Unfiled Tax Returns

How Many Years of Back Taxes Do I Have to File? The 6-Year Rule (2026)

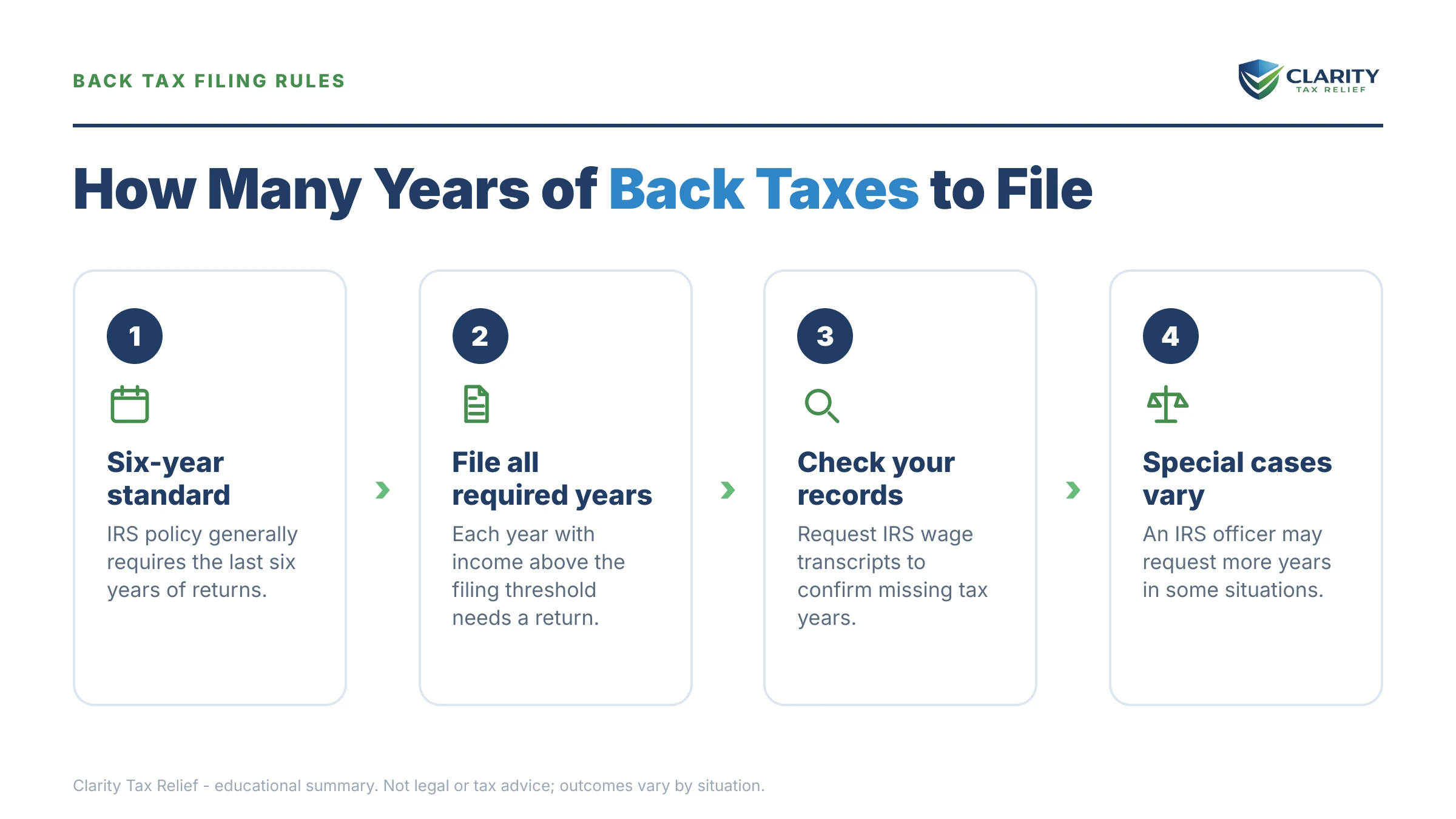

How many years of back taxes do I have to file? In most cases, six. IRS Policy Statement 5-133 treats the last six years of returns as full compliance. You may need more years if the IRS filed a substitute return or a notice demands a specific year — and refunds are only recoverable for the last three.

