program."

- Economic-hardship levy release — an emergency release under IRC §6343 when a levy that's already in motion is taking money you need to live. See levy causing hardship.

- Offset bypass refund — a narrow rescue that can release a tax refund before the IRS seizes it, in cases like pending eviction. See offset bypass refund for hardship.

One warning up front: some companies advertise the "hardship program" as if it were a secret settlement. It isn't a settlement at all, and requesting it costs nothing. Anyone charging you to "enroll" you in a program that doesn't reduce the debt should explain exactly what work they're doing for that fee.

How to qualify for the IRS hardship program in 2026

You qualify for IRS hardship status when your monthly income is fully consumed by IRS-allowable living expenses, proven with a financial statement — usually Form 433-F. There is no fixed income cutoff. The IRS compares what comes in each month against what it considers necessary to keep your household running: housing and utilities, food and clothing, transportation, health care, and court-ordered payments.

The catch is the word "allowable." The IRS doesn't accept your actual budget at face value — it caps most categories using its published allowable living expense standards, which vary by county and family size. A $900 car payment or private school tuition generally won't count, no matter how real those bills are.

If your income minus allowable expenses is zero or negative, you have a legitimate case. If there's money left over, the IRS will expect it as a monthly payment instead. The full walkthrough of the test lives in our hub on how to qualify for CNC, and the CNC income limits guide shows the expense math with real category caps. If you live on fixed benefits, the analysis has its own wrinkles — see IRS hardship on Social Security.

What happens if you do nothing

IRS collection escalates automatically whether or not you ever get around to requesting hardship status — searching for the program pauses nothing. On an unpaid balance, the sequence runs like this:

- First bill (CP14) — the balance with penalties and interest itemized. No enforcement yet, but the clock on the notice sequence starts.

- Reminder notices (CP501/CP503) — the balance regrows with each one as monthly penalties post.

- CP504, Notice of Intent to Levy — the IRS can now take your state tax refund, and a federal tax lien becomes a live possibility.

- LT11 or Letter 1058, Final Notice — a 30-day window with Collection Due Process appeal rights. After it closes, the IRS can garnish wages and levy bank accounts.

- Levy — a bank levy holds funds for 21 days before they leave; a wage levy is continuous until released.

Here's the part most people miss: hardship approval is not retroactive. CNC protects you from the day the IRS grants it forward. If a levy lands while you're still deciding, you're then fighting for an emergency release instead of calmly submitting a financial statement — a harder, faster-moving problem. In 2026, with IRS phone staffing down sharply after the 2025 workforce cuts, the automated levies keep firing while the humans who can undo them are harder to reach.

Not sure you'd pass the IRS hardship test?

Send us your notice and your basic monthly numbers. An experienced tax professional will run the same allowable-expense math the IRS uses and tell you — free — whether hardship status, a payment plan, or something better fits your situation, before another month of interest posts to the balance.

IRS hardship status vs. your other options

Hardship status is one of five real paths for a balance you can't pay in full — and for balances under $10,000 it's often not the best one. Here's how the options compare on eligibility, cost, and what each actually does:

| Option | Who typically qualifies | Upfront cost | Effect on your debt and collection |

|---|---|---|---|

| Currently Not Collectible (hardship) | Income ≤ allowable living expenses, proven on Form 433-F | $0 | Levies and garnishments stop; balance keeps growing; refunds still taken; lien possible |

| Short-term payment plan | Can pay in full within 180 days | $0 setup fee | Enforcement pauses while you pay; interest and penalties continue until paid |

| Guaranteed installment agreement | Owe $10,000 or less, can pay within 3 years, clean filing history | Setup fee applies (lower with direct debit) | IRS must accept if you meet the criteria; enforcement stops while you stay current |

| Streamlined installment agreement | Owe $50,000 or less, up to 72 months, no full financial disclosure | Setup fee applies (lower with direct debit) | Predictable monthly payoff; interest and penalties continue on the declining balance |

| Offer in Compromise | Assets plus future income genuinely below the balance; means-tested | $205 fee (waived with low-income certification) | Settles for less if accepted — roughly 1 in 5 offers were accepted in FY2024 |

| Penalty relief (FTA / AEP) | Clean compliance for the prior 3 years | $0 | Removes penalties, not the tax; becomes automatic under AEP starting summer 2026 |

Two notes on that table. First, CNC and an Offer in Compromise use similar financial math but do opposite things — one pauses the debt, the other ends it. Second, penalty relief stacks with any of the others: if your last three years are clean, ask for it regardless of which path you take, and starting summer 2026 the new Automatic Exemption from Penalty applies without a request at all.

