IRS Notices

CP87A Notice: What to Do When Someone Else Claimed Your Dependent (2026)

The short answer: a CP87A notice means the IRS found the same dependent — same Social Security number — on two different tax returns. It is a warning, not a bill or an audit. If your claim is correct, you don't have to respond. If it isn't, file Form 1040-X to remove the dependent.

Maybe you're the grandparent who has raised this child all year, and now a letter says another return lists the same grandchild — and it refuses to say whose return. That silence is the strangest part of a CP87A notice, and it's deliberate: privacy law forbids the IRS from naming the other taxpayer. The good news is that this conflict is usually resolved on paper, quietly, and the person with the stronger claim almost always keeps it.

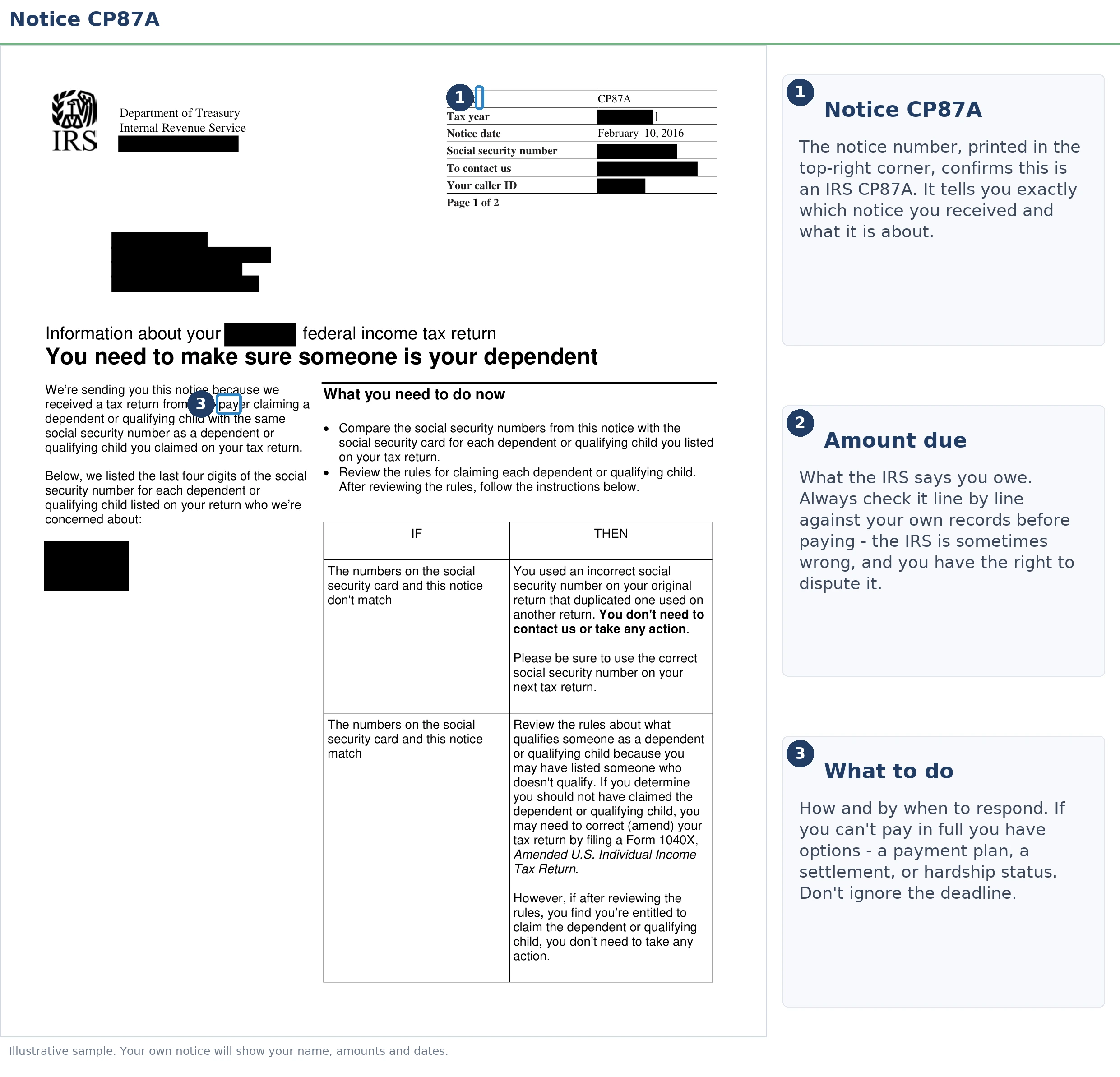

The image below shows exactly what a CP87A looks like and where to find the tax year and the dependent the IRS is questioning — those two details on your copy define the entire dispute.

