IRS Forms

Form 9465 Instructions: How to Fill Out the IRS Installment Agreement Request (2026)

The short answer: Form 9465 asks the IRS for a monthly payment plan. List every year's balance on lines 5–7, propose at least the balance divided by 72 on line 11a if you owe $50,000 or less, choose direct debit on line 13 for the lowest fee, and attach Form 433-F only above $50,000.

You finished the return, the number at the bottom is bigger than anything you can write a check for, and your software just asked whether you want to "include Form 9465." Now you're staring at a two-page form where one line — the monthly payment you propose — could follow you for up to six years. The good news: these Form 9465 instructions come down to about four lines that actually matter, and once you know what the IRS expects on each one, the form is straightforward.

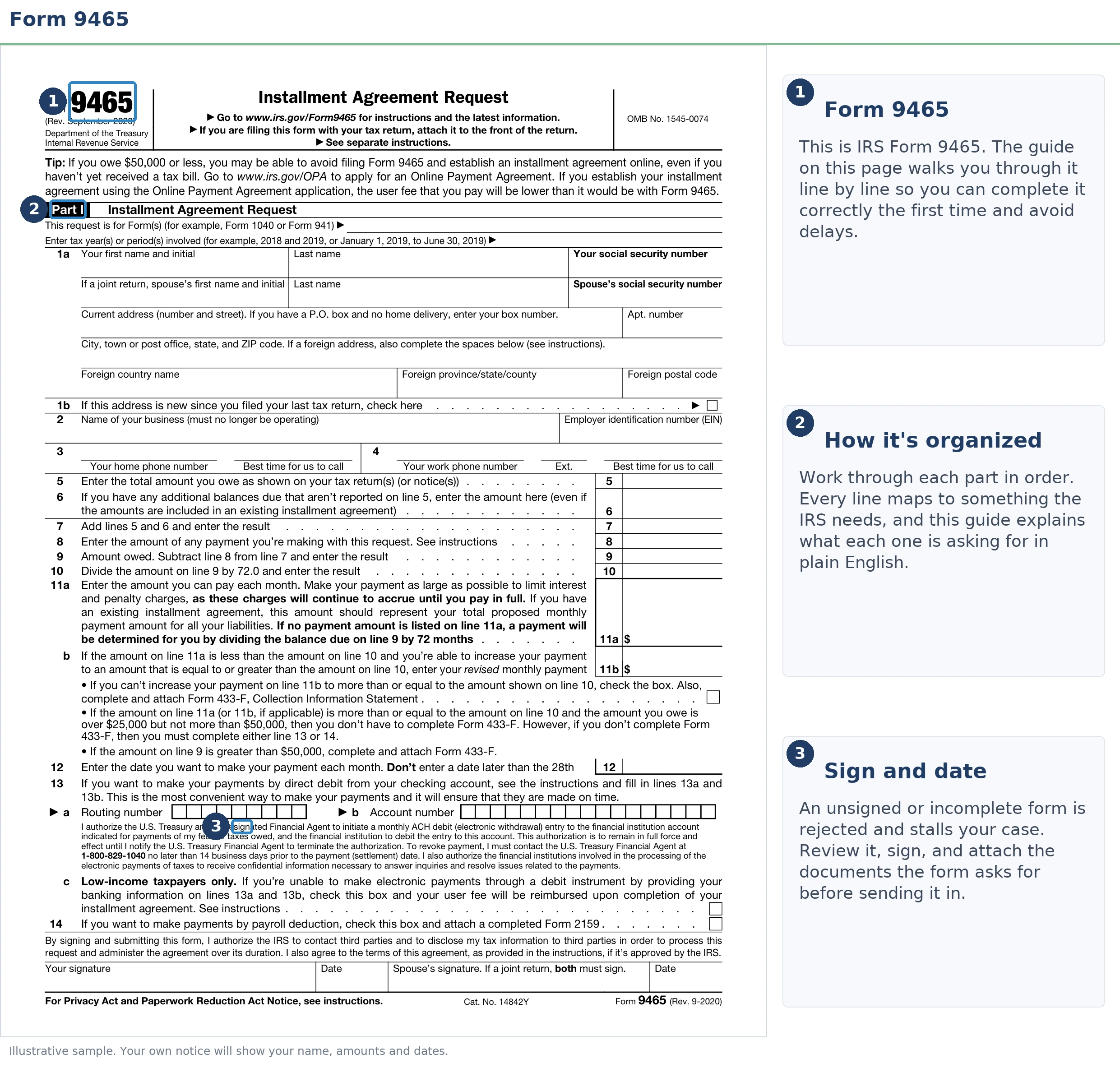

The image below shows exactly what Form 9465 looks like and where those decision lines sit on the page, so you can follow along with the form in front of you.

⏱ The real clock: Form 9465 has no filing deadline — but your balance does. The failure-to-pay penalty adds 0.5% of the unpaid balance every month, plus daily-compounding interest, until an agreement is in place. Once your plan is approved, that penalty rate is cut in half to 0.25% per month (for returns filed on time). Every month you wait costs real money.

