IRS Collections

How Long Can the IRS Collect Back Taxes? The 10-Year Rule (CSED) in 2026

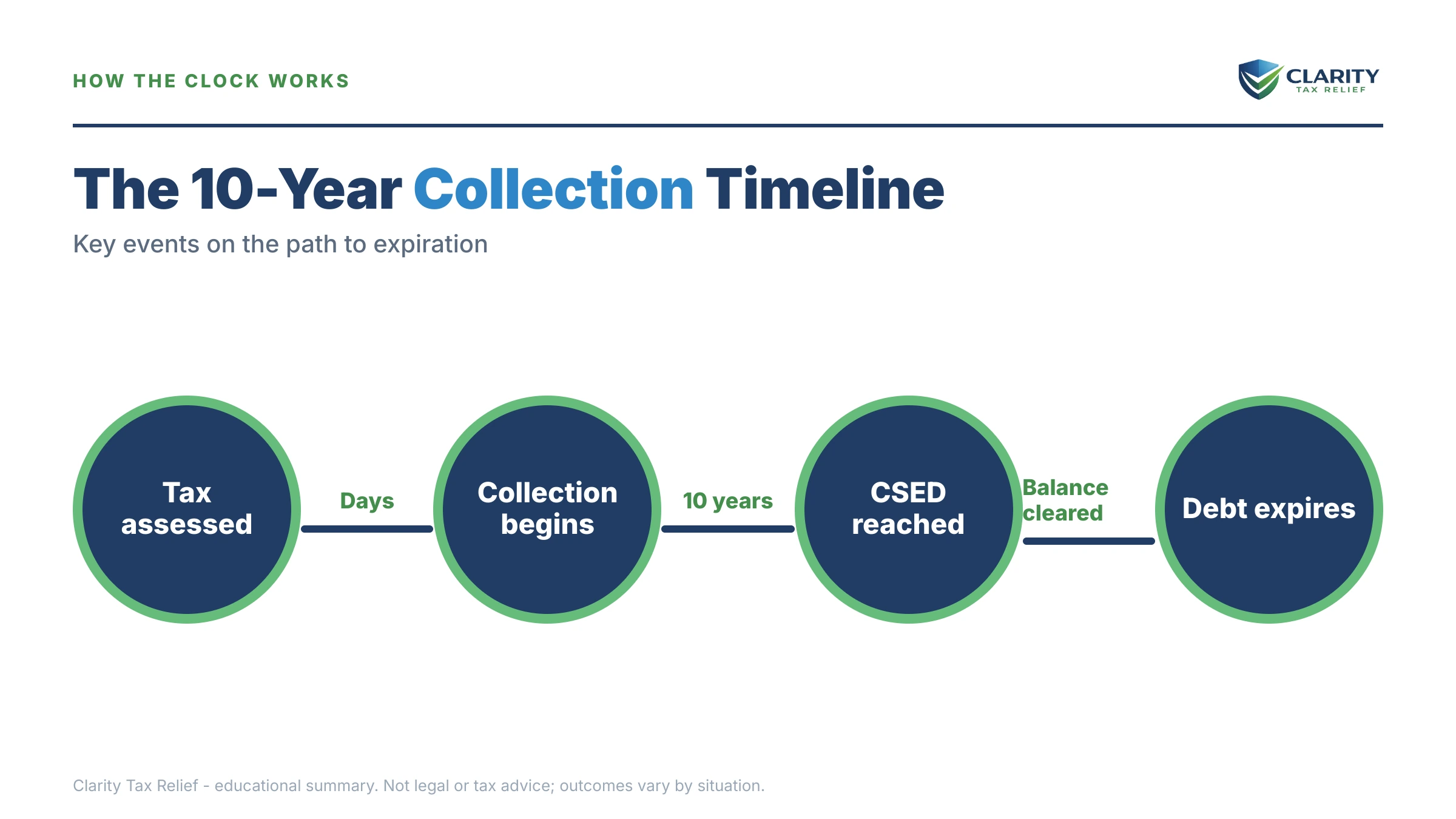

The short answer: how long can the IRS collect back taxes? 10 years from the date each tax was assessed — a deadline called the CSED (Collection Statute Expiration Date). After that date passes, the remaining balance is written off. But offers in compromise, bankruptcy, and appeals pause the clock, so your real date may be later.