What hardship status looks like on your transcript

Transcript code 530 is the official marker that the IRS has placed your account in currently-not-collectible status. If you request hardship relief and want proof it actually happened, your account transcript is where you look — the image on this page shows what an account transcript looks like and where the transaction codes sit. Here are the codes that matter around hardship status:

| Code | What it means | What to do |

|---|---|---|

| 530 | Account placed in CNC / hardship status | Save the confirmation letter; keep filing every return on time to protect the status |

| 971 | A notice was issued — during CNC, often the confirmation or the annual CP71 reminder | Read it; an annual reminder does not mean your status ended |

| 582 | A Notice of Federal Tax Lien was filed on your account | Critical if you plan to sell or refinance — get advice before any closing date |

| 583 | The lien was released or withdrawn | Keep documentation of the release with your mortgage or closing paperwork |

| 196 / 276 | Interest and failure-to-pay penalty posting to the account | Normal during CNC — this is the balance growing while collection is paused |

A worked example: $8,900, a refinance, and the hardship trap

Say you owe $8,900 and plan to refinance your mortgage in about 18 months. Run all three realistic paths — the numbers are hypothetical, but the arithmetic is the arithmetic:

- Hardship status for 18 months. The failure-to-pay penalty alone adds about 0.5% per month — roughly $44 a month, or about $800 over 18 months. Add daily-compounding interest and your $8,900 is realistically past $10,500 by the time you sit down with an underwriter. Worse, the IRS may file a Notice of Federal Tax Lien when it parks a balance in CNC — and a recorded lien is exactly the kind of title problem that stalls a refinance. See does CNC stop a tax lien for why the status doesn't prevent the filing.

- Guaranteed installment agreement. Because the balance is under $10,000, the IRS must accept a plan that pays it off within 3 years if your filing history is clean. $8,900 ÷ 36 months is about $247 a month — a little more in practice to cover accruing interest, or finish a few months early. By closing time you'd show an IRS agreement in good standing with a shrinking balance, which most lenders can work with.

- Short-term plan. If cash flow allows, $8,900 over 180 days is roughly $1,485 a month for six months with a $0 setup fee — and the debt is simply gone before the refinance file is even opened.

The honest conclusion: for this reader, hardship status is probably the wrong tool even if the IRS would grant it. CNC is designed for people who genuinely cannot pay anything — not as a parking spot while life events play out. If $247 a month truly isn't there, then CNC is the right answer, and the smart move is to raise the lien question with the IRS at the moment you request the status, not at closing.

