IRS Forms

Form 433-F Instructions: How to Fill Out the IRS Collection Information Statement (2026)

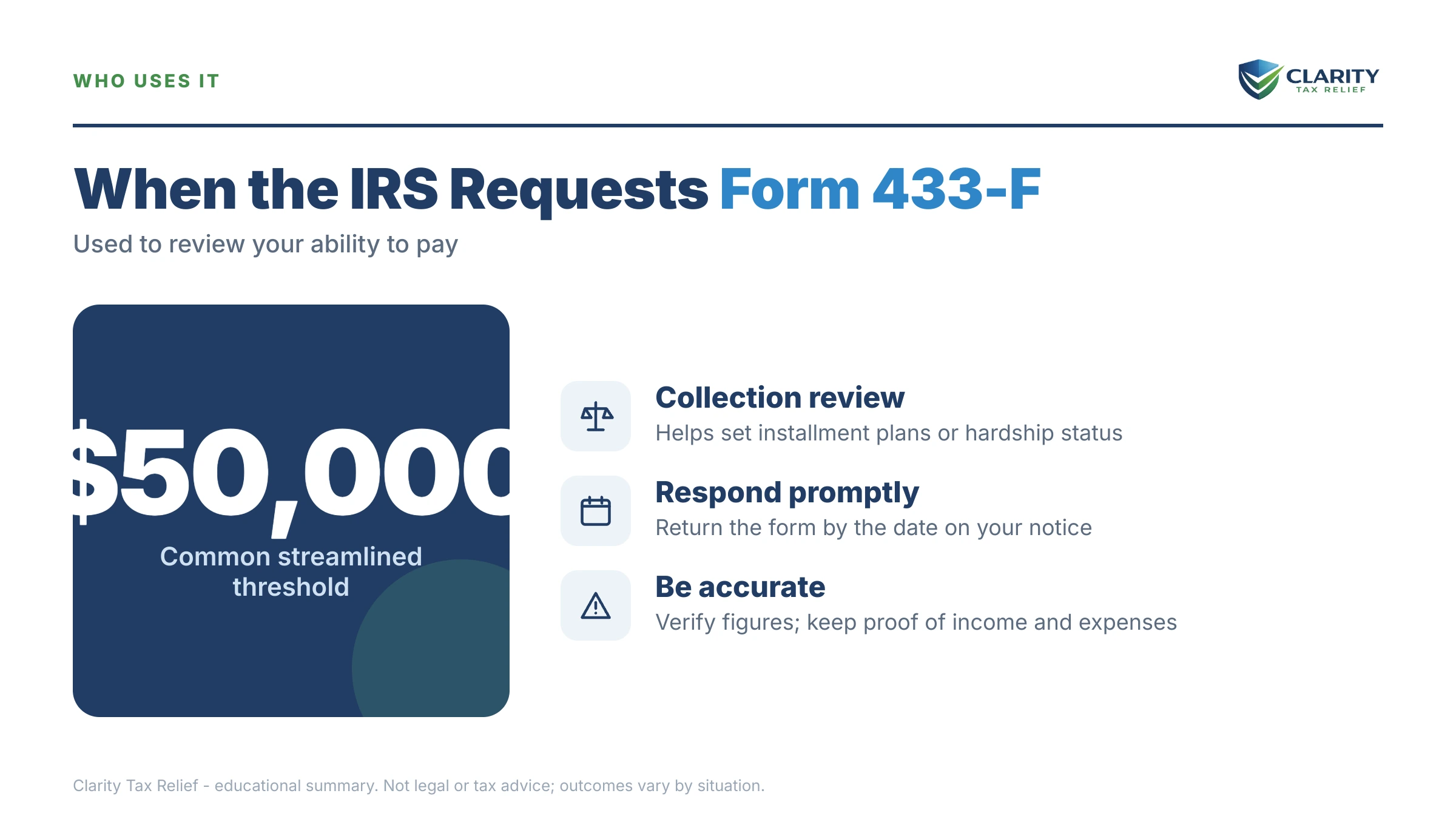

The short answer: Form 433-F is the IRS's two-page Collection Information Statement. The IRS uses it to decide how much you can pay each month — or whether you can pay at all. You usually need it for a payment plan when you owe more than $50,000, or to request Currently Not Collectible hardship status.

