Business Tax Debt

941 Back Taxes in 2026: What Happens When Your Business Falls Behind on Payroll Taxes

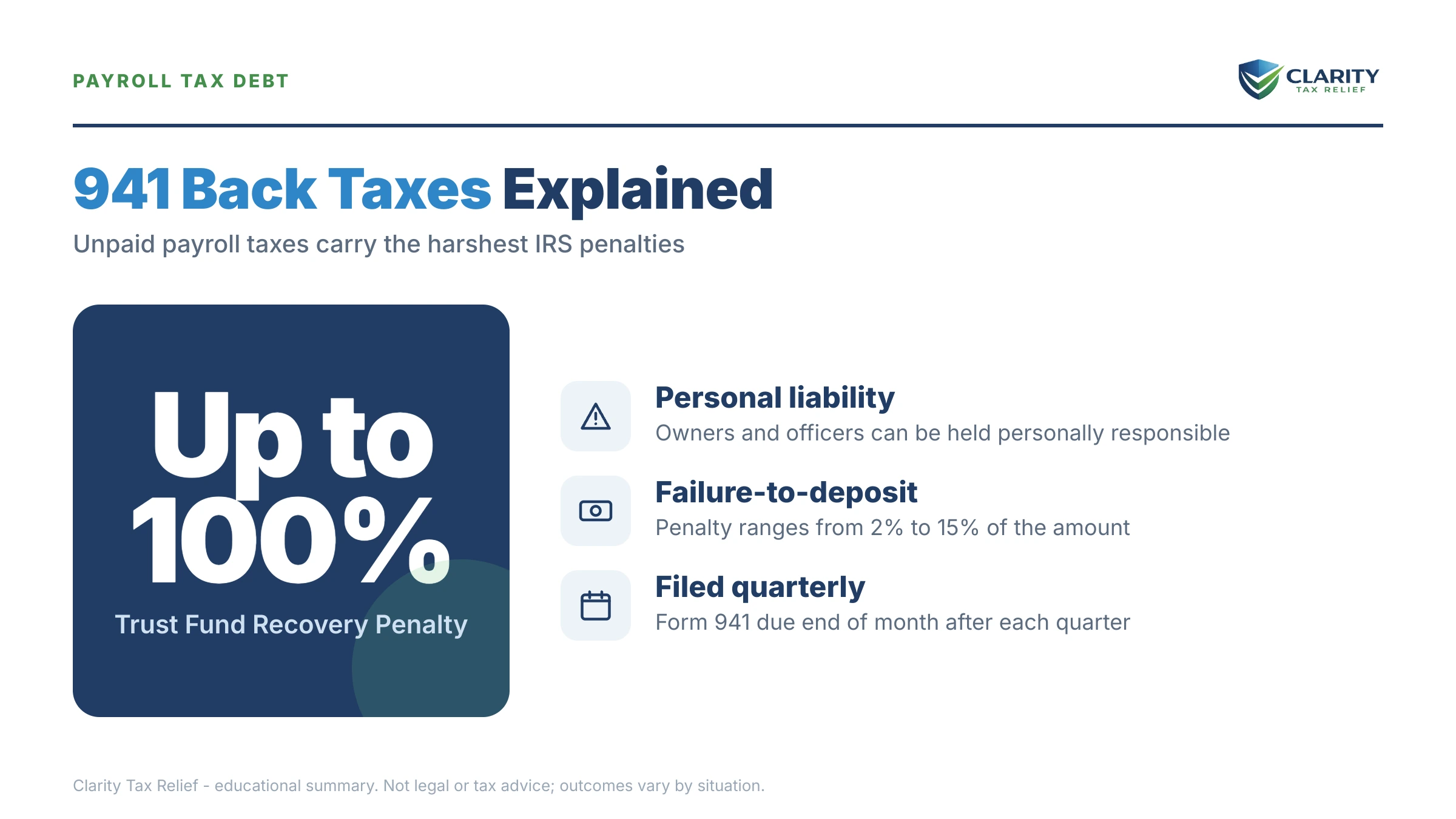

The short answer: 941 back taxes are unpaid federal payroll taxes — the income tax and FICA you withheld from employee paychecks, plus your employer match. The IRS collects them harder than any other tax debt, because roughly half the balance is employee money it can assess against owners and officers personally.

