IRS Notices

CP91 Social Security Levy: How to Stop the 15% Before It Starts (2026)

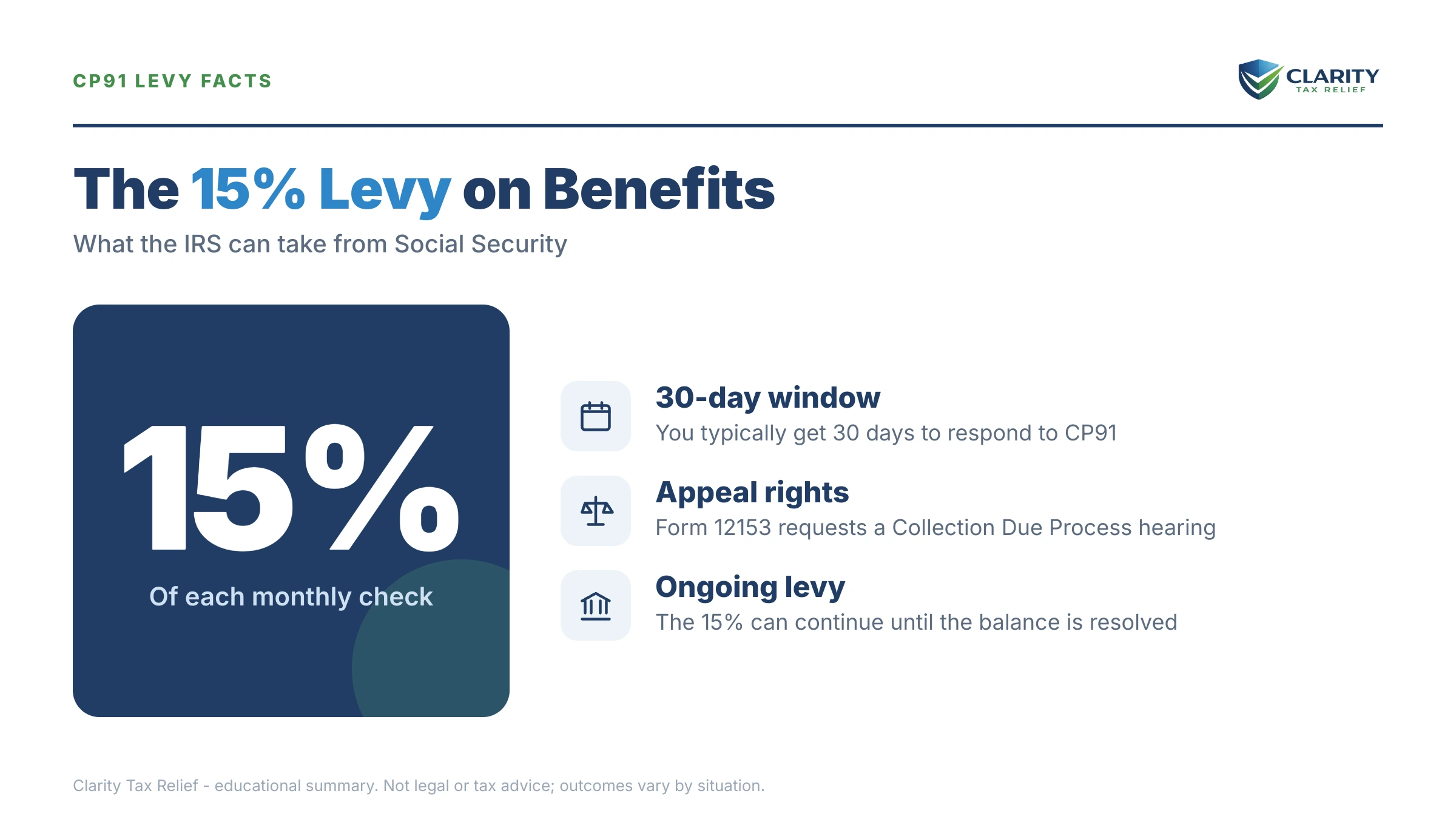

The short answer: a CP91 is the IRS's final warning before it takes up to 15% of your monthly Social Security check through the Federal Payment Levy Program. You have 30 days from the date on the notice to arrange payment, hardship status, or an appeal — otherwise the 15% deduction starts and repeats every month.

The letter in your hand says the government intends to take a slice of the one deposit you count on. If you're recently divorced and the balance traces back to a return you signed years ago — maybe one your ex was supposed to handle — the unfairness stings. But the CP91 social security levy follows rules, the rules cut both ways, and you have a real window to use them.

