Dependent Disputes

Both Parents Claimed the Same Child: How the IRS Decides Who Wins (2026)

The short answer: when both parents claim the same child, the IRS doesn't split the benefits. The second e-filed return rejects automatically, both filers eventually receive letters, and if neither amends, the IRS tiebreaker rules decide the winner: the parent the child lived with for more nights — and with equal nights, the higher AGI.

The rejection landed seconds after you hit submit: your child's Social Security number has already been used on another return. You know exactly whose return that was. Your first tax season after the divorce just became a standoff — and the good news is the IRS resolves it with a fixed set of rules, not a coin flip, so you can know today whether you're likely to win.

If letters have already started arriving, the image below shows exactly what the IRS's duplicate-dependent letter looks like and where to find the information that matters on it.

⏱ The clock: there's no single statutory deadline in a dependent dispute — the date that controls is the response date printed on each IRS letter you receive, first the CP87A and later any audit letter. Miss an audit response date and your claim can be disallowed by default. And if you claimed in error, interest on the credits you'll repay accrues monthly from your return's original due date.

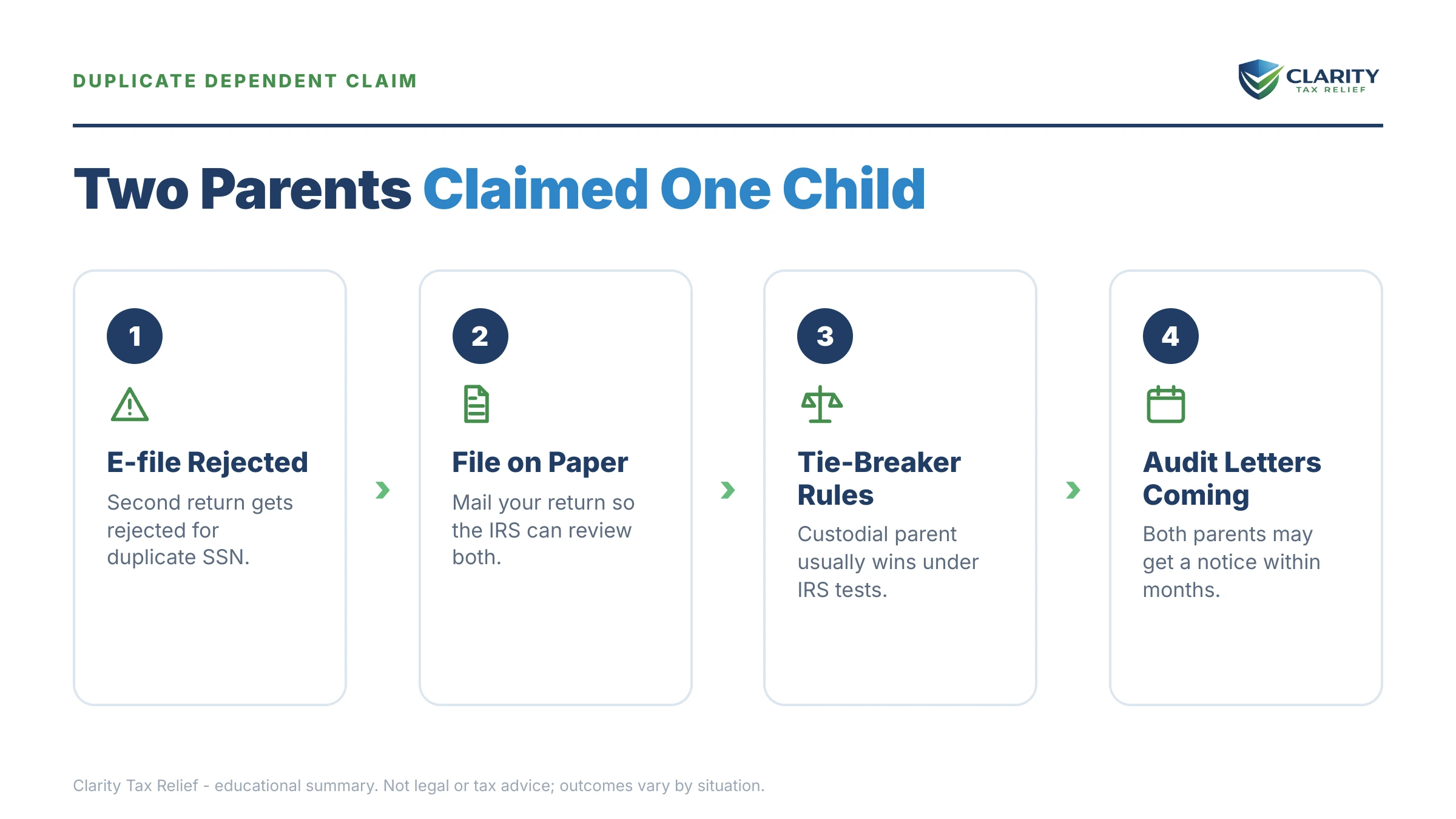

Why "both parents claimed a child" triggers an instant IRS rejection

The IRS e-file system automatically rejects any return that claims a dependent Social Security number already used on a processed return for the same year. It's a database check, not a judgment — whoever filed first got through, even if their claim is dead wrong.

That's the single most misunderstood fact in this dispute: a rejection is not a ruling. Filing first buys your ex nothing except a faster refund that may have to be paid back. If the rules favor you, you print your return, sign it, and mail it — and the IRS is required to process it.

How did this happen? In the first year or two after a divorce, it's almost always one of three things: the decree says one thing and the custody calendar says another, you agreed to alternate years and someone jumped the line, or you both honestly believe the child lived with you "most of the time." The IRS doesn't care which of those it is. It applies the same test to all of them.