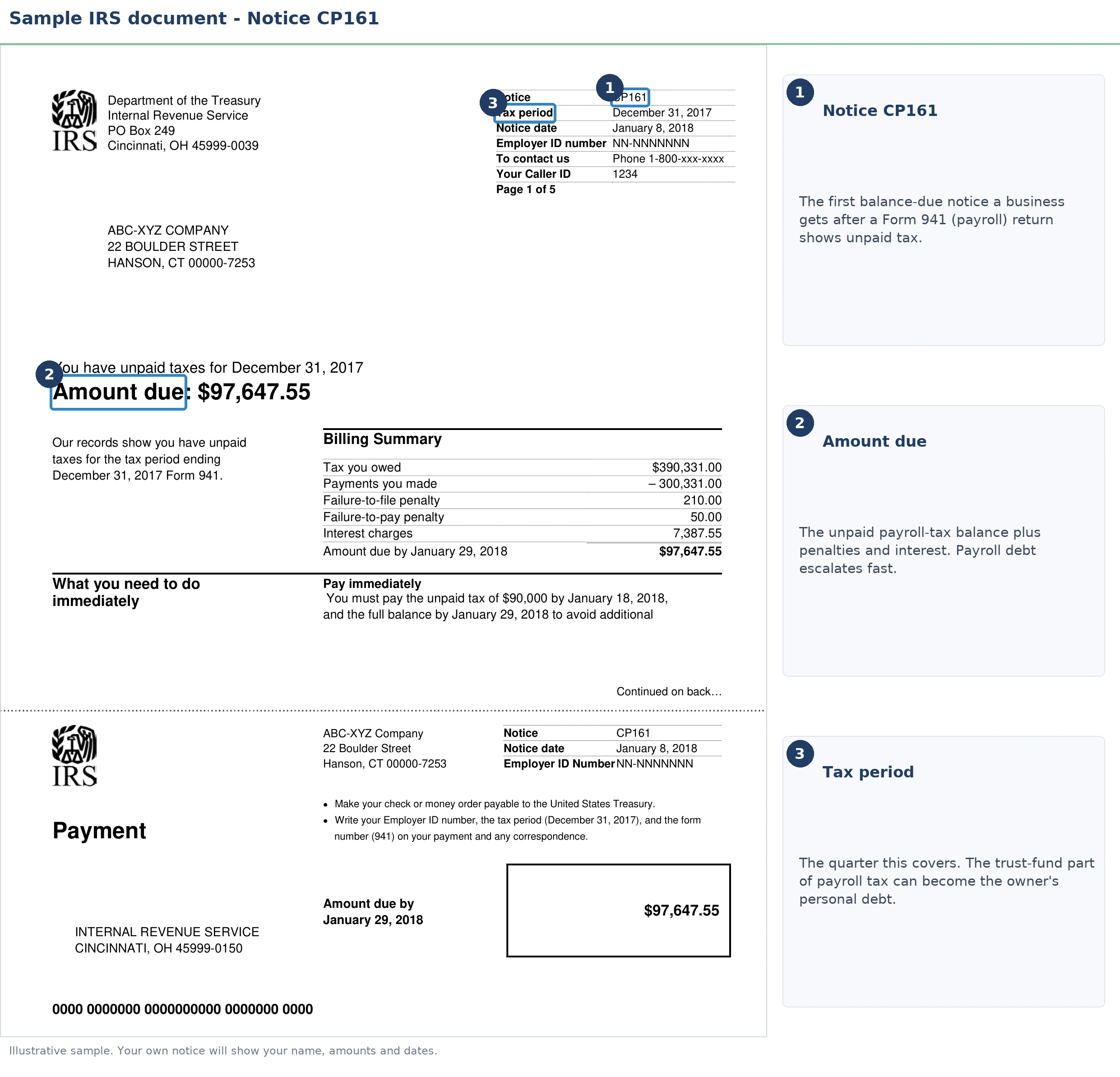

You made a call most owners eventually face: the deposit money went to keeping the crew paid or the lights on, and now the quarterly filings — or the letters that follow them — show a growing 941 balance in your business's name. That decision is fixable, but it sits in a different category than an income-tax debt, and the path out starts with knowing exactly which quarters are assessed and what portion of the balance the IRS considers employee money. The image below shows you exactly what a 941 balance-due notice looks like and where to find the quarter and the figures that matter.