⏱ The real clock: a CP87A prints no response deadline. But if your claim was wrong, the 0.5%-per-month failure-to-pay penalty and daily interest on the resulting balance have been running since that return's original due date. Every month you wait to amend costs more than the last — and waiting until an audit opens costs the most.

Why you got a CP87A notice

A CP87A goes out when the IRS's computers match the same dependent's Social Security number on two returns for the same tax year. No human reviewed either return — the match is automated, and both taxpayers receive the identical notice. Getting one doesn't mean the IRS thinks you're the one who's wrong; it means the system can't tell yet.

The notice lists the tax year and the dependent in question, but never the other filer. In real life, the "someone else" is usually predictable: an ex-spouse claiming out of turn, the child's other parent, an adult child who filed and claimed their own kid without telling the grandparent supporting them, or a relative in a shared household. If two parents are the ones colliding, our guide to both parents claiming the same child covers that specific fight in depth.

If you're not sure why the IRS writes at all — or how this notice fits into the larger universe of IRS mail — our overview of why you got a letter from the IRS explains the system in one place. The rest of this page stays on what makes a CP87A different: it's the only common notice that asks two strangers to sort out a dispute the IRS won't referee yet.

First question: was your claim correct?

When two taxpayers claim the same child, IRS tiebreaker rules decide who keeps the dependent: parent over non-parent, then more nights with the child, then higher adjusted gross income. Everything you do after a CP87A flows from how those rules apply to you — so run them honestly before you decide whether to hold firm or amend.

| Situation | Who gets the dependent |

|---|---|

| Only one claimant is the child's parent | The parent — a grandparent, aunt, or other relative loses to a parent who qualifies and claims |

| Both claimants are parents, child lived longer with one | The parent the child spent more nights with during the year |

| Both are parents, time split exactly equally | The parent with the higher adjusted gross income (AGI) |

| Neither claimant is a parent (e.g., grandparent vs. aunt) | The claimant with the highest AGI, if the child qualifies for each |

| A parent qualifies but chooses not to claim the child | A non-parent may claim only if their AGI is higher than the highest AGI of any parent who could have claimed the child |

Two threshold tests come before the tiebreakers even matter. First, residency: a qualifying child generally must have lived with you for more than half the tax year. Second, support and age rules must be met. A grandparent whose grandchild genuinely lives in her home most of the year often has a stronger claim than a parent who sees the child on weekends — the rules follow where the child sleeps, not what a custody paper or a family agreement says.

One wrinkle worth knowing: a custodial parent can release the dependency claim to a non-custodial parent with Form 8332 — but that release moves only the Child Tax Credit, not the Earned Income Tax Credit or Head of Household status. Split-credit situations like this are a common source of CP87A collisions where, in a sense, both people are partly right.

