IRS Levies

IRS Levy Release for Hardship: How to Get an Emergency Release in 2026

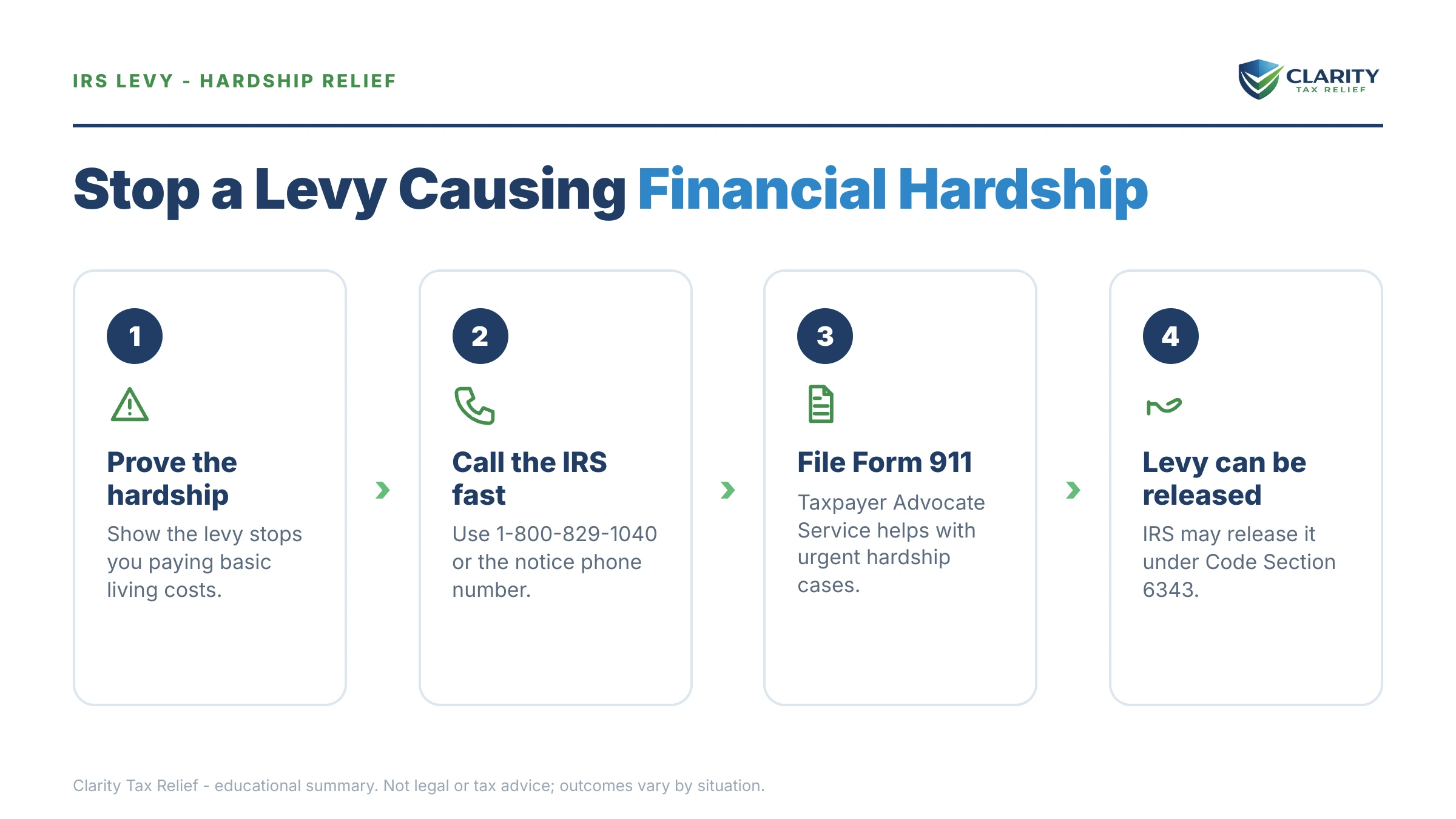

The short answer: an IRS levy release for hardship works because the law requires it — under IRC §6343, the IRS must release a levy that leaves you unable to pay basic, reasonable living expenses. Call the number on the levy paperwork, state the hardship, and prove it with income and expense documents. The debt itself remains.

Your debit card just bounced at the supplier — or the deposit you invoiced never landed — and the bank told you the IRS levied the account this morning. Rent is due, and that account was going to pay it. That panic is real, but so is your leverage: this exact situation is the one the law says the IRS cannot leave in place.