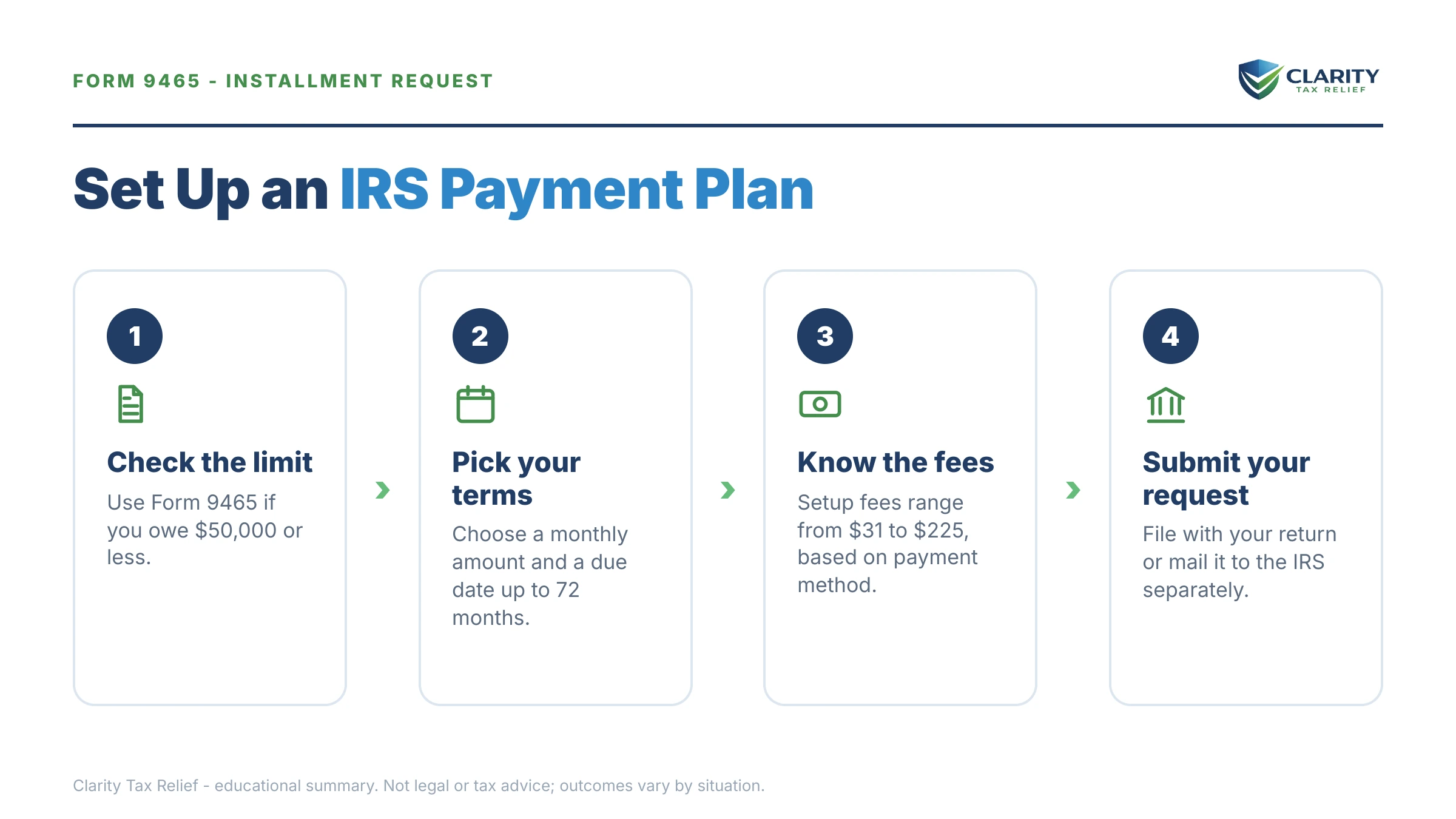

What Form 9465 does — and when you actually need the paper form

Form 9465 is the Installment Agreement Request: the IRS's official form for asking to pay a tax balance in monthly installments instead of all at once. It covers federal individual tax — Form 1040 balances, and in limited cases the tax of a business that has stopped operating. It does not cover state balances, and it is not the only way to request a plan.

Here's the part most guides bury: for most people who owe $50,000 or less, the paper form is the slowest and most expensive way to get the exact same agreement. The IRS Online Payment Agreement tool approves the same plan in minutes, at a lower setup fee, with no mail time. We walk through that route in our guide to setting up an IRS payment plan online, and cover what the form is at a higher level in our Form 9465 installment agreement request overview. This page is the line-by-line walkthrough for when the paper form is the right tool.

Form 9465 earns its place in five situations:

- You're filing a return with a balance due and want the plan request to travel with it — the form attaches to a mailed return or e-files with your software.

- You owe more than $50,000, which pushes you out of the standard online plan and into a request supported by Form 433-F financial disclosure — see what changes in an IRS payment plan over $50,000.

- You can't pass the online identity verification, or you simply can't get an IRS online account working.

- You want payroll deduction — payments taken from your paycheck via Form 2159, which the online tool doesn't set up.

- You're requesting a partial-payment arrangement that won't full-pay the debt before the collection statute runs — a partial payment installment agreement always requires financials and human review.

One scope note before the lines: Form 9465 is for individuals and sole proprietors. An operating business with payroll or income tax debt uses a different process with stricter rules — start with our guide to a business IRS installment agreement instead.

