IRS Notices

IRS CP71 Notice: What the Annual Reminder of Balance Due Means in 2026

The short answer: a CP71 notice is the IRS's annual reminder that you still owe back taxes — not a new bill, not an audit, and not a levy threat. Federal law requires the IRS to send this yearly statement, and the balance on it keeps growing with interest and penalties until you resolve the debt or the collection statute expires.

The balance on this letter probably isn't news to you — it's been sitting on the books since a hard year. What stings is that the envelope keeps coming back every year, and each time the number is bigger. That's what a CP71 is built to do: remind you, once a year, that the debt is still alive. It's also a once-a-year prompt to finally pick a resolution — and there are more of them than the notice mentions.

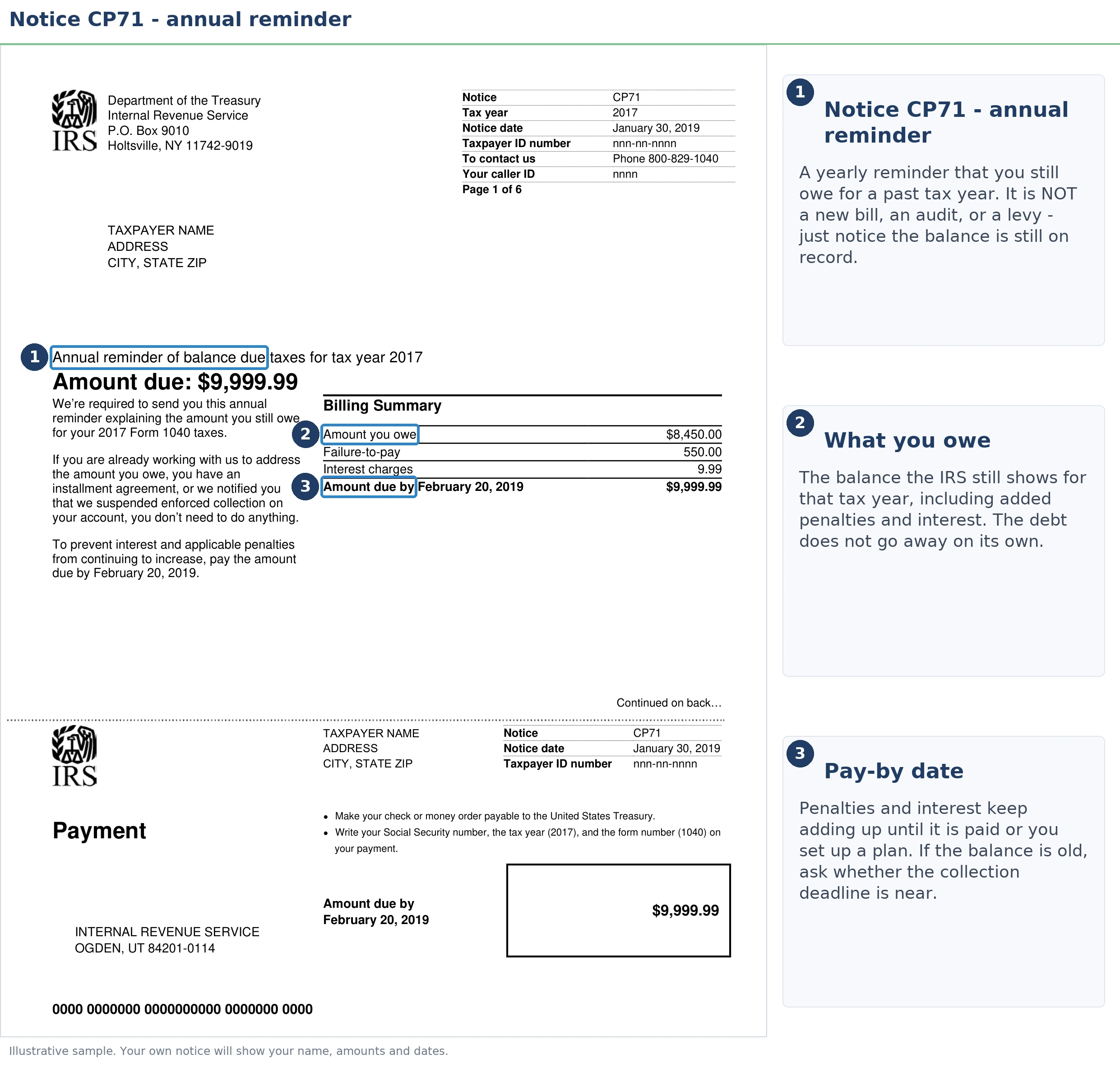

Because CP71s go out year after year, they also carry information most people never extract: how old the debt is, what status your account is in, and how close you are to thresholds that trigger real consequences. The image below shows exactly what a CP71 looks like and where to find the three figures that matter most — the tax year, the total balance, and how much of it is penalty and interest.

⏱ Your real clock: a CP71 has no response deadline — but the account behind it never stops moving. The failure-to-pay penalty adds up to 0.5% of the unpaid tax every month (until it caps at 25%), interest compounds daily on the whole balance, and the 10-year collection statute keeps running whether you act or not.

Why you got a CP71 notice

The IRS is required by law — Internal Revenue Code §7524 — to send anyone with an unpaid tax balance a written statement at least once a year, and the CP71 is that statement. Receiving one means exactly three things: the debt is still on the books, it accrued another year of interest and penalties, and the amount printed is the IRS's snapshot as of the notice date.

Nothing you did recently triggered it. Nobody reviewed your file, reopened your return, or made a new decision about your account. The CP71 is generated automatically, on a yearly cycle, for every account carrying a balance — including accounts on active payment plans and accounts the IRS has agreed not to collect from for now.

If the balance itself is a surprise — you don't remember ever owing this year — trace where it came from before doing anything else. Old math-error adjustments (a CP11 notice you may barely remember), a substitute return the IRS filed for an unfiled year, or penalties on a year you thought was settled are the usual sources. And if you're not sure why the IRS is writing to you at all, start with our decoder on why you got a letter from the IRS.

