IRS Notices

IRS CP79 Notice: EITC Disallowed and Why You Must File Form 8862 (2025)

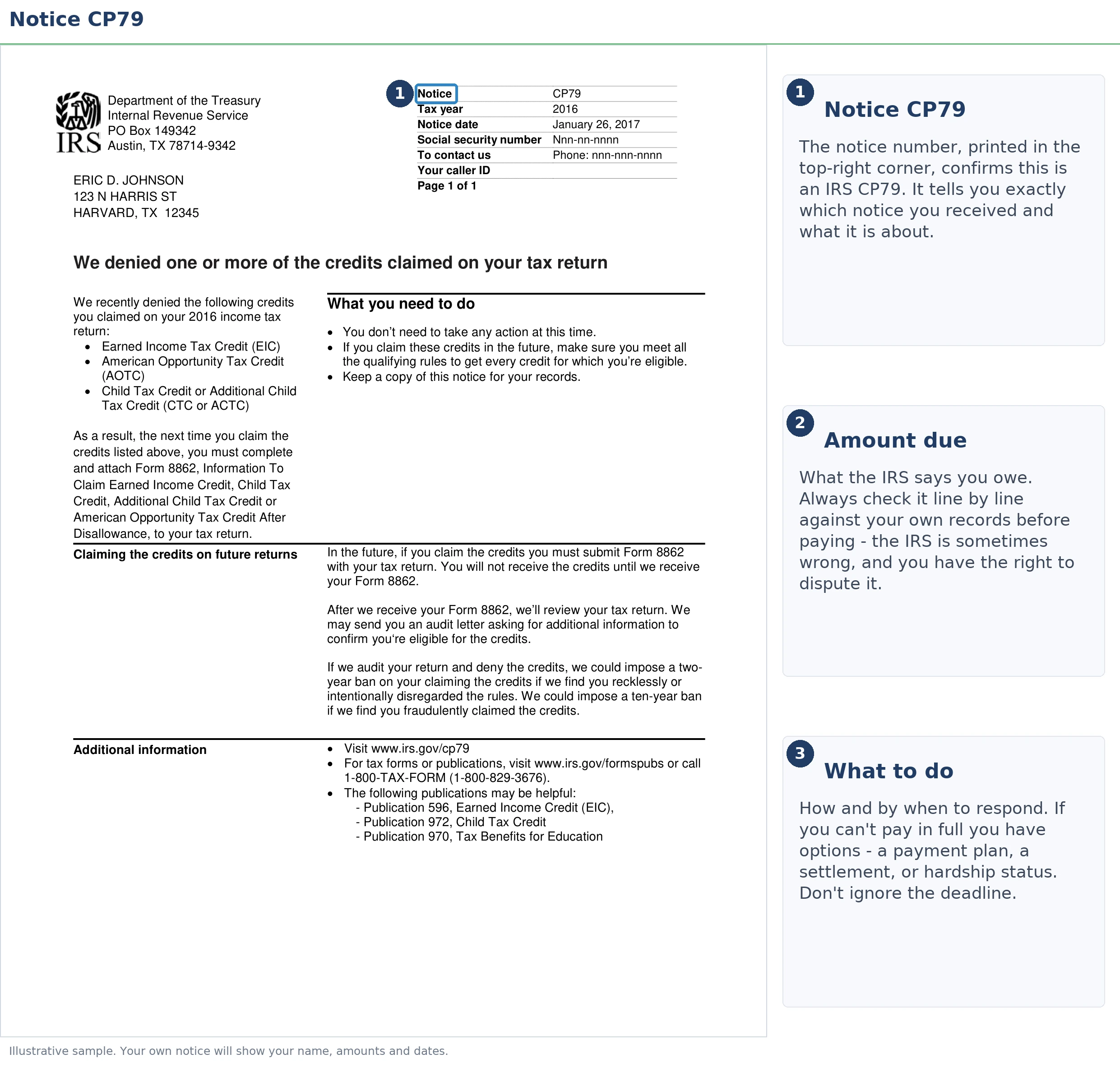

The short answer: a CP79 notice means the IRS disallowed a credit — most often the Earned Income Tax Credit (EITC) — on a past return. It is not a bill by itself. To claim that credit again in any future year, you must attach Form 8862 to your return. Without it, the IRS will automatically reject the credit.

Not sure which CP79 you got — or whether the credit was even disallowed correctly?

Send us a photo of your notice. An experienced tax professional will read it line by line, tell you whether a ban applies, and map out the Form 8862 steps — free, confidential, no pressure.

⏱ Your timeline: there's no single "pay by" date on a CP79. The thing to track is your next tax return — that's when Form 8862 must be attached. If a separate bill (like a CP14) also arrived for the disallowed year, that notice carries its own deadline, usually 21 days from its notice date.

Why you got a CP79 notice

The IRS reviewed a return where you claimed a refundable credit and decided you didn't qualify for all or part of it. The CP79 notice tells you the credit was disallowed and sets a rule for the future: the next time you claim it, you have to prove eligibility on Form 8862. The credit involved is usually the Earned Income Tax Credit, but a CP79 can also cover the Child Tax Credit (CTC), Additional Child Tax Credit, Credit for Other Dependents, or the American Opportunity Tax Credit (AOTC).