The balance is from years ago — maybe a decade of interest has piled onto a bill you couldn't cover back when you were still working, and now you're managing it on a fixed income. You need to know one thing: does this ever end? It does, on a specific calendar date — and where you stand relative to that date should drive every decision you make from here.

Here's the catch: that date isn't printed on any letter the IRS has ever mailed you. It lives in your IRS account transcript, and the image below shows you exactly what that document looks like and where to look for the date that starts your clock.

⏱ Your clock: there is no response deadline attached to the 10-year rule — the clock runs on its own. But interest and the 0.5% monthly failure-to-pay penalty keep accruing until the CSED, and the IRS can lien, levy, and offset refunds right up to the expiration date. The statute limits how long you can be collected from, not how much the balance grows in the meantime.

How long can the IRS collect back taxes? The 10-year rule explained

The IRS has 10 years from the date a tax is assessed to collect it, under IRC §6502 — a deadline the IRS calls the Collection Statute Expiration Date, or CSED. "Assessed" is the key word, and it's where most people miscount by a year or more.

The clock does not start with the tax year. It starts when the IRS formally records the debt on its books. For a return you filed on time, assessment usually happens within a few weeks of processing. So a 2018 return filed in April 2019 was typically assessed in mid-2019 — and expires in mid-2029, not 2028.

Each assessment has its own separate 10-year clock. That matters in three common situations:

- Multiple years owed: your 2017, 2019, and 2021 balances each have their own CSED. One can expire while the others keep running.

- Audit and penalty additions: if the IRS audited a year and added tax later (Transaction Code 290 or 300 on your transcript), that addition got its own assessment date — and its own 10 years — even though it's the same tax year.

- Late-filed returns: if you filed a 2015 return in 2023, the clock started in 2023. An old tax year is not the same as an old assessment.

Two myths worth killing right away. First, making a payment does not restart the 10 years — that's a private-debt rule that doesn't apply to the IRS. Second, the clock never starts on a year you haven't filed, because there's nothing assessed yet. And don't confuse this with the separate statute governing how long the IRS has to assess tax in the first place — for example, the ERC statute of limitations gives the IRS five years to assess Employee Retention Credit claims; only once something is assessed does the 10-year collection window begin.

