IRS Notices

IRS CP71C Notice: What It Means and What to Do in 2026

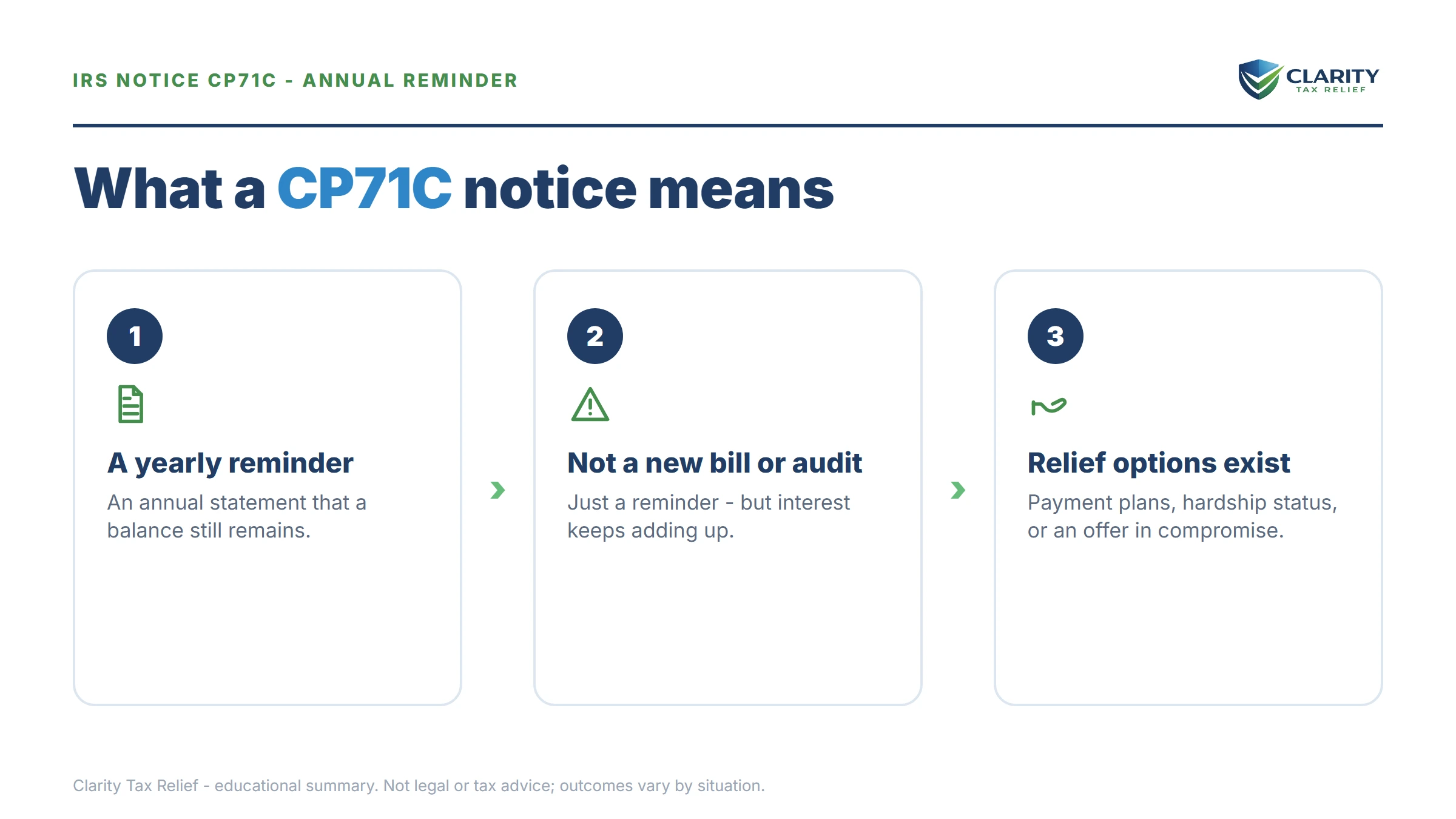

The short answer: a CP71C notice is the IRS's annual reminder of an unpaid tax balance — the law requires one statement per year on every account that still owes. It adds no new enforcement power by itself, but it proves the debt is active, growing with interest, and still on the IRS collection clock.