You asked the IRS for a payment arrangement — or the IRS asked first, with an LT24 or LT27 letter — and now you're staring at Form 433-F wondering how honest to be about your bank balance. These Form 433-F instructions walk every section, line by line, because the numbers you write here become your monthly payment for years. Unlike the six-plus-page Form 433-A a revenue officer demands, the 433-F is the short form used by the IRS's phone-based collection unit — but it's signed under penalty of perjury, and it's graded against expense caps the form never mentions.

The image below shows you exactly what Form 433-F looks like and where each section sits, so you can follow along as we walk through it.

⏱ Your deadline: the response date printed on the IRS letter that requested the form. LT24 and LT27 letters give you a window measured in days, not months — miss it and the IRS can close your payment-plan or hardship request and put the account back into active collection, while penalties and interest keep accruing monthly either way.

Why the IRS is asking you for Form 433-F

Form 433-F is the financial statement the IRS's Automated Collection System (ACS) requires before it will approve a payment arrangement it can't rubber-stamp. If you're wondering why any IRS letter showed up in the first place, our decoder on why did I get a letter from the IRS covers the system behind it — this page covers only what the 433-F itself demands. In practice, the form gets requested in five situations:

- You owe more than $50,000. Above that line, the online streamlined installment agreement is off the table and the IRS wants financials before setting a payment — see our guide to an IRS payment plan over $50,000.

- You asked for a payment lower than the balance divided by 72 months — the IRS won't take your word that money is tight; it wants the math.

- You requested hardship status. The 433-F is the standard proof for Currently Not Collectible status.

- The IRS sent an LT24 or LT27. The LT24 notice says the IRS needs a completed Form 433 (often plus unfiled returns) to consider your request; the LT27 notice demands the 433-F directly.

- You defaulted a prior plan and need new terms the old numbers no longer support.

One distinction matters before you write anything: the 433-F belongs to ACS — the automated, phone-and-letter side of IRS collections. If a revenue officer has your case, you'll be handed the longer Form 433-A instead. More on that difference below.

| Letter | What it means | Your window | What's at stake |

|---|---|---|---|

| LT24 | The IRS needs a completed Form 433 — and any unfiled returns — before deciding your payment request | The response date printed on the letter | Your pending plan or hardship request stays open |

| LT27 | A direct demand to complete Form 433-F for your account | The response date printed on the letter | No financials, no decision — the request closes |

| CP504 | Intent to levy your state tax refund under IRC §6331(d) — the account is escalating | Act by the date printed on the notice | Your state refund; a federal lien filing becomes more likely |

| LT11 / Letter 1058 | Final Notice of Intent to Levy | 30 days | Your Collection Due Process rights (Form 12153) — then wages and bank accounts |

What happens if you ignore a Form 433-F request

Ignoring a 433-F request doesn't make the IRS forget — it makes the IRS decide without you. The sequence that follows is automated, and it runs in this order:

- Your request closes. Without financial data, ACS can't approve a plan or hardship status, so it denies the request and the account returns to the active collection stream.

- Balance-due notices resume and escalate, ending in a CP504 — the IRS can then seize your state tax refund, and a federal tax lien filing becomes far more likely.

- The final notice arrives — LT11 or Letter 1058 — starting a 30-day clock on your appeal rights. Requesting a hearing with Form 12153 for a CDP hearing is your last structured stop before enforcement.

- Levies begin. A bank levy freezes funds for a 21-day holding period before the money leaves; a wage levy is continuous until released. And here's the irony: to get a levy released, the IRS will ask for — a completed Form 433-F.