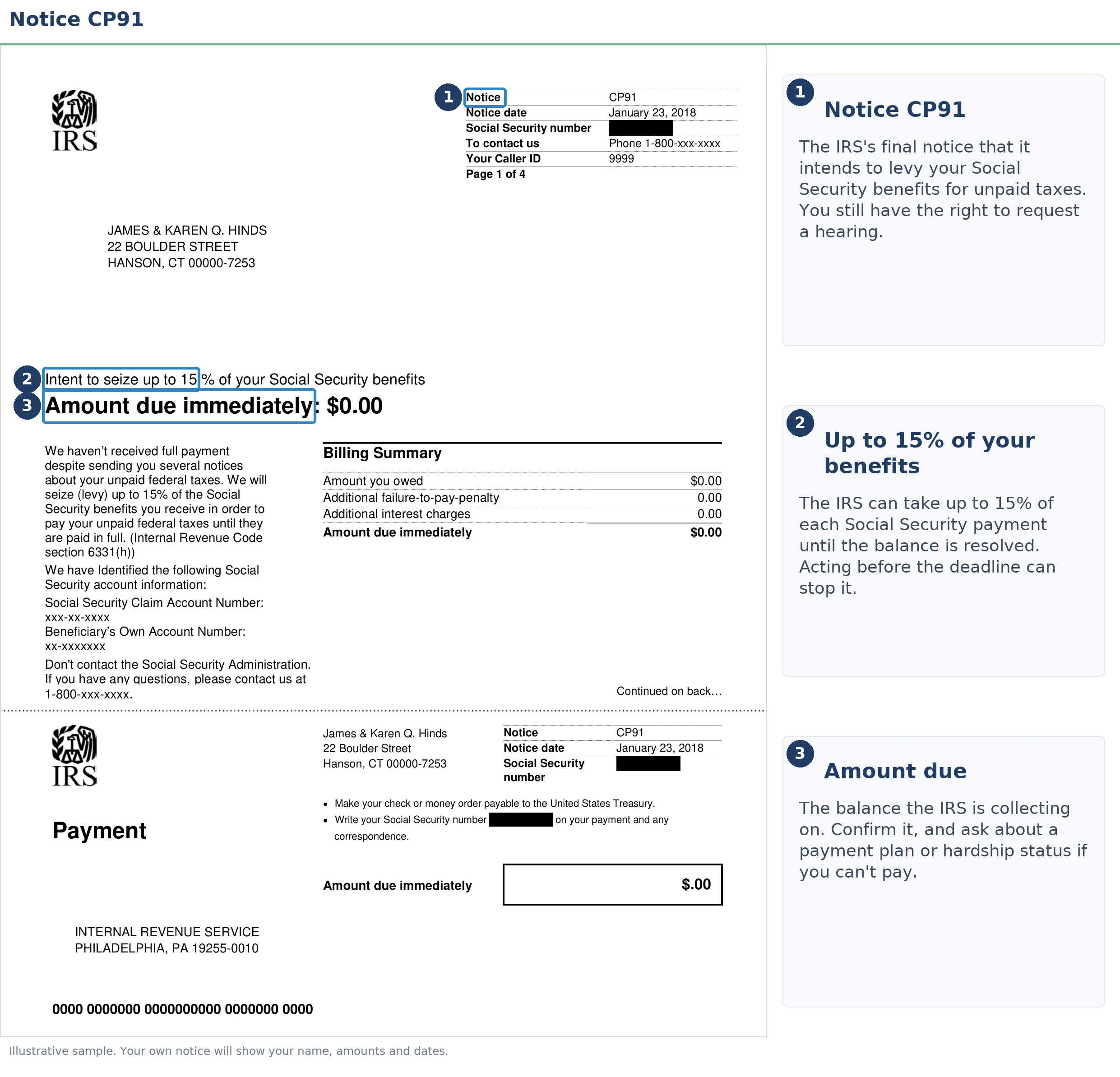

Not sure the letter you're holding is actually a CP91? The image below shows exactly what this notice looks like and where the balance, tax year, and deadline sit on the page — check yours against it before you do anything else.

⏱ Your deadline: the CP91 gives you 30 days from the notice date printed on page one — not the day you opened it — before the IRS can begin taking up to 15% of your Social Security benefit. After that, the deduction repeats every month until the debt is resolved or the levy is released.

