Payroll & Business Taxes

Am I Personally Liable for Payroll Taxes? Owner, Officer, Bookkeeper & Check-Signer Liability (2025)

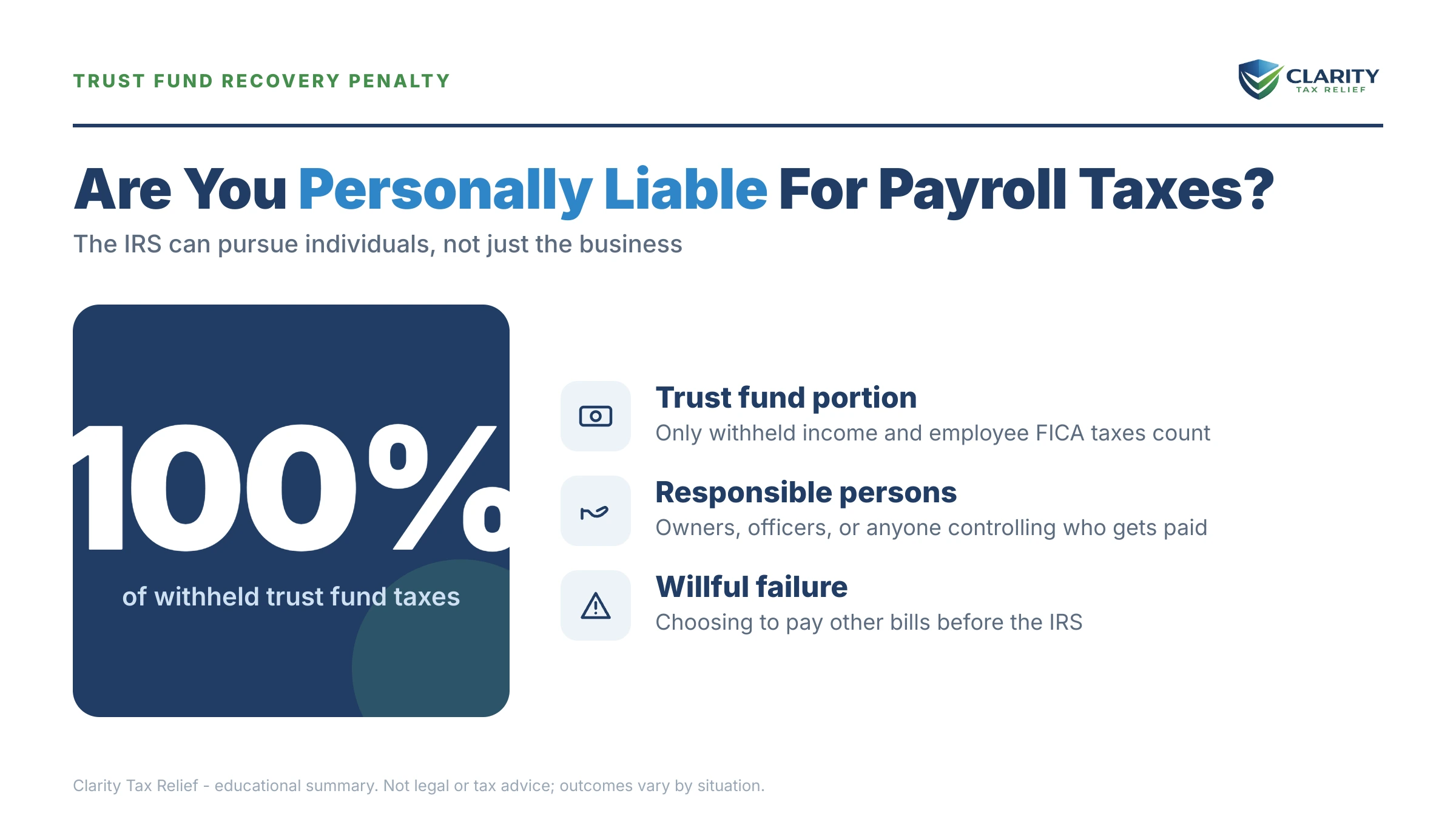

The short answer: yes — you can be personally liable for payroll taxes even if the business is a corporation or LLC. Through the Trust Fund Recovery Penalty (TFRP), the IRS can collect the withheld "trust fund" taxes from any "responsible person" — an owner, officer, bookkeeper, or check-signer — who willfully failed to pay them over.

Named on a payroll tax case?

Send us the IRS letter and your title. An experienced tax professional will tell you, honestly, whether the IRS can hold you personally liable — and how to push back — free, confidential, no pressure.

⏱ Your deadline: if you've received IRS Letter 1153, you generally have 60 days from the date on the letter to file a written appeal before the penalty is assessed against you personally. After that window closes, the IRS can record liens and start levies on your own income and accounts.