How the IRS decides which parent claims a child: the tiebreaker rules

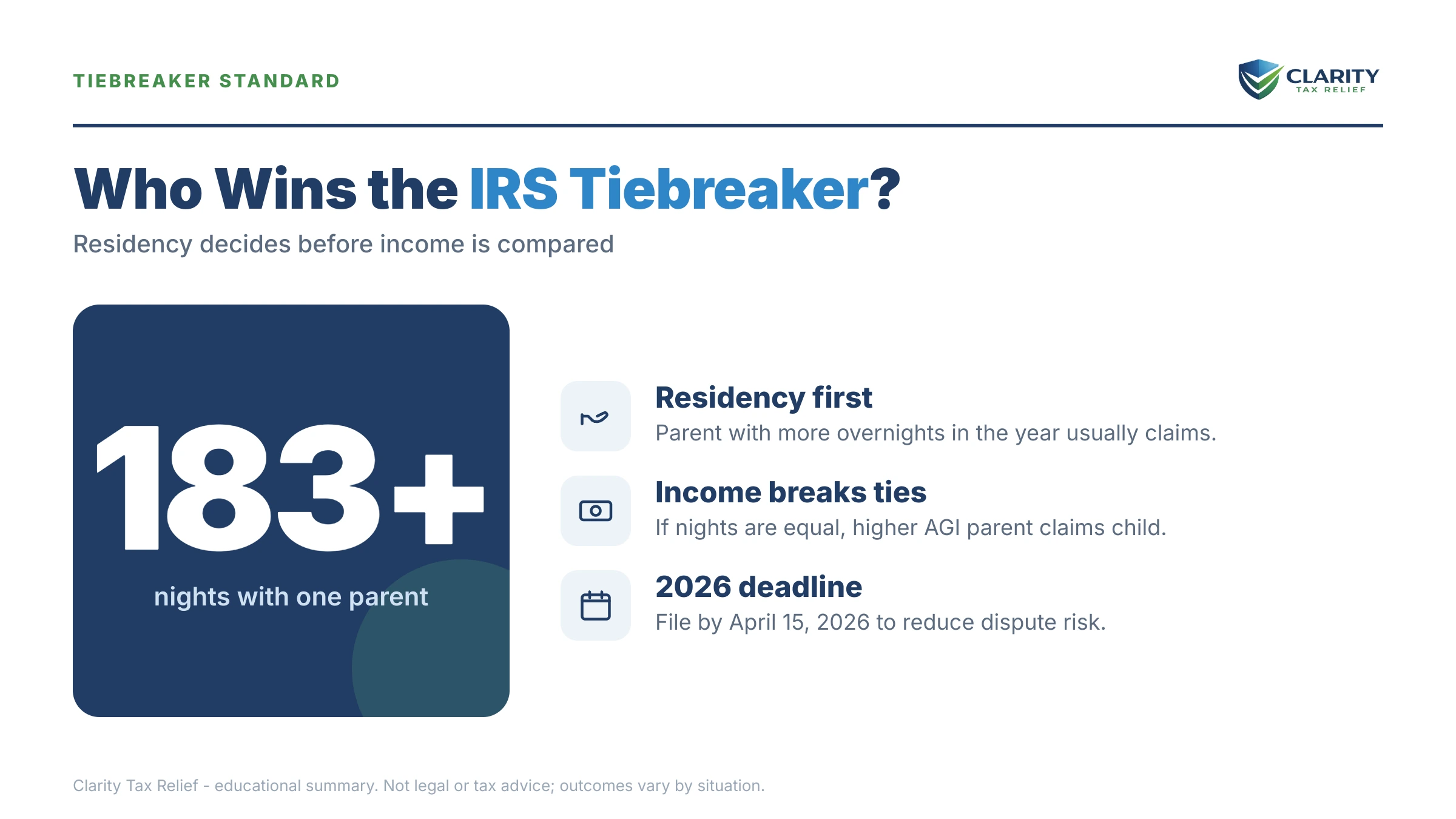

Between two parents, the parent with whom the child spent the greater number of nights during the year — in practice usually at least 183 — wins; if nights are exactly equal, the parent with the higher AGI claims the child. The parent with more nights is the "custodial parent" in IRS terms, no matter what your decree calls anyone.

Nights, not days, and not court-ordered custody percentages. If your daughter sleeps at your apartment Sunday through Thursday during the school year, you're likely custodial even if the decree says "joint custody, 50/50." If the nights come out exactly even — it happens with true week-on/week-off schedules — the parent with the higher adjusted gross income wins.

| Situation | Who gets the child |

|---|---|

| Only one claimant is the child's parent | The parent, always |

| Both parents; child spent more nights with one | The parent with more nights (the custodial parent) |

| Both parents; nights exactly equal | The parent with the higher AGI |

| Neither claimant is a parent (e.g., two grandparents) | The claimant with the highest AGI |

| A parent could claim but doesn't | A non-parent, only if their AGI is higher than that of any parent who could claim |

Your divorce decree does not override any of this. For decrees signed after 2008, the only way a noncustodial parent legitimately claims the child is with Form 8332, signed by the custodial parent. A decree that "awards" the dependency without that signed release is enforceable in family court — not at the IRS. We cover that collision in detail in divorce decree irs debt.

What happens if neither parent backs down

A duplicate dependent claim moves through a fixed, automated sequence, and every stage gets more expensive for whichever parent is wrong:

- E-file rejection. The second return is blocked electronically. No decision has been made — the paper-filing door is wide open.