Maybe the filing slipped during the divorce — the returns were always your ex's job, or splitting one household into two swallowed every spare hour — and now several Aprils have gone by unanswered. The good news is specific: the IRS almost never wants every missing year. It wants six in most cases — the six-year period comes from IRS Policy Statement 5-133, and IRS managers can require additional years with managerial approval when the facts warrant — and often the practical list is shorter than the pile in your head.

This guide gives you the exact rule, the situations that change your number, the three deadlines quietly running on every unfiled year, and how to rebuild returns when the paperwork stayed with your ex. Farther down, the image shows you exactly what the IRS's record of your income looks like and where to find each year's reported wages — it's the document that makes filing possible even with no records of your own.

⏱ The one hard deadline: a refund on an unfiled return expires 3 years from that return's original due date. Your 2023 refund (return due April 15, 2024) is gone after roughly April 15, 2027 — and for most filers, the 2022 refund window already closed in April 2026. Balance-due years have no expiration; penalties and interest just keep growing.

Why six years is the standard answer: IRS Policy Statement 5-133

IRS Policy Statement 5-133 directs that enforcement of delinquent returns normally extends to six years of unfiled returns. That's the internal guidance IRS employees follow when deciding how far back to make a non-filer go. File the last six years, and in the IRS's own language you're back in "filing compliance" — the status you need before any payment plan, hardship status, or settlement gets approved.

Two things about the rule matter. First, it's policy, not statute — a manager can require more than six years when the older years involve large income, business activity, or signs of deliberate avoidance. In routine wage-earner cases, that rarely happens. Second, the six years are the six most recent required years: if your income in a given year was below that year's filing threshold, you may not owe a return for it at all.

The rule also cuts the job down to size. Someone who hasn't filed taxes in 10 years usually files six returns, not ten. Someone who hasn't filed in 5 years files all five, because five is inside the window. The lookback is a ceiling on the routine case — not a promise, and not a reason to skip a year the IRS has already acted on.

How many years of back taxes do I have to file in my situation?

Six is the default, but four situations move the number — sometimes up, sometimes down. Find your row:

| Your situation | Years to file | Why |

|---|---|---|

| Routine non-filer, no IRS contact yet | Last 6 required years | Policy Statement 5-133 treats six years as full compliance |

| IRS filed a substitute return (SFR) for a year | That year, regardless of age — plus the standard 6 | An original return triggers reconsideration and usually lowers the assessment |

| An IRS notice names specific years (CP59, CP518, LT26) | Every year the notice demands | A named year is no longer discretionary — the IRS is actively working it |

| You're owed refunds | At minimum the last 3 years | Refunds expire 3 years from the original due date — file before they lapse |

| Applying for a payment plan, OIC, or CNC status | All 6 — no exceptions | The IRS rejects resolution requests while required returns are missing |

| High income, business income, or fraud indicators in older years | Possibly more than 6 | Managers can extend the lookback when older years are significant |

| Lender, immigration, or FAFSA needs proof of filing | Whatever the third party requires — often 2 | Their requirement is separate from (and usually shorter than) the IRS's |

One row deserves emphasis for anyone whose ex handled the taxes: an SFR year never ages out. If the IRS filed a substitute return for you in a year outside the six-year window, filing your real return for that year is almost always worth it — because the SFR version is built to overstate what you owe, as the worked example below shows in dollars.

Business owners have a harsher rule to know: the six-year lookback is an individual-income-tax practice. Payroll returns don't get the same grace — unfiled 941 returns carry personal-liability exposure for every missing quarter, and the IRS pursues them year by year.

The three clocks running on every unfiled year

Every unfiled return has three separate statutes attached, and only one of them works in your favor. Understanding them is the difference between panic and a plan:

The refund clock (RSED) — 3 years, and it's yours to lose. You must claim a refund within three years of the return's original due date. Miss it and the money is forfeited to the Treasury — it can't even be applied to other years you owe. If a refund from 3 years ago is sitting in an unfiled year, that year jumps to the top of your list.

The assessment clock (ASED) — never starts until you file. The IRS normally has three years after you file to audit and assess more tax. An unfiled year has no start date, so it stays open forever. Filing is the only way to start the clock that eventually closes the year for good.

The collection clock (CSED) — 10 years from assessment, not from the tax year. The 10-year collection statute begins when tax is assessed — either when your return posts or when the IRS assesses an SFR. A 2018 tax year assessed via SFR in 2024 is collectible into 2034. "It's old, so it's expired" is almost never true for non-filers, because nothing expired that never started.