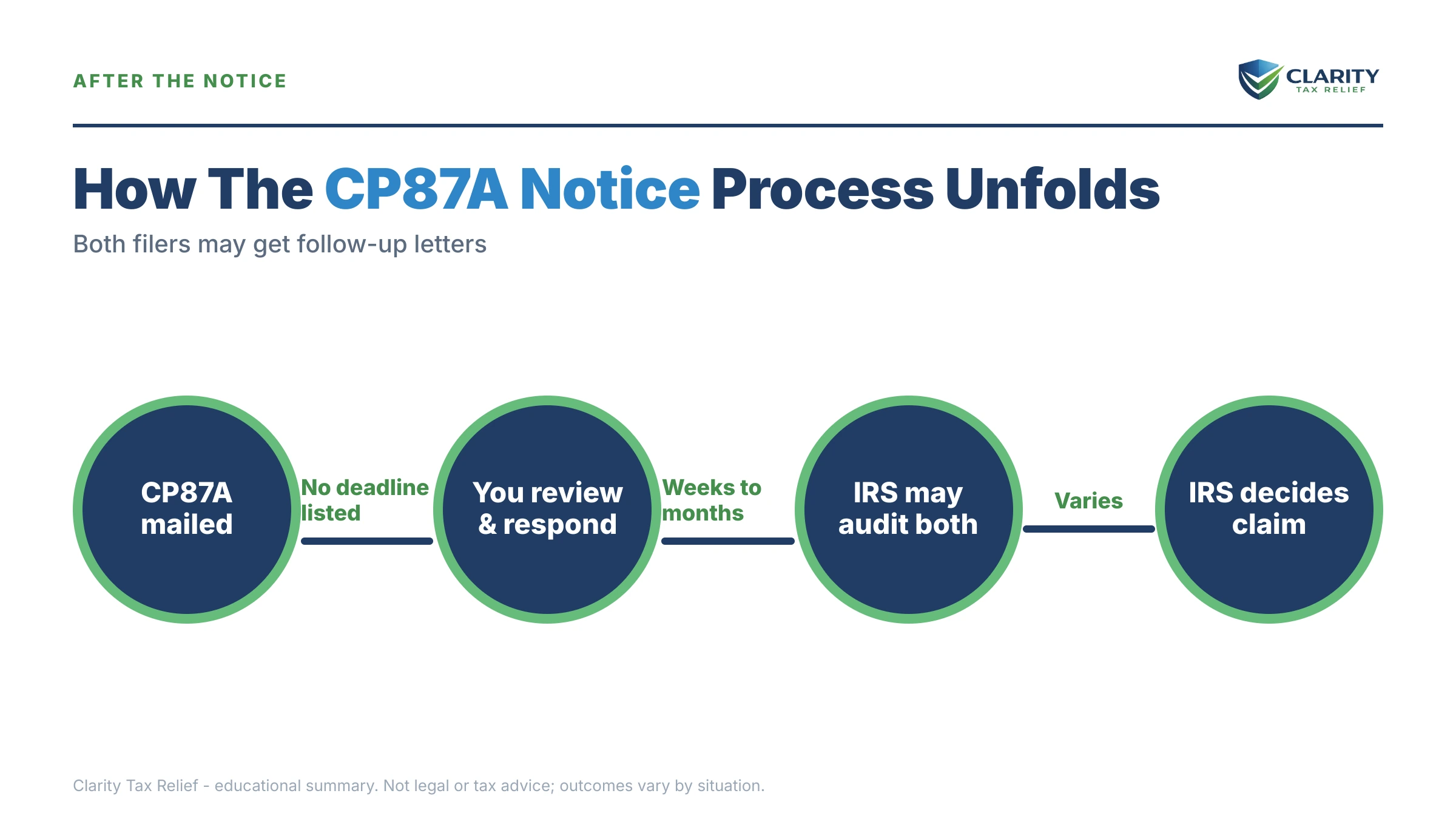

What happens if you ignore a CP87A notice

Ignoring a CP87A triggers no immediate bill — but if neither taxpayer amends, the IRS can audit both returns and disallow the losing claim with interest and penalties added. The sequence isn't calendar-driven the way a collection notice is; it's decision-driven. Here's the order things unfold in:

- CP87A arrives at both households. Informational only. No enforcement, no balance due, no examiner assigned.

- One party amends. If the person with the weaker claim files Form 1040-X and removes the dependent, the conflict usually closes with no further contact for the other filer.

- Neither party amends. The IRS can select one or both returns for examination — often a CP75 EIC audit or a correspondence exam asking each claimant to prove the child's relationship and residency using the Form 886-H-DEP document list.

- The tiebreaker loser gets a proposed change. Disallowed credits must be repaid with interest, a 20% accuracy-related penalty can attach, and a reckless or fraudulent Earned Income Tax Credit claim can bring a two-year ban on claiming that credit.

- An unpaid assessment enters collections. The balance becomes a bill — starting with a CP14 notice — and from there the standard IRS collection sequence takes over.

Notice what that sequence means strategically: doing nothing is a legitimate choice only for the person whose claim survives the tiebreaker rules and who can prove it on paper. For everyone else, "wait and see" just converts a quiet amendment today into an audit, a penalty, and a collections file later. In 2026, with IRS staffing down sharply, the exam that follows may take longer to arrive — but the interest meter on a wrong claim never pauses while you wait.

Not sure your claim survives the tiebreaker?

