Payroll & Business Taxes

941 vs 940 Back Taxes: FUTA vs FICA and Withholding Explained (2025)

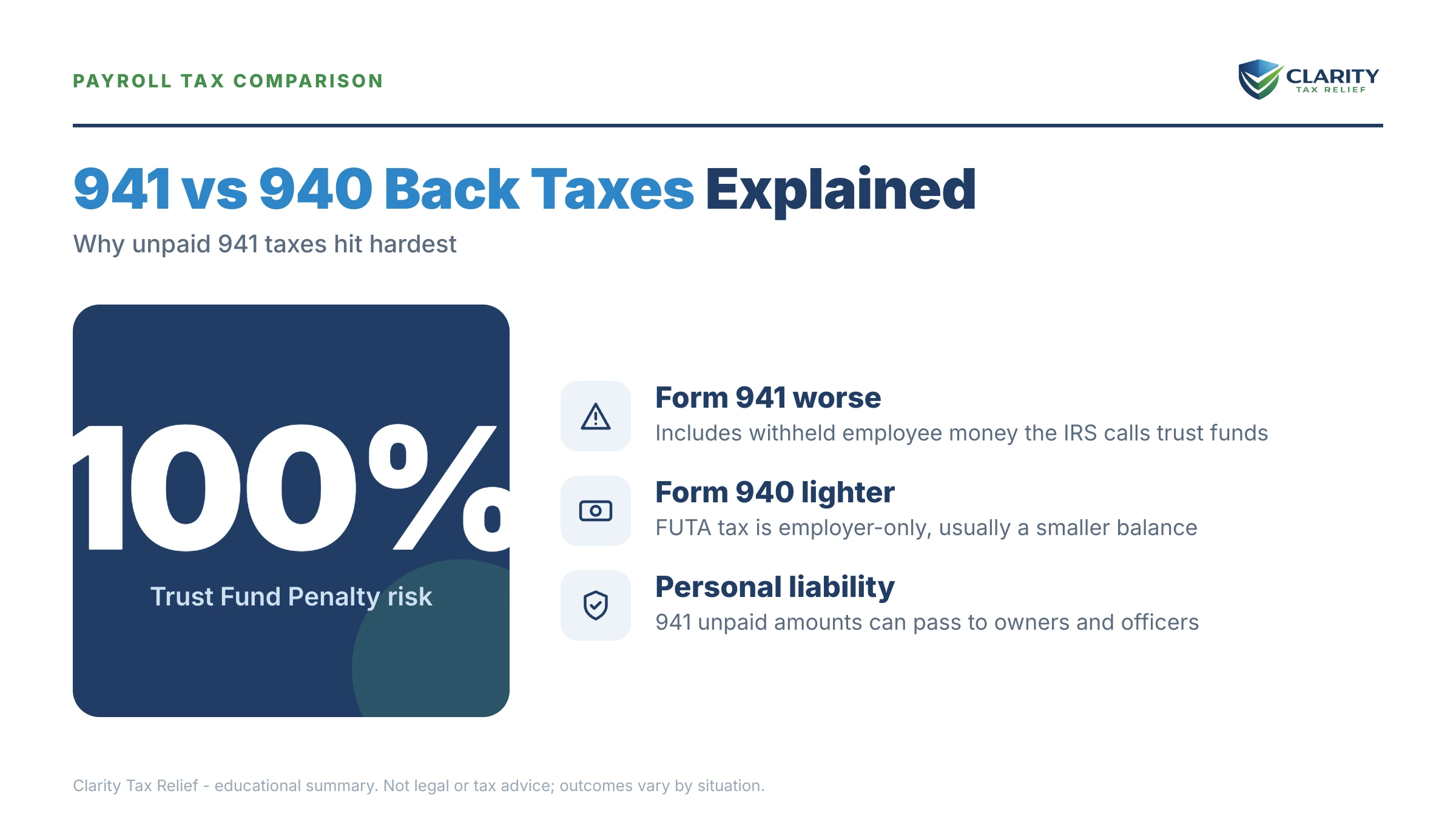

The short answer: when you're behind on 941 vs 940 back taxes, the difference matters a lot. Form 941 is your quarterly payroll tax — income tax withheld plus Social Security and Medicare (FICA). Form 940 is the annual federal unemployment tax (FUTA) the employer pays alone. Unpaid 941 taxes are far more dangerous because they include "trust fund" money the IRS can collect from you personally.

Behind on 941 or 940 — and not sure how exposed you are?

Send us your notices. An experienced tax professional will show you exactly how much of your balance is trust fund tax, whether the personal penalty is on the table, and what your real options are — free, confidential, no pressure.

⏱ Why timing matters: Form 941 is due the last day of the month after each quarter; Form 940 is due January 31 each year. Once payroll tax debt is referred to a revenue officer, things move quickly — and the Trust Fund Recovery Penalty can be assessed against you personally. If a Letter 1153 arrives, you have just 60 days to respond.

What each form actually covers

Both forms are payroll taxes, but they're not the same tax — and the IRS treats them very differently.

Form 941 — the quarterly return. This reports three things: the federal income tax you withheld from your employees' paychecks, the employees' share of Social Security and Medicare, and the employer's matching share of Social Security and Medicare. Together, Social Security and Medicare are called FICA (Federal Insurance Contributions Act). You file Form 941 four times a year. The IRS explains it on the About Form 941 page.