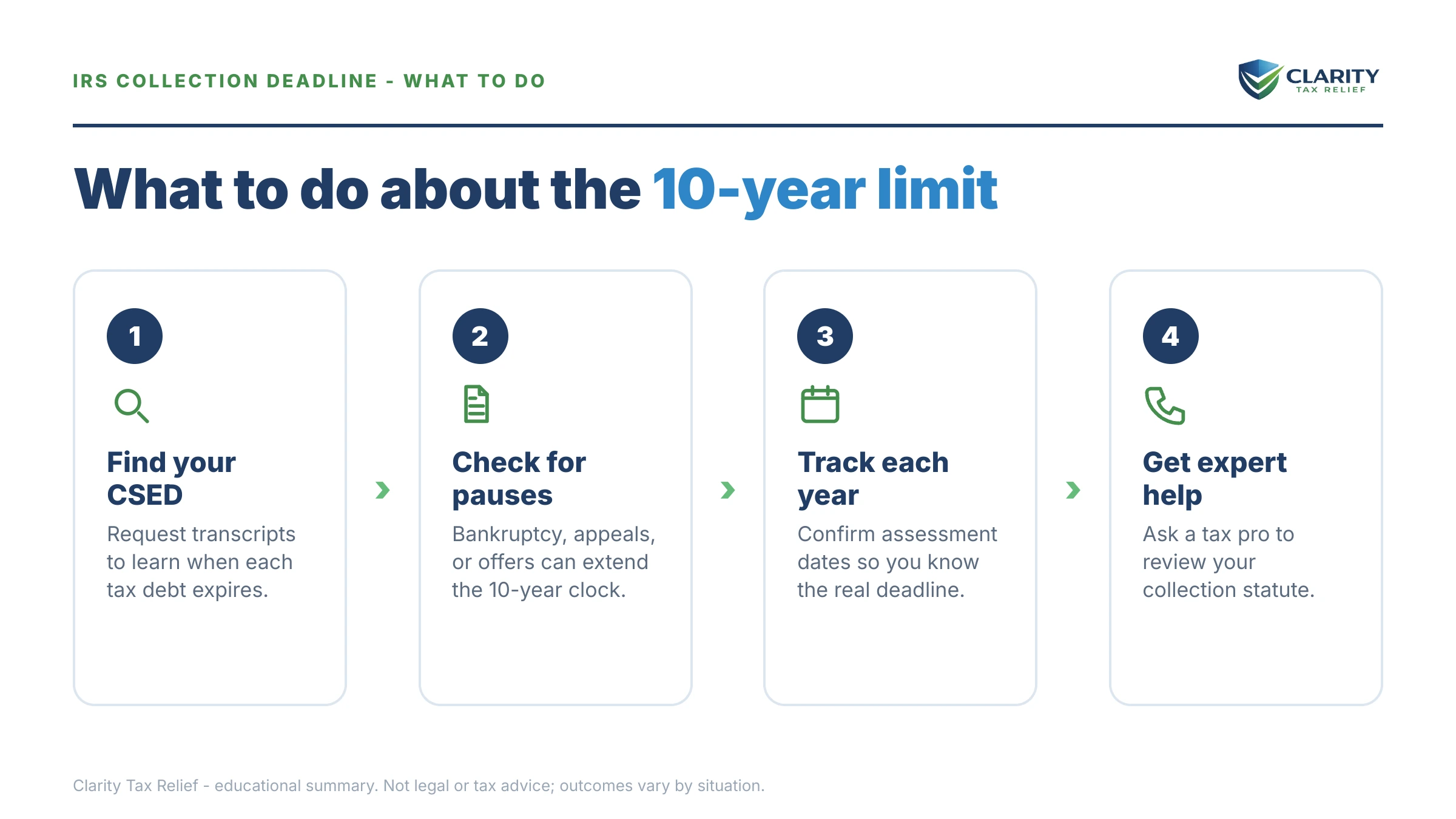

How to find your exact CSED date

Your CSED is calculated from the assessment date printed on your IRS account transcript — it appears next to Transaction Code 150 for the original return. Pull the transcript for every year you owe through your IRS online account, and check for later assessments too (codes 290 and 300), because each carries its own date.

Reading a transcript takes some getting used to — our guide on how to read an IRS account transcript walks through it line by line. Once you have each assessment date, the base math is simple: assessment date + 10 years = your starting CSED. Then you adjust for anything that paused the clock (next section). You can estimate your own dates with our CSED Calculator, which estimates expiration based on your assessment dates and tolling events.

Three more ways to pin it down:

- Ask the IRS directly. A collections representative can read you the CSED for each balance. Get the date for every year, not a single combined answer.

- Authorize a professional. With a power of attorney, an experienced tax professional can pull the IRS's own internal CSED calculations — the figures the IRS is actually using, tolling included.

- Don't rely on notices. The annual CP71 reminder shows your growing balance but never the expiration date. The IRS has no obligation to tell you the clock is running out.

What pauses the 10-year collection statute (tolling)

Certain events legally stop the CSED clock — and every one of them is something you initiate. This is the trap in the 10-year rule: the actions people take to fight a debt often extend how long the IRS can collect it. If your dates matter, know what each move costs before you make it. Our deep dive on what extends the IRS collection statute covers each event in detail; here's the reference table.

| Event | Clock stops? | How much time it adds |

|---|---|---|

| Offer in compromise pending | Yes | The entire review period, plus 30 days after rejection or return — and any appeal time on top. |

| Bankruptcy | Yes | The full automatic-stay period, plus 6 months after the case closes. |

| CDP hearing (Form 12153) | Yes | While the hearing and any Tax Court review are pending; if under 90 days remain afterward, the IRS gets at least 90. |

| Pending installment agreement request | Yes | While the request is under review, plus 30 days after a rejection and during any appeal. |

| Innocent spouse request | Yes (requesting spouse) | While the IRS is barred from collecting on the request, plus 60 days. |

| Living outside the U.S. | Yes | A continuous absence of 6 months or more stops the clock for the entire absence. |

| Military combat-zone service | Yes | The qualifying service period, plus 180 days after it ends. |

| Active installment agreement or CNC status | No | None — the clock keeps running the whole time. This is the strategic core of the next sections. |

One more way the date moves: a signed Form 900 waiver, which voluntarily extends the CSED. Since the 1998 IRS reforms, the IRS mainly requests these alongside certain partial-pay installment agreements. It's the only situation where your signature — not a statute — pushes the date out, which is exactly why you should never sign one without understanding what it changes.