Two features make this debt unique. First, it never stays contained in the business — the withheld "trust fund" portion can pierce a corporation or LLC and land on you as an individual. Second, it draws human attention: payroll cases go to field revenue officers at far lower dollar amounts than personal tax debt does.

⏱ Your real clocks: there is no single grace period on 941 back taxes. Failure-to-deposit penalties stack in tiers up to 15%, interest compounds on top, and if the IRS mails you Letter 1153 proposing the Trust Fund Recovery Penalty, you have 60 days to protest personal liability. Every quarter you stay behind adds a new balance to the pile.

Why 941 back taxes are the tax debt the IRS chases hardest

About half of a typical 941 balance is money withheld from employee paychecks — money the IRS treats as its own, held by you in trust. When you run payroll, you deduct federal income tax and the employee's share of Social Security and Medicare from each check. That money was never yours. Spending it on rent or inventory, in the IRS's eyes, is closer to misappropriation than to falling behind on a bill.

That framing drives everything that follows. The employees still get full credit for their withholding whether or not you deposited it — so every unpaid quarter is a direct loss to the Treasury, not a deferred one. Congress responded with IRC §6672, which lets the IRS collect the withheld portion from the people who ran the business, not just the business itself.

The employer's matching share of FICA is different: it's the business's own liability, and it generally stays with the entity. When you look at your notice or transcript, that split — trust fund versus employer share — is the single most important number on the page, because it defines how much of this debt can follow you home. If your letters reference Form 940 instead, that's the annual unemployment tax, a different animal — the split is explained in our guide to 941 vs 940 back taxes.

How businesses get here matters less to the IRS than you'd hope, but it matters to your fix. The common paths: cash-flow triage (deposits skipped to make payroll), a payroll service that collected the money but never paid it over, quarters that were never filed at all (the IRS can file substitute returns for those quarters, and its numbers are never in your favor), or an entity structure that left the owners exposed in ways they didn't expect — covered in our guide to personal liability for payroll taxes.

The penalty math on late payroll tax deposits

The failure-to-deposit penalty reaches 10% of the unpaid deposit after just 16 days late — before interest and before any late-filing penalty. It's tiered by how late the deposit is, and it applies per deposit, so a business that misses every deposit in a quarter takes the hit on the whole quarter's tax:

| How late the deposit is | Penalty (% of unpaid deposit) |

|---|---|

| 1–5 days late | 2% |

| 6–15 days late | 5% |

| 16 or more days late | 10% |

| Still unpaid more than 10 days after the first IRS notice demanding payment | 15% |

On top of the deposit penalty, an unfiled 941 adds a failure-to-file penalty of 5% per month, up to 25% — ten times the monthly rate of the failure-to-pay penalty. That's why the first move for any behind business is filing every quarter, even the ones you can't pay. Interest then compounds on the whole stack. You can estimate what your quarters have grown into with our Penalty & Interest Calculator, and the full tier mechanics are in our federal tax deposit penalty guide.

One piece of good news: a meaningful share of these penalties can come back off. Reasonable-cause relief applies to deposit and filing penalties when the failure traces to something outside your control, and starting in summer 2026 the IRS's new Automatic Exemption from Penalty (AEP) begins replacing first-time abatement with automatic relief for qualifying taxpayers — no request needed. The payroll-specific paths are covered in 941 penalty abatement.