- Passport certification. At $66,000 or more in 2026, the IRS can certify your debt as seriously delinquent to the State Department — see passport revoked for tax debt. Entering a payment agreement, which the 433-F unlocks, prevents or reverses it.

In 2026, IRS staffing is down roughly 27% — humans are harder to reach, but the notice-and-levy machinery is automated and never stopped. The form you're avoiding is the off-ramp, not the trap.

About to send the IRS your Form 433-F?

The numbers on this two-page form set your monthly payment for years — and the IRS won't tell you which expenses it will cap. Get your draft 433-F reviewed free before your letter's response date passes.

What your Form 433-F numbers can get you: the options

A 433-F isn't a punishment — it's the key that unlocks every resolution that requires proof of your finances. Which outcome you land depends entirely on what the form shows:

| Option | When it fits | What your 433-F must show |

|---|---|---|

| Streamlined installment agreement (≤ $50,000) | Balance at or under $50,000 — or you pay it down to get there | Nothing — no 433-F required at all |

| Installment agreement over $50,000 | You can retire the debt before the 10-year collection statute runs | Monthly income minus allowed expenses covers the payment |

| Partial-payment installment agreement | You can pay something, but not everything, before the CSED | A documented gap between what you owe and what you can pay |

| Currently Not Collectible | Any payment would leave you unable to cover basic living costs | Allowed expenses equal or exceed your income |

| Short-term plan (up to 180 days, $0 setup) | You can raise the full amount within about six months | Typically none — usually no 433-F needed |

| Offer in Compromise | Assets plus future income genuinely can't cover the debt | Uses Form 433-A (OIC), not the 433-F |

Two strategic notes hide in that table. First, if you can pay the balance below $50,000, you may be able to skip the 433-F entirely and set up a streamlined plan online — the worked example below shows how dramatic that difference can be. Second, if the gap between what you owe and what you can pay is permanent, a partial payment installment agreement lets the rest expire at the collection statute date — but the IRS re-reviews your finances periodically, so the "gap" must be real and provable. Whatever route you take, interest and the late-payment penalty keep accruing until the balance is paid; you can estimate what that adds with our Penalty & Interest Calculator before you commit to terms.

Once ACS approves a monthly amount, the agreement itself is typically confirmed on Form 433-D — the 433-F decides the number; the 433-D locks it in. If you're initiating the request yourself rather than responding to a letter, the request form is covered in our Form 9465 walkthrough.