Form 9465 instructions, line by line (2026)

Part I of Form 9465 does almost all the work: it identifies you, totals what you owe, and states what you'll pay each month and how. The table below decodes each line; the paragraphs after it cover the four lines where people cost themselves money.

| Line | What it asks | How to answer |

|---|---|---|

| 1a | Name(s) and SSN(s) | Exactly as they appear on the return. On a joint balance, both spouses' names, SSNs, and signatures. |

| 2 | Business name and EIN | Only for a business that is no longer operating. Skip it otherwise. |

| 5–7 | What you owe | Line 5 is the balance from your return or notice; line 6 adds any other years; line 7 totals them. Every year you owe must be included. |

| 8 | Payment sent with the request | Anything you can spare. It shrinks the balance that accrues interest from day one. |

| 9 | Balance after that payment | Line 7 minus line 8 — the amount your plan will actually cover. |

| 10 | Line 9 divided by 72 | The working minimum monthly payment for balances of $50,000 or less. |

| 11a | Your proposed monthly payment | At or above line 10 if you owe $50,000 or less. Round up a few dollars so interest doesn't stretch the term. |

| 12 | Monthly payment date | Pick a day from the 1st through the 28th — ideally just after payday. |

| 13a–13b | Bank routing and account numbers | Completing these makes it a direct debit agreement — lowest fee, and no missed-payment risk. |

| 14 | Payroll deduction | Check it only if you want payments taken from your paycheck; attach Form 2159. |

Lines 5–7 are where requests quietly go wrong. If you owe for 2023 and 2024 but only list 2024, the plan won't cover the older year — and that year keeps moving through collections as if you never responded. Pull your IRS online account or your newest notice for each year and total everything before you fill in line 7.