What happens if you ignore it while the clock runs

The 10-year statute is not a grace period — the IRS can and does enforce for the entire decade. If you do nothing, the automated system works through this sequence, and in 2026 that automation matters more than ever: the IRS workforce shrank roughly 27% in 2025, but notices, liens, and levies are issued by computers that never stopped.

- Assessment and first bill. Interest and the monthly failure-to-pay penalty begin accruing immediately and continue until the balance is paid or the statute expires.

- The notice ladder. Reminder notices give way to a CP504 (the IRS can seize your state refund) and then an LT11 or Letter 1058 final notice, which opens a 30-day window to request a CDP hearing before levies begin.

- Federal tax lien. A Notice of Federal Tax Lien becomes public record, attaching to your home and other property and complicating any sale or refinance.

- Levies. Bank accounts (with a 21-day hold before funds leave), wages (continuous until released), and federal benefits. Yes, the IRS can garnish Social Security — up to 15% through the Federal Payment Levy Program.

- Ongoing offsets and certifications. Every tax refund you're owed gets applied to the debt, year after year. If the balance grows past $66,000 (the 2026 threshold), the IRS can certify it to the State Department, blocking passport issuance or renewal.

- The final years. As a large balance nears expiration, the IRS can sue to "reduce the debt to judgment" — converting it to a court judgment that survives past 10 years. It's rare and generally reserved for large-dollar cases, but it's the reason big balances shouldn't simply be waited out unmanaged.

Not sure how many years are left on your balance?

Every month, interest compounds and the automated system keeps escalating — while some resolution moves quietly add years to your clock. An experienced tax professional will pull your transcripts, work out the CSED for every year you owe, and map the option that protects your dates. Free and confidential.

Your options — and which ones protect the clock

Every IRS resolution option interacts with the CSED differently, and when your expiration date is close, that interaction can matter more than the monthly payment. The general mechanics of each program are covered in our guide on how to settle tax debt yourself; here's how each one treats your clock.

| Option | Pauses the clock? | When it fits with limited time left |

|---|---|---|

| Currently Not Collectible | No | Genuine hardship, fixed income. Levies stop while the statute keeps running — the debt can expire while you're protected. |

| Partial-pay installment agreement | No* | You can afford something but not full payoff before expiration. *Watch for a Form 900 waiver request. |

| Streamlined installment agreement | No | Balance ≤ $50,000, up to 72 months, minimal financial disclosure. Best when you can realistically pay off within the window. |

| Offer in compromise (Form 656) | Yes | Strong when many years remain and the math genuinely favors you. Risky near the CSED — a rejected offer hands the IRS back the review time plus 30 days. |

| Bankruptcy | Yes | Broader debt problems beyond taxes. Adds the stay period plus 6 months to the IRS clock. |

| CDP hearing | Yes | Stopping an imminent levy or proposing an alternative — valuable rights that cost clock time. |

The pattern to notice: the two options that pause nothing — CNC and a partial-pay agreement — are the natural fits for someone whose statute is already well underway. Both require a financial statement (Form 433-F for most individuals) showing what you can actually afford under IRS expense standards. The options that pause the clock aren't wrong; an offer in compromise ($205 application fee, 20% down on lump-sum offers, both waived with low-income certification, and roughly 1-in-5 acceptance in FY2024) can still make sense with six or eight years remaining. The mistake is choosing without knowing your dates.

Worked example: $48,300, Social Security income, four years on the clock

This is a hypothetical, but it's a common shape. Say you owe $48,300 from your 2019 return, filed and assessed in July 2020, and you now live on $2,400 a month in Social Security. Your CSED is roughly July 2030 — about four years away as of mid-2026. Here's the math that should drive your decision:

- What the IRS can actually take: the 15% Social Security levy would cost you $2,400 × 15% = $360 a month. Over the roughly 48 months remaining, that's $360 × 48 = $17,280 maximum — barely a third of the $48,300 balance, assuming no other assets.

