IRS Forms

Form 433-D: The IRS Installment Agreement Confirmation Form (2025)

The short answer: Form 433-D is the IRS form that confirms and locks in the terms of your installment agreement — your monthly payment amount, the due date, and your bank info if you choose direct debit. It is not a request and it does not ask about your finances. You sign it, return it, and your payment plan is set.

Not sure your 433-D payment is one you can keep?

Send us the form and the notice that came with it. An experienced tax professional will check whether the monthly amount fits your budget and whether a better option exists — free, confidential, no pressure.

⏱ Your deadline: sign and return Form 433-D by the date on the cover letter — usually within 10 to 14 days. For a direct debit plan, your first payment is pulled on the date you and the IRS agree to. Miss a scheduled payment and the IRS can default the agreement and restart collection.

What Form 433-D actually is

If the IRS sent you Form 433-D, that's good news — it means a payment plan is being set up, not torn down. The "433-D" is short for "Installment Agreement." It's the paper that puts your deal in writing: how much you'll pay each month, what day the payment is due, the tax years it covers, and — if you agree to direct debit — the bank account the IRS will draw from. The official form lives at About Form 433-D on IRS.gov.

People mix this up with the 433-A and 433-F all the time, so let's be clear. Those other forms are Collection Information Statements — they ask for your income, expenses, and assets so the IRS can decide what you can afford. Form 433-D asks for none of that. By the time you get a 433-D, the IRS has already decided the terms. This form just makes it official.

433-D vs. 9465 vs. 433-F — which is which

Three forms show up around payment plans, and the names blur together. Here's the plain-English split:

- Form 9465 is the request. You file it to ask the IRS for a monthly plan. Our Form 9465 walkthrough covers it step by step.

- Form 433-F (or 433-A) is the financial disclosure. The IRS uses it to verify what you can pay when your balance is higher or your case is complex. See our Form 433-F walkthrough.

- Form 433-D is the confirmation. It's the final handshake that locks in the agreement once it's approved.

Not everyone sees a 433-D. If you set up a plan through the IRS payment plan online tool, the system confirms the terms on screen and you may never touch the paper form. The 433-D usually appears when you set up a plan by phone, by mail, or through a revenue officer.