Line 10 is the divide-by-72 rule. The IRS will generally accept a plan without any financial disclosure when the balance is $50,000 or less and the monthly payment full-pays it within 72 months. Divide line 9 by 72 and you have your floor. Propose less than that and you've converted a rubber-stamp request into one that needs financial review.

Line 11a is a commitment, not an opening bid. Don't propose the biggest number you can imagine on a good month — propose one you can hit every month, because a defaulted agreement puts you back in collections with a reinstatement fee on top. If the divide-by-72 amount itself is unaffordable, that's the signal to look at a partial-payment agreement or hardship status rather than overpromising.

Line 13 is the cheapest box on the form. Direct debit cuts the setup fee dramatically, removes the possibility of a forgotten payment, and — for balances between $25,001 and $50,000 — is what keeps the agreement "streamlined" without a lien determination. The trade-offs between bank-debit and paycheck withholding are covered in our direct debit installment agreement guide.

Part II (the second page) asks about your county, household, pay frequency, and income. You only complete it in narrow cases — most commonly when you've defaulted on an agreement in the past 12 months, or you owe between $25,000 and $50,000 and are proposing less than the divide-by-72 minimum. If you owe more than $50,000, Part II isn't enough: attach a full Form 433-F.

Two housekeeping items. First, married filing jointly means both spouses sign — an unsigned joint request bounces back weeks later. Second, if you're self-employed, the IRS expects your current-year estimated payments to stay on schedule; a new unpaid balance next April is one of the fastest ways to default the agreement you're setting up today.

What happens if you owe and never set up a plan

An unpaid balance with no agreement in place moves through the IRS's automated collection sequence, and each stage carries more enforcement power than the last:

- CP14 — the first bill, with roughly 21 days to pay or arrange something before the system escalates.

- CP501 / CP503 — reminder notices while penalties and daily interest keep compounding.

- CP504 — Notice of Intent to Levy: the IRS can now take your state tax refund, and a federal tax lien becomes a live possibility.

- LT11 / Letter 1058 — the final notice, starting a 30-day clock and your Collection Due Process rights; after it runs, wage and bank levies are on the table.

- Enforcement — a bank levy freezes funds for 21 days before they leave; a wage levy continues paycheck after paycheck until released. Balances over $66,000 (the 2026 threshold) also risk passport certification once collection escalates.

Filing Form 9465 interrupts this machine: a properly submitted installment-agreement request generally pauses levy action while the IRS considers it, and an approved agreement keeps enforcement off as long as you keep the terms. In 2026, with IRS staffing down roughly 27% but automated notices running uninterrupted, getting a request into the system is the difference between a managed debt and an escalating one.

Filling out Form 9465 right now?

The monthly payment you write on line 11a — and whether a lien determination comes with it — depends on numbers worth checking twice. An experienced tax professional will review your balance, your plan options, and your form for free before you commit, while penalties and interest are still compounding monthly.

Which installment agreement can Form 9465 get you?

Form 9465 is one form, but it can request four different kinds of agreement — and your balance on line 9 largely decides which one you get. The thresholds below are what separate a request the IRS approves almost automatically from one that triggers financial review and a lien determination.

| Agreement type | Balance threshold | Financial disclosure | Key terms |

|---|---|---|---|

| Guaranteed installment agreement | $10,000 or less (tax) | None | Approval is required by law if you've filed and paid on time the prior 5 years and can full-pay within 3 years. |

| Streamlined installment agreement | $25,000 or less — or up to $50,000 with direct debit or payroll deduction | None | Up to 72 months; no lien filing in the normal course. |

| Non-streamlined installment agreement | Over $50,000 | Form 433-F required | Payment set by ability to pay; lien determination is part of the review. |

| Partial payment installment agreement | Any balance | Form 433-F required | Pays less than the full debt before the 10-year collection statute expires; the IRS re-reviews your finances periodically. |