You may not have heard from the IRS in a year — maybe longer — and part of you hoped the balance had quietly died. Then a CP71C shows up with a bigger number than you remember, and if a levy threat was the last thing in your file, this letter feels like the fuse being relit. It isn't a levy. But it is proof the debt survived, and this is the right moment to deal with it on your terms.

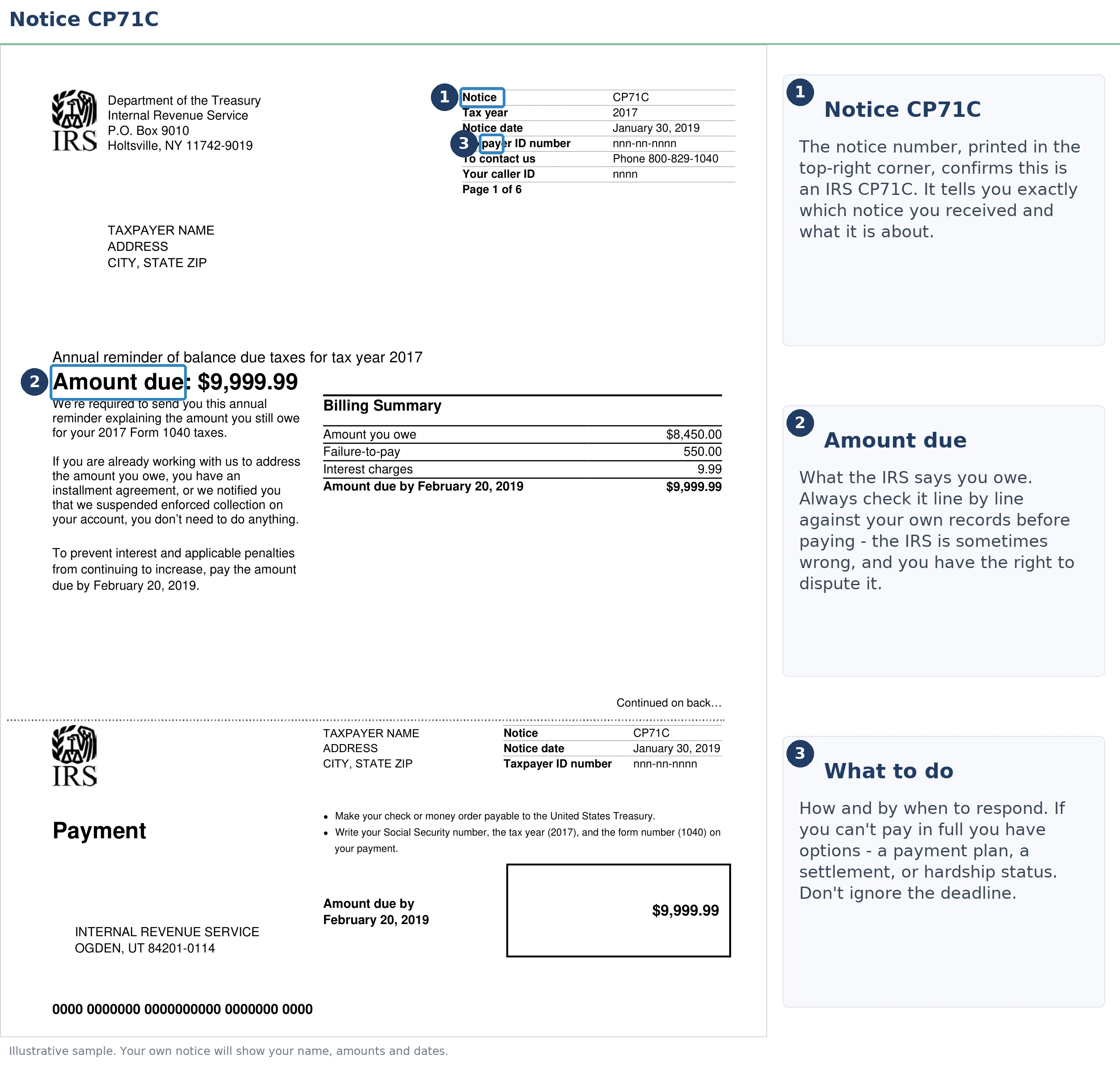

The image below shows exactly what a CP71C looks like and where to find the two numbers that matter most: the total balance and the tax years it covers. Those two numbers drive every decision on this page.