A duplicate dependent claim only gets more expensive to untangle after an audit opens. Send us a photo of your CP87A — an experienced tax professional will tell you whether your claim holds up under the tiebreaker rules and exactly what to do next. Free and confidential: (888) 825-7779 or the 2-minute form.

Your options after a CP87A — both lanes

After a CP87A you have exactly two lanes: defend a correct claim with documents, or amend a wrong one with Form 1040-X before an audit opens. There is no middle path where the notice simply goes away on its own — one return keeps the dependent, and one doesn't.

Lane 1 — your claim is correct. Do not amend, and don't remove the dependent out of fear. You aren't required to reply to the notice at all. Instead, build the file you'd need if an audit follows: school records showing your address, pediatrician and dental records, a lease or landlord statement listing the child, benefits or insurance paperwork tying the child to your home. Our guide to proving residency and relationship in an EIC audit walks through exactly what examiners accept. If a CP75 or exam letter never comes, that folder cost you an afternoon. If one does come, it wins the case.

Lane 2 — your claim was wrong. File Form 1040-X for the year on the notice, remove the dependent, recompute the Child Tax Credit, Earned Income Tax Credit, and — often forgotten — your filing status, since losing the dependent may also mean losing Head of Household. Amending voluntarily generally avoids the 20% accuracy-related penalty an audit disallowance can bring, and if EITC was involved, it can spare you the two-year credit ban that follows a reckless claim (a ban that arrives with a CP79 notice and a Form 8862 requirement to reclaim the credit later).

Amending will usually create a balance due. Here's what realistically fits at each size — note that dependent-credit balances rarely reach the levels that require financial disclosure:

| Balance after amending | Realistic options | What to know |

|---|---|---|

| Under $1,000 | Pay in full, or a short-term plan (up to 180 days) | $0 setup fee on a short-term plan; interest still accrues until paid |

| $1,000 – $10,000 | Short-term plan, or a guaranteed installment agreement | At $10,000 or less with clean compliance, the IRS must accept a qualifying monthly plan |

| $10,000 – $25,000 | Streamlined installment agreement, up to 72 months | Set up online, no detailed financial disclosure; penalties and interest continue during the plan |

| $25,000 – $50,000 | Streamlined agreement with direct debit | Direct debit is required in this band to stay streamlined; multi-year disallowances land here most often |

If you're on a fixed income and even a small monthly payment would squeeze rent, food, or medicine, hardship status exists for exactly that situation — see our guide to IRS hardship on Social Security income before agreeing to a payment you can't sustain.

What a duplicate dependent claim can cost: a worked example

Say you're 67, living on Social Security plus about $14,500 a year from a part-time job, and you claimed your 9-year-old grandson for 2023, 2024, and 2025 because he lives with you full-time. Between the Child Tax Credit, the Earned Income Tax Credit, and Head of Household filing status, that claim is worth roughly $5,000 per year on a return like that.

Now his father — your son — claims him too, and CP87As land in both mailboxes. If the IRS ultimately disallowed all three of your years, the clawback would run roughly 3 × $5,000 = $15,000, and interest plus a failure-to-pay penalty could push the total to about $16,400. On a 72-month installment agreement, that's roughly $228 a month ($16,400 ÷ 72) — from a fixed income — while interest keeps accruing.

But run the tiebreaker rules: the child lived with you more than half of each year, so your son's weekend visits don't give him a qualifying child at all, and the parent-beats-non-parent rule never comes into play. In this hypothetical, that $16,400 is what your document folder protects — and what his Form 1040-X resolves. If you're the one amending instead, you can estimate what the added months are costing with our IRS penalty and interest calculator before you file.