Why you got a CP91 notice

A CP91 means the IRS has an assessed, unpaid tax balance on your account and has matched your Social Security number to monthly benefit payments through the Federal Payment Levy Program (FPLP). It is not a bill, a review, or an audit — it is the last notice specific to your Social Security income before the automated levy switches on. (Businesses get the same warning as a CP298.)

You didn't skip straight to this letter. The IRS mails a sequence of bills first — if you never saw them, the most common reason after a divorce is that earlier notices went to a former address or a former spouse's mailbox. The IRS mails to the last address on your most recent return, and it isn't required to track you down before levying. Our overview of why the IRS sends letters covers the general notice system; what matters here is that the system has now found income it can reach automatically.

The mechanics are worth understanding, because they explain both the threat and the fix. The IRS transmits your account to the Treasury's Bureau of the Fiscal Service, which pays Social Security benefits. The Fiscal Service then withholds 15% of each payment and applies it to your tax debt. No revenue officer decides this. No human weighs your circumstances. A computer matches your SSN to a benefit payment — which also means changing your account's status (a plan, a hardship code, a pending claim) is what turns the computer off.

How much of your Social Security the CP91 levy takes

A CP91 levy takes up to 15% of every monthly Social Security payment — continuously, until the balance is paid, the collection statute expires, or the levy is released. Unlike a bank levy, which grabs what's in the account on one day, this is a continuous levy: it renews itself automatically each month with no further notice.

Two features make the FPLP levy different from other garnishments, and both matter on a fixed income. First, there is no exempt floor under FPLP — the 15% comes out even of a small check. A paycheck garnishment leaves you a calculated exempt amount; the automated Social Security levy does not. Second, it reaches retirement, survivor, and Social Security Disability Insurance (SSDI) benefits alike. The program excludes Supplemental Security Income (SSI), lump-sum death payments, and benefits paid to children — we cover the disability side in detail in can the IRS garnish SSDI.

One more distinction: the 15% figure belongs to the automated program. If your case lands with a human collector instead, a manually issued paper levy on Social Security follows different rules and can sometimes reach more of your benefit. Responding inside the CP91 window keeps you out of both lanes. If you also have wages or other income the IRS could reach, you can estimate that exposure with our IRS wage garnishment calculator — it estimates, it doesn't predict your exact outcome. For the full mechanics of the program itself, see our guides to the Federal Payment Levy Program and the 15% Social Security levy.

What happens if you ignore a CP91

If you do nothing for 30 days after a CP91, the IRS transmits your account to the Treasury's payment system and the 15% deduction begins with an upcoming benefit payment. The sequence from there is automated and repeats itself:

- Day 0 — CP91 issued. The notice date starts the clock. Nothing has been taken yet.

- Day 30 — the window closes. With no arrangement on your account, the IRS is free to transmit the levy to the Bureau of the Fiscal Service.

- A following benefit cycle — the first deduction. Because of payment-processing lead times, the first 15% cut may land one or two deposits after day 30. Don't read the delay as a reprieve.

- Every month after — the levy renews automatically. It continues until the debt is fully paid, the 10-year collection statute expires, or you get a release.

- In parallel — other collection continues. The CP91 doesn't limit the IRS to your benefit. If final-notice rights were already issued for these years, bank accounts remain reachable, refunds keep being offset, and a federal tax lien can be filed.

In 2026 this automation matters more than ever. The IRS workforce shrank roughly 27% in 2025, so reaching a human to fix a problem is slower — but the FPLP computer never took a furlough. The machine escalates on schedule whether or not anyone answers the phone, which is why the 30 days on your notice are worth more than the 30 days after them.

Here is where the CP91 sits in the full collection sequence, so you can see what came before it and what the next stage looks like:

| Notice | What it does | Your window |

|---|---|---|

| CP14 | First bill for the balance due | ~21 days before escalation |

| CP501 / CP503 | Reminder bills; penalties and interest keep accruing | Escalates if unpaid |

| CP504 | Intent to levy your state tax refund | Date printed on the notice |

| CP90 / LT11 | Final notice of intent to levy, with Collection Due Process rights | 30 days to request a hearing |

| CP91 / CP298 | Final warning before the FPLP levy on Social Security specifically | 30 days from the notice date |

| FPLP levy | 15% of each monthly benefit, continuously | Until resolved, released, or the CSED passes |

If a CP504 is also sitting in your stack, our guide to CP504 — how long before levy explains where that notice fits and why it isn't the final one. And note the CP90 row: if you received a CP90 notice for these same years, that letter — not the CP91 — is the one that carried your formal hearing rights. Check your CP91's appeal-rights paragraph; if a hearing is still available, filing Form 12153 for a CDP hearing in time generally holds the levy while your case is heard.

