IRS Hardship Programs

IRS Currently Not Collectible Status: How CNC Works, Who Qualifies, and the Catch (2026)

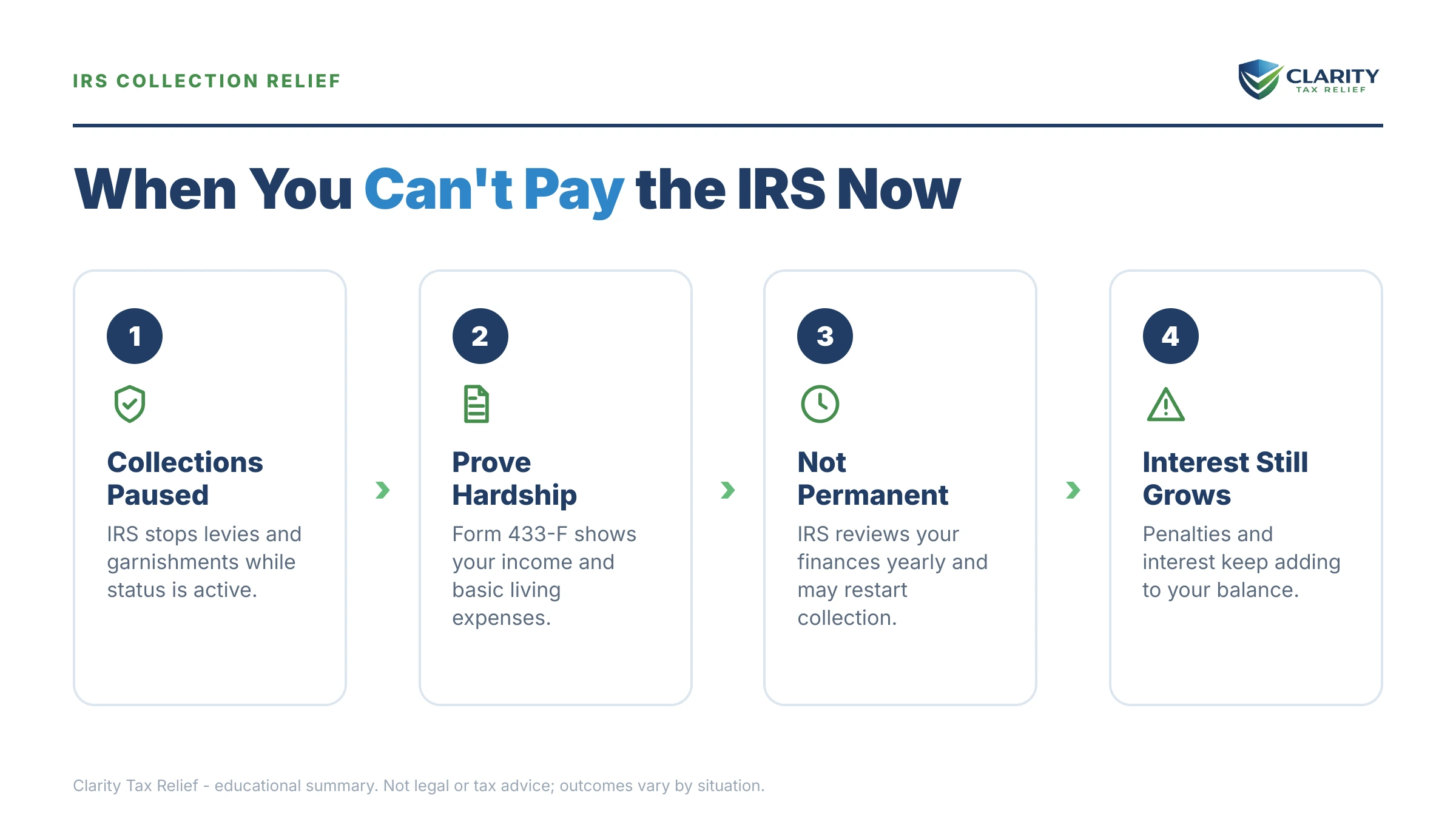

The short answer: IRS currently not collectible (CNC) is a hardship status that pauses levies and garnishments when paying anything would leave you unable to cover basic living expenses. The debt doesn't go away — interest keeps accruing and a lien can still be filed — but the 10-year collection clock keeps running while you're protected.