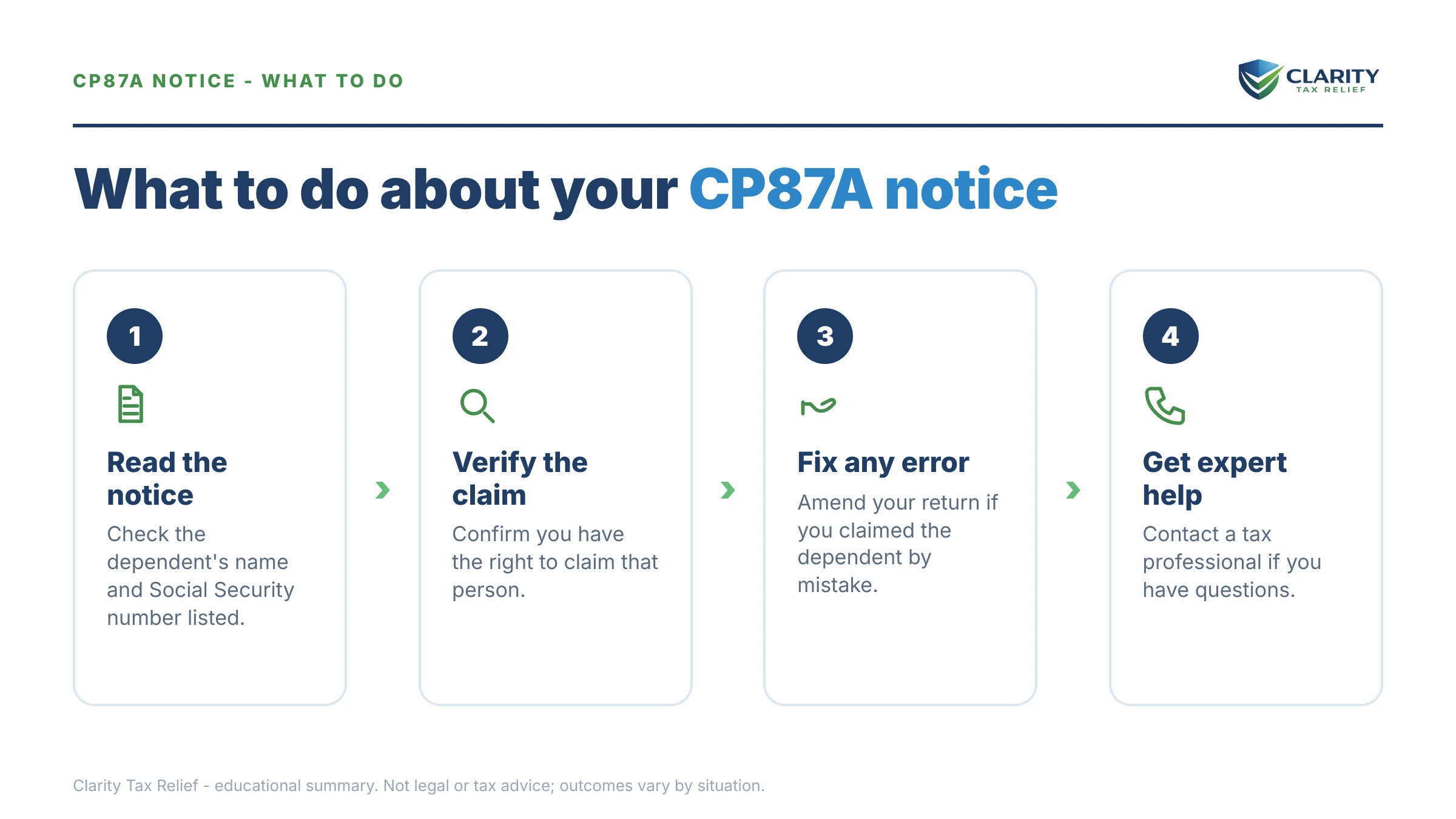

How to respond to a CP87A, step by step

- Confirm your claim — run the tiebreaker rules above against your situation for the tax year printed on the notice.

- Gather proof — if you're keeping the claim, collect school, medical, and residency records that place the child in your home for more than half that year.

- Amend if you were wrong — file Form 1040-X for that year, remove the dependent, and recalculate the credits and your filing status.

- Handle any new balance — pay at IRS.gov/payments or set up a payment plan so penalties and interest stop growing.

- Get help if an audit follows — if a CP75 or another exam letter arrives next, have an experienced tax professional review it before you reply.

One practical note on step 3: amended returns move slowly, often several months, and the CP87A conflict stays technically open until the amendment processes. That delay is normal, not a sign your fix failed — see why amended returns take so long if you're waiting.

When you can handle a CP87A yourself

Most people can handle a CP87A without professional help — the notice itself requires no response if your claim is correct. You're fine on your own when the facts are simple: the child clearly lived with you more than half the year, you can pull school and medical records showing your address, and the other claimant is someone you can identify and, ideally, talk to. Likewise, if you know you claimed in error and the resulting balance is one you can pay or put on a simple online plan, a Form 1040-X and twenty minutes at IRS.gov settles it.