Holding a CP91 with the clock running?

Get your CP91 reviewed free before the 30-day window closes — before the first 15% comes out of your check. An experienced tax professional will confirm what you actually owe, whether the balance is even yours to pay after a divorce, and the fastest way to keep your benefit whole.

How to stop the Social Security levy: your options

Every option that stops a CP91 levy works the same way: it changes your account's status before — or after — the levy transmits. The IRS computer checks status, not sympathy. Here is the full menu, with the eligibility line for each:

| Option | Effect on the levy | You may qualify if | Cost |

|---|---|---|---|

| Pay in full | Levy never transmits; account closes | You can pay by the notice deadline | Balance only; stops future accruals |

| Short-term payment plan | Blocks the levy while active | You can pay everything within 180 days | $0 setup; interest and penalties continue |

| Guaranteed installment agreement | Blocks the levy while you pay monthly | You owe $10,000 or less and can pay within 3 years, with returns filed | Modest setup fee (reduced for direct debit / low income); accruals continue |

| Streamlined installment agreement | Blocks the levy while you pay monthly | You owe $50,000 or less; up to 72 months, set up online | Setup fee varies by method; accruals continue |

| Currently Not Collectible (hardship) | Levy is held or released while CNC is in place | Your benefit barely covers allowable living expenses (Form 433-F) | Free to request; debt remains and accrues |

| Offer in Compromise | Levy generally held while the offer is pending | Your income and assets genuinely can't cover the debt before the CSED | $205 fee + 20% down on lump-sum offers; both waived with low-income certification |

| Innocent spouse relief | Collection against you generally pauses during review | The debt traces to a former spouse's income or errors on a joint return | Free to request (Form 8857) |

| Penalty abatement | Shrinks the balance; doesn't stop the levy by itself | Clean compliance for the prior 3 years (First-Time Abate), or reasonable cause | Free to request |

Three of these deserve a closer look for the person most likely to be holding this notice.

The hardship route is real, and it was built for fixed incomes. If losing 15% of your benefit would leave you unable to pay rent, utilities, food, or medical costs, the IRS can place your account in Currently Not Collectible status — and if the levy has already started, an economic hardship levy release under IRC §6343 can stop it. Either path runs on a financial statement, usually Form 433-F, comparing your benefit against the IRS's allowable living expense standards. Our guide to IRS hardship while on Social Security walks through that math for benefit-only households. Be honest with yourself here: CNC pauses collection, it doesn't erase the debt, and interest keeps accruing — but for many retirees the debt then quietly ages toward the 10-year statute.

The divorce angle can change who owes at all. If the balance comes from a jointly filed return, you and your ex are each liable for 100% of it — and a divorce decree saying your ex pays does not bind the IRS, a trap we unpack in divorce and IRS debt: who pays. But if the tax traces to income your ex earned or hid, innocent spouse relief via Form 8857 can remove your share of the liability entirely, and collection against you is generally suspended while the claim is reviewed. For someone facing a CP91 over an ex's tax, this is often the single highest-value move on the board.

Penalty relief shrinks what everything else has to solve. If this is your first slip after years of clean filing, First-Time Abate can remove the failure-to-pay penalty — and starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) begins applying similar relief automatically, with no request needed. A smaller balance means a smaller plan payment, a shorter payoff, and less interest.

A worked example: $4,800, a divorce, and a $1,900 benefit

Say you owe $4,800 from the last joint return you filed before your divorce, and your Social Security retirement benefit is $1,900 a month. This is a hypothetical, but the arithmetic is exactly what the IRS's computer will run.

If you do nothing: the FPLP levy takes 15% of $1,900 — $285 out of every monthly check. Meanwhile the balance keeps growing: the failure-to-pay penalty adds 0.5% a month and interest compounds on top. At $285 a month against a growing balance, the levy runs roughly 18 months and pulls somewhere around $5,100 from your benefit before it releases — all on the government's schedule, not yours.