Which release path you use — and how many days you have — depends on which levy form hit you. The image below shows exactly what the levy paperwork looks like and where to find the two details that control everything: the form number and the contact number.

⏱ Your clock: a bank levy comes with a 21-day hold — your bank freezes the money on day one but doesn't send it to the IRS until day 21. A hardship release issued inside that window keeps the money in your account. A wage or 1099 levy has no hold: every day without a release is money gone.

Why the IRS must release a levy that causes hardship

Under IRC §6343, the IRS is legally required to release a levy that prevents you from meeting basic, reasonable living expenses. This is not a favor, a program you apply into, or a discretionary courtesy — it's a mandatory release once hardship is established.

The catch is the word "established." The IRS won't spot the hardship on its own; you have to raise it and prove it. "Basic and reasonable" is measured against the IRS allowable living expenses standards — national and local tables for food, housing, transportation, and health care — not against your actual spending.

For a sole proprietor, hardship has a second dimension the IRS also recognizes: a levy that destroys your ability to earn. If the levied account is the one that buys materials, pays your subcontractor, or covers the insurance you need to stay on job sites, the levy is choking off the very income the IRS wants to collect from. Say that explicitly when you call.

This page covers the emergency release itself — the phone-and-fax sprint. For the underlying legal standard in depth, see our guide to a levy causing hardship, and for every release path (not just hardship), see how to get an IRS levy released.

Which levy hit you — and the clock on each

The form number on the levy paperwork tells you your deadline. Form 668-A is a one-time snapshot levy — it grabs only what existed at the moment it was served. Form 668-W is a continuous wage levy that repeats every payday until released.

Self-employed readers often face the 668-A version served on a client or a bank rather than an employer. A levy on a client reaches only what that client owed you on the levy date — but nothing stops the IRS from serving your other clients with separate levies, one by one. If a wage-style levy is in play, you can estimate what it reaches with our IRS Wage Garnishment Calculator.

| Levy type | Your clock | What a hardship release can still save |

|---|---|---|

| Bank levy (Form 668-A) | 21-day hold before the bank remits the frozen funds | Everything — the money hasn't moved yet if you act before day 21 |

| Wage levy (Form 668-W) | No hold; part of every paycheck, continuously | All future paychecks; amounts already withheld are generally gone |

| 1099 / contractor levy | One-time; grabs only what the client owed you on the levy date | Future invoices to that client — and it signals the IRS to stop before serving your other clients |

| Social Security (FPLP) | Up to 15% of each monthly benefit, ongoing | All future 15% offsets once the release or CNC posts |

| Accounts receivable levy | Attaches to receivables owed on the levy date | New receivables — the cash flow that keeps your business (and income) alive |

The bank-levy window deserves its own deep dive — the mechanics of that hold are covered in our guide to the IRS bank levy 21 days rule.

What happens if you do nothing after the levy

A levy left alone doesn't stabilize — it repeats, spreads, and compounds. Here is the sequence, in order:

- The frozen money leaves. On a bank levy, the 21-day hold ends and your bank remits every levied dollar. There is no undo after that.

- Continuous levies keep taking. A wage levy hits every paycheck and a Social Security levy takes up to 15% of every benefit check until released — neither has an end date short of full payment or the collection statute expiring.

- The IRS levies again. A one-time bank levy can be re-served whenever new deposits land, and each of your clients can be levied separately. What a repeat looks like — and how to prevent it — is covered in IRS levied me again.

- The balance grows underneath it all. The 0.5%-per-month failure-to-pay penalty and daily-compounding interest keep running on the full debt, no matter how much the levy takes.

- Bigger tools come out. A federal tax lien can be filed against your business and personal assets, and if the total debt ever crosses $66,000 (the 2026 threshold), the IRS can certify it for passport denial.

One 2026 reality makes this worse: the IRS workforce is down roughly 27%, but levies are issued by automated systems that never got smaller. The machine that levied you doesn't need a human to do it again — while reaching a human to undo it takes real persistence.

Levy draining you right now?

If it's a bank levy, the 21-day hold is already running — a release has to reach your bank before it ends. Send us the levy paperwork and an experienced tax professional will map your fastest release path free, today.