Notice the cliff at $50,000. At $50,000 you can have a 72-month plan with no financial disclosure and, typically, no lien. At $50,001 you're disclosing income, expenses, and assets on Form 433-F, and the IRS decides both your payment and whether to file a Notice of Federal Tax Lien. If you can realistically get below that line before filing, it changes everything about your request — the worked example below shows the math.

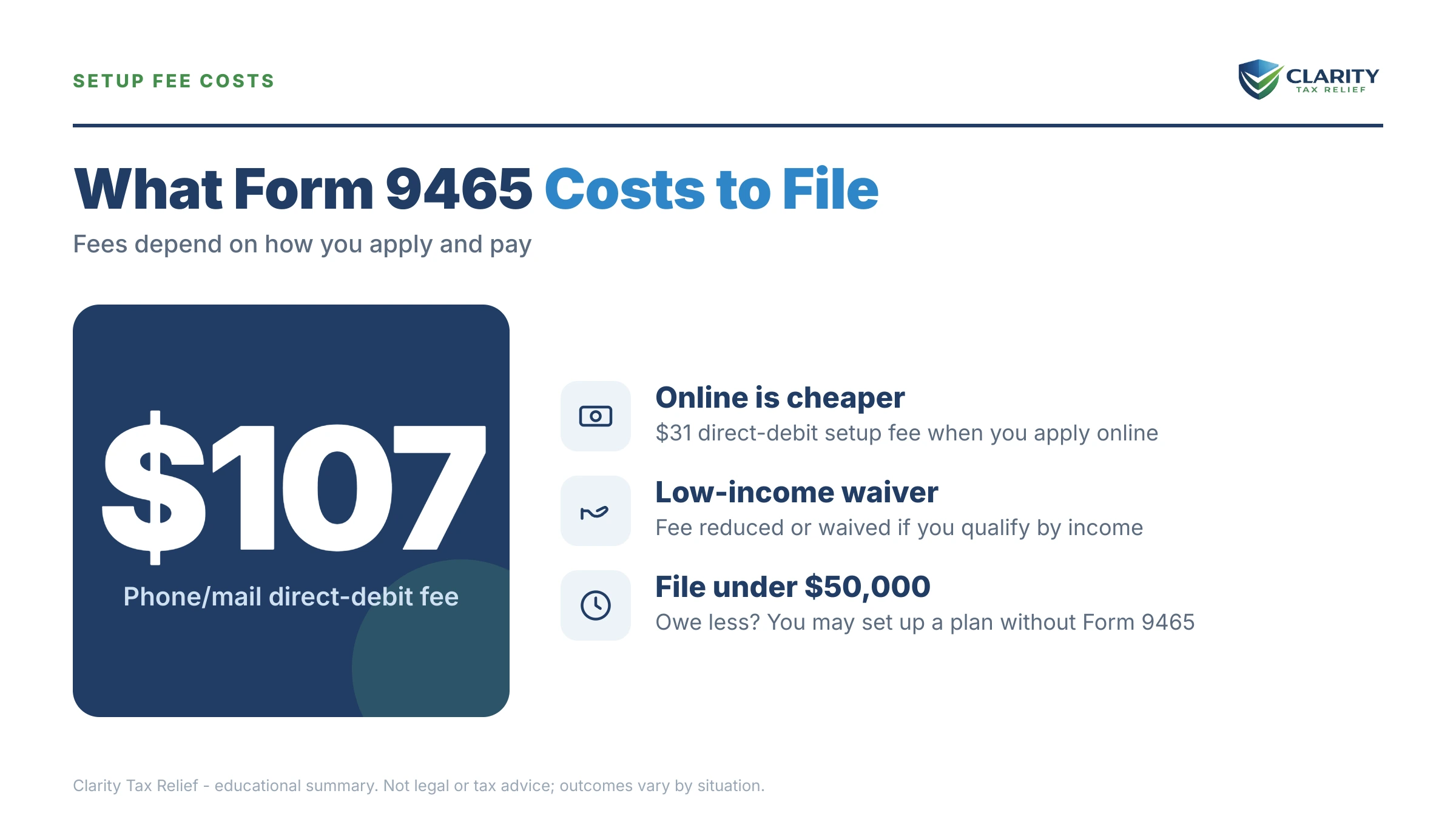

What Form 9465 costs: setup fees and the interest math

Filing Form 9465 on paper is the most expensive way to set up an IRS payment plan — the setup fee can run roughly five times what the same agreement costs online. The fee depends on two choices: how you apply and how you pay.

| How you apply | Direct debit | Check, card, or other |

|---|---|---|

| Online (Online Payment Agreement) | $22 | $69 |

| Form 9465 by mail, phone, or in person | $107 | $178 |

| Low-income taxpayers (Form 13844 certification) | Waived or reimbursed | Reduced fee, reimbursable in some cases |

User fees change periodically, so confirm the current schedule before filing — our guide to the IRS payment plan setup fee tracks the tiers and every waiver path, including the Form 13844 low-income application for paper filers.

The fee is the small cost. The bigger one is accrual: interest on unpaid tax runs at the federal short-term rate plus 3%, compounding daily, and the failure-to-pay penalty continues at 0.25% per month even while your agreement is active. Over a 72-month term that meaningfully raises the total you'll pay — which is why line 8 (pay something now) and a shorter self-imposed term both save real money. You can estimate what your own balance is accruing with our Penalty & Interest Calculator, and see how the rate is set in our guide to the installment agreement interest rate. If you get ahead later, there's no prepayment penalty — paying the plan off early stops the accrual cold.

Worked example: Form 9465 on an $83,100 balance — before a refinance