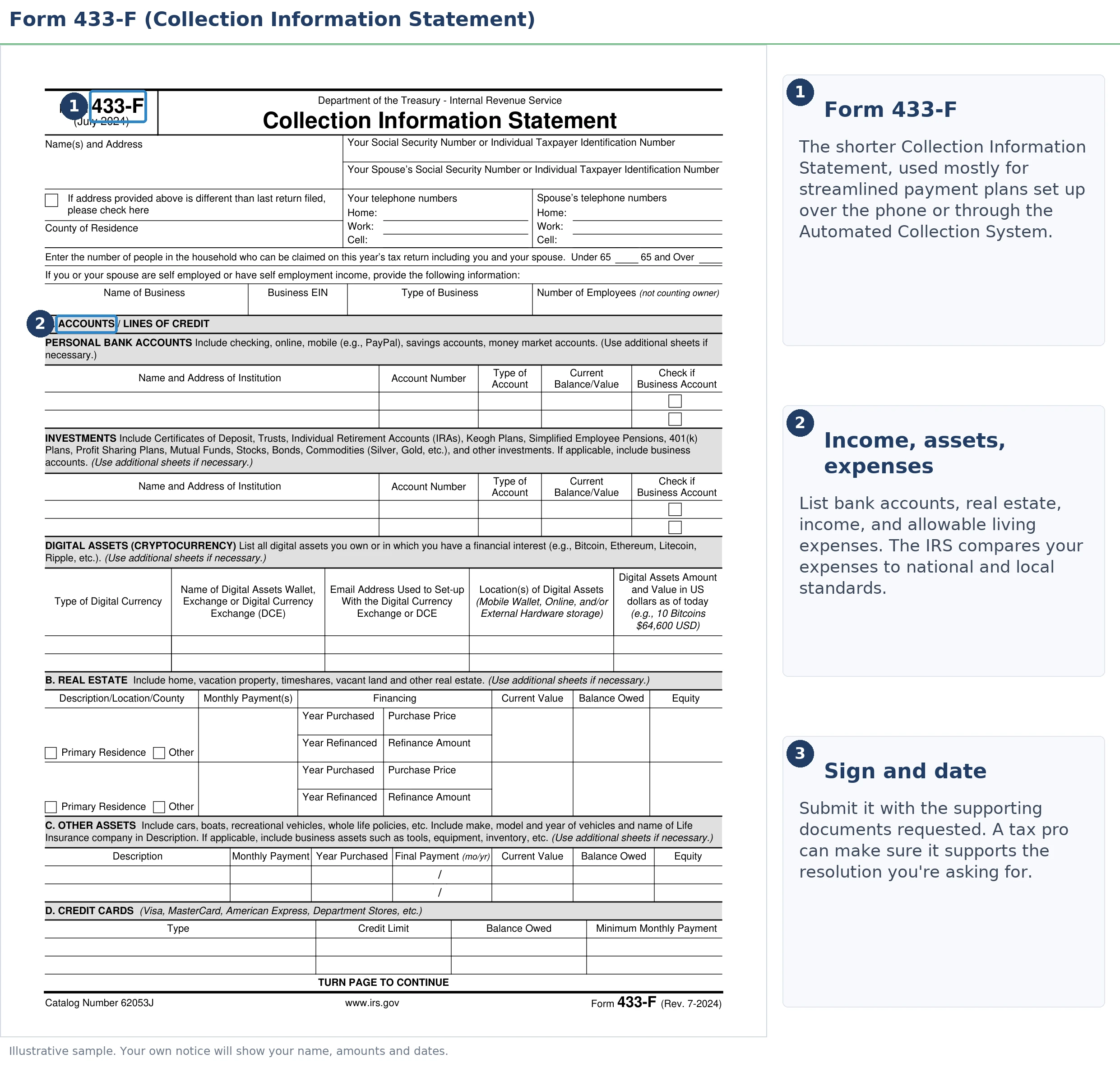

Form 433-F instructions, section by section

Form 433-F has a header block plus eight lettered sections, A through H, covering assets, debts, income, and expenses. The whole form is an equity-and-cash-flow test: Sections A–C measure what you own, F–G measure what comes in, and H measures what the IRS will let you keep spending. Here's the map, then the traps.

| Section | What it asks for | The mistake to avoid |

|---|---|---|

| Header block | Names, SSNs, address, county, household size and dependents | Listing dependents inconsistently with your last filed return |

| A — Accounts / lines of credit | Checking, savings, investment and retirement accounts, online and digital-asset accounts | Omitting small or dormant accounts — the IRS sees the 1099-INT payers |

| B — Real estate | Your home and any other property: value, loan balance, monthly payment | Guessing value carelessly — equity drives what the IRS expects from you |

| C — Other assets | Vehicles, boats, whole-life insurance cash value, other property | Forgetting cash-value life insurance — it counts |

| D — Credit cards | Card issuers, limits, balances, minimum payments | Assuming card payments count as allowable expenses — they generally don't |

| E — Business information | Accounts receivable and payment processors, if self-employed | Skipping it because you "just freelance" — 1099 income means Section E applies |

| F — Employment | Each spouse's employer, pay frequency, gross pay, take-home pay | Mixing weekly and biweekly figures — convert everything to monthly |

| G — Non-wage household income | Self-employment, rental, Social Security, pensions, alimony, distributions | Leaving out irregular income the IRS already sees on 1099s |

| H — Monthly living expenses | Food/clothing/misc., housing and utilities, transportation, medical, other | Claiming actual costs above the IRS caps with no supporting proof |