⏱ The clock on a CP71C: there is no response deadline printed on this notice — the clock that matters is the ongoing one. The failure-to-pay penalty adds 0.5% of the balance every month (until it caps at 25%) — rising to 1% per month once the IRS has issued a final notice of intent to levy, and dropping to 0.25% while an installment agreement is in effect. Interest compounds daily on top, and if a final notice of intent to levy was ever issued on this debt, the IRS can levy without warning you again.

Why the IRS sent you a CP71C notice

A CP71C exists because federal law requires the IRS to send every taxpayer with a delinquent balance a written statement at least once every year until the debt is paid or expires. It is not triggered by anything you did this year — it is the system confirming, on schedule, that your account still shows money owed.

The CP71C version of that annual statement most often lands on accounts that have gone quiet: a debt that fell out of active collection, sat in hardship status, or was simply never resolved after earlier notices. It may also include language about passport certification for "seriously delinquent" tax debt — more on that threshold below, because it likely applies if your balance looks anything like the example in this guide.

The notice itself breaks your balance into three pieces: the original tax, accrued penalties, and accrued interest. On old debts, the accruals often rival the tax itself — which is exactly why penalty relief belongs in your plan, not just a payment. If you're not sure how the balance started, it usually traces back to an original bill like a CP14 notice or a math-error adjustment like a CP11 notice. (For the general map of how IRS mail works, see why did I get a letter from the IRS — this page stays focused on the CP71C specifically.)

The 10-year clock hiding behind your CP71C

Every CP71C is a snapshot of a debt that legally expires: the IRS generally has 10 years from the date each tax was assessed to collect it. That expiration date is called the CSED, and it's the single most important fact a CP71C doesn't print. If your debt is from 2019, the IRS may have only a few years of collection runway left — and that changes which resolution is cheapest for you.

The clock isn't simple, though. Bankruptcy, a pending offer in compromise, and collection appeals all pause it, so the true date is often later than year ten. Our guide to the 10-year collection statute (CSED) explains the rules, and you can estimate your own expiration date with our CSED Calculator — it estimates, based on your assessment dates and history; your account transcript confirms the real number.

One useful habit: keep every CP71C you receive. Comparing this year's balance to last year's shows you exactly what the accruals are costing you — and each notice documents which tax years the IRS is still pursuing.

What happens if you ignore a CP71C notice

Ignoring a CP71C doesn't trigger a levy — but it leaves you exposed to everything the IRS's automated system can do next, on the system's schedule instead of yours:

- The balance keeps compounding. Interest accrues daily and the failure-to-pay penalty adds 0.5% per month until it caps — a dormant debt is never a frozen debt.

- Your refunds keep disappearing. Any federal refund you're owed is applied to the old balance automatically, every year, until it's gone.