Put together, the clocks explain the strategy every experienced tax professional uses: file the refund years before they lapse, file the required years to close them, and get SFR years corrected so the 10-year collection clock runs against the right number.

What happens if you keep not filing

The IRS non-filer process ends with the IRS filing your return for you — with no deductions, no dependents, and the worst allowable filing status. The sequence is automated, driven by the W-2s and 1099s employers and banks already reported under your Social Security number. It runs in stages:

- CP59 — first notice that no return is on file. A request, not yet a demand. The cheapest moment to act.

- CP516 → CP518 — escalating demands to file. CP518 is the final reminder before the IRS stops asking and starts doing.

- Substitute for Return (SFR) proposed — CP2566. The IRS drafts a return from third-party income data: single or married-filing-separately status, standard deduction only, zero credits. For a divorced parent who actually qualified for head of household, this version is dramatically inflated.

- CP3219N — statutory notice of deficiency. You get 90 days to file your real return or petition Tax Court. Silence means the SFR numbers become a legal assessment.

- Assessment and full collections. The inflated balance enters the collection stream: balance-due notices, a possible federal tax lien, then levy warnings and wage or bank levies. Once the assessed debt tops $66,000 (the 2026 threshold), passport certification is on the table too.

- Refund forfeiture, quietly, in the background. While the balance years escalate, each refund year silently crosses its 3-year line and the money is gone.

A 2026 reality check: the IRS lost roughly 27% of its workforce in 2025, so reaching a human is harder than ever — but the non-filer pipeline above is run by computers that never got cut. The system will build your return without you. The only question is whether the numbers on it are yours or theirs.

Years of unfiled returns and not sure where to start?

We'll pull your IRS transcripts, tell you exactly which years the IRS actually requires, and flag any refund about to expire or SFR inflating your balance — free, confidential, before penalties grow another month.

Your options once the six years are filed

Filing compliance is the key that unlocks every IRS resolution program — none of them are available while required returns are missing. Once the six years post, your balance (if any) can be handled several ways; the broader playbook lives in our guide to how to settle tax debt yourself, but here are the thresholds that decide which door you can walk through:

| Option | Who's eligible | Cost & terms |

|---|---|---|

| Short-term payment plan | Can pay in full within 180 days | $0 setup; interest and penalties continue until paid |

| Guaranteed installment agreement | Owe $10,000 or less (tax only), compliant history | Up to 36 months; approval is required by law if conditions are met |

| Streamlined installment agreement | Owe $50,000 or less (combined tax, penalties, interest) | Up to 72 months, set up online, no financial statement |

| Currently Not Collectible (CNC) | Paying anything would prevent basic living expenses | Collection pauses; debt remains and interest accrues; IRS reviews periodically |

| Offer in Compromise | Assets + future income genuinely can't cover the debt before the CSED | $205 fee; 20% down on lump-sum offers (both waived with low-income certification); roughly 1 in 5 offers accepted in FY2024 |

| Penalty relief (FTA / reasonable cause / AEP) | Clean 3-year history (FTA) or circumstances beyond your control | Free to request; from summer 2026, Automatic Exemption from Penalty (AEP) begins applying some relief with no request needed |

Two notes for multi-year filers specifically. First-time penalty abatement requires a clean prior three years, so it typically helps only the first delinquent year in a stack — the later years need reasonable cause, and a divorce with documented upheaval can genuinely support that argument. And whatever you owe, file even if you can't pay a dollar of it: the failure-to-file penalty is 5% per month — ten times the 0.5% failure-to-pay penalty. You can estimate how much of your balance is penalties and interest with our Penalty & Interest Calculator.

What filing actually changes: a worked example

Say your divorce finalized in 2022 and you stopped filing when the marriage came apart — tax years 2020 through 2025 are all unfiled. The IRS ran SFRs on 2020 and 2021 from your W-2s and a 1099 for the retirement split, and assessed $83,100 combined, tax plus penalties. The SFRs used married-filing-separately status, standard deduction only, no dependents.

In reality, your two kids lived with you and you qualified as head of household for both years. Here's the hypothetical arithmetic:

- 2020 + 2021 (SFR years): real returns with head-of-household rates, child tax credits, and correctly applied withholding bring the combined liability to roughly $46,800 — about $36,300 less than the SFR assessment. Filing originals triggers SFR reconsideration.

- 2023 (refund year): your withholding overshot; the return shows a $2,600 refund. Filed before April 2027, it isn't paid out — it's applied against the older balance. Unfiled past the deadline, it's simply gone.