Common reasons the IRS disallows the EITC include a qualifying child who didn't meet the residency or relationship tests, income that fell outside the limits, a Social Security number issue, or the same child being claimed by two people. You can read the IRS's own explainer at Understanding your CP79 notice, and the eligibility rules at the IRS Earned Income Tax Credit page.

Important: a CP79 is not the same as a debt notice. It's a record on your account that changes how a future credit is processed.

CP79 vs. CP79A: read which one you got

There are two versions, and the difference matters:

- CP79 — your credit was disallowed. No ban. You simply file Form 8862 the next time you claim that credit.

- CP79A — your credit was disallowed because the IRS found you claimed it through reckless or intentional disregard of the rules. This usually triggers a 2-year ban on the credit. After the ban ends, you still have to file Form 8862 to claim it again.

One more rule worth knowing: if the IRS determined the claim was fraudulent, the ban can stretch to 10 years. Most people who receive a CP79 are not in that category — but check the wording on your notice so you know which rule applies to you.

What happens if you ignore it

A CP79 won't send a levy or garnishment after you — it isn't a collection notice. But ignoring it costs you money in a quieter way:

- You lose the credit next year. File a return claiming the EITC without Form 8862, and the IRS will automatically strip the credit back out — even if you fully qualify.

- Your refund shrinks or disappears. The EITC is often the largest part of a refund. Losing it can turn a big refund into a small one, or a refund into a balance due.

- The disallowance stays on your account. It doesn't expire on its own. Until you file Form 8862 (or get the disallowance corrected), the block on the credit follows you year to year.

- If a balance was created for the disallowed year, that flows into the normal collection sequence — CP14 first, then reminder and levy notices — with penalties and interest growing monthly.

What Form 8862 is and how it works

Form 8862, "Information To Claim Certain Credits After Disallowance," is the IRS's way of asking you to re-prove eligibility for a credit that was taken away. You attach it to the tax return for the first year you claim the credit again. The form asks about your qualifying children, residency, income, and filing status — the same facts the IRS questioned the first time. You can find it and its instructions at About Form 8862 on IRS.gov.

You only need to file it once after a disallowance, not every year — unless the credit is disallowed again later. If you e-file, most tax software walks you through Form 8862 when you indicate the credit was previously disallowed. If you mail your return, it has to be physically attached.

What if the CP79 is wrong?

Sometimes the disallowance is a mistake. Maybe your child really did live with you more than half the year, or two people claimed the same child and you're the parent with the stronger claim. If that's your situation, you have ways to push back:

- Respond with documents. School records, medical records, or a landlord letter can prove a child lived with you. Our guide on proving residency and relationship in an EIC audit walks through exactly what the IRS accepts.

- Sort out a duplicate claim. If the issue is that both parents claimed the same child, the tie-breaker rules decide who wins — and the other person may need to amend.

- Request audit reconsideration if the credit was disallowed through an exam and you have records you didn't get to submit. Our CP75 EIC audit guide explains how that review process works.

Don't just let an incorrect disallowance sit. It keeps blocking the credit until it's fixed.

How to respond to a CP79, step by step

- Read which notice you got. Plain CP79 means no ban. CP79A usually means a 2-year ban. Note the credit and tax year listed.

- Check whether a balance was created. Log into your IRS online account and look at the disallowed year. If there's a balance due, a separate notice with its own deadline is coming or already arrived.

- Decide if the disallowance is correct. If it is, do nothing for now — just remember to file Form 8862 next year. If it's wrong, gather your documents and respond.

- File Form 8862 with your next return for the first year you claim the credit again. E-file software handles it automatically; mailed returns need it attached.

- If you're banned (CP79A) or unsure, wait out the ban period before claiming the credit, then file Form 8862. Claiming during a ban can extend your problems.

- Keep copies of everything — the notice, your proof of eligibility, and the return where you attached Form 8862.

CP79 notice questions, answered

Do I owe money because of a CP79 notice?

Not by itself. A CP79 explains that a credit like the EITC was disallowed on a past return and tells you to file Form 8862 next time. If disallowing the credit also created a balance for that year, the bill comes in a separate notice — usually a CP14. The CP79 is the rule for future years.

How long am I barred from claiming the EITC after a CP79?

A basic CP79 has no ban — you just have to file Form 8862 the next year you claim the credit. But if the IRS found reckless or intentional disregard of the rules, you can be barred for 2 years, and 10 years for fraud. A CP79A notice usually signals the 2-year ban. Read which version you received carefully.

What is Form 8862 and when do I file it?

Form 8862, Information To Claim Certain Credits After Disallowance, is how you tell the IRS you now qualify for a credit that was previously disallowed. You attach it to the tax return for the first year you claim the credit again. Without it, the IRS will automatically reject the credit even if you fully qualify.

Can I still claim the EITC after it was disallowed?

Yes, as long as you genuinely qualify and any ban period has ended. You claim it on a future return and attach Form 8862. The disallowance is not permanent — it just means the IRS will check your eligibility more closely the next time you claim the credit.

What if I think the CP79 is wrong?

If you believe the credit was disallowed by mistake — for example, you actually had the qualifying child or income the rules require — you can ask for audit reconsideration or respond with documents proving eligibility. Don't just ignore it; the disallowance stays on your account and blocks the credit until it's corrected.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.