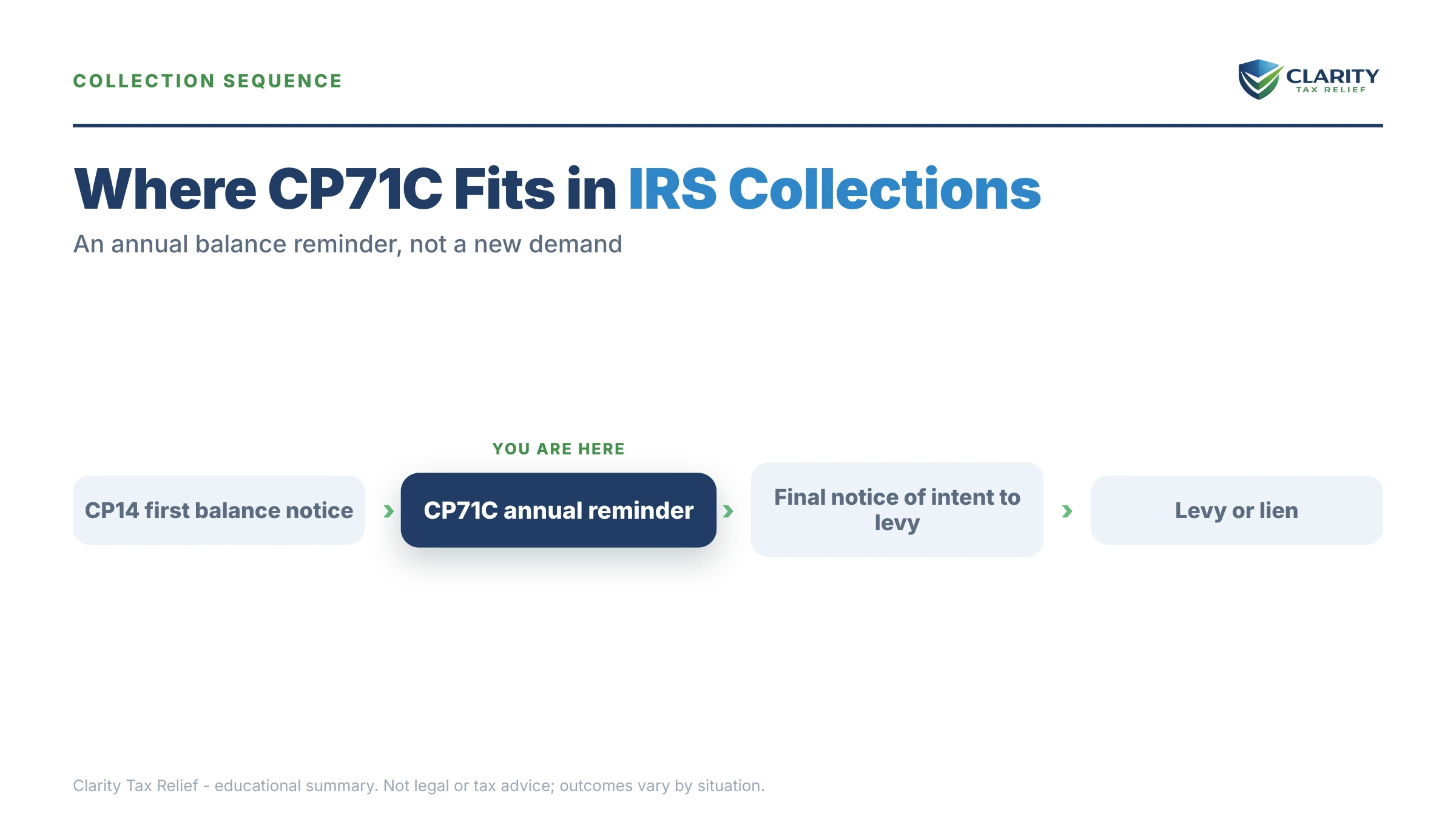

- The account can re-enter active collection. A CP504 intent-to-levy notice can follow, letting the IRS seize your state refund and making a federal tax lien likely.

- A final notice opens the levy door. An LT11 or Letter 1058 starts a 30-day window; after it closes, wages and bank accounts are fair game.

- If a final notice already went out — the door is already open. The IRS only has to give that warning once per debt. Levies can resume with no new letter.

- Above $66,000, your passport is in play. Debt with no arrangement in place can be certified to the State Department, which can deny or revoke your passport.

The 2026 wrinkle: the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder than ever — but the notice stream, refund offsets, and levies are automated and never stopped. Silence from the IRS is not safety; the CP71C in your hand is proof of that.

| Stage | What the IRS can do | Your window |

|---|---|---|

| CP71C (annual reminder) | Nothing new — restates the balance with updated penalties and interest | No printed deadline; accruals run daily |

| CP504 notice (intent to levy) | Seize your state tax refund; a federal tax lien becomes likely | Act before the final notice — this is not it |

| LT11 notice / Letter 1058 (final notice) | Levy wages and bank accounts once the window closes | 30 days to request a Collection Due Process hearing (Form 12153) |

| Levy | Bank funds held 21 days before release to the IRS; wage levies run continuously until released | Fastest exits: hardship release or entering a formal resolution |

Holding a CP71C on a debt you can't pay?

Send us a photo of the notice. An experienced tax professional will check whether a final levy notice was ever issued on your account, how much collection time the IRS has left, and which resolution fits your budget — free, confidential, no pressure. Interest and penalties are accruing either way; the review costs nothing.