- 2024 + 2025: modest balances totaling about $4,100 after a job change dropped your withholding.

- Net position: roughly $46,800 + $4,100 − $2,600 ≈ $48,300 — under the $50,000 streamlined line, so a 72-month online payment plan runs about $671/month before ongoing interest and penalties, with no financial disclosure required.

Notice what filing changed beyond the monthly number: at $83,100 assessed, this filer sat above the $66,000 passport-certification threshold. At $48,300, they're below it, inside streamlined territory, and eligible to request penalty relief on top. Every figure here is illustrative — your income, status, and credits set your own math — but the direction is typical: SFR balances shrink when real returns replace them, because the IRS's version deliberately gives you nothing.

Reading your transcripts: the codes that tell you where each year stands

Your IRS account transcript shows, year by year, exactly what the IRS has done — which years are missing, which have SFRs, and which are already assessed. Pull them free through your IRS online account (our wage and income transcript guide walks through it), and the image below shows what one looks like and where the income entries sit. Then decode what you see:

| What you see | What it means for that year | What to do |

|---|---|---|

| "N/A" or no record of return filed | No return has posted — the year is open and unworked | File it if it's inside your required list; you're ahead of the machine |

| Code 150 with "substitute" language or bare-bones figures | A return posted — possibly the IRS's SFR, not yours | Compare to what you'd actually owe; file an original for reconsideration if it's an SFR |

| Code 806 | Your W-2/1099 withholding was credited to the year | Good news — it counts against any balance, even on SFR years |

| Code 290 | Additional tax assessed — often the SFR assessment posting | This balance is now collectible; correcting it means filing the real return |

| Code 971 | A notice was issued for that year | Match the date to the letter you received; it tells you which stage you're at |

| Code 599 | Your delinquent return was received and secured | Confirmation that a back-year filing landed — keep it with your records |