CP71, CP71A, CP71C, CP71D, CP71H — which one are you holding?

Every notice in the CP71 series is the same annual statement of balance due; the letter suffix reflects your account's status, not a different debt. The table below decodes each version and the first thing to check on it.

| Notice | What it typically signals | What to check first |

|---|---|---|

| CP71 | Standard annual reminder of unpaid tax, penalties, and interest | That the balance matches your IRS online account |

| CP71A | Usually sent when the account sits in a non-collection (hardship) status; the debt still exists and still accrues | Whether your hardship status is still in place — and how much the balance grew this year |

| CP71C | Annual reminder that often includes passport-certification language for seriously delinquent tax debt | How close your balance is to the $66,000 certification threshold — see our full CP71C notice guide |

| CP71D | Same annual statement; commonly seen on larger balances or accounts moving through active collection | Whether any active collection notice (CP501–CP504) has also arrived recently |

| CP71H | Reminder of an unpaid health-care shared responsibility payment rather than income tax | That the amount traces to the shared responsibility payment — the IRS collects it mainly through refund offsets |

Whichever version you're holding, the mechanics of the balance are identical: the printed amount is already out of date the day you open it, because interest compounds daily. Your IRS online account shows the current figure.

What happens if you ignore a CP71 notice

A CP71 triggers no levy by itself — but the account behind it keeps moving through the IRS's automated collection machinery, and each stage that follows carries more power than the last. Here is the sequence an unresolved balance travels:

- Accrual, quietly. The failure-to-pay penalty adds up to 0.5% of the unpaid tax each month until it caps at 25%, and interest compounds daily on the entire balance — penalties included. Next year's CP71 arrives with a bigger number.

- Refund offsets. Every federal tax refund you're owed is taken and applied to the debt, year after year, without any new notice or approval step.

- Re-entry into active collection. A dormant account can be queued back into the notice stream at any time: CP501 and CP503 reminders, then a CP504 notice — which lets the IRS seize your state refund and usually precedes a federal tax lien.