Your options for the balance on a CP71C

The IRS has five real paths for a CP71C balance, and which one fits depends on your income, your assets, and how much collection time remains. Here's how they compare on a balance the size of our running example:

| Option | Upfront cost | What it takes |

|---|---|---|

| Short-term payment plan | $0 setup | Full payoff within 180 days; realistic only if money is genuinely coming (a sale, a bonus, a settlement) |

| Installment agreement over $50,000 | Setup fee applies; Form 433-F financial disclosure required | Monthly payment negotiated from your income and allowable expenses — the simple online 72-month plan tops out at $50,000, so this balance needs the fuller process |

| Partial-pay installment agreement | Same disclosure | Pays what your budget allows until the CSED expires; the IRS re-reviews your finances periodically |

| Currently Not Collectible | $0 | Prove that any payment would leave you unable to cover basic living costs; collection pauses but the balance still accrues and refunds still offset |

| Offer in Compromise | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) | Show the IRS your offer matches the most it could ever collect; roughly 1 in 5 offers were accepted in FY2024 |

| Penalty relief (FTA / AEP) | $0 | Clean compliance for the prior 3 years for first-time abatement; the Automatic Exemption from Penalty begins rolling out summer 2026 |

A few notes that change the math. A balance over $50,000 means financial disclosure — our IRS payment plan over $50,000 guide and Form 433-F walkthrough cover what the IRS counts. If your budget genuinely has no room, Currently Not Collectible status stops collection while you recover. And on an old debt, penalties may be a quarter of the total — first-time penalty abatement can remove some of them with one request if your prior three years were clean.

A worked example: say you owe $76,400

Say your CP71C shows $76,400 across two old tax years, you rent, and your last IRS contact was a levy warning. Here's the math, hypothetically:

- Doing nothing: the failure-to-pay penalty alone runs 0.5% × $76,400 ≈ $382 a month until it caps at 25%, with daily-compounding interest on top. The balance grows by thousands a year while you wait.

- Passport exposure: $76,400 is above the $66,000 2026 threshold for seriously delinquent debt, so with no arrangement in place you're certifiable to the State Department — see passport revoked for tax debt. Entering a payment plan or filing an offer generally removes that exposure.

- Payment plan: suppose your Form 433-F shows $900/month of capacity and roughly 4 years remain before the CSED. Full payment would need about $76,400 ÷ 48 ≈ $1,592/month before accruals — beyond your budget. At $900/month, a partial-pay agreement would collect about $43,200 before the statute runs; the rest expires.

- Offer in Compromise: as a renter, you have no home equity for the IRS to count. On a lump-sum offer, future income is generally figured at 12 months of monthly capacity — 12 × $900 = $10,800 — plus asset equity. If your assets are thin, the IRS's own math can land far below $76,400. That doesn't make acceptance easy (about 1 in 5 offers succeed), but this profile — low assets, modest income, large old balance — is exactly the one the program exists for.

Same debt, four wildly different outcomes. The deciding inputs are your CSED, your monthly capacity, and your assets — which is why verifying those comes before choosing anything.