- Both returns processed. The mailed return works through the system (slowly — paper processing takes months, and 2026 staffing cuts have not sped it up). Any refund on it is delayed, sometimes held while the duplicate is examined. The IRS computer now sees the same SSN on two returns.

- CP87A letters go to both filers. Each parent gets a cp87a notice saying someone else claimed the same dependent and asking each to re-check the return. Nobody is accused of anything yet — this is the cheap exit for whoever claimed in error.

- Audit. If neither parent amends, the IRS can examine one or both returns. When the earned income credit is involved, that's typically a cp75 notice demanding proof the child lived with you.

- Disallowance and repayment. The losing parent's child-related benefits are removed. That means repaying the credits with interest, a possible 20% accuracy related penalty irs, filing Form 8862 before claiming the credits again (see the cp79 notice), and — for reckless or fraudulent EITC claims — a ban of 2 or 10 years.

One more path worth naming: if the other claim wasn't your ex — if you have no idea who used your child's SSN — you're likely dealing with identity theft, not a custody fight. That's a different playbook entirely: see someone filed taxes in my name.

Both parents claimed the same child — and the letters have started?

Send us the letter and the custody picture. An experienced tax professional will tell you which parent the tiebreaker rules actually favor and exactly what to send back — free, before the response date printed on your letter passes.

Your options, by which parent you are

Every parent in this dispute is in one of four positions, and each has one correct move.

You're the custodial parent (more nights). Paper-file with the child claimed, keep the mailing receipt, and start assembling residency proof now — school and medical records dated during the tax year are gold. Our guide to eic audit proof of residency walks through exactly which documents examiners accept, and the same evidence wins a child tax credit dispute.