Three sections deserve extra care:

Section A — including retirement and digital accounts. The current form asks for investment and retirement accounts and online accounts, including digital assets. Retirement money is still an asset in the IRS's eyes: if you have accessible funds, ACS may treat them as a potential source of payment before approving low monthly terms. Don't omit an account hoping it's invisible — banks and brokerages report to the IRS, and a mismatch here undermines everything else on the form.

Sections F and G — the whole household. On a joint liability, one form covers both spouses and both sign. If only one of you owes, the other's income still appears, because the IRS allocates shared expenses proportionally — a non-liable spouse who pays 60% of the rent means only 40% of the housing cost counts toward the liable spouse's allowable expenses. If one of you is self-employed, Section E plus Section G capture the business side; use net monthly profit, not deposits, and be ready to show the arithmetic.

Section H — where cases are won and lost. Your actual bills matter less than the IRS's caps, which brings us to the standards.

The expense caps: how the IRS judges Section H

The IRS grades Section H against its Collection Financial Standards, not against your actual bills. Food, clothing, and miscellaneous costs are capped at national tables by household size; housing, utilities, and transportation are capped at county-level tables. Health insurance, out-of-pocket medical costs, current taxes, court-ordered payments, term life insurance, and child care are treated as necessary when documented.

Anything above a cap is disallowed unless you prove it's necessary for health, welfare, or the production of income. A $2,900 rent payment in a county with a lower housing standard doesn't automatically get honored — which is why two families with identical bills can be told two very different monthly payments. Our plain-English breakdown of the IRS allowable living expenses standards covers each category and the documentation that moves the needle.

The practical takeaway: fill in Section H with your real numbers, but know the caps before you submit. If your actual costs exceed a standard for a defensible reason — a medically necessary vehicle, a special-needs dependent, a commute that produces the income — attach the proof up front rather than waiting for a denial.

Worked example: a married couple owing $76,400

Say you and your spouse filed jointly and owe $76,400 across two tax years. Because that's over $50,000, the online streamlined plan is unavailable and ACS wants a 433-F. Here's how the math plays out — all figures hypothetical:

- Income (Sections F–G): gross wages of $6,900 + $4,300 = $11,200/month; combined take-home of $8,850.

- Claimed expenses (Section H): rent and utilities $2,600; food, clothing, and misc. $1,800; two vehicles $1,700; health insurance $540; out-of-pocket medical $160; term life $60 — total claimed: $6,860.

- IRS-allowed expenses: suppose the county housing standard caps you at $2,300, the national food/clothing table allows $1,600, and transportation is capped at $1,400. Medical and life insurance are allowed as claimed. Total allowed: $6,060.

- Ability to pay: $8,850 − $6,060 = $2,790 per month. At that rate, $76,400 pays off in roughly 27–28 months before accruals — call it about two and a half years with interest and penalties.

Now the alternative that the form itself never suggests. If this couple could raise $26,500 — savings, a family loan, home equity — the balance drops to $49,900, under the $50,000 line. A streamlined 72-month plan on $49,900 runs about $693/month minimum ($49,900 ÷ 72), with no financial disclosure at all. That's a difference of roughly $2,100 per month in required payment, and no IRS review of their bank accounts. (Faster payoff still saves interest — the minimum is a floor, not a strategy.)

One more reason the number matters for this couple: at $76,400, they're above the $66,000 passport-certification threshold for 2026. Getting into an approved agreement — which the 433-F unlocks — is what keeps that certification off the table.