You've paid the mortgage, the utilities, and the grocery bill, and there is genuinely nothing left over for the balance on the IRS notice. That's not a character flaw — it's arithmetic, and the IRS has a formal status built for exactly this math. Getting into it is a documentation exercise, not a plea for mercy, and this guide walks you through every piece of it.

One thing to know up front: CNC never arrives as a certificate you can frame. It shows up as a code on your IRS account transcript — the image below shows you exactly what that looks like and where to find it.

⏱ The clock that matters: there's no application deadline for CNC — but interest compounds daily and the failure-to-pay penalty adds 0.5% of the balance every month until it caps at 25%. And if an LT11 final notice of intent to levy is already in your mailbox, you have 30 days from its date to preserve your appeal rights.

What IRS currently not collectible status actually is

IRS currently not collectible status stops levies, wage garnishments, and seizures while your account sits in hardship — but the balance, the interest, and the 0.5% monthly failure-to-pay penalty all remain. Internally, the IRS calls it a "status 53" or hardship closing: a collection employee closes your account as uncollectible and the enforcement machinery stands down.

There is no application form titled "CNC." You get the status by proving, with a financial statement — usually Form 433-F — that your allowable monthly expenses equal or exceed your income. The full qualification test is covered in our guide on how to qualify for CNC; this page focuses on what the status actually does, what it costs you, and the strategy around it.

You'll also see CNC marketed as the "IRS hardship program," which makes it sound like a special initiative you apply to. It isn't — it's a collection-status decision — and our honest breakdown of the IRS hardship program label explains what's real versus sales copy. Once granted, the status posts to your account transcript as code 530. The image below shows where that line sits on a real transcript, so you can verify the status yourself instead of taking anyone's word for it.

Who qualifies for CNC hardship status in 2026

You may qualify for CNC if your monthly income, measured against the IRS's allowable living expense standards, leaves nothing over after necessary living costs. The key word is allowable: the IRS doesn't accept your actual budget. It caps housing and utilities at a county-level standard, vehicle costs at set amounts, and food, clothing, and miscellaneous at national figures — our guide to the IRS allowable living expenses standards decodes each category, and the dollar-level math is worked through in CNC income limits.

Three conditions matter beyond the income math:

- Filing compliance. All required returns must be filed. The IRS won't classify an account uncollectible while it can't even see the full debt.

- Assets. If you hold easily-reachable assets — a large bank balance, a paid-off second vehicle — the IRS may ask why those can't pay the debt. Home equity is treated more gently: the IRS rarely pushes a hardship taxpayer to borrow against a primary residence, but significant equity invites questions, so expect to explain it.

- The whole household. On a joint liability, both spouses' income and expenses go on the financial statement. Even on a single liability, the IRS looks at household income to figure out your true share of shared expenses.

There is no fixed income cutoff. A retiree on $2,100 a month can be denied if expenses are low; a family earning $7,000 can qualify if allowable expenses genuinely consume it. The test is the gap, not the gross.