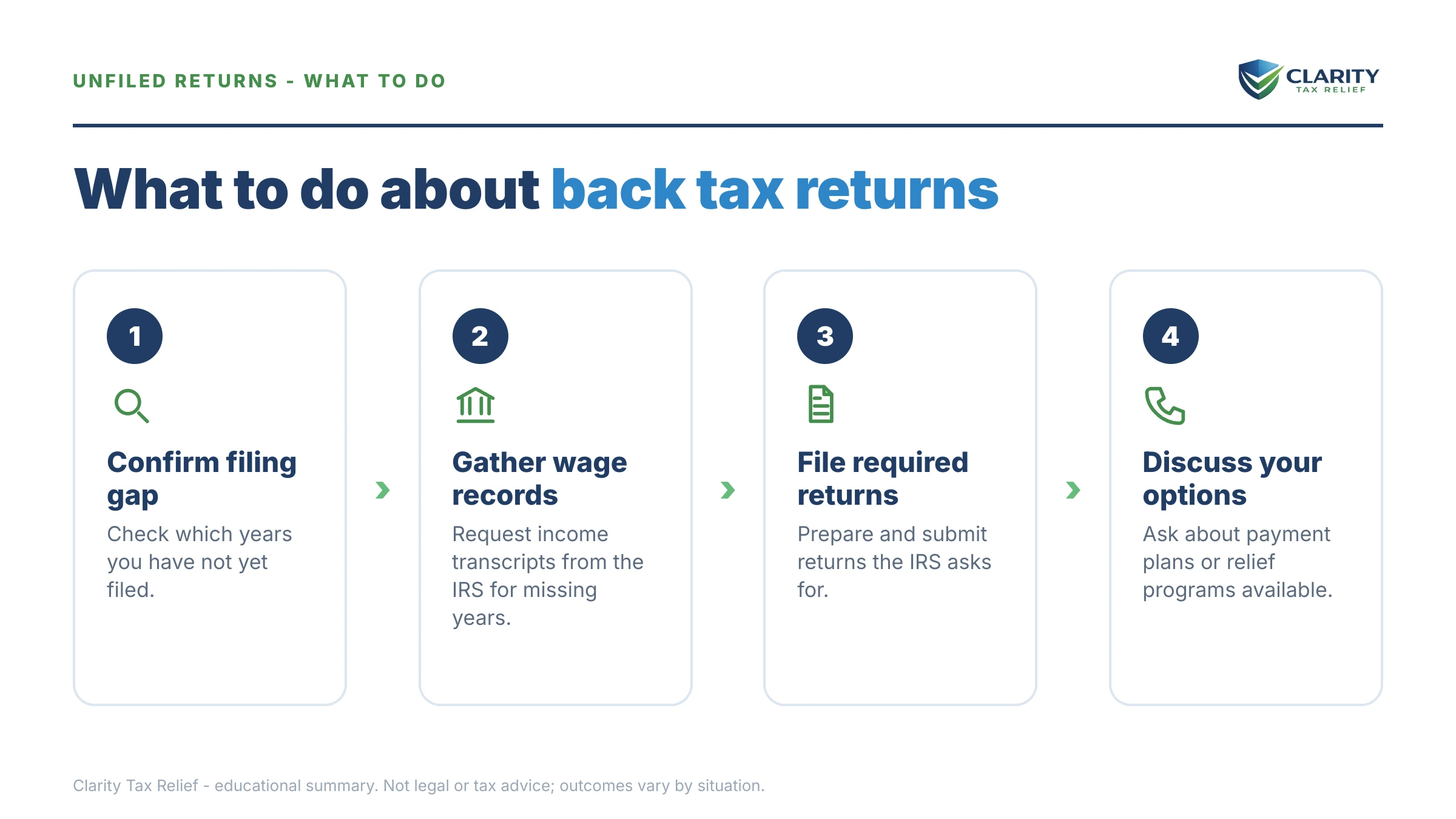

Transcripts also solve the divorced filer's biggest practical problem: the records that stayed in your ex's filing cabinet. Wage and income transcripts list every W-2, 1099, and 1098 reported under your SSN for roughly the last ten years — enough to file back taxes with no records of your own, supplemented by bank statements for self-employment income transcripts won't show.

How to file your back taxes, step by step

- Pull your transcripts — get wage and income transcripts plus account transcripts for at least the last six years through your IRS online account — they show every W-2, 1099, and IRS action on file.

- Confirm your required years — start with the last six, then add any year with a substitute return, any year named on an IRS notice, and any of the last three years with a refund coming.

- Reconstruct your records — combine transcripts with bank statements, old pay stubs, and — after a divorce — copies of prior joint returns and documents from the divorce file.

- Prepare and file oldest to newest — use each year's correct Form 1040 and tax tables, paper-file the older years, and submit original returns for any SFR years to request reconsideration.

- Resolve the balance — once returns post, set up a payment plan, request Currently Not Collectible status, or pursue an Offer in Compromise — and request penalty relief where you qualify.

- Confirm every year posted — check each year's account transcript for code 150 or 599, and keep proof of mailing until you see all years on file.

One ordering detail worth its own sentence: file oldest to newest so refunds and carryforwards flow in the right direction, and mail each year in its own envelope with tracking — batched years in one envelope are a classic cause of "lost" returns. Coming forward on your own timeline, before the IRS makes contact, also matters more than most people realize; our guide to voluntarily filing old tax returns explains why the sequence protects you.

When you can handle this yourself — and when help changes the outcome

Plenty of back-filing cases are genuinely do-it-yourself. If you're a W-2 employee with one to three missing years, your transcripts show all your income, and you expect refunds or small balances, you can pull transcripts, prepare the returns with each year's software or forms, and mail them — no professional required. The same is true if your only need is proving two years of filing to a mortgage lender.

Experienced help earns its cost in specific situations: an SFR has already been assessed and you need reconsideration done correctly; you have self-employment or business income that transcripts don't capture; the stack spans divorce years where filing status, dependents, and a decree collide (see who pays IRS debt after divorce — the answer surprises most people); the combined balance will exceed $50,000, where financial disclosure and negotiation begin; or collection has already started — a lien filed, a levy warning received. In those cases, the order you fix things in changes the final number, and that's precisely what a professional review determines up front.

Terms you'll see, decoded

- Policy Statement 5-133 — the internal IRS guidance setting six years as the normal enforcement lookback for delinquent returns.

- Substitute for Return (SFR) — a return the IRS constructs for you from third-party data, using the least favorable status with no credits or dependents.

- RSED — Refund Statute Expiration Date; the 3-year deadline to claim a refund before it's forfeited.

- ASED — Assessment Statute Expiration Date; the IRS's window to assess tax, which never opens until a return is filed.

- CSED — Collection Statute Expiration Date; the 10-year limit on collecting an assessed tax, which can be paused by appeals, offers, or bankruptcy.