- What CNC does: if your budget shows the $360 would prevent basic living expenses, Currently Not Collectible status stops the levy entirely while the clock keeps running. In July 2030, whatever remains is written off.

- What a mistimed OIC does: file an offer that sits under review for 10 months and gets rejected, and your CSED moves out about 11 months (review time plus 30 days) — to roughly June 2031. You'd have paid $205 to give the IRS an extra year, unless low-income certification (AGI ≤ 250% of the poverty level) waived the fee.

- One more note: at $48,300, this balance sits below the $66,000 passport-certification threshold for 2026 — but interest and penalties are still compounding, so a balance near the line can cross it.

Nothing here is guaranteed — CNC depends on what your Form 433-F actually shows, and the IRS reviews hardship cases periodically. But the arithmetic explains why, for a fixed-income retiree with a mature debt, protecting the clock often beats attacking the balance. If this is your situation, our guide for people who are retired and owe back taxes goes deeper on the fixed-income specifics.

State back taxes don't follow the 10-year rule

The federal 10-year statute applies only to the IRS — states set their own collection windows, and several are dramatically longer. If you owe both, resolve them as two separate problems with two separate clocks.

| Agency | Collection window | Notes |

|---|---|---|

| IRS | 10 years from assessment (IRC §6502) | Pausable by the tolling events above; extendable by Form 900 waiver or judgment. |

| California FTB | 20 years (R&TC §19255) | Twice the federal window — see California's 20-year collection statute. |

| New York | Enforced via tax warrant | A warrant operates like a civil judgment and public lien — see New York tax warrants, and confirm timelines with the NY Department of Taxation and Finance. |

| Other states | Varies widely | Some longer than the IRS, some shorter, some renewable. Verify with the state agency — never assume 10 years. |

How to respond, step by step

- Pull your account transcript. Download the account transcript for every year you owe from your IRS online account — one transcript per tax year.

- Find each assessment date. Locate the date beside Transaction Code 150 — and any later 290 or 300 assessments — because each one starts its own 10-year clock.

- Compute each CSED. Add 10 years to each assessment date, then add time for any tolling events on your record: a pending offer in compromise, a bankruptcy, or a CDP hearing.

- Match your remedy to the time remaining. Choose the option that fits your clock — hardship status or a partial-pay plan preserves it, while an offer in compromise or bankruptcy pauses it.

- Verify before signing anything. Never sign a Form 900 waiver or file an offer without knowing exactly how it moves your dates — get a free professional review first.

When you can handle this yourself

Plenty of CSED questions don't need professional help. You can handle this on your own if:

- You owe one recent year with a clean history. If your only assessment was last year, the CSED is nearly a decade away and irrelevant to your planning — pick a payment option on the merits and move on.

- Your transcript is simple. One TC 150 date, no offers, no bankruptcies, no hearings: assessment date plus 10 years is your answer, and you can compute it in five minutes.

- You can pay in full within 180 days. A short-term plan costs nothing to set up and makes the statute a non-issue.

Experienced help changes outcomes in the harder cases: transcripts showing multiple assessments or past tolling events, where the real CSED can differ from your math by years; a levy already hitting Social Security or a bank account while the clock runs; multiple years where some balances are near expiration and others aren't (paying the wrong year first wastes money); unfiled years mixed with assessed ones; and any situation where the IRS is asking you to sign a Form 900 waiver or you're weighing an OIC against simply protecting the time you have. In those cases, the professional's first job isn't negotiating — it's getting the dates right, because everything else depends on them.

Terms on your transcript and notices, decoded

- CSED — Collection Statute Expiration Date: the day the IRS's legal right to collect a specific assessment ends.

- Assessment — the formal recording of a tax debt on the IRS's books; the event that starts the 10-year clock.

- Transaction Code 150 — the transcript line showing your return posted; the date beside it is your original assessment date.

- Tolling — a legal pause in the collection clock caused by events like a pending offer, bankruptcy, or appeal.

- Form 900 waiver — a document you sign that voluntarily extends the CSED; the IRS may request one with certain partial-pay agreements.

- Reduce to judgment — a federal lawsuit converting a tax debt into a court judgment, letting collection continue past the 10 years; rare and typically large-dollar.