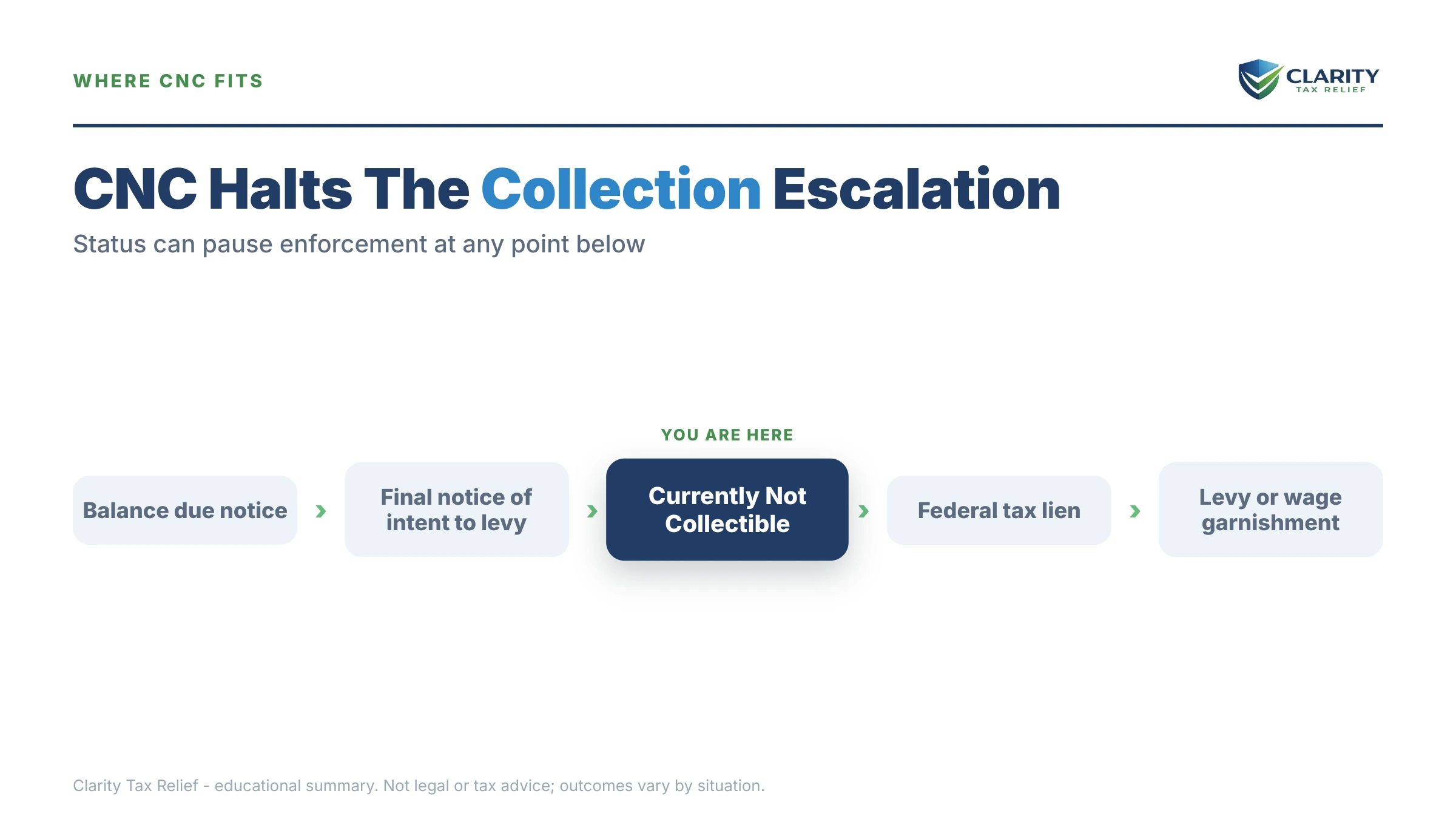

What happens if you can't pay and do nothing

The IRS collection sequence is fully automated, and it escalates from a bill to a levy without a human ever reviewing your hardship. That's the core reason CNC exists — the computer doesn't know you can't pay until someone puts your finances on the record. Left alone, the sequence runs like this:

- CP14 — first bill. You typically have about 21 days from the notice date before the sequence moves.

- CP501 / CP503 — automated reminders. The balance grows monthly; no enforcement yet.

- CP504 — intent to levy your state refund. Under IRC §6331(d), the IRS can now take your state tax refund, and a federal tax lien becomes likely.

- LT11 / Letter 1058 — final notice of intent to levy. A 30-day clock starts on your Collection Due Process rights (requested via Form 12153). After it runs, full levy power is live.

- Levy. A bank levy freezes funds for a 21-day hold before they leave; a wage levy is continuous until released; up to 15% of Social Security can be taken through the Federal Payment Levy Program.

In 2026 this matters more, not less. The IRS workforce was cut roughly 27% in 2025, so reaching a human is harder — but the notices and levies are issued by systems that never stopped. You can request CNC at any point in this sequence, including after a levy hits. But it's a far calmer conversation at the CP503 stage than while your paycheck is being garnished.