Why payroll taxes become a personal debt

When a business pays wages, it holds back part of every paycheck — federal income tax plus the employee's share of Social Security and Medicare. That money never belonged to the business. It's held "in trust" for the employees and the government, which is why it's called the trust fund portion. The employer is just supposed to forward it on the Form 941 (Employer's Quarterly Federal Tax Return).

When cash gets tight, owners sometimes use that withheld money to make rent, payroll, or a vendor payment — promising themselves they'll catch up with the IRS later. The IRS treats this very differently from normal back taxes. In its eyes, you spent money that was never yours. That's why the law lets the IRS reach past the business and collect from people personally. The corporate shield that protects you from ordinary business debts does not protect you here.

The Trust Fund Recovery Penalty, explained

The tool the IRS uses is the Trust Fund Recovery Penalty, or TFRP. Despite the name, it isn't an add-on penalty — it's a way of transferring the trust fund tax itself onto individuals. It equals 100% of the trust fund amount. The IRS explains the basics on its own Trust Fund Recovery Penalty page.

To assess the TFRP against you, the IRS has to show two things:

- You were a "responsible person." That means you had the authority to decide which bills got paid — to sign checks, control bank accounts, hire and fire, or direct the company's finances.

- You acted "willfully." This is a lower bar than it sounds. Willful just means you knew the taxes were due and chose to pay someone else first — a landlord, a supplier, even other employees — instead of the IRS. No bad intent is required.

Both pieces have to be true. A title alone doesn't make you liable, and a low-level employee who just follows orders usually isn't on the hook. The fight is almost always about whether you really controlled the money.

Who the IRS goes after — and who can be cleared

The IRS casts a wide net at first, often naming several people on one business, then narrows it down. Here's how the common roles tend to play out:

- Owners & officers — the most common targets. If you owned the company or held a title like president, treasurer, or managing member and had check-signing authority, you're squarely in the IRS's sights.

- Bookkeepers & controllers — liable only if they had real authority over which creditors got paid. A bookkeeper who chose to pay vendors over the IRS can be held responsible; one who simply cut checks on the owner's instructions usually can't.

- Check-signers — signing authority is strong evidence, but it isn't automatic. The key is whether you had discretion, not just a signature card. A spouse or office manager added "for convenience" who never decided anything may be able to get cleared.

- Silent or passive owners — investors with no control over the checkbook are often able to show they weren't responsible.

Because more than one person can be held liable for the full trust fund amount, the IRS may pursue several people at once. It can't collect the same dollars twice, but it can chase each responsible person until the trust fund balance is paid.

What happens if you ignore it

Trust fund cases are usually worked by a revenue officer — a real person assigned to collect, not an automated notice mill. The sequence moves faster and hits harder than a typical balance-due case:

- Form 4180 interview — the revenue officer interviews you to decide who was responsible and willful. What you say here shapes everything that follows.

- Letter 1153 & Form 2751 — the IRS proposes the TFRP against you personally. You have 60 days to appeal.

- Assessment — if you don't respond, the penalty becomes a personal liability with your name and Social Security number on it.

- Personal collection — the IRS can then file a lien against your home, levy your personal bank accounts, and garnish your wages, just like any other individual tax debt.

One hard truth: the trust fund tax generally can't be wiped out in bankruptcy. Once it's assessed against you, it tends to stick. That's exactly why the time to act is before the assessment, not after.

A quick example of the dollars

Say a business owes $90,000 on its Form 941 accounts. Roughly $55,000 of that might be trust fund tax (the withheld income tax plus the employee share of Social Security and Medicare). The other ~$35,000 — the employer's matching share plus penalties and interest — stays with the business. The IRS can pursue that $55,000 trust fund piece against you personally through the TFRP. Knowing how the bill splits is the first step in protecting yourself.