What happens if you ignore 941 back taxes

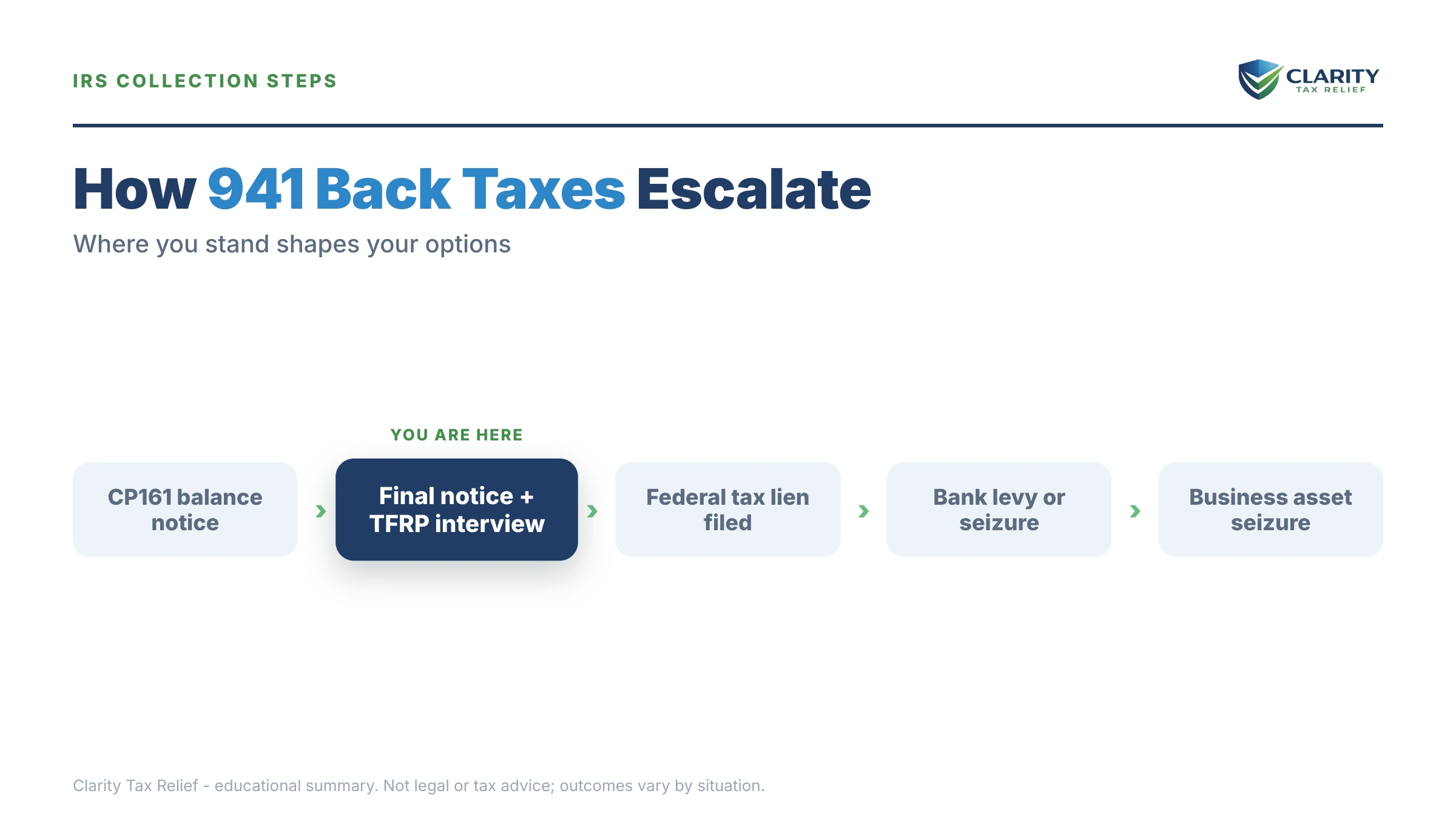

Ignored 941 back taxes escalate on two tracks at once: automated business collection notices, and a human investigation into who should pay personally. The notice track looks like this:

- CP161 — the business balance-due notice. The bill stage: tax, penalty, and interest for a specific quarter, no enforcement power yet.

- CP504B — the business intent-to-levy notice under IRC §6331(d). The IRS can now take the business's state refund, and a federal tax lien against business assets becomes likely. Details in our CP504B notice guide.

- Final notice of intent to levy (Letter 1058 / CP297-series) — starts a 30-day clock and your Collection Due Process rights. After it runs, the IRS can levy the business bank account (funds are held 21 days before they leave) and send levies to your customers for your accounts receivable — which cuts off cash flow at the source.

- Revenue officer assignment — payroll cases get pulled from the automated stream and assigned to a field RO earlier and at lower balances than personal debt. The RO's first demands are always the same: current-quarter deposits and missing returns, now. What that first visit looks like is in revenue officer payroll taxes.

- The TFRP investigation — Form 4180 interviews of everyone who touched the money, then Letter 1153 proposing personal assessment of the trust fund portion against one or more people.