Nothing left after the bills — and the IRS notices keep coming?

Get a free CNC eligibility review before the automated sequence reaches the levy stage. An experienced tax professional will run your income against the IRS's own expense standards and tell you honestly whether hardship status — or something better — fits your numbers. Interest and penalties compound every month you wait.

CNC vs. your other options when you can't pay the IRS

CNC is one of five real programs for a balance you can't pay in full, and it's the only one that costs nothing to enter and requires no monthly payment. That doesn't automatically make it the best fit — each option trades something different.

| Option | Typical eligibility | Cost to enter | What happens to the balance |

|---|---|---|---|

| Short-term payment plan | Can pay in full within 180 days | $0 setup | Paid off; interest and penalties accrue until paid |

| Streamlined installment agreement | Balance ≤ $50,000, up to 72 months, all returns filed | Setup fee (lower with direct debit) | Paid monthly while accrual continues |

| Partial-payment installment agreement | Can pay something, but not everything before the CSED; full financials required | Setup fee + financial review | Paid partially; the rest expires at the CSED |

| Currently Not Collectible | Allowable expenses equal or exceed income; financials required | $0 | Collection paused; balance accrues; can expire at the CSED |

| Offer in Compromise | Offer must match what the IRS could realistically collect | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) | Settled for the accepted amount if approved — roughly 1 in 5 offers were accepted in FY2024 |

| Penalty abatement / AEP | Clean 3-year history (first-time abate) or reasonable cause; AEP becomes automatic starting summer 2026 | $0 | Penalties removed; tax and interest remain |

Two comparisons come up constantly. Against a monthly plan, the trade is cash flow versus growth: a plan shrinks the debt while CNC lets it grow — our payment plan vs currently not collectible breakdown shows when each wins. Against a settlement, the trade is speed versus finality: an offer can end the debt for less, but it's slow, means-tested, and pauses the collection clock while pending — see CNC vs offer in compromise for the full decision framework.

Where your balance puts you

The size of the debt changes which doors are open, which thresholds you cross, and how hard the IRS looks at your financials:

| Balance | Realistic options | CNC notes |

|---|---|---|

| Under $10,000 | Guaranteed installment agreement; short-term plan | Lien unlikely; a small monthly plan is often simpler than CNC |

| $10,000–$25,000 | Streamlined plan; CNC; penalty relief | A federal tax lien becomes likely once CNC posts |

| $25,000–$50,000 | Streamlined plan (direct debit helps); PPIA; CNC; OIC | Plans need little disclosure; CNC needs full financials |

| $50,000–$66,000 | Non-streamlined plan with financials, or pay below $50k to go streamlined; PPIA; CNC; OIC | Still under the $66,000 passport line — and CNC blocks certification anyway |

| $66,000–$100,000 | Full financial-review options: plan, PPIA, CNC, OIC | Passport certification risk unless in CNC, a plan, or a pending OIC |

| Over $100,000 | Often assigned to a revenue officer; all options remain, with deeper review | CNC still available — expect asset-by-asset scrutiny |

A worked example: $54,600, a house, and a refinance

Say you owe $54,600 across two tax years, you own your home, and you were planning to refinance this fall. Here's how the CNC math — and the homeowner's complication — actually plays out. (This is a hypothetical illustration, not a client case.)

Your gross monthly income is $4,450. On Form 433-F, your allowable expenses come out like this: mortgage and utilities at $1,985 (within your county's housing standard), vehicle ownership and operating costs at $915, food, clothing, and miscellaneous at the allowance — call it $795 — health insurance at $460, out-of-pocket medical at $85, and current-year tax withholding of $370. Total allowable expenses: $4,610 against $4,450 of income — a $160 monthly deficit. On the IRS's own math, there is nothing to collect, and CNC is a legitimate request.

While the account sits in CNC, the balance still grows. The failure-to-pay penalty alone is 0.5% × $54,600 ≈ $273 per month until that penalty reaches its 25% lifetime cap, plus daily-compounding interest at the rate the IRS sets quarterly. You can model how fast a balance like this grows with our IRS penalty and interest calculator — it estimates, it doesn't promise, but it makes the accrual visible.