Experienced help changes the outcome in a narrower set of situations: an audit letter has already arrived and the money at stake spans multiple years; the residency facts are genuinely messy (the child moved mid-year, or lived in two households); an EITC ban is on the table; or you're on a fixed income and the repayment demand would create real hardship — our guide for people who are retired and owe back taxes covers that intersection. In those cases, how the documents are assembled and argued often decides who keeps thousands of dollars in credits.

Terms on your CP87A, decoded

- Qualifying child — the IRS test a dependent must pass: relationship, age, residency (more than half the year with you), and support.

- Tiebreaker rules — the fixed order the IRS uses when two people claim the same child: parent over non-parent, more nights with the child, then higher AGI.

- Form 1040-X — the amended-return form you file to remove a dependent you claimed in error.

- Form 886-H-DEP — the IRS's checklist of documents that prove a dependent claim in an audit.

- Form 8332 — the release a custodial parent signs to let the other parent claim the child's tax credit (it does not transfer EITC or Head of Household status).

- Two-year EITC ban — the penalty barring you from claiming the Earned Income Tax Credit for two years after a reckless or intentional wrong claim.

CP87A questions, answered

Do I need to respond to a CP87A if I correctly claimed my dependent?

No — if your dependent claim is correct, the IRS does not require a reply to a CP87A. Keep the notice and gather proof of residency and relationship (school records, medical records, a lease showing the child's address) in case an audit letter follows. The other person who claimed the dependent received the same notice, and if they amend, the matter usually closes without you doing anything.

Does a CP87A tell me who else claimed my dependent?

No. Federal privacy law bars the IRS from naming the other taxpayer, so the notice only tells you a duplicate claim exists. In practice it is most often an ex-spouse, the child's other parent, or another relative in the household. If you genuinely cannot think of anyone who could have claimed the child, treat it as possible dependent identity theft and consider filing Form 14039.

What happens if neither of us amends after a CP87A?

The IRS can select one or both returns for examination — usually a correspondence audit asking each of you to prove the child's residency and relationship. The examiner applies the tiebreaker rules: parent over non-parent, then more nights with the child, then higher adjusted gross income. The losing taxpayer repays the credits with interest and can face a 20% accuracy-related penalty.

Can a grandparent claim a grandchild instead of the parent?

Sometimes. A grandchild who lived with you more than half the year can be your qualifying child. But if a parent also qualifies to claim the child and chooses to, the parent wins the tiebreaker. When a parent qualifies but doesn't claim the child, you can claim the grandchild only if your adjusted gross income is higher than the highest AGI of any parent who could have claimed them.

What documents prove my child lived with me?

The IRS's own checklist, Form 886-H-DEP, is the standard: school records showing your address, medical or daycare records, a lease or landlord letter listing the child, and official mail sent to the child at your address. Records should cover more than half the tax year in question. Start collecting them now — an audit that follows a CP87A runs on paper deadlines, and thin documentation is the most common reason legitimate claims get disallowed.

Will I be penalized if I claimed a dependent by mistake?

You'll owe back the credits plus interest from the return's original due date, and possibly a failure-to-pay penalty of 0.5% per month. Amending voluntarily with Form 1040-X before an audit opens generally puts you in a far better position than waiting for the IRS to disallow the claim, which can add a 20% accuracy-related penalty. Reckless or fraudulent EITC claims can also trigger a two-year ban on claiming that credit.

Is a CP87A notice an audit?

No. A CP87A is an informational notice — no one is examining your return yet, and there is no balance due printed on it. Think of it as a warning shot: the IRS's computers matched a duplicate dependent Social Security number, and if the conflict isn't resolved by one party amending, an audit of one or both returns may follow later.

Your next 24 hours

- Find the tax year and dependent on your CP87A — both appear near the top of the notice. That's the only year and only claim in dispute; nothing else on your return is being questioned.

- Pull three documents — that year's tax return, the notice itself, and one record placing the child at your address (a school enrollment form or a pediatrician's statement is a strong start).

- Get a free case review — if you're unsure your claim survives the tiebreaker rules, or an amendment would leave a balance you can't pay, call (888) 825-7779 or use the 2-minute form. Interest on a wrong claim compounds daily; clarity today is the cheapest version of this problem.

Primary sources: the IRS's official page, Understanding your CP87A notice; the amendment form itself at About Form 1040-X; and payment and plan setup at IRS.gov/payments.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.