- Personal collection — once the TFRP is assessed, the IRS can lien and levy your personal accounts, wages, and property for the trust fund portion, even if the business closes.

Two 2026 realities sharpen this. The IRS workforce shrank roughly 27% in 2025 — but the notice stream, lien filings, and levies are automated and never paused. And continuing to run payroll while not depositing — quarter after quarter — is what the IRS calls pyramiding, the pattern most likely to turn a civil case into a criminal referral. If that describes your situation, read pyramiding payroll taxes and stop the pattern this pay period.

How the Trust Fund Recovery Penalty makes payroll debt personal

The Trust Fund Recovery Penalty lets the IRS assess 100% of the withheld portion of 941 debt against any "responsible person" who "willfully" failed to pay it over. Both tests are broader than owners expect. A responsible person is anyone with the status and authority to decide which bills got paid — owners and officers, yes, but potentially also a check-signing spouse, an office manager, or a bookkeeper. Willfulness doesn't require bad intent; paying any other creditor while knowing the withholding was unpaid usually satisfies it.

Three things to understand before anyone from the IRS interviews you:

- The IRS can assess multiple people for the same debt. In a jointly run business, both spouses can each be assessed the full trust fund amount (the IRS collects it only once, but pursues everyone until it does). Who qualifies is covered in depth in our Trust Fund Recovery Penalty guide.

- The Form 4180 interview decides most cases. It's a structured questionnaire about who hired, who signed checks, who knew. Casual answers given without preparation are the most common way non-owners get swept in — see Form 4180 interview before you sit for one.

- Letter 1153 is your one administrative window. It proposes the assessment and gives you 60 days to file a written protest. Miss it, and the assessment posts against your Social Security number. The full protest process is in Letter 1153.

The TFRP is also why bankruptcy is a weak escape hatch here: the trust fund portion is a priority claim that survives both Chapter 7 and Chapter 13, though a Chapter 13 plan can at least force structured repayment while the automatic stay holds collection off.

Behind on 941s right now?

Get your payroll tax balance reviewed free before the trust-fund investigation opens. Deposit penalties compound monthly, and once Letter 1153 arrives you have only 60 days to contest personal liability. An experienced tax professional will map your quarters, your exposure, and your fastest path out — no pressure, no obligation.

Your options for resolving unpaid 941 payroll taxes

Every 941 resolution program has the same entry requirement: the business must be current on this quarter's deposits and filings first. The IRS will not formalize any arrangement for a business that's still adding new payroll debt — which is why "stop the bleeding" is step one, not step four. Once you're current, these are the realistic paths (the general mechanics of each program live in our guide to how to settle tax debt yourself; below is how each one behaves specifically for payroll debt):

| Option | Who it fits | Key threshold / requirement | What to know |

|---|---|---|---|

| In-Business Trust Fund Express IA | Operating business, modest balance | Owe $25,000 or less; full pay within 24 months; direct debit required at $10,000–$25,000 | No Form 433-B financials; typically avoids the TFRP investigation while you stay compliant |

| Regular in-business installment agreement | Balances over $25,000 | Form 433-B financial disclosure; usually negotiated with a revenue officer | Lien filing likely; interest and penalties keep accruing during the plan |

| Currently Not Collectible | Business that genuinely cannot pay anything | Documented proof that any payment prevents basic operations | Pauses levies, not the debt; the TFRP against individuals usually still proceeds |

| Offer in Compromise | Rare for operating businesses | $205 fee; current on all recent deposits; IRS math must show the debt is uncollectible | Roughly 1 in 5 offers accepted in FY2024; payroll offers face extra scrutiny |

| Penalty abatement / AEP | Any business with penalty-heavy balances | Reasonable cause with documentation, or automatic relief under AEP starting summer 2026 | Attacks the penalty layer, not the tax; often pairs with a payment plan |

Three payroll-specific notes on that table. The business payroll tax payment plan (IBTF-Express) is the workhorse — for qualifying balances it's fast, it skips financial disclosure, and staying on it is the most reliable way to keep the trust fund investigation from opening. A business offer in compromise on payroll debt exists but is the exception, not the plan — never build your strategy around it. And if the business is winding down or already closed, the playbook changes entirely, because the entity's ability to pay stops mattering and your personal exposure becomes the whole case — see payroll tax debt after a business closes.