Now the refinance twist. At $54,600, you're well over the $10,000 mark where the IRS generally files a Notice of Federal Tax Lien when it grants CNC. That lien attaches to your home, your lender's title search will find it, and most lenders won't close over it. Your realistic paths: ask the IRS to subordinate its lien so the new mortgage takes priority — that's tax lien subordination via Form 14134, and the IRS often agrees when the refinance helps you pay — or pay the lien from closing proceeds if there's enough equity.

One more wrinkle worth thinking through before you call the IRS: if the refinance would cut your mortgage payment by, say, $400 a month, your $160 deficit becomes a $240 surplus — and at the next review, the IRS could reasonably ask for a monthly plan around that number. Alternatively, at $54,600 you're only $4,600 above the $50,000 streamlined-plan ceiling; if family help or a small asset could get you under it, a 72-month plan runs roughly $50,000 ÷ 72 ≈ $695 a month before accrual. On a $160 deficit that's not viable today — which is exactly why sequencing (CNC now, subordination and reassessment after the refinance) usually beats improvising.

What CNC does not do — the three catches

CNC stops enforced collection, but it does not reduce the debt, stop its growth, or keep a lien off your property. Being clear-eyed about the trade is what separates a good CNC decision from a regretted one.

| Stops while in CNC | Continues while in CNC |

|---|---|

| Bank levies (and the 21-day hold pipeline) | Interest, compounding daily |

| Wage garnishments | Failure-to-pay penalty — 0.5% per month, up to 25% |

| FPLP levies on Social Security (up to 15%) | Federal refund offsets applied to the balance |

| New enforced collection actions | Notice of Federal Tax Lien filing (typically over $10,000) |

| Passport "seriously delinquent" certification | CP71 annual balance reminders |

| Demands for a monthly payment | The 10-year collection countdown — which works in your favor |

Catch one: the lien. Granting CNC on a balance over $10,000 usually comes with a Notice of Federal Tax Lien if one isn't already filed. The lien takes nothing from you day to day, but it clouds title on your home — the full picture is in does CNC stop tax lien.

Catch two: refunds. Every federal tax refund you're due gets applied to the balance until it's gone. If you count on a refund each spring, plan without it — or adjust withholding so you stop overpaying into a debt-offset machine.

Catch three: the annual look. Each year you'll receive a CP71 notice restating the balance. It's a reminder, not a reactivation — but the IRS is also comparing each new return you file against the income threshold it recorded when it closed your account. Rising income reopens the case.

The quiet upside: the 10-year collection clock keeps running

The IRS has 10 years from assessment to collect a tax debt, and CNC does not pause that clock. This is the strategic heart of hardship status. Time spent in CNC counts fully toward the Collection Statute Expiration Date — unlike a pending offer in compromise, a bankruptcy, or a CDP appeal, each of which tolls the statute and gives the IRS more runway.

In the $54,600 example, if both years were assessed in 2023, the CSEDs land around 2033. A taxpayer whose hardship never lifts can ride CNC to that date and watch the remaining balance legally expire — the closest thing to genuine forgiveness in the IRS collection system, with no application fee and no settlement negotiation. You can estimate your own expiration dates with our CSED calculator; the dates are account-specific, and prior tolling events shift them.

This is also why the IRS scrutinizes CNC requests on large balances close to the CSED: it knows exactly what the clock is worth. Expect the financial review to be more careful, not less, when expiration is near.