- Final notice and levy. An LT11 or Letter 1058 starts a 30-day clock with Collection Due Process appeal rights (requested on Form 12153). After it runs, the IRS can levy bank accounts and wages — and take up to 15% of Social Security benefits through the Federal Payment Levy Program.

- Passport certification. Once the balance reaches the seriously delinquent threshold — $66,000 in 2026 — the IRS can certify the debt to the State Department (notice CP508C), which can block passport issuance and renewal. Our guide to passport revocation for tax debt covers how to reverse it.

One 2026 reality check: IRS staffing fell roughly 27% in 2025, so reaching a human is harder than ever — but every stage above is run by automated systems that didn't get laid off. The machine escalates on schedule whether or not anyone ever reads your file.

This comparison shows exactly where a CP71 sits relative to the notices that do carry teeth:

| Notice | What it is | Enforcement power |

|---|---|---|

| CP71 series | Legally required annual statement of your balance | None by itself — informational |

| CP501 / CP503 | Reminder bills in active collection | None yet, but the sequence is moving |

| CP504 | Notice of intent to levy your state refund | State refund seizure; federal lien becomes likely |

| LT11 / Letter 1058 | Final notice of intent to levy | Bank, wage, and Social Security levies after 30 days; appeal via Form 12153 |

Getting a CP71 every year and tired of watching the number grow?

Send us a photo of the notice. An experienced tax professional will pinpoint where your account actually stands — how old the debt is, what status it's in, and which resolution fits your income — free and confidential. Interest and penalties accrue every month the balance sits.

Your options for the balance on a CP71

The IRS has five realistic paths for a balance old enough to generate annual reminders, and which one fits depends on your income, assets, and how much time remains on the collection statute:

- Pay in full or short-term plan. Up to 180 days to full-pay with no setup fee. Stops the escalation sequence, though interest runs until the last dollar posts.

- Installment agreement. Balances of $50,000 or less can usually be set up online for up to 72 months without a financial statement (Form 9465 works by mail). Above $50,000, the IRS wants a Form 433-F financial disclosure first. Interest and the (reduced) failure-to-pay penalty continue during the plan.

- Partial-pay installment agreement. A monthly payment sized to what you can actually afford — even if it won't retire the debt before the 10-year statute expires. The unpaid remainder is written off at expiration. See how a partial payment installment agreement works.

- Currently Not Collectible status. If paying anything would leave you unable to cover basic living expenses, collection is paused. You'll keep getting a CP71 (often the CP71A) each year while the statute runs, but levies and garnishments stop. Details in our guide to Currently Not Collectible status.

- Offer in Compromise. Settling for less than the full balance is real but means-tested — the IRS accepted roughly 1 in 5 offers in FY2024, based on math about your assets and future income, not on how compelling your story is. The $205 application fee and 20% down payment are waived if your income is at or below 250% of the federal poverty level.

- Penalty relief. On older debts, penalties are frequently the most removable slice of the balance. First-time penalty abatement can erase a year's penalties if your prior three years were clean — and starting in summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) begins applying similar relief automatically, with no request needed. Reasonable-cause relief covers illness, disaster, and other events outside your control.

| Balance owed | Realistic options | What it takes |

|---|---|---|

| Under $10,000 | Guaranteed installment agreement; short-term full pay | Filed returns current; plan pays off within 3 years — approval is automatic if conditions are met |

| $10,000–$25,000 | Streamlined installment agreement; penalty abatement | Online setup, no financial statement; up to 72 months |

| $25,001–$50,000 | Streamlined plan (direct debit usually required); partial-pay IA | Online setup still available; direct debit keeps it streamlined |

| $50,001–$66,000 | Financial-statement plan, partial-pay IA, CNC, or OIC | Form 433-F disclosure; watch the $66,000 passport threshold closely |

| Over $66,000 | Same options plus passport decertification strategy | Getting into an approved plan or CNC generally reverses certification |

Say you owe $61,200 on Social Security income: the real math

A hypothetical makes the stakes concrete. Say your CP71 shows $61,200 from a tax year several years back, and your income today is a $2,300 monthly Social Security check plus a small pension.