| 941 balance | Realistic path | What changes at this level |

|---|---|---|

| Under $10,000 | IBTF-Express agreement, any payment method; aggressive penalty abatement | Usually stays in automated collections; fixable in weeks if you act before CP504B |

| $10,000–$25,000 | IBTF-Express with mandatory direct debit | Lien filing becomes a live risk; direct debit keeps the agreement from defaulting |

| $25,000–$100,000 | Negotiated IA with Form 433-B; possible partial-pay agreement | Revenue officer assignment likely; TFRP investigation typically opens in parallel |

| Over $100,000 | RO-managed resolution; asset review; representation strongly advised | Lien is near-certain, levies on receivables common, and personal assessments move fast |

A worked example: $8,900 in 941 back taxes

Say you and your spouse run a small LLC together, file jointly at home, and the business is two quarters behind for a total of $8,900. Here's how that number typically breaks apart. Each quarter's payroll tax was about $3,850: $1,700 in federal income tax withheld from employee checks, $1,075 for the employees' share of Social Security and Medicare, and $1,075 for your employer match. Two quarters means $7,700 in tax. Add a 10% failure-to-deposit penalty ($770) and roughly $430 in accrued interest and late-pay penalty, and you're at $8,900.

The split that matters: the trust fund portion is 2 × ($1,700 + $1,075) = $5,550 — the amount the IRS could assess against you, your spouse, or both of you personally if the business doesn't resolve it. The employer-share and penalties ($3,350) generally stay with the LLC.

The fix: at $8,900, you're squarely inside IBTF-Express territory. Full payment over 24 months works out to roughly $371/month (interest keeps accruing, so the true payoff runs modestly higher, or you pay it off faster). If one missed quarter traces to a documented event — a hospitalization, a payroll provider failure — a reasonable-cause abatement request could take several hundred dollars of the penalty layer back off. Total cost of acting now: a manageable monthly payment. Total cost of waiting: a lien against the business, a possible levy on your operating account, and a $5,550 assessment against each spouse's Social Security number.