IRS levy release for hardship vs. your other options

A hardship release stops the taking, but it resolves nothing by itself — the balance survives, with interest accruing. The release buys you the breathing room to choose one of these; the wrong move is treating the release as the finish line.

| Option | Who may qualify | What it does to the levy and the debt |

|---|---|---|

| Economic-hardship release (IRC §6343) | Anyone whose income is at or below allowable living expenses once the levy takes its cut | Releases this levy; the debt remains and interest keeps accruing |

| Currently Not Collectible status | Financials show no ability to pay after ALE-standard expenses | Pauses active collection entirely; balance still grows; IRS re-reviews periodically |

| Streamlined installment agreement | Balance of $50,000 or less; up to 72 months | Levy is typically released once the agreement is in place; penalties and interest continue |

| Partial-pay installment agreement | Full financial disclosure shows you can't pay everything before the 10-year collection statute runs | Monthly payment set to what you can actually afford; IRS revisits your finances over time |

| Offer in Compromise | Assets plus future income total less than the balance; $205 fee and 20% down on lump-sum offers unless low-income certified | Collection generally pauses during review; the IRS accepted roughly 1 in 5 offers in FY2024 |

| Bankruptcy automatic stay | Anyone who files a bankruptcy case | Levy must stop while the stay is in effect; whether the tax itself is dischargeable depends on age-of-debt rules |

For a self-employed reader, the CNC route has its own wrinkles — business income counts, but so do the expenses of producing it. See currently not collectible self employed for that math, and Currently Not Collectible status for the program itself. If bankruptcy is genuinely on the table, start with does bankruptcy stop an IRS levy before assuming it solves the tax.

Say you owe $27,500: a worked hardship example

This is hypothetical, but the math is how the IRS actually runs it. Say you're a sole proprietor who owes $27,500 across two years of self-employment and income tax, and the IRS just levied the business checking account holding $6,400 — next month's rent plus your quarterly estimate.

Your monthly picture: net self-employment income after business costs of $5,100. Necessary expenses at or under the IRS standards: rent and utilities $2,150, health insurance $540, vehicle payment and operating costs $780, food and essentials $750, and $1,000 set aside for current-year estimated taxes (current taxes are an allowable expense). Total: $5,220 against $5,100 of income — you're $120 underwater before the levy took a dime.

That's a textbook §6343 hardship: the levied $6,400 is literally the rent, and your monthly financials show nothing left over. Compare the alternative the IRS might suggest — a streamlined installment agreement at $27,500 ÷ 72 months ≈ $382/month before interest. Your own numbers prove you can't fund that today.

So the realistic sequence is: hardship release inside the 21-day hold to save the $6,400, then CNC status (or a small partial-pay agreement once income recovers) documented on the same financials you just gathered. One set of paperwork, two wins.

How to request an emergency hardship levy release, step by step

- Find the levy form number. Form 668-A means a one-time bank or third-party levy with a 21-day hold; Form 668-W means a continuous wage levy. The phone and fax numbers printed on that paperwork are the ones that matter — not the general IRS line.

- Assemble your hardship proof. Gather three months of bank statements, proof of monthly income (invoices, 1099s, a profit-and-loss), and your rent or mortgage, utility, insurance, and medical bills.

- Call the number on the levy. Say the words "this levy is creating an economic hardship" and ask for a release under IRC §6343. Be ready to walk through your income and expenses line by line — this is a Form 433-F interview conducted by phone.

- Fax your documents the same day. The IRS won't issue Form 668-D on your word alone; whatever the representative asks for, send it before the end of the day and confirm it was received.

- Confirm the release reached the right hands. Ask the IRS to fax Form 668-D directly to your bank's levy department, your employer, or your payer — then call that party yourself to confirm they have it.

- Lock in what comes next. The same week, get into Currently Not Collectible status or an agreement you can afford, so a second levy doesn't follow the first.

Before the call, prepare your numbers using our Form 433-F walkthrough — the interview follows that form's categories almost exactly, and stumbling on a line item is the most common reason a release call ends with "send more documentation" instead of a same-day fax.

If the collections line stalls you while a genuine hardship is unfolding — the money leaves in days, an eviction notice is posted — the Taxpayer Advocate Service can intervene. File Form 911 or start at taxpayeradvocate.irs.gov; TAS exists precisely for cases where IRS process is causing the harm.

When you can handle this yourself — and when help changes the outcome

You can likely make this call alone if the picture is simple: one levy, all returns filed, and clean documentation that your income doesn't cover ALE-standard expenses. The legal standard is on your side; persistence on the phone is the main cost. If the balance is small enough to pay within 180 days, a $0-setup short-term plan may release the levy without any hardship argument — see the IRS payment plans page.