You're the noncustodial parent with a decree awarding you the claim. Your claim is only IRS-valid with a signed Form 8332 attached. If your ex won't sign, the IRS will side with them on residency — your leverage is a contempt motion in family court, not a standoff with the IRS. Claiming without the release usually ends in repayment.

You claimed in error. File Form 1040-X now, before an audit opens. Amending voluntarily means you repay the credits plus interest but usually avoid the 20% penalty, the audit, and any EITC ban. Waiting for the IRS to disallow you costs strictly more.

You're negotiating a split. The tax code allows a clean division — but only one specific one, shown below. The most common divorced-parent mistake is assuming Form 8332 hands over everything. It doesn't.

| Tax benefit | Custodial parent | Noncustodial parent with signed Form 8332 |

|---|---|---|

| Child tax credit / credit for other dependents | Yes, unless released | Yes — this is what Form 8332 transfers |

| Earned income tax credit (EITC) | Yes, if income-eligible | Never — cannot be transferred |

| Head of household filing status | Yes, if other tests are met | Never, based on this child |

| Child and dependent care credit | Yes | Never — cannot be transferred |

That split is why alternating years works better on paper than in practice: even in "your ex's year," you may still be entitled to head of household and EITC if the child sleeps at your home most nights. Two parents can legitimately get child-related benefits from the same child in the same year — just never the same benefit.

What losing the claim costs: a worked example at $68,500

Losing a dependent dispute means repaying every child-linked benefit on the return, with interest, and sometimes a penalty on top. Here's the math — hypothetical, but realistic for a recently divorced filer.

Say you divorced last year, earned $68,500, and filed head of household claiming your daughter and the child tax credit. Your ex claimed her too — and when you count the school-year calendar honestly, the nights favor your ex. At $68,500 as a single filer you're above the EITC income limits, so EITC isn't in play; the fight is over the child tax credit and your filing status.

| Item | Approximate cost |

|---|---|

| Child tax credit repaid | Up to $2,200 |

| Extra tax: single vs. head of household (smaller standard deduction, narrower brackets) | Roughly $1,600 |

| 20% accuracy-related penalty, if asserted (20% × $3,800) | About $760 |

| Interest, accruing monthly from the original due date | Grows until paid |

| Rough total | About $4,560 plus interest |

For a lower-income parent whose return included EITC, the repayment can more than double — and a reckless EITC claim adds a 2-year ban on the credit. You can estimate your own penalty and interest exposure with our Penalty & Interest Calculator.

If the repayment lands as a bill you can't write a check for, it's handled like any IRS balance — payment plans, hardship status, and the rest are laid out in how to settle tax debt yourself, and the cheapest routes are compared in best way to pay the irs. One honest note: penalties can sometimes be removed, but interest almost never comes off — see can irs interest be waived.