If you set up a guaranteed installment agreement instead: at $4,800 you're under the $10,000 ceiling for a guaranteed installment agreement, which the IRS must accept if your returns are filed and you can pay within three years. The bare math is $4,800 ÷ 36 ≈ $133 a month; choosing something like $160 keeps you ahead of the accruing penalty and interest. The levy never starts, and you keep roughly $125 more of your check each month than the levy would have left you — and you chose the number.

If $1,900 barely covers your life: rent, Medicare premiums, prescriptions, food — run the Form 433-F numbers. If nothing is left over under the IRS's expense standards, CNC status can hold collection entirely at $0 a month.

If the $4,800 is really your ex's tax: say it comes from 1099 income he earned and never told you about on that joint return. An innocent spouse claim could remove your liability altogether — worth evaluating before you agree to pay a dime of it.

How to respond to a CP91, step by step

- Find the deadline — locate the notice date on page one of your CP91 and count 30 days from that date — not from the day you opened the envelope.

- Verify the balance — log into your IRS online account and confirm the tax year, the amount, and that no payments or credits are missing from the total.

- Choose your resolution — pick the path that fits your finances: a payment plan, hardship status, an innocent spouse claim, or an Offer in Compromise.

- Get it on the record before day 30 — set up the plan online, or submit Form 433-F, Form 12153, or Form 8857 as your path requires — the arrangement must post to your account before the window closes.

- Confirm the levy is held — check that your arrangement shows as active on your IRS account, then watch your next benefit deposit to confirm the full amount arrives.

A note on step 4: an online agreement posts to your account the day you complete it, which is why the online route beats the phone in 2026. If you'd rather file on paper, Form 9465 requests the same installment agreement by mail — but mailed forms take weeks to process, and the levy clock doesn't wait for the mailroom.

When you can handle a CP91 yourself

A $4,800 balance with a CP91 is often a case you can resolve yourself in one afternoon. Be honest about which side of this line you're on.

You can likely handle it alone if: you agree the balance is yours, it's under $10,000, your returns are all filed, and you can manage a monthly payment. Log into your IRS account, set up the guaranteed installment agreement online before day 30, and confirm it shows active. That's the whole fix — no firm required, ours included.

Experienced help changes outcomes when: the levy has already started deducting and you need a release negotiated; the balance comes from a joint return and an innocent spouse claim needs facts, timelines, and evidence assembled correctly the first time; you have multiple years unfiled (the IRS won't grant most agreements until returns are in); the numbers point toward an Offer in Compromise, where the IRS accepted roughly 1 in 5 offers in FY2024 and the difference is usually in the financial-statement math; or the CP91 sits on top of other enforcement — a lien, a bank levy, a passport certification on a larger balance. In those cases, sequence matters: fixing things in the wrong order can cost you months of levied checks.

If your CP91 involves a joint-return balance from before your divorce and you're not sure whose debt it legally is, have it reviewed free before the 30-day window closes — or call (888) 825-7779.

Transcript codes to watch after a CP91

Your IRS account transcript records the CP91 — and everything that happens after it — as three-digit transaction codes. Pulling your transcript is the fastest way to confirm your fix actually posted before the deadline:

| Code | What it means | What to do |

|---|---|---|

| 971 | Notice issued — the CP91 (and prior notices) post under this code | Match the 971 dates against the letters you actually received; gaps suggest mail went to an old address |

| 670 | Payment posted to the account | Confirm every payment you've made appears; a missing one may shrink or erase the balance |

| 480 | Offer in Compromise pending | Confirms your offer was accepted for processing — the levy is generally held while it's under review |

| 530 | Account placed in Currently Not Collectible status | This is the code that proves your hardship request took effect; keep the date for your records |

| 520 | Bankruptcy or litigation freeze on collection | If you've filed bankruptcy, verify this posted — it suspends the levy while active |

| 582 | Federal tax lien indicator | A lien can run parallel to the levy; factor it into any plan involving property or refinancing |

Terms on your CP91, decoded

The notice uses collection vocabulary that rewards a plain-English translation:

- FPLP (Federal Payment Levy Program): the automated Treasury system that withholds up to 15% of federal payments — including Social Security — and applies it to tax debt.

- Continuous levy: a levy that renews itself against each payment as it's issued, month after month, unlike a one-time grab from a bank account.

- Levy vs. lien: a levy takes money or property; a lien is a legal claim against what you own. A CP91 is about a levy — but a lien can be filed alongside it.

- CDP hearing (Collection Due Process): your formal right to an independent appeal before certain levies, requested on Form 12153 within the 30-day window on a final notice.