If your transcript shows dates or codes that don't match what you expected — or the IRS's CSED answer differs from your own math — a free review with an experienced tax professional can pin down your real dates before you commit to any plan: (888) 825-7779.

10-year rule questions, answered

Does IRS tax debt really go away after 10 years?

Yes — once the CSED passes, the IRS can no longer levy or sue to collect, and it writes off the remaining balance. But the 10 years runs from the assessment date, not the tax year, and events like an offer in compromise, bankruptcy, or a CDP hearing pause the clock and push the date later. Always verify your real date on a transcript before counting on it.

Does making a payment restart the IRS 10-year clock?

No. Unlike some private-debt statutes of limitations, a voluntary payment does not restart or extend the CSED. What does move the date is signing a Form 900 waiver or taking an action that pauses collection by law — filing an offer in compromise, filing bankruptcy, or requesting a Collection Due Process hearing. Paying is safe; signing without reading is not.

How do I find my exact CSED date?

Pull the IRS account transcript for each year you owe and find the assessment date next to Transaction Code 150 — then add 10 years and adjust for any tolling events. You can also call the IRS and ask for the CSED on each balance, or authorize a tax professional to obtain it in writing. The date is never printed on collection notices.

Does an installment agreement extend the 10-year statute?

An active installment agreement does not pause the CSED — the clock keeps running the entire time you pay. Only the pending request tolls it briefly (while the IRS considers it, plus 30 days if rejected). The exception to watch: on some partial-pay agreements the IRS asks you to sign a Form 900 waiver extending the date. Read anything you sign.

If I never filed a return, is the 10-year clock running?

No. The clock starts at assessment, and nothing is assessed until you file or the IRS files a substitute for return (SFR) for you. An unfiled year has no expiration date at all — it can follow you indefinitely. Filing the return is what starts the countdown, which is one more reason unfiled years should be resolved first.

Can the IRS collect after the 10 years expire?

Generally no — levies must stop and the balance is written off. There are two exceptions: the IRS sued to reduce the debt to a court judgment before expiration (rare, and usually reserved for large balances), or tolling events pushed your true CSED later than you calculated. Confirm the current date on your transcript before assuming a balance has died.

Will the IRS tell me when my tax debt expires?

No. The CSED does not appear on any collection notice, and the IRS has no duty to warn you it is approaching. The annual CP71 reminder shows your growing balance but not the expiration date. You have to compute it yourself from your account transcripts — or have a professional pull the IRS's own CSED figures — to know where you stand.

What happens to a federal tax lien when the CSED passes?

The Notice of Federal Tax Lien self-releases by its own terms once the collection statute expires, unless the IRS refiled it based on an extended date. County records don't always update automatically, so if a stale lien is blocking a sale or refinance, request a Certificate of Release from the IRS to clean up the record.

Do state tax debts also expire after 10 years?

No — every state sets its own collection statute, and many are longer than the IRS's. California's FTB has 20 years to collect under R&TC §19255, and New York enforces through tax warrants that function like civil court judgments. Never apply the IRS 10-year rule to a state balance; check with that state's tax agency.

Is waiting out the CSED a legitimate strategy?

It can be — hardship status and partial-pay agreements exist precisely because the law limits how long the IRS can collect. It is legal to pay only what your finances allow within the window; it is not legal to hide income or assets to run out the clock. Expect the IRS to review your finances periodically and to get more attentive in the final years.

For a closer look at what expiration actually looks like on your account — and the ways people miscount it — see does IRS debt go away after 10 years and does an IRS tax lien expire. The IRS's own resources on payment options are at IRS.gov/payments and its payment plans page; if collection is causing hardship the IRS won't address, the independent Taxpayer Advocate Service can intervene.

Your next 24 hours

- Find your assessment dates. Log into (or create) your IRS online account and download the account transcript for the oldest year you owe. The date next to code 150 is where your clock started.

- Gather your paperwork. Every IRS notice you've kept, your most recent return, and a simple monthly budget — income (Social Security, pension, wages) against essential expenses. That budget is what determines whether hardship status or a partial-pay plan fits.

- Get your dates verified free. Call (888) 825-7779 or use the 2-minute form for a free case review before you sign anything that could extend your statute. Interest and penalties accrue monthly either way — the clock only helps you if you know where it stands and protect it.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.