Experienced help earns its fee when the clock and the complexity collide: a bank levy deep into its 21-day hold, unfiled returns the IRS will demand before releasing anything, multiple clients or accounts levied at once, or self-employment financials where how you present business income decides whether you "qualify" as hardship or get routed to a payment demand. A release request denied for thin documentation burns days you may not have — and a professional who has run this play knows what the collections unit needs to see the first time.

One honest note: a hardship release is means-tested. No one can promise you one, and anyone who guarantees a levy release before seeing your financials is selling, not advising.

Terms on your levy paperwork, decoded

- Levy vs. lien: a levy takes property (money in an account, part of a paycheck); a lien is a legal claim recorded against property you still hold.

- IRC §6343: the statute that requires the IRS to release a levy in specific situations — including when it creates economic hardship.

- Form 668-D: the Release of Levy the IRS faxes to your bank, employer, or payer — the document that actually turns the levy off.

- ALE standards: the IRS's allowable living expense tables — the yardstick for what counts as "basic and reasonable" spending.

- Currently Not Collectible (CNC): account status that pauses IRS collection while your finances show no ability to pay; the debt continues to accrue interest.

- CSED: the collection statute expiration date — generally 10 years after assessment, after which the IRS can no longer collect (certain events pause the clock).

The IRS's own overview of levies — including its statement that a levy causing hardship must be released — is at IRS.gov: Levy.

Hardship levy release questions, answered

How fast can the IRS release a levy for hardship?

A wage or bank levy can be released the same day you prove hardship — the IRS faxes Form 668-D directly to your employer, bank, or payer. In practice it takes as long as it takes to reach a person and verify your financials, which in 2026's understaffed phone environment can mean multiple calls. For a bank levy, everything must happen inside the 21-day hold, or the money is gone.

What counts as economic hardship for an IRS levy release?

Economic hardship means the levy leaves you unable to pay basic, reasonable living expenses — housing, utilities, food, health care, transportation, and current taxes. The IRS measures "reasonable" against its allowable living expense standards, not your actual lifestyle spending. A levy that merely makes life uncomfortable doesn't qualify; one that puts rent, medication, or your ability to keep working out of reach usually does.

Does a hardship levy release erase my tax debt?

No. A release under IRC §6343 removes the levy, not the balance — penalties and interest keep accruing on the full amount you owe. That's why a hardship release should be paired with a resolution the same week: Currently Not Collectible status, a payment plan you can actually afford, or an Offer in Compromise if your finances genuinely qualify.

Can I get back money the IRS already took?

Usually not. Once your bank remits funds after the 21-day hold, or your employer sends withheld wages, that money is applied to your balance and is generally not returned. The IRS can return levied funds in limited situations — such as its own procedural error or a wrongful levy on property that wasn't yours — but a standard hardship release only stops future taking.

Can the IRS levy me again after a hardship release?

Yes. A hardship release covers the specific levy, and the underlying debt survives, so a new levy can follow if your finances improve or you fall out of contact. The IRS typically asks for updated financials before re-levying, but the protection is not permanent — which is why locking in CNC status or an affordable agreement right after the release matters so much.

Is there a 21-day hold on wage levies too?

No. The 21-day hold applies only to bank levies — it gives you a window before the bank remits the frozen funds. A wage levy has no hold and no end date: it takes a slice of every paycheck continuously until the IRS releases it, the balance is paid, or the collection statute expires. That makes speed even more important with wage levies.

Can the Taxpayer Advocate Service stop an IRS levy?

TAS can't override the law, but it can force fast action when a levy causes significant hardship and normal IRS channels are failing you. You request help with Form 911, and a case advocate can push through a release the collections line is sitting on. TAS is free, independent inside the IRS, and especially useful in 2026 while collection phone lines are badly understaffed.

Your next 24 hours

- Find the form number and contact number on the levy paperwork. Form 668-A vs. 668-W tells you whether you're racing a 21-day hold or an every-paycheck drain — and the fax number on that page is where the release will go.

- Gather your hardship file: three months of bank statements, proof of monthly income, and your rent, utility, insurance, and medical bills — the exact documents the release call will demand.

- Get a free levy review before the clock runs. If it's a bank levy, the 21-day hold is already counting down — call (888) 825-7779 or use the 2-minute form and an experienced tax professional will tell you today whether your numbers support a hardship release and what to pair it with.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.