- Economic hardship release (§6343): the law requiring the IRS to release a levy that prevents you from meeting basic living expenses.

- CSED (Collection Statute Expiration Date): the date, generally 10 years after assessment, when the IRS's right to collect — and any levy — ends. Certain events pause the clock; see how long the IRS can collect back taxes.

Primary sources, if you want them: the IRS's own page at Understanding your CP91 notice, the official IRS payment plans and installment agreements page for setting up an arrangement online, and the Taxpayer Advocate Service if the levy is causing hardship and normal channels stall.

CP91 Social Security levy: your questions, answered

Can the IRS really take my Social Security check?

Yes. Under the Federal Payment Levy Program, the IRS can take up to 15% of your monthly Social Security retirement or disability benefit, and the CP91 is the warning that it is about to start. There is no dollar floor protecting small checks under FPLP — the 15% comes out even of a modest benefit. SSI is the exception: it can never be levied through this program.

How much of my Social Security can a CP91 levy take?

Up to 15% of each monthly payment, continuously, until the debt is resolved or the levy is released. On a $1,900 benefit that is $285 a month, every month. A manually issued levy outside the automated program follows different rules and can sometimes reach more of your benefit — which is one more reason to respond within the window rather than wait for the IRS to pick its tool.

Does a CP91 levy apply to SSDI and SSI?

SSDI yes, SSI no. Social Security Disability Insurance is paid from the same trust-fund system as retirement benefits, so it is subject to the 15% FPLP levy. Supplemental Security Income is a needs-based payment and is exempt from FPLP entirely. If you receive both, only the SSDI portion is exposed to the CP91 levy.

How do I stop the levy before it starts?

Get a resolution entered on the IRS system before the deadline printed on the notice. A payment plan, currently-not-collectible hardship status, a pending Offer in Compromise, or an appeal filed in time each blocks the levy from being transmitted. The arrangement has to actually post to your account before the 30-day window closes — a phone call that goes nowhere doesn't count, and 2026 hold times make early action essential.

The debt is from a joint return with my ex — do I still get levied?

Yes, unless you obtain relief. Both spouses on a joint return are each liable for the full balance, and a divorce decree assigning the debt to your ex does not bind the IRS. Innocent spouse relief (Form 8857) can remove your liability if the balance traces to your ex's income or errors and you meet the tests, and collection against you is generally suspended while a claim is under review.

What's the difference between a CP90 and a CP91?

A CP90 is the general final notice of intent to levy with Collection Due Process hearing rights; it can precede a levy on wages, bank accounts, or other assets. A CP91 targets one specific asset — your Social Security benefit — through the automated 15% Federal Payment Levy Program. Many people on benefits receive both: the CP90 carries your hearing rights, and the CP91 tells you which income is about to be hit.

Can I get money back after the levy has started?

You can usually stop future deductions much faster than you can recover past ones. Once you set up an agreement or document economic hardship, the IRS releases the levy and the 15% deductions stop, typically after one or two more payment cycles. Refunds of amounts already taken are limited to narrow situations, such as a levy issued in error — so acting before the first deduction matters far more than acting after it.

Does the levy stop when the 10-year collection statute runs out?

Yes — a levy can't outlive the debt. The IRS generally has 10 years from assessment to collect (the CSED), and an FPLP levy must be released when that date passes. But events like a pending Offer in Compromise, bankruptcy, or a Collection Due Process hearing pause the clock, so the true expiration date is often later than ten calendar years. Don't build a plan on waiting it out without confirming your actual CSED.

Will a CP91 levy affect my Medicare?

Your Medicare coverage continues. The levy takes a share of your benefit payment; it does not cancel your enrollment, and your Part B premium keeps being withheld as usual. The practical effect is a smaller net deposit each month — which is exactly why the economic-hardship release exists if that smaller deposit no longer covers your basic living expenses.

Your next 24 hours

- Find the notice date in the upper section of page one of your CP91 and count 30 days forward. Write that date somewhere you'll see it — it's the day the IRS can transmit the levy against your benefit.

- Gather three things: the CP91 itself, your most recent tax return (the joint one, if that's where the balance came from), and your benefit information — the SSA award letter or SSA-1099 — plus a rough list of your monthly living expenses if hardship might apply.

- Get the free case review. Send us a photo of the notice through the 2-minute form or call (888) 825-7779. Before your 30-day window closes, you'll know whether the balance is truly yours, which option keeps your check whole, and exactly what to file first.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.