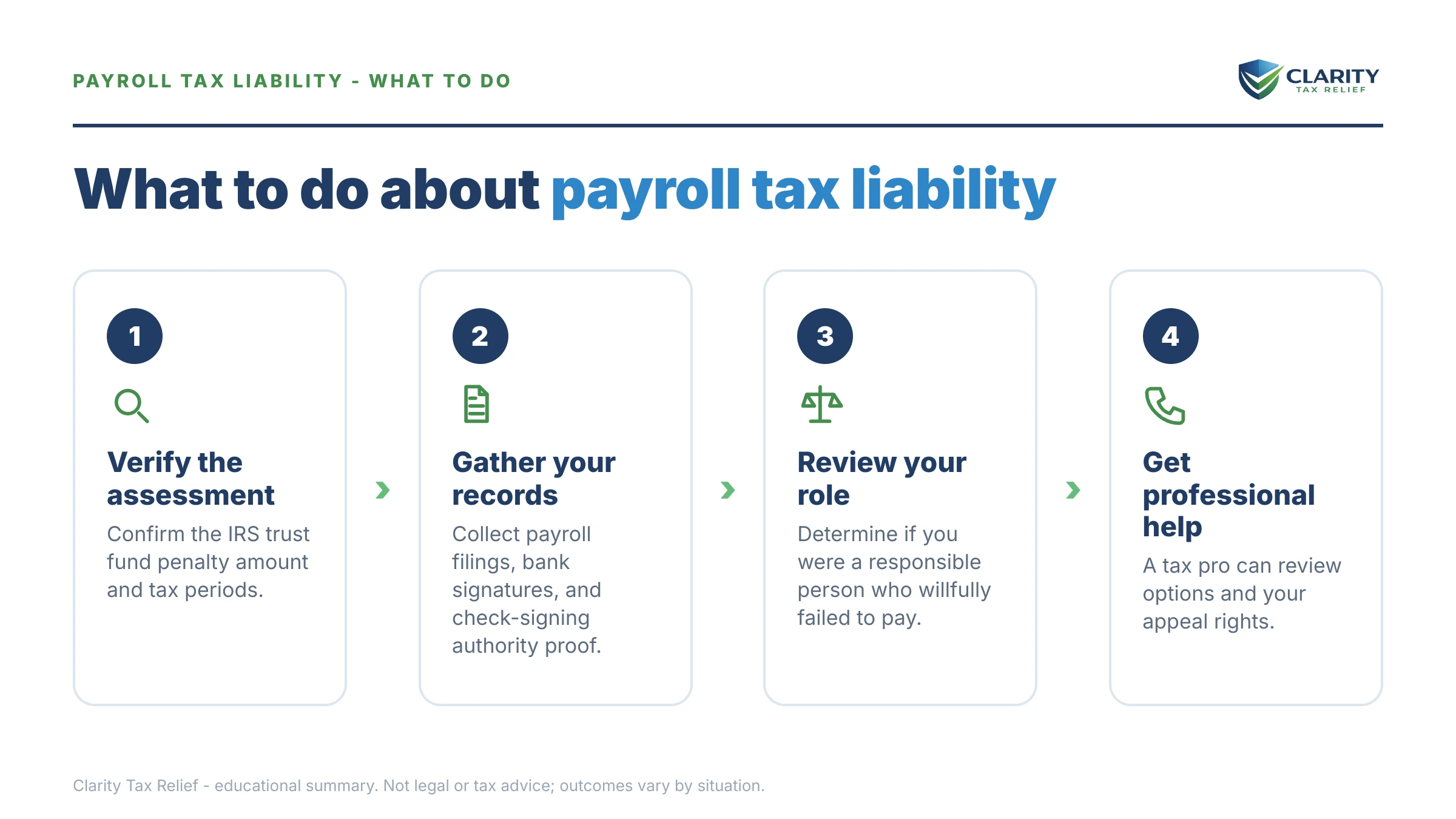

How to respond, step by step

- Don't talk to the revenue officer unprepared. The Form 4180 interview is where most liability is decided. Get representation lined up before you answer questions about who controlled the money.

- Gather proof of who really had control. Bank signature cards, corporate minutes, org charts, emails, and pay records can show you weren't the decision-maker — or that someone else was.

- If you got Letter 1153, calendar the 60 days. File a written protest with the IRS Office of Appeals to challenge responsibility or willfulness before the penalty is assessed.

- Keep the business returns current. Filing ongoing 941s and depositing current payroll taxes shows good faith and stops the hole from getting deeper. See our guide to 941 back taxes for a business that's fallen behind.

- Plan the resolution. Once liability is settled, the trust fund debt can often be folded into a payment plan, hardship status, or — depending on your finances — an offer. An experienced tax professional can map the order to fix things in.

Personal payroll tax liability, answered

Can I be personally liable for payroll taxes even though the business is an LLC or corporation?

Yes. The corporate or LLC shield does not protect you from the Trust Fund Recovery Penalty. The IRS can assess the trust fund portion of unpaid payroll taxes against you personally if you were a responsible person who willfully failed to pay it over. That liability follows you, not the business entity.

Can a bookkeeper be held personally liable for payroll taxes?

A bookkeeper can be held liable if they had authority over which bills got paid and chose to pay others instead of the IRS. Simply preparing the payroll or signing checks at someone else's direction usually is not enough. The question is whether you had real control over the money.

What is the Trust Fund Recovery Penalty?

The Trust Fund Recovery Penalty, or TFRP, lets the IRS collect the withheld income tax and the employee share of Social Security and Medicare from the individuals responsible for paying it. It is 100% of the trust fund amount and is assessed against people personally, not the business.

How much of the payroll tax debt can the IRS make me pay personally?

Only the trust fund portion — the income tax withheld plus the employee half of Social Security and Medicare. The employer's matching share and most penalties stay with the business. On a typical bill the trust fund part is often more than half of the total balance.

What happens after I get IRS Letter 1153?

Letter 1153 proposes the Trust Fund Recovery Penalty against you. You generally have 60 days to appeal in writing before the IRS makes the assessment final. Miss that window and the penalty becomes a personal debt the IRS can collect through liens, levies, and wage garnishment.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.