Form 433-F vs Form 433-A: which one you actually need

The IRS has a family of Collection Information Statements, and sending the wrong one wastes your deadline. The 433-F is the two-page short form for cases handled by ACS — most individual balance-due cases worked by letter and phone. The moment a revenue officer is assigned, you'll be required to complete the far more detailed long form instead; our Form 433-A instructions walk that version. Businesses with their own liabilities use Form 433-B, and an Offer in Compromise requires Form 433-A (OIC) attached to Form 656 — the 433-F is never accepted for an offer.

The categories of information are the same across all versions, which cuts both ways: the work you do assembling records for a 433-F transfers directly if your case later escalates — but so do the numbers. Whatever you tell ACS on a 433-F will be compared against anything you file later, so treat the short form with long-form accuracy.

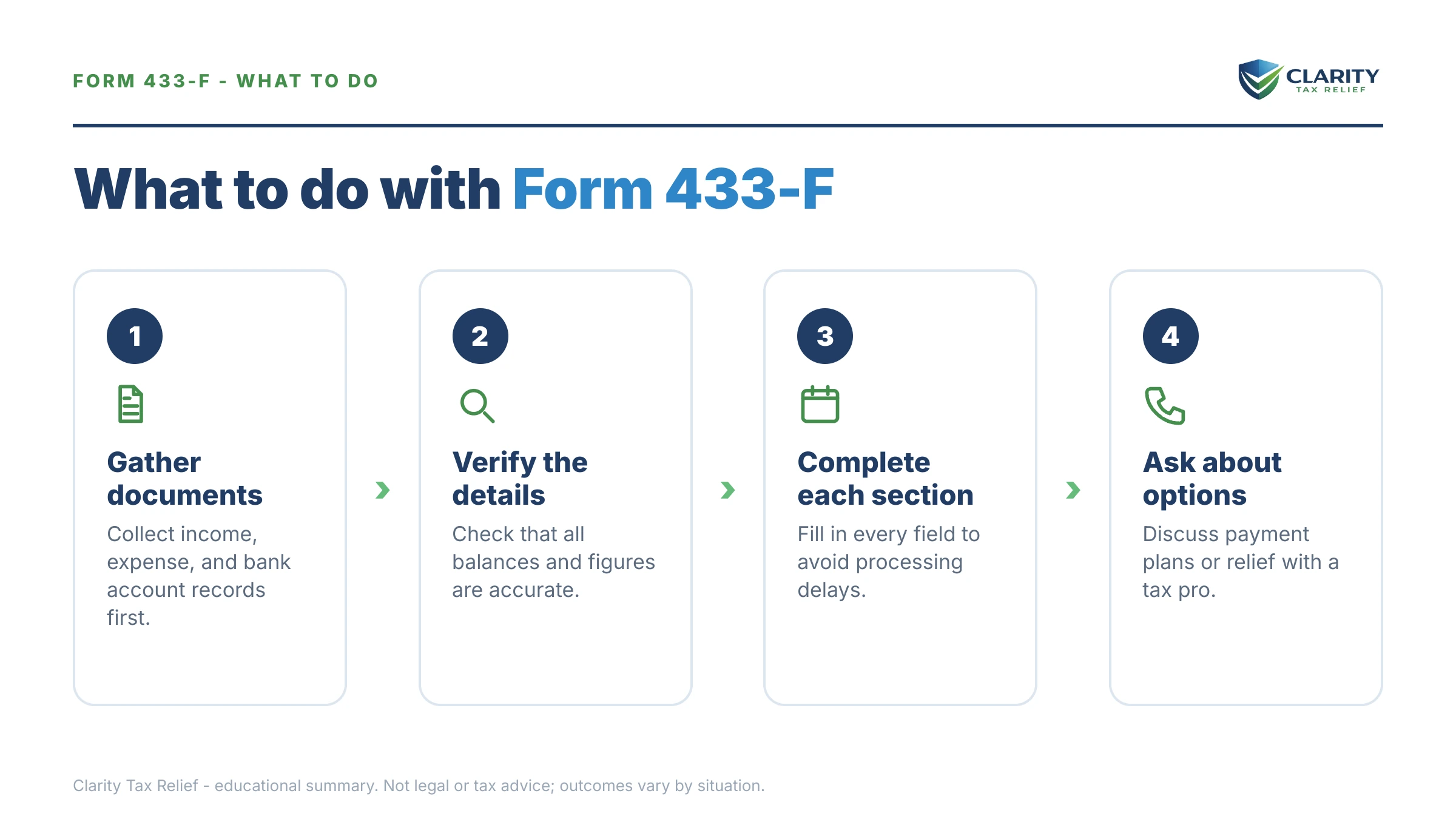

How to fill out and submit Form 433-F, step by step

Download the current form directly from the IRS at Form 433-F (PDF) — never a third-party copy, which may be an outdated revision. Then:

- Gather three months of records. Collect recent pay stubs for both spouses, bank and investment statements, and bills for any expense you plan to claim above the IRS standards.

- List every asset in Sections A through C. Report accounts, real estate, and vehicles at current market value, and note the loan balances against them — equity is what the IRS is measuring.

- Enter all household income in Sections F and G. Include both spouses' wages plus any non-wage income like self-employment, rental, or Social Security, converted to monthly amounts.

- Complete Section H using the IRS expense standards. Claim your actual costs up to each cap, and attach proof for anything above the standards, such as high medical costs or court-ordered payments.

- Sign, date, and send it to the address or fax number on your letter. On a joint liability, both spouses sign under penalty of perjury. Keep a complete copy of the form and every attachment.

- Follow up and stay current. Call the number on your letter to confirm receipt, and keep this year's withholding or estimated payments current so a new balance doesn't sink the request.

What the payment plans themselves cost and how they're structured is on the IRS's own page for payment plans and installment agreements.