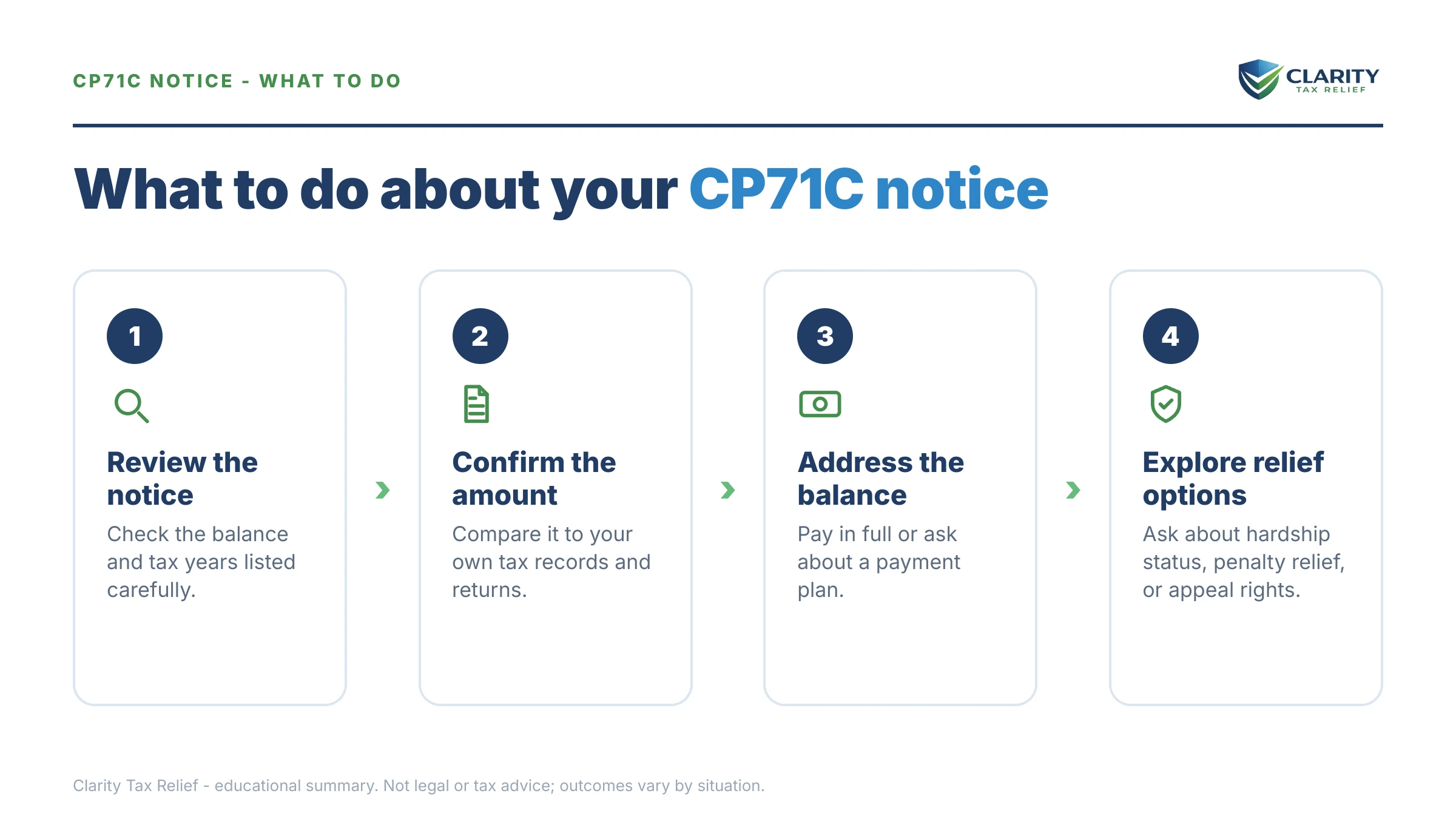

How to respond to a CP71C notice, step by step

- Verify the balance. Log into your IRS online account and match the CP71C's total and tax years against your transcripts before you act.

- Pull your notice history. Confirm whether a final notice of intent to levy (LT11 or Letter 1058) was ever issued for these years — that decides how exposed you are right now.

- Check the collection clock. Estimate the CSED for each year on the notice from your account transcript; the time remaining changes which option is cheapest.

- Choose a resolution that fits your finances. Set up a payment plan, request currently-not-collectible status, or pursue an offer in compromise — matched to what you can actually pay, not what the notice demands.

- Request penalty relief. Ask about first-time abatement or reasonable cause; starting summer 2026, the Automatic Exemption from Penalty may apply some relief with no request at all.

- Get help if enforcement is live. If a levy is in motion or your balance tops $50,000, have an experienced tax professional review the account before you call the IRS.

CP71C vs CP71, CP71A, and CP71D

All four notices are versions of the same legally required annual statement — the letter suffix mainly reflects your account's status. Read the balance, tax years, and accruals the same way on each:

| Variant | How it differs |

|---|---|

| CP71 | The standard annual reminder of a balance due — covered in our CP71 notice guide |

| CP71A | Commonly seen when active collection is paused — for example, accounts in currently-not-collectible (hardship) status |

| CP71C | Often sent on older or long-inactive balances; may include language about passport certification for seriously delinquent tax debt |

| CP71D | Another variant of the same required statement; the balance and your options are identical in practice |

When you can handle a CP71C yourself

You don't need professional help for every CP71C. Handle it yourself if the balance is one you can pay within 180 days, you agree with the amount, and no levy notice has ever been issued — a short-term plan or straightforward installment agreement set up at IRS.gov's payment plans page ends the problem cleanly, with no fee for the 180-day option.