What's on the form, box by box

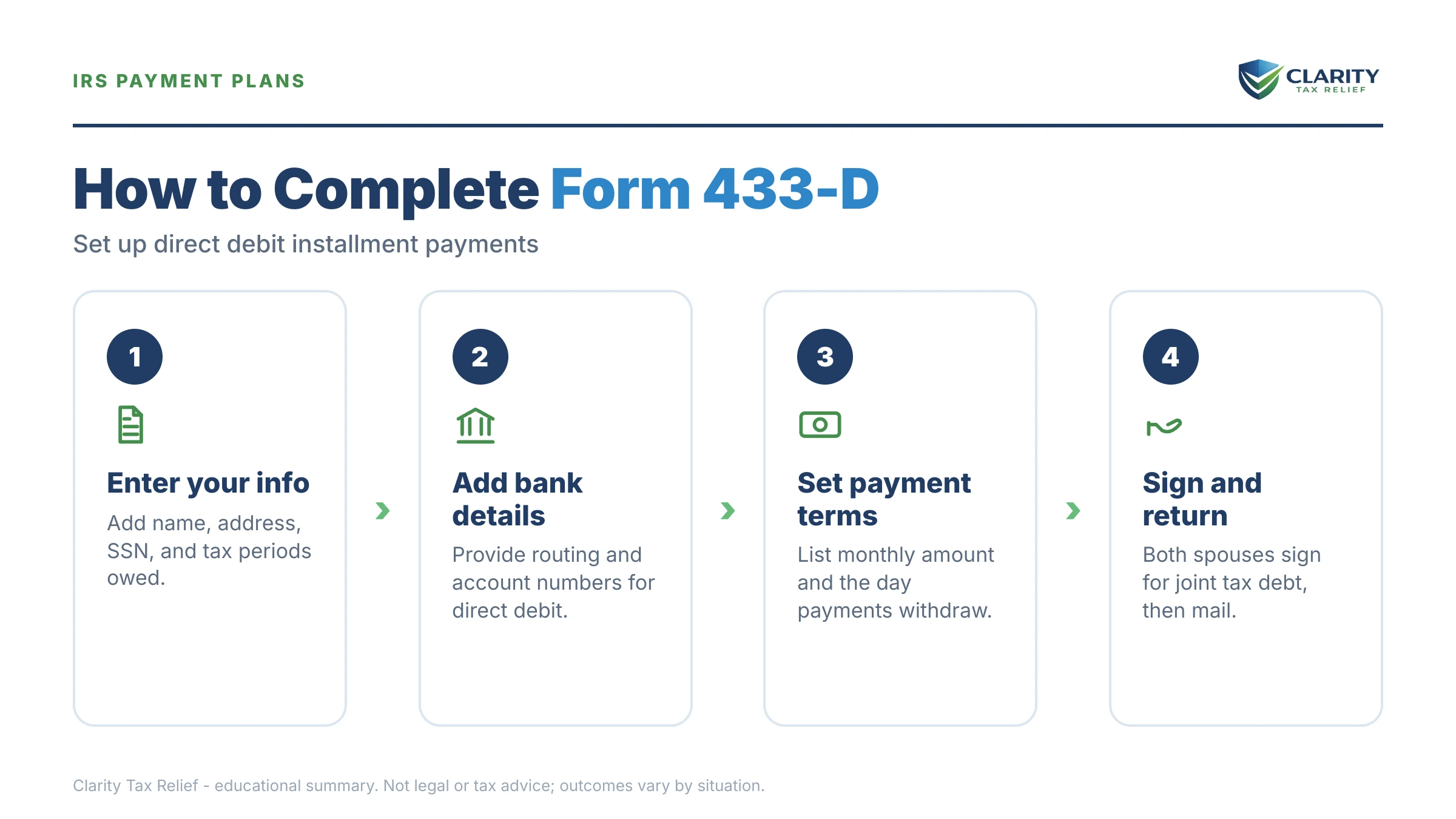

Form 433-D is one page. Don't let it intimidate you. The key fields are:

- Your name, address, and SSN — taken from your tax records. Check that the tax years and balance match what you actually owe.

- The monthly payment amount — the figure you agreed to. Make sure it's a number you can truly afford every month, not just this month.

- The payment due date — the day each month your payment is due or will be pulled. Pick a date right after payday if you can.

- Direct debit section — your bank routing number and account number, if you choose automatic withdrawals. This is optional but often the smartest choice (more below).

- Your signature — you (and your spouse, on a joint debt) sign and date here. That signature is what makes the agreement binding.

Why direct debit usually wins

The 433-D gives you a choice: mail a check each month, or let the IRS pull the payment automatically from your bank. A direct debit installment agreement is almost always the better deal:

- Lower setup fee. Direct debit plans set up online cost far less than mailing checks.

- No forgotten payments. The single biggest cause of defaults is a payment someone simply forgot to send. Auto-draft removes that risk.

- Sometimes required. If you owe roughly $25,000 to $50,000 and want a streamlined plan, the IRS generally requires direct debit. See our streamlined installment agreement guide for the thresholds.

The trade-off: the money leaves on time, every time, whether or not your account is ready. If your cash flow is tight, line up the due date with payday and keep a small buffer in the account.

What happens if your 433-D agreement defaults

A signed installment agreement is a promise — and the IRS treats a broken promise seriously. Here's the sequence if payments stop:

- Missed or late payment — the agreement is now at risk. Interest and the 0.5%-per-month failure-to-pay penalty keep running on the balance.

- CP523 notice — the IRS warns that your agreement is about to terminate. You typically get about 30 days to fix it. Read our CP523 notice guide for the exact steps.

- Agreement terminated — collection restarts. The IRS can move toward liens and levies again.

- Enforcement — wage garnishment or bank levy can follow if you don't reinstate the plan or set up a new one.

The good news: a default is fixable, and it's far easier to act before a payment is missed. If your income drops, call the IRS and ask to lower your monthly payment rather than letting the plan collapse. If you've already defaulted, see what to do when a payment plan defaults.