- Filing compliance — the IRS's term for having all required returns on file; the prerequisite for every payment plan and relief program.

If the six years look likely to end in a five-figure balance like the example above, it costs nothing to have an experienced tax professional map the filing order and the resolution path before you mail the first return — start with a free case review or call (888) 825-7779.

Back-tax filing questions, answered

Do I have to file all 10 years if I haven't filed in 10 years?

Usually not — the IRS's own guidance, Policy Statement 5-133, treats the last six years as full compliance for most people. You'd still file an older year if the IRS filed a substitute return for it, sent a notice demanding it, or if that year has significant self-employment or business income a manager flags. Six is the default, not a legal ceiling.

Can I go to jail for not filing back taxes?

Willful failure to file is technically a crime, but criminal cases are rare and almost always involve large income, deliberate concealment, or ignoring the IRS after direct contact. Taxpayers who come forward and file before the IRS opens an investigation are overwhelmingly handled through the civil system — penalties and interest, not prosecution. Filing voluntarily is the single best protection you have.

Will I get refunds from old unfiled years?

Only for the last three years. A refund expires three years from the return's original due date — so as of mid-2026, the 2022 refund window has closed for most filers, and the 2023 refund (due April 15, 2024) expires around April 15, 2027. Older refunds are forfeited permanently, but you may still need to file those years to be compliant.

What if the IRS already filed a substitute return for me?

File your real return for that year no matter how old it is. A substitute for return (SFR) uses the worst-case filing status with no dependents, no credits, and only the standard deduction, so it almost always overstates what you owe. Filing an original return triggers SFR reconsideration, and the IRS generally adjusts the assessment down to your actual liability.

Should I file back taxes if I can't pay what I'll owe?

Yes — file anyway. The failure-to-file penalty runs 5% per month, ten times the 0.5% failure-to-pay penalty, so an unfiled return costs you far more than an unpaid one. Filing also starts the assessment and collection clocks and unlocks payment plans, hardship status, and settlement programs, none of which are available while returns are missing.

Can I e-file back tax returns?

Generally only the current year and the two prior years can be e-filed through tax software or a tax professional. Anything older must be printed, signed, and mailed to the IRS on that year's version of Form 1040 — using the correct year's forms and tax tables matters. Mail each year in a separate envelope and keep proof of mailing.

Do states follow the six-year rule for back taxes?

No — the six-year standard is IRS policy only, and each state sets its own rules. Some states expect every missing year, and several collect far longer than the IRS: California's FTB, for example, has a 20-year collection statute. If you owe state returns too, check that state's revenue agency directly rather than assuming the federal lookback applies.

Does my divorce decree decide who files or pays back taxes?

No. A divorce decree binds you and your ex-spouse, but it does not bind the IRS — if a joint return was filed, both spouses remain fully liable regardless of what the decree says, and unfiled years remain each person's own obligation. If your ex was ordered to handle a tax year and didn't, the IRS can still pursue you; your remedy against your ex is in family court.

What filing status do I use on back tax returns after a divorce?

Your status for each year is set by your marital situation on December 31 of that year. Years you were still legally married must be filed as married filing jointly or separately (or head of household if you qualified as considered unmarried); years after the divorce finalized are single or head of household. Getting this right on old returns often changes the balance by thousands.

How long does the IRS take to process back tax returns?

Plan on months, not weeks. Most back-year returns must be paper-filed, and paper processing was already slow before the IRS cut roughly 27% of its workforce in 2025. Watch each year's account transcript for code 150 or 599 to confirm the return posted, and don't assume silence means a problem — but do follow up if a year hasn't posted after several months.

Your next 24 hours

- Make your year list. Write down every unfiled year, then circle the last six, any year an IRS letter has named, and any of the last three years where you expect a refund — that circled list is your real assignment.

- Create your IRS online account and pull transcripts. Wage and income plus account transcripts for each circled year show what the IRS already knows and whether any SFR has been filed — no calls, no waiting on hold.

- Get a free case review. Send us your year list and we'll confirm exactly which returns the IRS requires, flag any refund approaching its 3-year expiration, and map the cheapest path through the balance — the 2-minute form or (888) 825-7779. Every month unfiled adds another 5% failure-to-file penalty; starting now is what stops it.

Primary sources: the IRS's own guidance on filing past due tax returns, its Get Transcript tool for pulling your income records, and the IRS payment plans page for current plan terms once your returns are filed.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.