Say you owe $83,100 across two tax years, you own your home, and you're planning to refinance the mortgage next spring. This is exactly the situation where the $50,000 threshold — not the monthly payment — is the decision that matters. (This is a hypothetical to show the math, not a client story.)

Route A: file Form 9465 as-is at $83,100. The balance is over $50,000, so the form goes in with Form 433-F, the IRS sets your payment based on ability to pay, and a lien determination is part of the review. For scale, the divide-by-72 arithmetic would be $83,100 ÷ 72 ≈ $1,155 per month; if you sent $3,100 with the request (line 8), you'd propose against an $80,000 line 9 — at $1,400 a month that's about 57 months of principal, plus interest extending the tail. The problem for you isn't the payment. It's that a filed Notice of Federal Tax Lien is a public record your refinance underwriter will find, and it can stall or sink the loan — see what lenders actually do in can I refinance with an IRS lien. An $83,100 balance also sits above the $66,000 passport-certification threshold for 2026 if collection escalates.

Route B: get under $50,000 first, then file. If you can put $33,100 toward the debt — savings, a bonus, selling something, even a deliberate choice to borrow at a lower rate than the IRS charges — line 9 drops to $50,000. Now the math is $50,000 ÷ 72 = $694.44, so you'd propose $695 per month on line 11a with direct debit on line 13. No Form 433-F, no asset disclosure, and streamlined direct-debit agreements generally don't come with a lien filing. Your refinance file shows a payment plan in good standing instead of a public lien — and many lenders will work with exactly that, especially with a few months of on-time payments behind you.

The gap between those two routes is why running the numbers before filing matters. Route A locks in financial disclosure and lien risk; Route B costs $33,100 up front but protects a six-figure refinance. Which one is right depends on what you can actually raise, what your equity looks like, and how the 10-year collection statute falls on each year you owe — which is precisely the analysis worth getting a second set of eyes on.