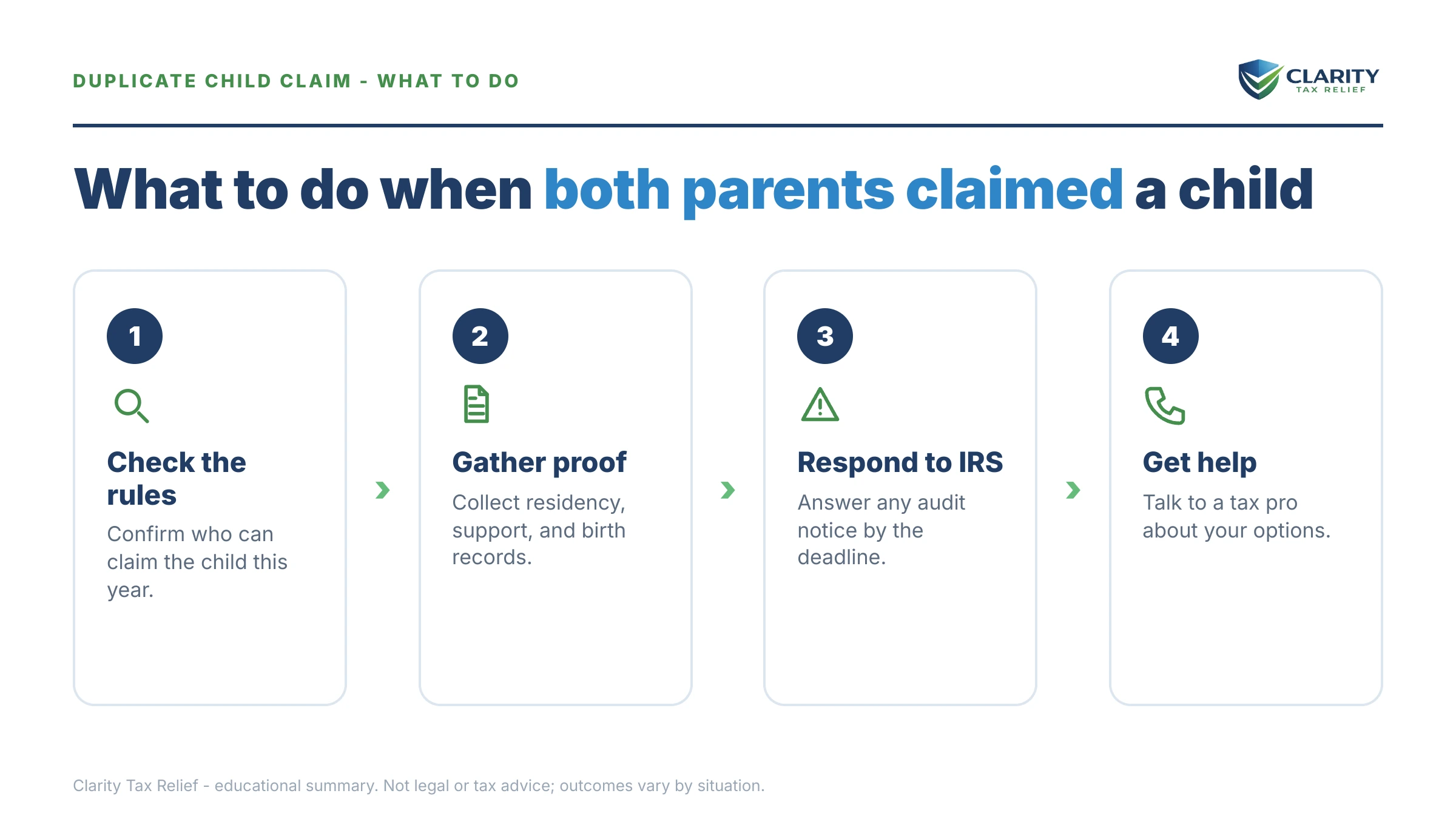

How to respond, step by step

- Count the nights. Work out which parent the child spent more nights with during the tax year. That single number — in practice usually at least 183 — decides most disputes before the IRS ever weighs in.

- Paper-file if the rules favor you. An e-file rejection isn't a ruling. Print your return claiming the child, sign it, and mail it; the IRS will process it and start its duplicate-claim procedure.

- Gather residency proof. Collect school enrollment records, pediatrician and dental records, daycare records, and a lease or mortgage statement showing the child's address matches yours.

- Respond to every IRS letter by its printed date. Silence is how valid claims get disallowed. Answer the CP87A if you claimed in error, and answer any audit letter with documents if you were right.

- Amend with Form 1040-X if the rules favor your ex. Repaying voluntarily costs far less than losing an audit — you avoid the 20% accuracy-related penalty and protect your ability to claim the credits in future years.

When you can handle this yourself

Most parents on the right side of the tiebreaker rules can win this without paying anyone. If your child is enrolled in school at your address, the pediatrician's file shows your address, and you're disputing a single tax year, you can paper-file, respond to the letters yourself, and prevail — patiently, because paper takes months.

Experienced help changes the outcome in a narrower set of situations: the nights are genuinely close to 50/50 and the case turns on how the calendar is documented, multiple years are in dispute at once, the IRS has proposed an EITC ban, you're a noncustodial parent whose only support is decree language without a Form 8332, or the repayment is a balance you can't pay. And if the IRS disallowed a claim you can clearly prove and normal channels have stalled, the Taxpayer Advocate Service exists for exactly that.

One fear worth retiring: a good-faith dependent dispute is a civil matter, full stop. The line between owing money and criminal exposure is explained in can you go to jail for owing irs — and an honest disagreement over custody nights is nowhere near it.