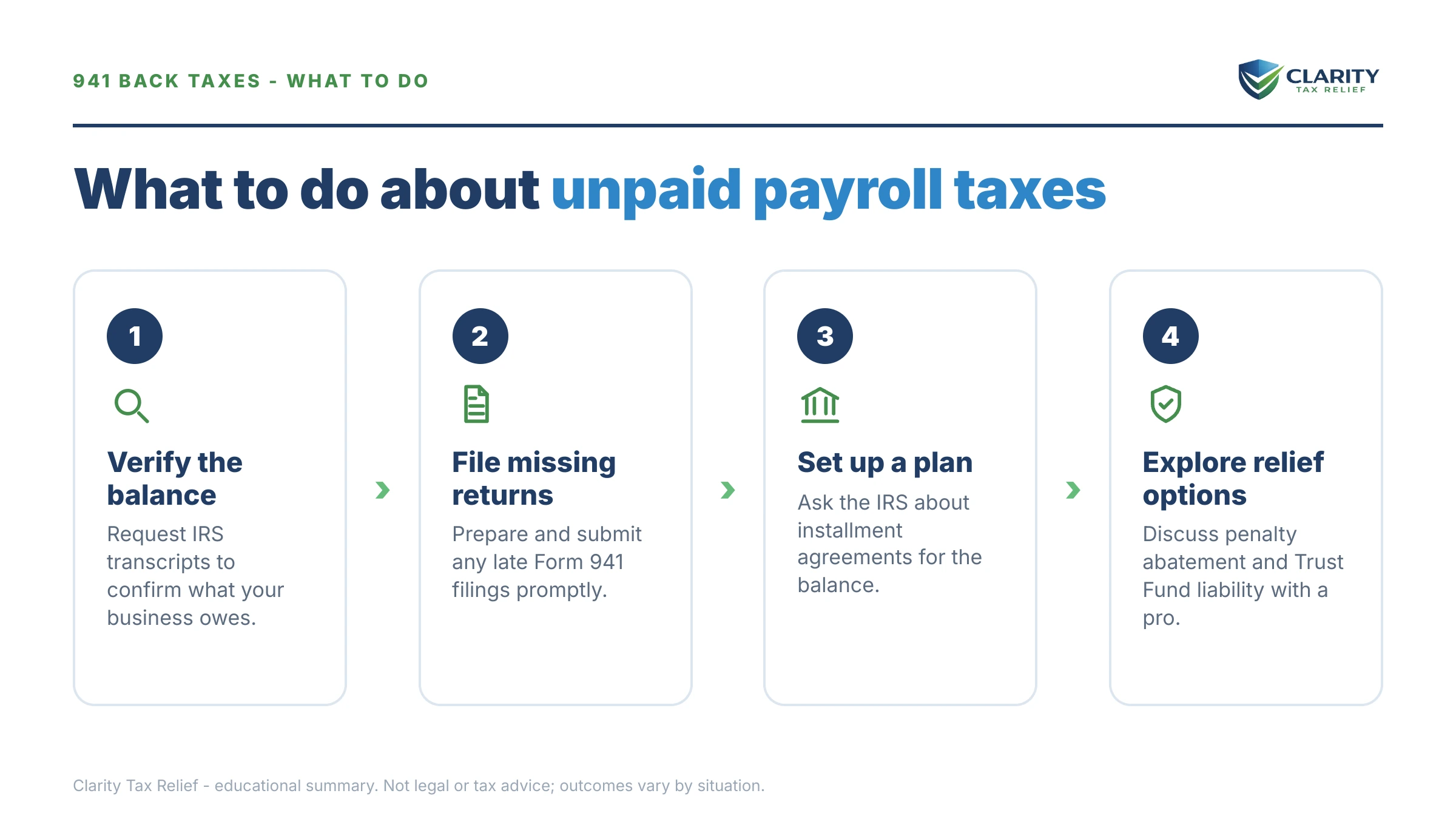

How to respond to 941 back taxes, step by step

- Start depositing this quarter's payroll taxes today — nothing gets approved while new debt is accruing; current compliance is the price of admission to every IRS program.

- File every missing Form 941 — even quarters you can't pay a dime on; unfiled returns block every resolution option and add a separate 5%-per-month late-filing penalty.

- Pull the business's account transcripts — confirm exactly which quarters are assessed and how each balance splits between tax, penalty, and interest.

- Open a resolution before the IRS opens one for you — an In-Business Trust Fund Express agreement under $25,000, or a negotiated agreement with financials above it.

- Answer Letter 1153 within 60 days if it arrives — that written protest is your only administrative shot at contesting personal Trust Fund Recovery Penalty liability.

- Get representation before any Form 4180 interview — your answers in that interview largely decide who gets assessed personally.

When you can handle 941 debt yourself — and when you shouldn't

A single missed quarter under $25,000, filed and caught early, is usually a DIY fix. If the business is operating, every 941 is filed, and you can commit to full payment within 24 months, you can request the IBTF-Express agreement yourself and pair it with a penalty relief request — no professional required. The same is true if the balance is small enough to simply pay within 180 days: a short-term arrangement costs nothing to set up and ends the notice stream.

Experienced help genuinely changes outcomes in five situations: a revenue officer has been assigned or has visited; a Form 4180 interview is scheduled for you or anyone on your team; you're more than three or four quarters behind (the pyramiding zone); the business is closing or already closed with debt outstanding; or the balance is large enough that the resolution requires Form 433-B financials and negotiation. In those cases, the sequencing — which returns to file first, which assets to apply where, who speaks to the RO and who doesn't — routinely changes both the dollar outcome and who ends up personally liable.

If any of those flags fit your situation — an RO on the case, a 4180 interview on the calendar, multiple quarters compounding — have your 941 file reviewed by an experienced tax professional before your next IRS contact: call (888) 825-7779 or use the 2-minute form.

Terms on your notice, decoded

- Trust fund taxes — the income tax and employee-share FICA withheld from paychecks; legally the government's money, held by your business in trust until deposited.

- Trust Fund Recovery Penalty (TFRP) — the IRC §6672 assessment that makes responsible individuals personally liable for 100% of the unpaid trust fund portion.

- Responsible person — anyone with the authority to decide which bills got paid; ownership isn't required and titles don't control.

- Willfulness — paying any other creditor while knowing withholding was unpaid; bad intent is not required.

- Federal tax deposit (FTD) — the electronic payroll tax payment due on a monthly or semiweekly schedule, well before the quarterly 941 is even filed.

- Pyramiding — accruing new unpaid payroll tax quarter after quarter while old quarters sit unpaid; the pattern the IRS treats most severely.