When you can handle Form 433-F yourself — and when help changes the outcome

Plenty of people complete a 433-F on their own, and honestly should. If your finances are simple — two W-2 incomes, expenses comfortably inside the IRS standards, no business, no equity surprises — the form is mostly careful bookkeeping. The same is true if your balance is at or under $50,000: you likely don't need the form at all, just a streamlined plan set up online. And if you can pay in full within 180 days, skip the paperwork entirely and use the $0-setup short-term plan.

Experienced help earns its cost in specific situations:

- A levy is already in motion — the 433-F becomes the release document, and speed plus presentation matter.

- Self-employment or business income — how you compute net monthly profit, and whether Section E is complete, changes the payment materially.

- Expenses above the standards — building the health-welfare-or-income-production case takes documentation strategy, not just receipts.

- You're near a threshold — a few thousand dollars of pay-down, a corrected asset value, or a properly allocated non-liable spouse's expenses can be the difference between $2,790 a month and a fraction of it.

- Multiple unfiled years — an LT24 demanding returns plus financials needs sequencing: returns first, then the 433-F, or the whole request stalls.

If you'd rather a professional handle the ACS calls entirely, that requires a power of attorney — our Form 2848 instructions explain how representation works and what it does (and doesn't) authorize.

If a Form 433-F request is sitting on your kitchen table right now, an experienced tax professional can review your draft — and the caps it will be graded against — free at the 2-minute form or (888) 825-7779.

Terms on your 433-F request, decoded

- Collection Information Statement: the IRS's official name for the 433 series — a sworn snapshot of your assets, income, and expenses.

- ACS (Automated Collection System): the IRS's letter-and-phone collection unit; it works cases without a human officer assigned, and it's who reads your 433-F.

- Collection Financial Standards: the national and county expense tables the IRS uses to cap Section H — published at IRS Collection Financial Standards.

- Currently Not Collectible (CNC): a status that pauses active collection when the 433-F shows you can't pay basic living costs and the debt too; the balance remains and accrues.