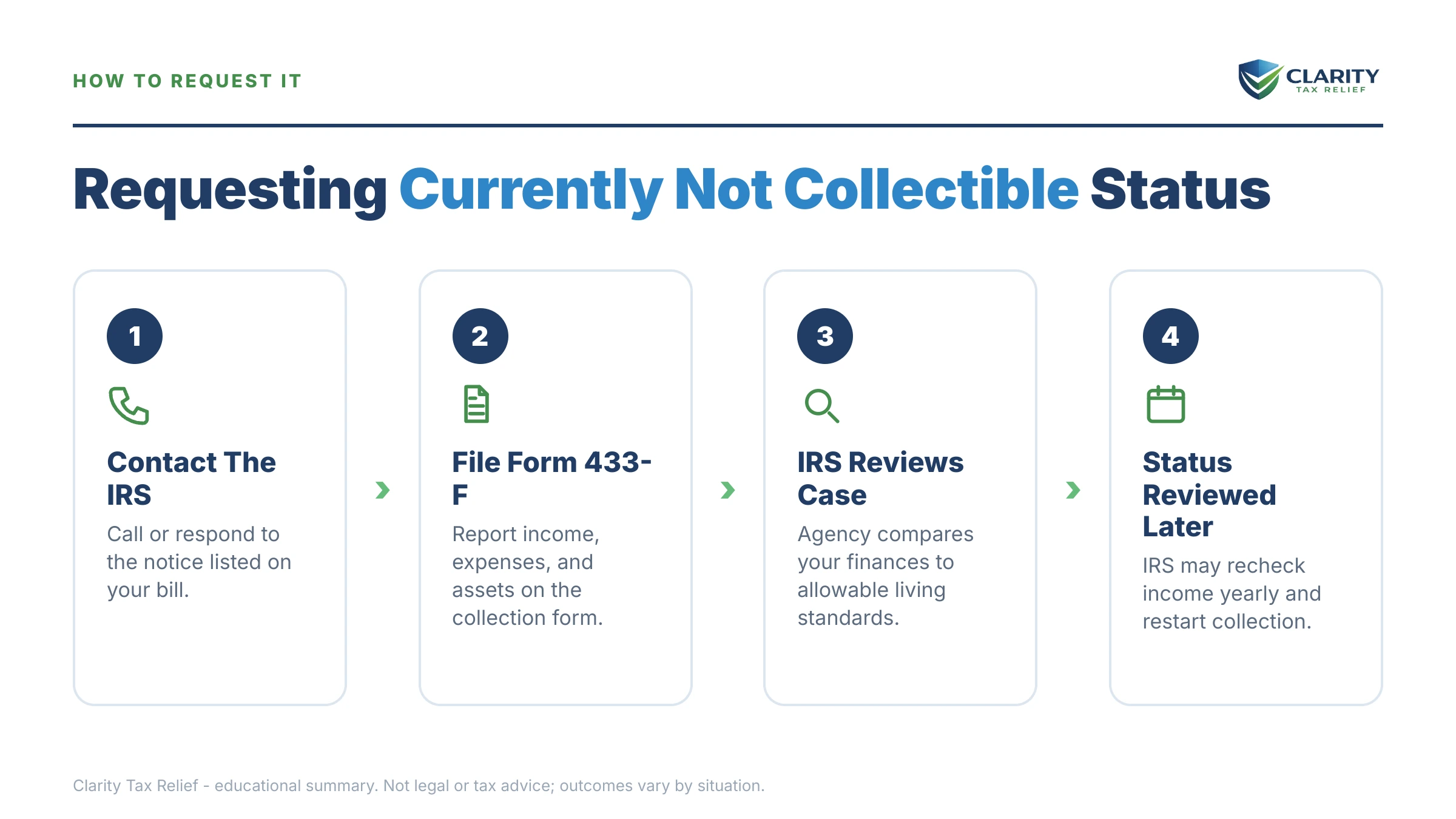

How to request IRS hardship status, step by step

- Pull your exact numbers. Log into your IRS online account and write down the balance, the tax years involved, and any notices on file — the IRS will ask, and guessing hurts you.

- Complete Form 433-F. List every source of monthly income and every monthly expense, and gather proof: pay stubs or benefit statements, your mortgage statement, utilities, insurance, and out-of-pocket medical costs.

- Compare your expenses to the IRS allowable standards. Check your housing, vehicle, and living costs against the IRS Collection Financial Standards for your county and family size — if income minus allowable expenses is zero or negative, you have a case.

- Call the IRS and request currently-not-collectible status. Use the number on your most recent notice, state that paying would create economic hardship, and be ready to read your 433-F figures over the phone or send the form with documentation.

- Get the determination confirmed and calendar the follow-up. Watch for code 530 on your account transcript and the confirmation letter, note any lien determination, and expect an annual CP71 reminder while the status holds.

What happens after you're in the hardship program

Currently Not Collectible status is a pause, not a settlement — and it comes with four ongoing realities you should plan around:

- Your refunds keep getting taken. Every federal refund you're owed is applied to the old balance automatically. That's not a default; it's how the status works.

- Your income is monitored. The IRS watches the income reported on your filed returns. If it rises past the threshold set at approval, collection reactivates — the sequence is covered in CNC status removed. An unfiled return can end the status even faster, so keep filing on time every year.

- You'll get an annual reminder. A CP71 notice arrives each year showing the balance with accrued interest. It's informational, not a demand — but it's also a yearly snapshot of how much the pause is costing you.

- The 10-year clock keeps running. The IRS generally has 10 years from assessment to collect. CNC does not pause that statute — which means some hardship cases quietly run out the clock and the remaining debt becomes uncollectible. You can estimate your own expiration date with our CSED Calculator.

That last point is why CNC is sometimes a strategy rather than a stopgap: for a taxpayer late in the collection statute with no realistic ability to pay, staying in hardship status until the statute expires can be the best legal outcome available. But note that certain events — an Offer in Compromise, bankruptcy, a Collection Due Process appeal — pause the clock and push the finish line out.

When you can handle this yourself

You don't need professional help for every hardship request. Handle it yourself when the picture is simple: one tax year you agree with, W-2 or benefit income, and a budget that's clearly underwater under the IRS standards. In that case, a Form 433-F, your documentation, and one long phone call will usually get it done — and the Taxpayer Advocate Service can step in free if the IRS mishandles a genuine hardship. Likewise, if you owe under $10,000 and could actually pay about $250 a month, skip the hardship route and set up a payment plan online at the IRS payment plans page.