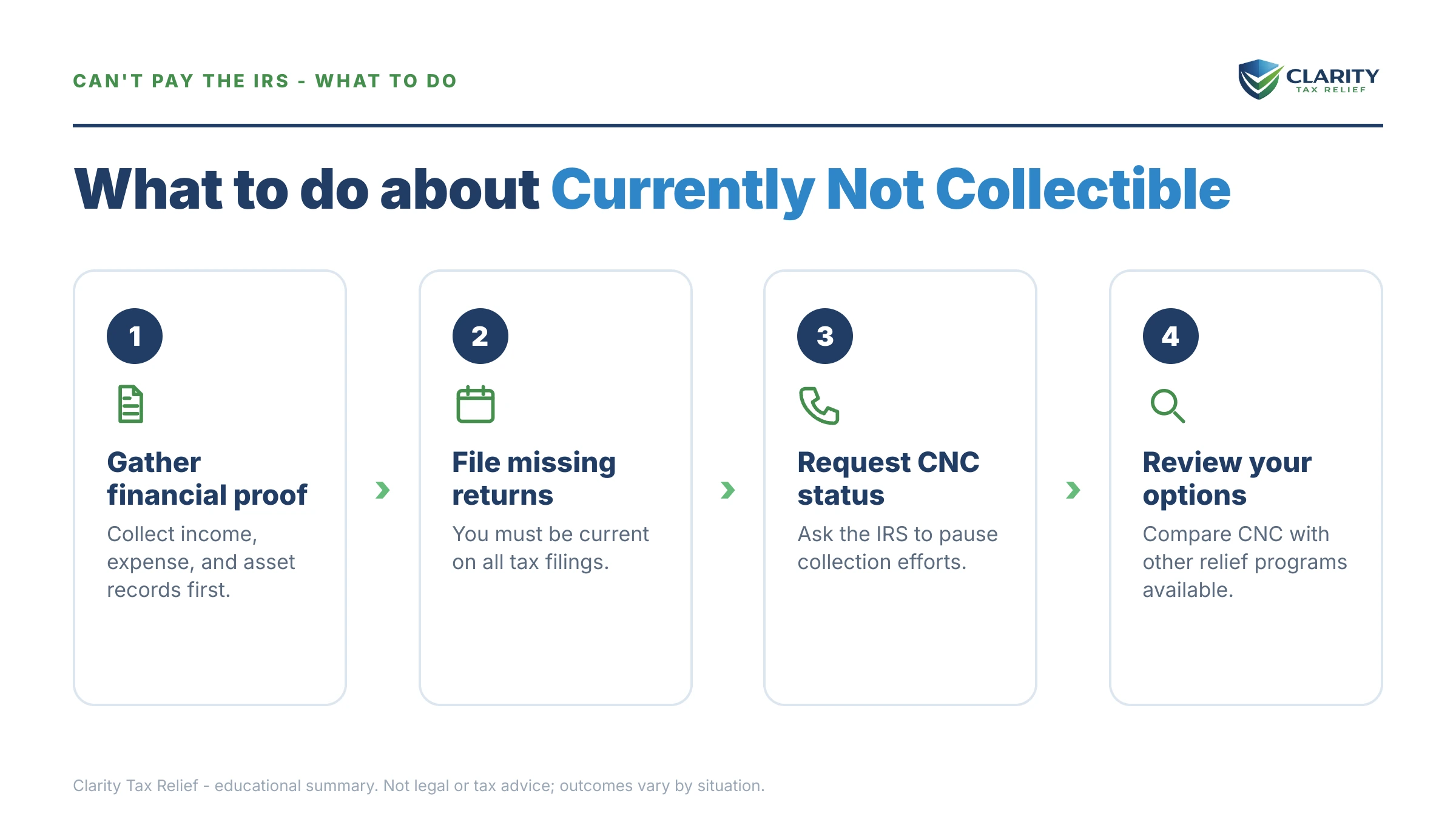

How to request currently not collectible status, step by step

- File any unfiled returns first. The IRS won't grant CNC while required returns are missing — filing compliance is the entry ticket, and filing also stops the 5% monthly failure-to-file penalty, ten times the failure-to-pay rate (in months where both penalties apply, the failure-to-file portion drops to 4.5%, for 5% combined).

- Complete Form 433-F honestly. List all household income, assets, and monthly expenses; the IRS measures your expenses against its allowable living expense standards, not against what you actually spend.

- Gather your proof. Pull two or three months of pay stubs or benefit statements, bank statements, and bills for rent or mortgage, utilities, insurance, and medical costs.

- Call the number on your most recent IRS notice. Tell the representative you're requesting currently not collectible status due to hardship, and be ready to read your 433-F figures over the phone or fax the form.