The accrual: the failure-to-pay penalty runs at 0.5% per month — about $306 a month on a balance this size until the penalty reaches its 25% cap. On a debt this old the penalty may already be capped, but interest never caps: it compounds daily on the full balance, penalties included.

The passport line: $61,200 sits just $4,800 below the $66,000 seriously-delinquent threshold for 2026. Accruals alone can carry the balance across it — and certification can block a passport renewal you were counting on.

The full-pay plan math: $61,200 spread over 72 months is roughly $850 a month before continuing accruals — plainly unworkable against $2,300 in monthly income. And because the balance tops $50,000, a self-serve online plan isn't available anyway; the IRS would require a Form 433-F financial statement.

The other side of that disclosure: if allowable living expenses consume the Social Security income, the very same financial statement that rules out a big payment plan supports Currently Not Collectible status or a small partial-pay agreement — and if there's little equity in assets, potentially an Offer in Compromise. On a fixed income, the resolution the notice implies (pay in full) is usually the least realistic one, and the programs it never mentions are built for exactly this situation. If this profile sounds like yours, our guide for people who are retired and owe back taxes goes deeper — including why the IRS can garnish Social Security only after specific notices and only up to 15%.

The 10-year collection clock behind every CP71

The IRS generally has 10 years from the date it assessed your tax to collect it — after that, the remaining balance is legally written off. A stack of CP71s is actually a rough calendar of that clock: the first one typically arrived about a year after assessment, so counting the annual reminders you've received tells you approximately how many years have burned off. Our guide to how long the IRS can collect back taxes explains the mechanics, and you can estimate your own expiration date with our CSED Calculator.

Two cautions before you plan around expiration. First, the clock pauses — a pending Offer in Compromise, bankruptcy, a collection due process hearing, or extended time outside the U.S. all stop it from running, sometimes for years. The honest version of "the debt disappears after 10 years" lives in our guide on whether IRS debt goes away after 10 years. Second, waiting out the clock is not a passive strategy: the account can re-enter active collection at any point along the way, and a levy in year eight hurts exactly as much as one in year two.