Form 940 — the annual return. This reports FUTA (Federal Unemployment Tax Act) tax. FUTA funds the unemployment benefits system. It is paid entirely by the employer — you never withhold it from a worker's paycheck. The standard FUTA rate applies to the first $7,000 of each employee's wages, and most employers get a large credit for state unemployment taxes paid, which drops the effective rate sharply. See the IRS About Form 940 page for the current figures.

The plain takeaway: 941 moves a lot more money and is reported four times a year. 940 is a smaller, once-a-year tax that's purely the employer's own expense.

Why 941 back taxes are so much riskier

Here's the heart of the 941 vs 940 difference. Part of what you report on Form 941 is money that was never yours. When you withhold income tax and the employee's FICA from a paycheck, you're holding that money in trust for the federal government. That's why it's called the trust fund portion of payroll tax.

The IRS views unpaid trust fund taxes very harshly — essentially as spending money that belonged to your employees and the government. Because of that, the IRS can reach past the business and assess the Trust Fund Recovery Penalty against any "responsible person" personally. That can include the owner, an officer, a partner, a bookkeeper — anyone with authority over which bills get paid. A corporation or LLC does not shield you from it. The IRS describes this on its Trust Fund Recovery Penalty page.

FUTA on Form 940 has no trust fund piece. It's the employer's own tax, so there's no equivalent personal penalty. If the business closes owing 940 taxes, that liability generally stays with the business.

A worked example: how a 941 balance splits

Say a quarter of payroll produced this on Form 941:

- Federal income tax withheld: $8,000 (trust fund)

- Employee share of Social Security & Medicare: $6,000 (trust fund)

- Employer matching share of Social Security & Medicare: $6,000 (employer tax)

Total unpaid: $20,000. Of that, $14,000 is trust fund tax the IRS can pursue from you personally. The remaining $6,000 — the employer match — stays a business debt. Knowing that split is exactly how an experienced tax professional builds a plan: protect you from personal exposure first, then resolve the rest.

What happens if you ignore payroll back taxes

Payroll tax debt escalates faster than personal income tax debt, and the IRS assigns these cases to field collection sooner. A typical path:

- Balance-due notices — the IRS bills the business for the unpaid 941 or 940 plus penalties and interest. Failure-to-pay penalties run 0.5% per month, and missed deposits carry their own steep penalties.

- Revenue officer assignment — payroll cases are often handed to a local revenue officer who may visit your business in person. This is far more aggressive than automated collection.

- Letter 1153 / Form 2751 — the IRS proposes the Trust Fund Recovery Penalty against you personally. You have 60 days to appeal.

- Liens and levies — the IRS can file a federal tax lien and levy business bank accounts or receivables. In serious, ongoing cases it can move to shut the business down.

The longer payroll taxes go unpaid while you keep running payroll, the worse the IRS treats it — because each new pay period creates new trust fund money. Acting early is everything here.

How to fix 941 and 940 back taxes, step by step

- File every missing return first. If the IRS hasn't received your 941s or 940, it may estimate the balance higher than reality. Filing the actual returns stops the guessing and locks in the real numbers.

- Get current going forward. The IRS will not approve a payment plan while you're still falling behind. Make your current payroll deposits on time — this is non-negotiable in any resolution.

- Separate the trust fund from the rest. Identify how much of the 941 balance is trust fund tax versus employer tax. This drives every decision about personal exposure.

- Request a payment arrangement. A business can set up an installment agreement for payroll tax debt. Larger balances usually require financial disclosure.

- Pursue penalty relief. First-time penalty abatement or reasonable-cause relief may remove some penalties if you qualify.

- Get representation before a revenue officer is assigned. Because 941 debt carries personal liability, this is not a do-it-yourself situation for most owners. Our full guide to 941 back taxes for a business walks through what to expect next.

Be wary of anyone promising to settle your payroll debt for "pennies on the dollar" before reviewing your finances — that's a sales pitch, not a strategy. Trust fund taxes in particular are very hard to settle, and honest help starts with the math.

941 vs 940 back taxes, answered

What is the difference between Form 941 and Form 940?

Form 941 is the quarterly payroll tax return that reports federal income tax withheld from employees plus both halves of Social Security and Medicare (FICA). Form 940 is the annual return that reports federal unemployment tax (FUTA), which the employer pays alone. 941 covers far more money and is reported four times a year; 940 is filed once a year.

Is owing 941 back taxes worse than owing 940?

Yes. Form 941 includes trust fund taxes — money withheld from employees' paychecks that the business held in trust for the government. The IRS treats unpaid trust fund taxes as theft and can assess the Trust Fund Recovery Penalty against owners and officers personally. FUTA on Form 940 is the employer's own tax, so it carries no trust fund piece and far less personal exposure.

What are trust fund taxes on Form 941?

Trust fund taxes are the federal income tax and the employee's share of Social Security and Medicare that you withhold from each paycheck. That money never belonged to the business — you hold it in trust and forward it to the IRS. When it isn't paid, the IRS can pursue the responsible person individually through the Trust Fund Recovery Penalty.

Can the IRS come after me personally for payroll back taxes?

For the trust fund portion of Form 941, yes. Owners, officers, bookkeepers, or anyone with authority over which bills get paid can be held personally liable through the Trust Fund Recovery Penalty, even if the business is a corporation or LLC. The FUTA tax on Form 940 stays a business liability and is not subject to that personal penalty.

How do I fix 941 and 940 back taxes?

File any missing returns first so the IRS stops estimating your balance, then address payment. A business can request an installment agreement, and penalty relief like first-time abatement may reduce what's owed. Because 941 debt carries personal exposure, the smartest first step is a review with an experienced tax professional before a revenue officer is assigned.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.