Experienced help changes outcomes in the harder versions of this: a levy already taking your paycheck, multiple unfiled years that must be resolved before the IRS will even discuss hardship, self-employment income the IRS wants to average unfavorably on the 433, a lien filing that threatens a home sale or refinance, or a close-call expense test where how the form is prepared determines whether you land in CNC or in a payment you can't afford. Whichever path fits, any payment you do make should go only through official channels at IRS.gov/payments.

Terms on your account, decoded

- Currently Not Collectible (CNC): the IRS's official designation that collecting from you now would create hardship — the real name behind "hardship program."

- Form 433-F: the collection information statement listing your income, expenses, and assets that the IRS uses to test hardship claims.

- Allowable living expenses: the IRS's published caps on what counts as a necessary monthly expense, by county and family size.

- CSED: the Collection Statute Expiration Date — the end of the IRS's 10-year window to collect, which keeps running during CNC.

- Code 530: the transcript transaction code confirming your account was placed in CNC status.

- Notice of Federal Tax Lien: a public filing that attaches the IRS's claim to your property — possible during CNC, and the main risk for homeowners.

IRS hardship program questions, answered

Is the IRS hardship program real?

Yes, but that's not its official name — the IRS calls it Currently Not Collectible (CNC) status, and it has existed for decades. When granted, the IRS pauses levies, garnishments, and active collection because your finances show you can't cover basic living expenses and the tax. Be wary of companies that market a "hardship program" as new or secret; the status is free to request directly from the IRS.

How do I qualify for the IRS hardship program?

You qualify by showing the IRS that your monthly income doesn't exceed your allowable living expenses — housing, food, transportation, health care — under the IRS's published standards. That usually means submitting Form 433-F with proof of income and bills. There's no fixed income cutoff: a retiree living on $2,100 in Social Security and a family of five earning $70,000 can both qualify or both be denied, depending on their expenses.

Does the IRS hardship program forgive my tax debt?

No — hardship status pauses collection but doesn't reduce what you owe. Interest and the monthly failure-to-pay penalty keep accruing, so the balance actually grows while you're protected. The debt only goes away when the 10-year collection statute (the CSED) expires — a clock that keeps running during CNC — or through a separate program such as an Offer in Compromise.

How long does IRS hardship status last?

Until your finances improve enough for the IRS to reactivate collection — there is no fixed term. The IRS monitors the income on your filed returns and can review the account periodically; if your income rises past the threshold set when you were approved, you'll get notices and eventually return to active collection. Some accounts stay in CNC until the collection statute expires and the remaining debt becomes uncollectible.

Will the IRS file a tax lien if I'm in hardship status?

It can, and on larger balances it often does — CNC stops levies and garnishments, not lien filings. A Notice of Federal Tax Lien attaches to your property and shows up in county records, which matters if you plan to sell or refinance a home. On smaller balances a lien is less common, but ask about the lien determination when you request the status.

Can I get IRS hardship status if I own a home?

Yes — owning a home doesn't disqualify you, because CNC is based on monthly cash flow, not assets alone. The IRS looks at whether your income covers allowable living expenses, and your mortgage payment counts inside the housing standard for your county. Significant home equity can complicate the picture, though: the IRS may ask whether you could borrow against it before granting the status.

Does the IRS take my tax refund while I'm in the hardship program?

Yes — the IRS keeps any federal refund you're owed and applies it to the old debt every year you're in CNC. That offset happens automatically and doesn't count as a default or end your status. In severe situations — an eviction notice, a utility shutoff — an offset bypass refund can release the money, but you must act before the refund is taken.

Does the 10-year collection clock keep running during hardship status?

Yes — and that's the quiet advantage of CNC over most alternatives. The IRS generally has 10 years from assessment to collect (the CSED), and hardship status does not pause that clock the way an Offer in Compromise, bankruptcy, or a Collection Due Process appeal does. If you remain in CNC to the end of the statute, whatever balance is left becomes legally uncollectible.

Your next 24 hours

- Find your real balance. Log into your IRS online account and write down the exact amount owed and the tax years — the notice in your drawer is already out of date by at least a month of interest.

- Gather your 433-F inputs. Pull last month's pay stubs or benefit statements, your mortgage or rent figure, utilities, insurance, and medical costs — the six numbers the hardship test turns on.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form and an experienced tax professional will tell you whether hardship status, a payment plan, or another path protects you best — before another month of penalties and interest posts to the balance.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.