Terms on your IRS letters, decoded

These are the terms this dispute turns on, in plain English:

- Custodial parent — the parent the child spent more nights with during the tax year (in practice usually at least 183), regardless of what the decree says.

- Qualifying child — the IRS's four-part test (relationship, age, residency, support) that determines who may claim child-related benefits at all.

- Tiebreaker rules — the fixed order the IRS applies when two people claim the same child; between parents, nights first, then AGI.

- Form 8332 — the signed release a custodial parent gives the noncustodial parent, transferring only the child tax credit and credit for other dependents (official page: About Form 8332).

- CP87A — the "someone else claimed your dependent" letter both filers receive (the IRS explainer is at Understanding your CP87A notice).

- Form 8862 — the form you must file to claim EITC or the child tax credit again after a disallowance.

- Accuracy-related penalty — a penalty of 20% of the understated tax when a wrong claim is due to negligence.

Both-parents-claimed-a-child questions, answered

What happens if both parents claim the same child on their taxes?

Neither parent's claim is automatically accepted — the second return to arrive rejects at e-file, and the IRS eventually mails CP87A letters to both filers. If neither parent amends, the IRS can audit both returns and apply its tiebreaker rules: the parent with more nights of residence wins, and with equal nights, the higher adjusted gross income wins. The losing parent repays every child-related benefit with interest.

How does the IRS decide which parent gets to claim a child?

The IRS uses the tiebreaker rules in the tax code, not your divorce paperwork. Between two parents, the child goes to the parent the child lived with for the greater number of nights during the tax year — in practice usually at least 183. If the nights are exactly equal, the parent with the higher adjusted gross income wins. A non-parent can only beat a parent in narrow, higher-AGI situations.

Does my divorce decree decide who claims our child?

Not by itself. For divorce decrees signed after 2008, the IRS requires Form 8332 — a release signed by the custodial parent — before a noncustodial parent can claim the child. If your ex violates the decree, your remedy is state family court (contempt), not the IRS; the IRS applies its own residency-based rules regardless of what the decree says.

What proof does the IRS accept that my child lived with me?

The IRS wants third-party records tying the child to your address for more than half the year: school enrollment records and report cards, pediatrician and dental records, daycare records, and a lease or mortgage statement listing the child. Your own calendar helps but rarely wins alone. Letters on official letterhead from a school or doctor confirming the child's address carry the most weight in an audit.

What is a CP87A notice and do I have to respond?

A CP87A tells you someone else claimed a dependent with the same Social Security number and asks you to double-check your return. You don't have to reply if your claim is correct — but if you claimed the child in error, you should file Form 1040-X promptly, because amending voluntarily avoids the audit, the 20% accuracy-related penalty, and the possible EITC ban that can follow a disallowance.

Can you go to jail for wrongly claiming a child on taxes?

Almost never for an honest dispute between parents. Duplicate dependent claims are handled civilly — repayment, interest, penalties, and credit bans — not criminally. Criminal exposure requires willful fraud, such as claiming children who don't exist or fabricating residency documents. If you're worried about the line between owing and crime, see our guide on whether you can go to jail for owing the IRS.

My e-file was rejected because my ex already claimed our child — what do I do?

Don't drop the claim just because the software rejected it — a rejection means the Social Security number was already used, not that the other claim was valid. If the tiebreaker rules favor you, print and mail your return claiming the child. The IRS will process it, pay any refund you're due more slowly, and then send both filers letters to sort out who was entitled.

If I sign Form 8332, can I still file as head of household?

Yes, if the child lived with you more than half the year. Form 8332 releases only the child tax credit and the credit for other dependents to the noncustodial parent. Head of household status, the earned income tax credit, and the child and dependent care credit stay with you as the custodial parent — they can never be transferred, no matter what a decree says.

Your next 24 hours

- Find the paperwork that starts the clock. Pull up your e-file rejection notice, or any IRS letter that has arrived, and write down the response date printed on it.

- Gather the nights evidence. School enrollment records, pediatrician and dental records, your lease or mortgage statement showing your child's address, and last year's return.

- Get a free case review. Call (888) 825-7779 or use the 2-minute form at the top of this page. Whether the rules favor you or your ex, acting before your letter's response date is what keeps this a paperwork problem — and if credits have to go back, interest on them is accruing monthly either way.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.