941 back taxes: your questions, answered

Can the IRS come after me personally for my business's 941 back taxes?

Yes — through the Trust Fund Recovery Penalty, the IRS can assess the withheld portion of 941 debt against any "responsible person" who willfully failed to pay it over. That includes owners, officers, and sometimes bookkeepers or check-signers. The corporate or LLC shield does not stop it, and the IRS can assess more than one person for the same debt at the same time.

Can 941 back taxes be discharged in bankruptcy?

The trust fund portion — the money withheld from employee paychecks — is a priority claim and is not dischargeable in Chapter 7 or Chapter 13. A Chapter 13 plan can force the IRS to accept structured repayment of it over three to five years, which is sometimes useful, but the debt itself survives. The employer-share portion and some penalties are treated differently depending on the debt's age and your filing history.

What happens to 941 back taxes if I close the business?

The liability doesn't vanish, and the trust fund portion follows the responsible people personally through the Trust Fund Recovery Penalty. Closing can actually accelerate the TFRP investigation, because the IRS knows the business itself will never pay. If you're considering shutting down, the order in which you wind things up matters — remaining assets should be applied strategically before dissolution.

Can I get a payment plan for 941 back taxes?

Yes. An operating business owing $25,000 or less can use the In-Business Trust Fund Express installment agreement, which requires full payment within 24 months and skips the detailed financial disclosure. Balances between $10,000 and $25,000 must be paid by direct debit. Above $25,000, expect to complete Form 433-B and negotiate terms, often directly with a revenue officer.

Can I settle 941 back taxes with an Offer in Compromise?

It's possible but genuinely rare for an operating business. The IRS accepted roughly 1 in 5 offers overall in FY2024, and payroll-tax offers face stricter scrutiny: you must be current on all federal tax deposits for recent quarters before the IRS will even process one. Most businesses resolve 941 debt through installment agreements and penalty relief instead.

Is owing 941 taxes a crime?

Falling behind by itself is a civil matter, not a criminal one. The line moves when a business keeps withholding from paychecks quarter after quarter while never depositing it — what the IRS calls pyramiding — or when withheld money is diverted to personal use. Stopping the pattern now and getting current on the present quarter is the strongest thing you can do.

How long can the IRS collect 941 back taxes?

Generally 10 years from the date each quarter's tax was assessed, and a Trust Fund Recovery Penalty assessed against you personally starts its own separate 10-year clock from its own assessment date. Certain events — an offer in compromise, bankruptcy, a collection appeal — pause the clock, so the real end date is often later than the simple math suggests.

What's the difference between 941 and 940 back taxes?

Form 941 covers the quarterly withholding and FICA taxes on employee wages; Form 940 covers annual federal unemployment (FUTA) tax, which is paid entirely by the employer. Only 941 debt carries a trust fund portion, which is why it triggers personal liability while 940 debt generally stays with the business.

Will a revenue officer show up at my business over 941 back taxes?

It's common — payroll tax cases are assigned to field revenue officers faster and at lower dollar amounts than personal income tax debt. An RO can appear unannounced, will typically demand current-quarter compliance and missing returns immediately, and usually opens the Trust Fund Recovery Penalty investigation. You have the right to representation and don't have to answer interview questions on the spot.

Your next 24 hours

- Find your quarters and your split. Pull the most recent IRS notice (or the business's account transcripts) and write down each quarter assessed, its balance, and — from your filed 941s — how much of it is withheld employee money versus employer match. That trust fund number is your personal exposure.

- Gather the working file. Copies of every filed 941 (and a list of unfiled quarters), your payroll reports for the affected periods, the last three months of business bank statements, and any IRS letters — especially anything mentioning Form 4180 or Letter 1153.

- Get the free case review. Deposit penalties and interest compound every month you wait, and the trust fund investigation only moves in one direction. Call (888) 825-7779 or use the 2-minute form — an experienced tax professional will map your quarters, your personal exposure, and the agreement that fits before the IRS chooses one for you.

Primary sources: the IRS's official pages for Form 941, Employer's Quarterly Federal Tax Return and IRS payment plans and installment agreements. If collection action is causing your business immediate economic harm and you can't get traction with the IRS, the independent Taxpayer Advocate Service can intervene.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.