- Confirm code 530 on your account transcript. A few weeks after approval, pull your account transcript and verify the transaction code 530 entry — that's your proof the status posted.

- Protect the status every year. File every return on time, adjust withholding or estimates so no new balance accrues, and expect a CP71 reminder notice annually.

If a revenue officer holds your case rather than the Automated Collection System, you'll use the longer Form 433-A instead, and the conversation happens with that officer directly. The IRS's own description of the process is on its temporarily delay the collection process page.

How long CNC lasts — and how you lose it

CNC has no expiration date of its own — it ends when your finances recover, when you break compliance, or when the debt itself expires. The IRS builds the exit ramp in at the start: when it closes your account, it records an income threshold, and every return you file afterward is compared against it. A return showing income above the line flags the account for review; the full mechanics are in how long does currently not collectible last — and note that link's companion piece, CNC status removed, on what reactivation looks like.

The self-inflicted exits are more common than the income-triggered ones. Filing late, skipping a return, or racking up a fresh unpaid balance tells the IRS the hardship story no longer holds, and the account can move back to active collection. The single best way to keep CNC is boring: file on time and owe nothing new — fix withholding or quarterly estimates so next April doesn't create a new debt on top of the paused one.

If a levy is already running or a revenue officer has your file, have an experienced tax professional pressure-test your 433 numbers before you call the IRS — start with a free case review of your CNC eligibility.

CNC in special situations: self-employed, Social Security, and state tax

The CNC test is the same everywhere, but three situations change how it's run.

Self-employed and 1099 income. The IRS treats variable income skeptically — it averages your deposits, questions business expenses that look personal, and may ask for a profit-and-loss statement alongside the 433. Hardship with business income is winnable but documentation-heavy; the specifics are in currently not collectible self employed.

Fixed income and Social Security. Retirees and benefit recipients are often the cleanest CNC candidates because income is documented and stable — and CNC releases the Federal Payment Levy Program's 15% Social Security levy. If benefits are your main income, see IRS hardship while on Social Security for the fixed-income version of this playbook.

State tax debt. IRS CNC does nothing for a state balance. Each state runs its own hardship process with its own forms, and the stakes differ: California's Franchise Tax Board, for example, collects under a 20-year statute (R&TC §19255) — twice the IRS's window — so "wait it out" is a much weaker strategy there. If you owe Sacramento, start with FTB currently not collectible and treat it as a separate case with its own paperwork.

When you can handle CNC yourself — and when help changes the outcome

Plenty of people get CNC on their own, and you may be one of them. If your income is W-2 wages or benefits, your expenses fit inside the IRS standards without argument, no levy is active, and you're comfortable filling out Form 433-F and sitting on hold, the request is a phone call plus paperwork. The IRS employee runs the same math either way.

Experienced help earns its cost in the harder fact patterns: a wage or bank levy already in motion (where the release has to be pushed, not assumed), a revenue officer on the file, self-employment income the IRS wants to reconstruct, multiple unfiled years that have to be cleaned up first, home equity or a planned refinance that puts the lien question front and center, or a CSED close enough that the IRS will fight the closing. In those cases the difference isn't filling in the form — it's knowing which expenses the IRS will allow, how to present borderline items, and whether CNC is even the right ask compared to a partial-payment plan or an offer. If you're unsure how badly a levy is hurting you in the meantime, the Taxpayer Advocate Service also exists precisely for hardship cases the normal channels are mishandling.

Terms on your transcript and notices, decoded

- Currently not collectible (status 53): the IRS's internal hardship closing — collection is suspended because your finances show nothing available to pay.

- Transaction code 530: the account-transcript entry proving the CNC closing posted; no code 530, no protection.

- CSED: the Collection Statute Expiration Date — 10 years from assessment, after which the IRS can no longer collect; CNC time counts toward it.

- Allowable living expense (ALE) standards: the IRS's capped budget categories — national amounts for food and clothing, local caps for housing and transportation — used to measure your ability to pay (the current figures live on the IRS collection financial standards page).

- Notice of Federal Tax Lien (NFTL): a public claim against your property securing the debt — it takes nothing, unlike a levy, which does.