How to fill out and return Form 433-D, step by step

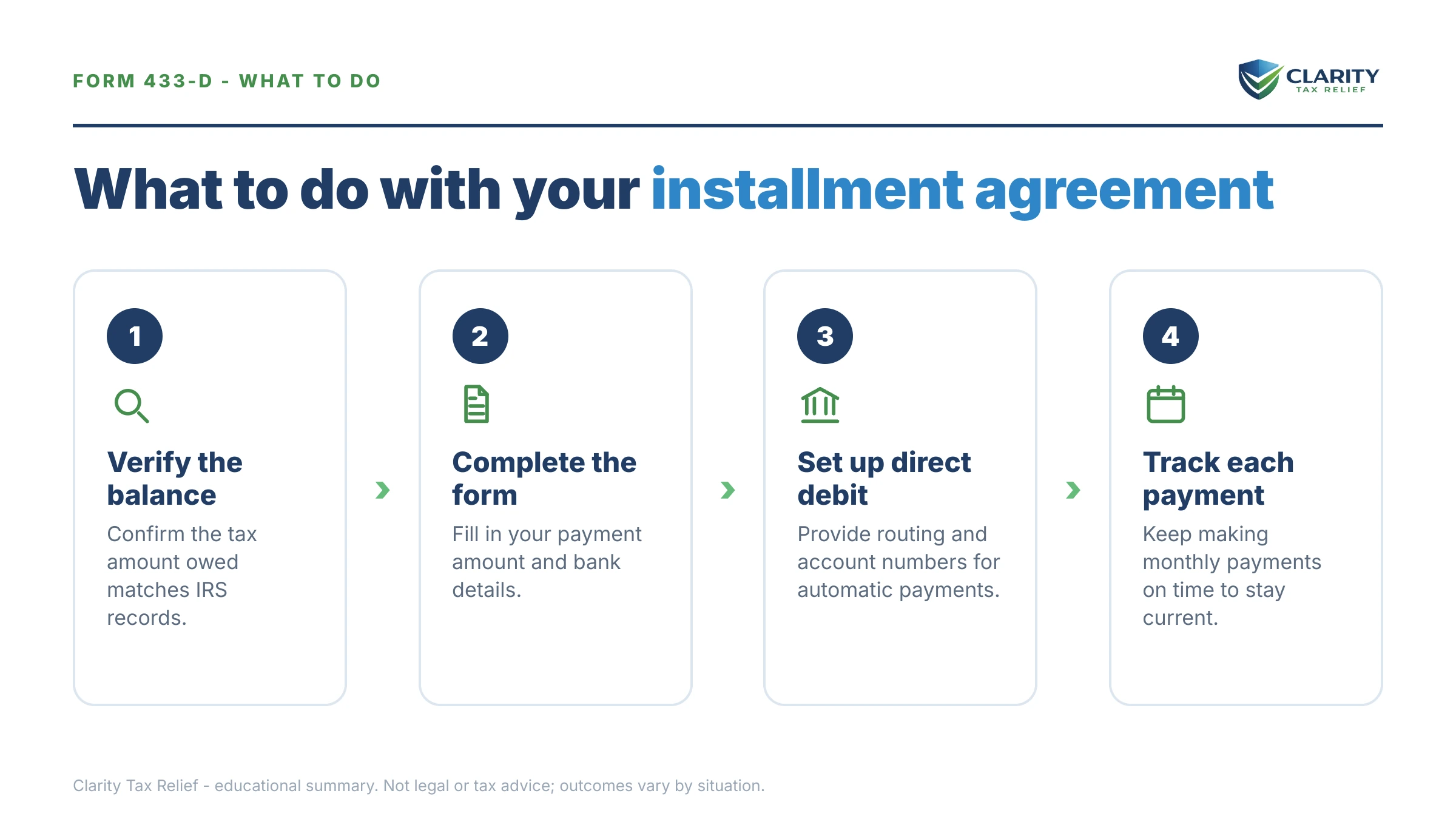

- Confirm the terms are right. Check the tax years, the total balance, the monthly amount, and the due date against your own records and your IRS online account.

- Decide on direct debit. If you choose it, enter your bank routing and account numbers carefully — one wrong digit can bounce a payment and risk a default.

- Make sure the payment is realistic. Pick an amount and a date you can hold for the full life of the plan, not just the first month.

- Sign and date. Both spouses must sign on a joint liability. Your signature is what makes the agreement binding.

- Return it the way the letter says. Mail or fax to the address or number on your cover letter, or hand it to your revenue officer. Keep a signed copy.

- Verify it posted. A week or two later, log into your IRS online account or check the IRS payment plans page to confirm the agreement is active.

One more thing: while a plan is in place, the 10-year collection clock (the CSED) keeps running, but interest never stops. If your balance is large or you have unfiled years, the order you fix things in matters — sometimes penalty relief or a different program saves more than a long payment plan. A quick professional review can tell you which path costs you less.

Form 433-D questions, answered

What is the difference between Form 433-D and Form 9465?

Form 9465 is the request — you use it to ask the IRS for a payment plan. Form 433-D is the confirmation — the IRS uses it to lock in the terms once a plan is approved, including your monthly amount, due date, and bank info for direct debit. One asks, the other finalizes.

Do I have to use direct debit on Form 433-D?

Not always, but it's strongly encouraged. Direct debit installment agreements have lower setup fees, fewer missed payments, and are sometimes required if you owe between roughly $25,000 and $50,000. The form has a section for your bank routing and account numbers if you choose direct debit.

What happens if I miss a payment on my 433-D agreement?

One missed payment can put your agreement into default. The IRS usually sends a CP523 notice warning that the plan will terminate, which can restart collection and levy action. If money is tight, contact the IRS before you miss a payment to ask about lowering the amount or pausing collection.

Does Form 433-D require financial disclosure?

No. Form 433-D is just the agreement terms — it does not ask for your income, expenses, or assets. That detailed financial disclosure happens on a separate Collection Information Statement, like Form 433-F or Form 433-A, when the IRS needs to verify what you can afford.

Where do I send a signed Form 433-D?

Mail it to the IRS address or fax it to the number printed on the notice or letter you received with the form. If a revenue officer is handling your case, send it directly to them. Keep a signed copy for your records and confirm the agreement posted to your IRS online account.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.