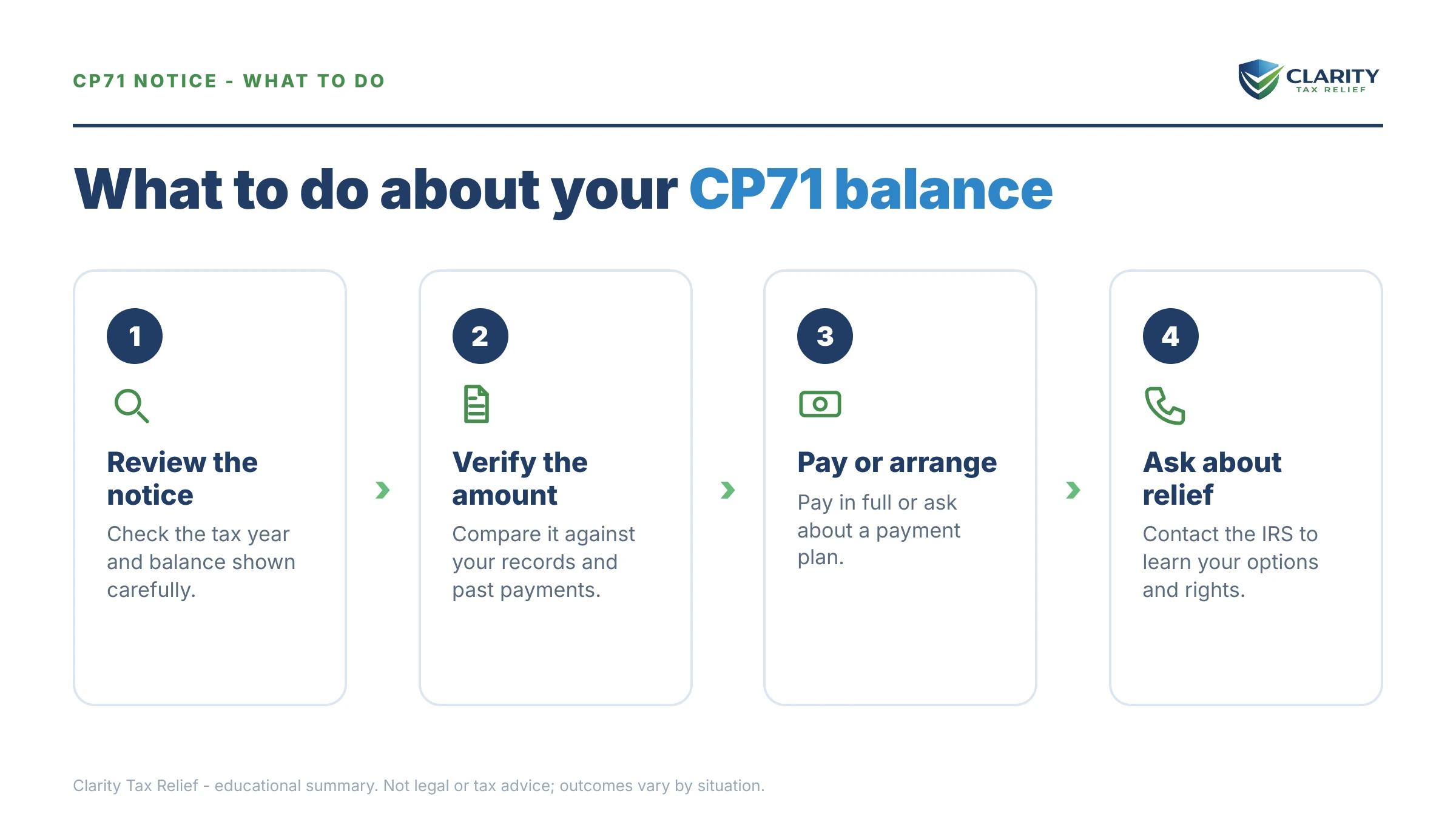

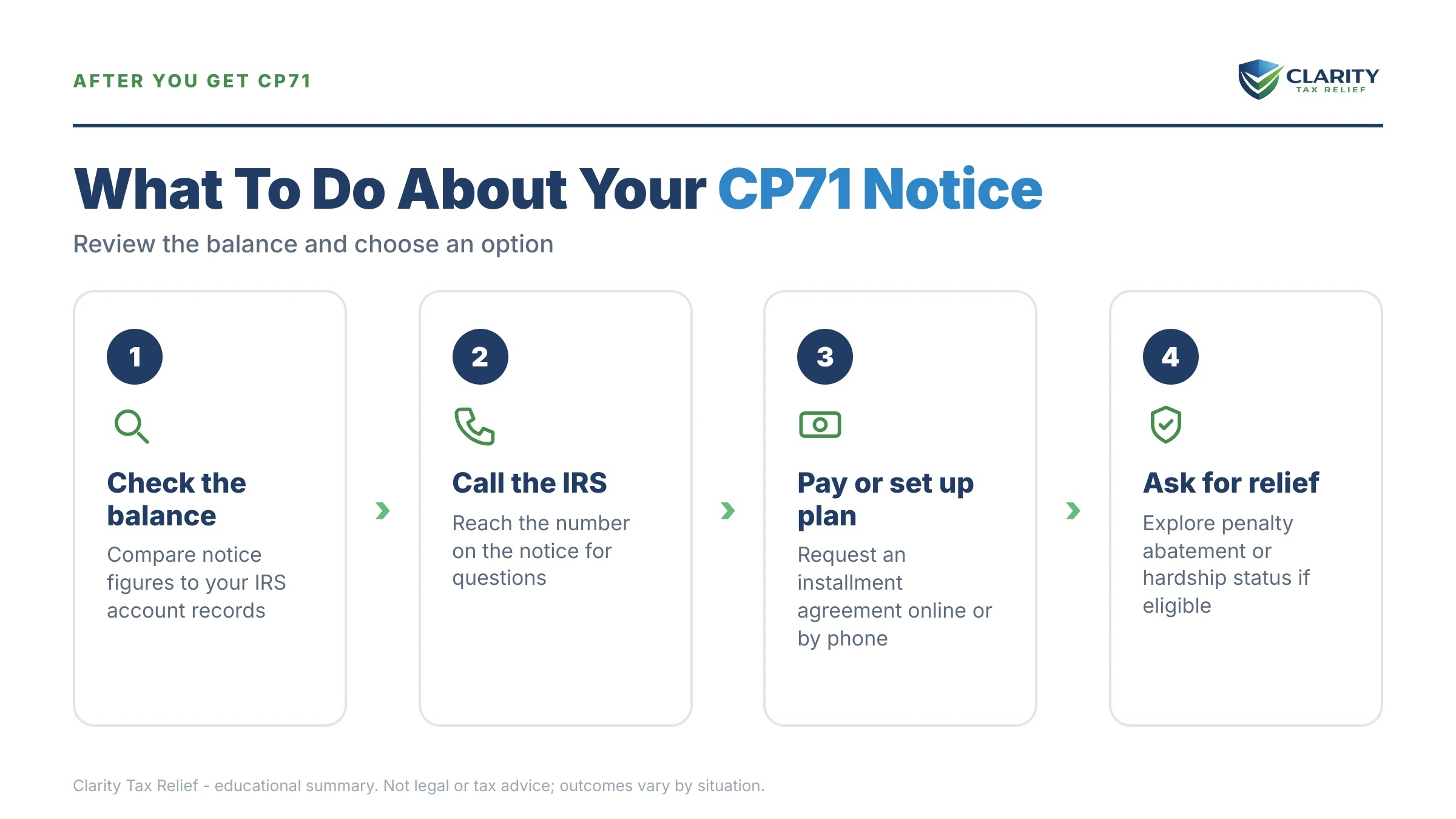

How to respond to a CP71, step by step

- Pull your IRS records. Log into your IRS online account (or request an account transcript) and confirm the balance, the tax year, and the date the tax was assessed.

- Date the debt. Count forward 10 years from the assessment date to estimate when the collection statute expires — that timeline shapes every other decision.

- Confirm your account status. Figure out whether you're on a payment plan, in hardship status, or unresolved — the CP71 suffix hints at it, but your transcript confirms it.

- Choose a resolution that fits. Match your balance and income to a payment plan, hardship status, or an Offer in Compromise, and set it up before the account re-enters active collection.

- Request penalty relief. Ask about first-time abatement, the new automatic exemption from penalty, or reasonable-cause relief — penalties are often the most removable part of the balance.

The IRS's own page, Understanding your CP71 notice, confirms the notice mechanics, and any payment or plan setup runs through IRS.gov/payments.

When you can handle a CP71 yourself

Plenty of CP71 situations need no professional at all. If you agree with the balance, it's under $50,000, and your income supports a monthly payment, you can set up a plan online in about twenty minutes and the annual reminders become routine statements. Same if you're already on an installment agreement or in hardship status and the CP71 simply confirms the balance — file it and carry on. If you get stuck dealing with the IRS on a straightforward issue, the Taxpayer Advocate Service is a free, independent resource.

Experienced help changes outcomes in a narrower set of cases: a balance above $50,000 (where a Form 433-F financial statement decides everything and small presentation choices swing the result), a fixed or protected income where CNC, partial-pay, or OIC math needs to be run before you commit to anything, multiple unresolved years, a balance sitting near the $66,000 passport threshold, or a CP504 or final notice that has already arrived alongside the annual reminder. In those cases the order you fix things — status first, penalties second, balance last — often matters more than the program you pick.

Terms on your notice, decoded

- CSED (Collection Statute Expiration Date): the date, generally 10 years after assessment, when the IRS's legal right to collect the balance ends.