- Partial-payment installment agreement (PPIA): a monthly plan that won't fully pay the debt before the collection statute expires; requires a 433-F and periodic re-review.

- Penalty of perjury: the legal standard your signature invokes — the statement must be true, correct, and complete, for both spouses on a joint debt.

Form 433-F questions, answered

What is IRS Form 433-F used for?

Form 433-F is the short Collection Information Statement the IRS uses to measure your ability to pay a tax debt. It sets the monthly amount on payment plans that require financial disclosure — generally balances over $50,000 — and it is the standard proof for Currently Not Collectible hardship status. The IRS's Automated Collection System requests it by letter (LT24 or LT27) or by phone.

Do I need Form 433-F if I owe less than $50,000?

Usually not. Balances of $50,000 or less generally qualify for a streamlined installment agreement of up to 72 months with no financial statement at all — you can set it up online. The main exceptions are when you ask for a payment lower than the streamlined minimum, request hardship status, or the IRS specifically sends a letter demanding the form.

What is the difference between Form 433-F and Form 433-A?

Form 433-F is the two-page short form used by the IRS's phone-based Automated Collection System; Form 433-A is the much longer version a revenue officer requires once a case is assigned to a human collector. They ask for the same categories of information, but 433-A goes far deeper. Offers in Compromise use a third version, Form 433-A (OIC) — never the 433-F.

Do I have to include my spouse's income on Form 433-F?

If the tax debt is from a joint return, yes — one Form 433-F covers the household and both spouses sign it. If only one spouse owes, the non-liable spouse's income still appears in the household picture, because the IRS uses it to figure out what share of the shared living expenses the liable spouse actually pays. It doesn't make the non-liable spouse responsible for the debt.

What documents do I need to send with Form 433-F?

Be ready to back up every number: roughly three months of pay stubs and bank statements, plus proof of any expense you claim above the IRS standards, such as health-care bills or court-ordered payments. If you give the information by phone, the agent may still ask you to fax supporting documents before approving anything. Send copies, never originals, and keep a complete set.

Can the IRS reject the expenses I list on Form 433-F?

Yes. The IRS caps most living expenses at its Collection Financial Standards — national tables for food and clothing, county tables for housing and transportation. Claim more than the cap and the excess is generally disallowed unless you prove it's necessary for health, welfare, or income production. That's why two households with identical bills can be told two very different monthly payments.

What happens after I submit Form 433-F?

The IRS reviews your figures against its expense standards, may ask for verification, and then decides: a monthly payment amount, hardship (Currently Not Collectible) status, or a request for more information. A payment plan is typically confirmed on Form 433-D or by letter. Until you have a decision in writing, keep any deadline the IRS gave you and stay current on this year's taxes — new balances can sink a pending request.

Where do I send Form 433-F?

Send it to the exact address or fax number printed on the IRS letter that requested it — LT24 and LT27 letters include the return address, and faxing is usually faster while you're working with the Automated Collection System. There is no single national filing address for Form 433-F, so never mail it to a generic IRS service center. Keep proof of the date you sent it.

Is Form 433-F signed under penalty of perjury?

Yes — the signature block declares the statement true, correct, and complete under penalty of perjury, and on a joint liability both spouses sign. An honest mistake can be corrected by sending updated figures. Deliberately hiding an account or asset is a different matter entirely: it can void any agreement based on the form and create far more serious exposure than the original tax debt.

Your next 24 hours

- Find the deadline and the letter number. Look at the top right of the IRS letter that requested the form — LT24 or LT27 — and circle the response date printed on it. That date, not the form, is your clock.

- Gather the raw material. Three months of pay stubs for both spouses, three months of bank statements, your last filed return, and statements for any retirement or investment account.

- Get the draft reviewed before it goes out. The numbers on a 433-F set your payment for years and are graded against caps the form never shows you. An experienced tax professional will review yours free — start with the 2-minute form or call (888) 825-7779 before your letter's response date passes.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.