- CP71: the annual reminder notice every CNC account receives; it restates the balance and is not a return to collection by itself.

IRS currently not collectible: questions people ask

Does IRS currently not collectible forgive the tax debt?

No. CNC pauses enforced collection — levies, garnishments, and seizures — but the balance stays on your account, and interest plus the 0.5% monthly failure-to-pay penalty keep accruing. The real relief is indirect: the 10-year collection statute keeps running while you're in CNC, so if your finances never recover before the CSED passes, whatever remains legally expires.

How do I know if the IRS actually put me in CNC status?

Check your account transcript for transaction code 530 — that's the entry the IRS posts when it closes an account as currently not collectible. You won't get a congratulatory letter, but you will receive a CP71 reminder notice each year showing the balance. If you requested CNC by phone, ask the agent for the date it will post and confirm on the transcript a few weeks later.

Will the IRS file a tax lien if I'm in currently not collectible status?

Usually yes when the balance is over $10,000 — placing an account in CNC generally triggers a Notice of Federal Tax Lien if one isn't already on file. The lien doesn't take anything from you; it secures the government's claim against your property. It matters most if you plan to sell or refinance a home, where a lien subordination or discharge may be needed to close.

How long does currently not collectible status last?

There's no fixed term — CNC lasts until your finances recover or the collection statute expires. When the IRS closes your account, it records an income threshold; if a future tax return shows income above it, the account is flagged for review and can return to active collection. Many taxpayers remain in CNC for years, and some stay in it until the debt expires.

Will I still get my tax refund while in CNC?

No. The IRS applies every federal refund to your outstanding balance until it's paid or expires — CNC doesn't stop the offset. That's not entirely bad news: offsets chip away at the debt without touching your monthly budget. If a refund offset would cause immediate hardship, a separate remedy called an offset bypass refund exists, but it must be requested before the refund is taken.

Can my passport be revoked while I'm in CNC?

No. Debt in CNC hardship status is excluded from 'seriously delinquent tax debt' certification, even above the 2026 threshold of $66,000. If you were certified before entering CNC, the IRS should reverse the certification once the status posts. This makes CNC one of the few paths that protects a passport without paying the balance down.

Do I use Form 433-F or Form 433-A to request CNC?

Form 433-F is the shorter statement used when you're dealing with IRS Automated Collection by phone or mail — it's what most CNC requests run on. Form 433-A is the longer version required when a revenue officer is assigned to your case. Use whichever the IRS employee handling your account asks for; the underlying math is the same.

Does CNC stop the 15% Social Security levy?

Yes. Hardship status releases levies issued through the Federal Payment Levy Program, which can take up to 15% of Social Security benefits. If the levy is already running, ask for the release explicitly when CNC is granted and get the levy release faxed to the paying agency — it doesn't always happen automatically or quickly.

Is currently not collectible better than an offer in compromise?

It depends mostly on your collection statute and how permanent your hardship is. CNC costs nothing, takes effect in weeks, and lets the 10-year clock run — often the stronger play when the CSED is only a few years out. An OIC costs $205 to file (waived for low-income applicants), takes months to over a year, pauses the CSED while pending, and the IRS accepted roughly 1 in 5 offers in FY2024.

Can I get currently not collectible status for state taxes too?

Not automatically — IRS CNC covers only your federal account, and each state runs its own hardship program with its own forms and rules. California's FTB, for example, has a separate hardship process and a 20-year collection statute, twice the IRS's. If you owe both, resolve them as two separate cases; never assume the state saw your IRS paperwork.

Your next 24 hours

- Find your numbers. Pull your most recent IRS notice and note the total balance and the tax years — and if you have an IRS online account, check whether a code 530 or a final levy notice already appears on your record.

- Gather the 433-F raw material. Your last filed return, two months of pay stubs or benefit statements, bank statements, and your monthly bills for housing, utilities, insurance, and medical costs.

- Get the eligibility read. Call (888) 825-7779 or use the 2-minute form for a free review of whether CNC — or a stronger option — fits your finances. There's no application deadline, but interest and the 0.5% monthly penalty compound on the full balance every month the account sits unresolved.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.