- Failure-to-pay penalty: a monthly charge of up to 0.5% of the unpaid tax, capped at 25% of the tax owed.

- Statutory interest: interest the IRS is required by law to charge, compounding daily on tax and penalties alike — it cannot be waived just because you ask.

- Currently Not Collectible (CNC): a hardship status in which the IRS pauses collection because paying would leave you unable to cover basic living expenses.

- Seriously delinquent tax debt: a balance of $66,000 or more (2026) that the IRS can certify to the State Department, affecting your passport.

- Federal Payment Levy Program (FPLP): the automated program that lets the IRS take up to 15% of certain federal payments — including Social Security benefits — after proper notice.

CP71 notice FAQs

Is a CP71 notice serious?

A CP71 is serious in the sense that the debt behind it is real and growing, but the notice itself carries no enforcement power. It's an annual statement the IRS is required by law to send, not a levy warning. The risk isn't the letter — it's another year of interest, penalties, and the chance the account moves back into active collection while you wait.

Do I have to respond to a CP71 notice?

No response is legally required, and there's no deadline printed on it. But treating it as ignorable is how balances quietly double. Use it as a yearly checkpoint: verify the amount against your IRS online account, confirm your account status, and put a resolution in place if you don't have one. If the amount looks wrong, dispute it in writing with documentation.

Why does the IRS send me a CP71 every year?

Internal Revenue Code Section 7524 requires the IRS to send taxpayers with unpaid balances a written statement at least once a year, and the CP71 series is how it complies. You'll keep receiving one annually until the balance is paid, settled, or the 10-year collection statute expires. A yearly CP71 does not mean the IRS reviewed your file or made any new decision about it.

What is the difference between CP71 and CP71C?

Both are annual reminders of the same kind of balance; the suffix reflects your account's status. A CP71C often includes language about passport certification for seriously delinquent tax debt — a designation that applies at $66,000 or more in 2026 — or accompanies accounts in special statuses. Read the body of your letter; the balance, tax year, and accrual figures work the same way on both.

Does getting a CP71 mean my payment plan or hardship status was cancelled?

No. The IRS sends the annual reminder even to taxpayers with active installment agreements and accounts in Currently Not Collectible status, because the law requires an annual statement whenever a balance exists. If your payment plan had defaulted, you'd get a CP523 notice instead. Keep making payments, treat the CP71 as a statement, and verify your status online if you're unsure.

Can the IRS take my Social Security for the balance on a CP71?

Not because of the CP71 itself — but if the account moves through the full collection sequence and reaches a final notice, the IRS can take up to 15% of Social Security retirement benefits through the Federal Payment Levy Program. That levy only follows proper notice, and hardship rules can stop or release it. Fixed-income taxpayers often qualify for Currently Not Collectible status instead.

Does the debt on my CP71 ever expire?

Generally yes — the IRS has 10 years from the date of assessment to collect, after which the remaining balance is written off. But the clock pauses for events like a pending Offer in Compromise, bankruptcy, collection due process hearings, or long periods outside the U.S. If you've received several annual CP71s, checking the exact expiration date should be your first move.

Is the amount on my CP71 the exact payoff amount?

No — it's a snapshot as of the notice date. Interest compounds daily and the failure-to-pay penalty accrues monthly, so the true payoff is higher by the time you pay. Your IRS online account shows a current balance, and the IRS can give you a formal payoff amount calculated to a specific date if you're paying in full.

Your next 24 hours

- Find two things on the notice: the tax year the balance comes from and the total amount due. Then subtract the tax year from today's year — that rough age tells you how much of the 10-year collection clock has already run.

- Gather three documents: the CP71 itself, your most recent tax return, and a summary of your monthly income (your SSA-1099 or benefit statement if you're on Social Security). That's everything a resolution decision needs.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form. An experienced tax professional will confirm your account status, date the debt, and match the balance to the option that fits your income — while this year's reminder is still just a reminder, and before another year of interest and penalties stacks onto it.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.