Experienced help changes outcomes in four situations: a final levy notice already exists in your history (enforcement can restart without warning), the balance is over $50,000 (the Form 433-F negotiation determines your payment for years), you have unfiled returns behind the debt (the IRS won't approve most resolutions until they're in), or the offer-in-compromise math is close — our guide to how an offer in compromise works shows why the calculation, not the paperwork, is where offers are won or lost. If money is impossibly tight, the Taxpayer Advocate Service and Low Income Taxpayer Clinics offer free help — start at taxpayeradvocate.irs.gov.

Terms on your CP71C, decoded

- Annual reminder: the once-a-year balance statement federal law requires the IRS to send until a debt is paid or expires — that's what a CP71C is.

- CSED (Collection Statute Expiration Date): the date, generally 10 years after assessment, when the IRS legally loses the right to collect a tax year's balance.

- Seriously delinquent tax debt: a balance over $66,000 (2026) with no arrangement in place — the trigger for passport certification and a CP508C notice.

- Currently Not Collectible (CNC): an IRS status that pauses collection when paying would prevent you from covering basic living expenses; the debt remains and keeps accruing.

- Accrued penalty and interest: the "statutory additions" lines on your notice — charges the law adds automatically each month, separate from the original tax.

- Levy vs. lien: a levy takes property (wages, bank funds); a lien is a public claim against everything you own. A CP71C is neither — but both remain possible while the debt is unresolved.

CP71C notice questions, answered

Is a CP71C notice serious?

It's a reminder, not an enforcement action — no levy or lien is triggered by the notice itself. But it confirms the IRS still counts the debt as collectible, penalties and interest are still accruing, and balances over $66,000 can be certified for passport denial. If a final notice of intent to levy was issued in the past, enforcement can resume without further warning.

Why did I get a CP71C if the IRS hasn't contacted me in years?

Federal law requires the IRS to send every taxpayer with an unpaid balance a statement at least once a year, even when active collection is paused. A CP71C often lands on accounts that have been dormant or in hardship status for a long time. It doesn't necessarily mean collection is restarting — but it proves the debt hasn't expired.

Can the IRS levy my wages or bank account after a CP71C?

Not because of the CP71C itself — the IRS must first issue a final notice of intent to levy (LT11 or Letter 1058) and give you 30 days to respond. But if that final notice was already sent for this debt in an earlier year, the legal requirement is satisfied and a levy can follow at any time. Check your notice history before assuming you're safe.

Does a CP71C mean my passport will be revoked?

Not automatically. Passport certification applies to seriously delinquent tax debt — over $66,000 in 2026 — that isn't in a payment plan, pending offer in compromise, or other qualifying arrangement. If your CP71C balance crosses that line with no arrangement in place, the IRS can certify you to the State Department, which can then deny or revoke a passport; a separate CP508C notice tells you it happened.

What is the difference between a CP71 and a CP71C notice?

Both are versions of the same legally required annual balance reminder. The plain CP71 is the standard version; a CP71C tends to appear on older or long-inactive accounts and may include language about passport certification for seriously delinquent debt. Whichever version you received, the balance, tax year, and your resolution options are read the same way.

Will the debt on my CP71C eventually expire?

Usually, yes. The IRS generally has 10 years from the date a tax was assessed to collect it — the Collection Statute Expiration Date, or CSED — after which the balance is written off. But the clock pauses during bankruptcy, a pending offer in compromise, collection appeals, and certain other events, so the real expiration date is often later than year ten. Your account transcript is the only reliable way to pin it down.

Should I make a payment on my CP71C if I can't pay it all?

A partial payment reduces interest but does not stop collection or protect you by itself — the IRS treats the account as delinquent until it's inside a formal arrangement. It's usually smarter to use what you can afford as the payment inside a structured resolution — an installment agreement, hardship status, or an offer — than to send unstructured checks against a balance that keeps growing.

Your next 24 hours

- Find two things on the notice: the total amount due in the billing summary and the tax year (or years) it covers. Write both down — every option starts from those.

- Gather three documents: the CP71C itself, your most recent filed tax return, and a recent pay stub or income snapshot. That's enough for a professional to map your options in one call.

- Get the free case review: call (888) 825-7779 or use the 2-minute form. There's no printed deadline on a CP71C — but the penalty and interest accruing on that balance run every single day, and if a final levy notice already exists in your file, resolving now is what closes that door.

The IRS's own explainer for this notice is at Understanding your CP71C notice.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.