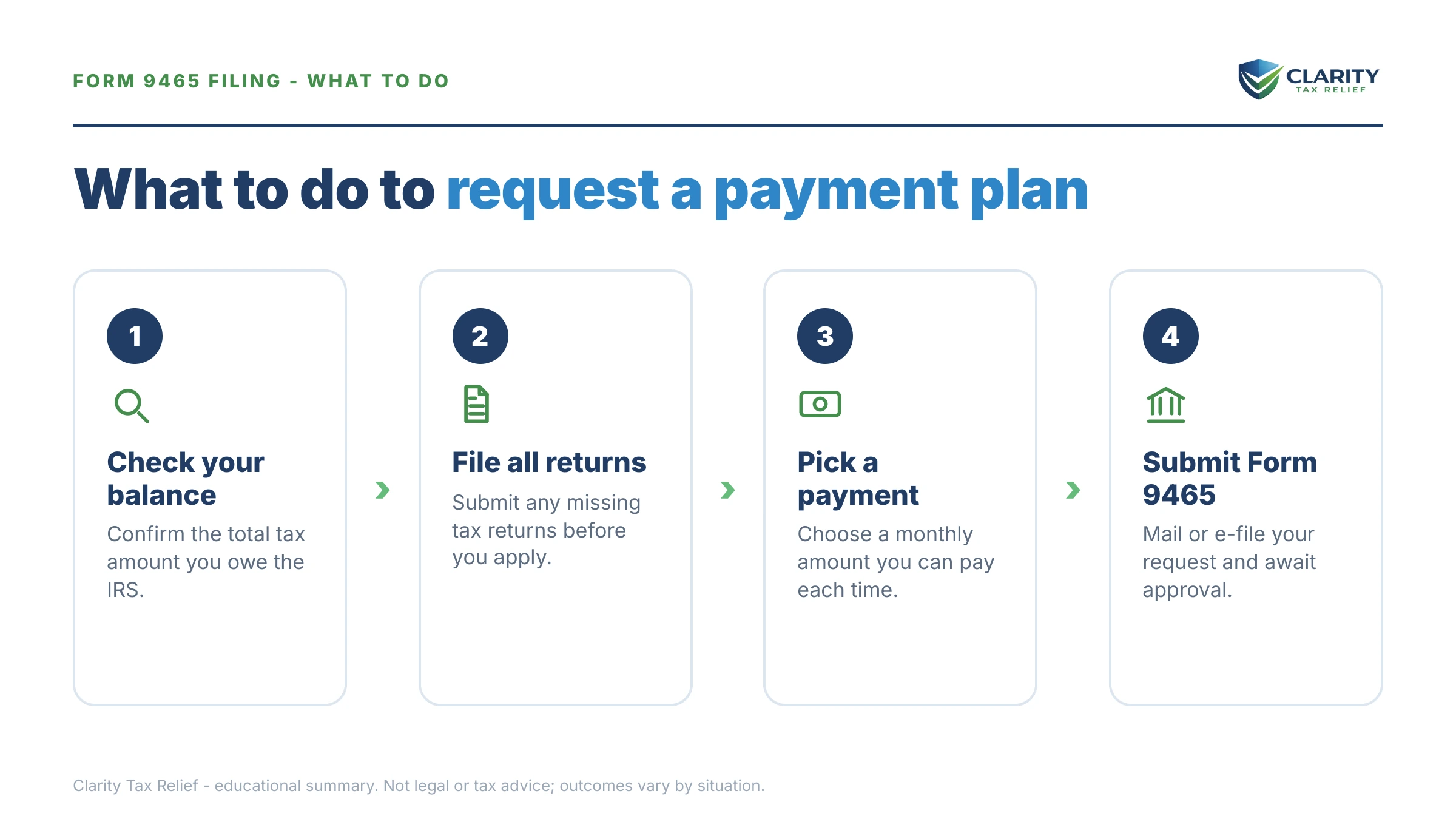

How to fill out and file Form 9465, step by step

- Pull your exact balance. Log into your IRS online account or gather the newest notice for every year you owe, and total them — every year must appear on lines 5 through 7.

- Decide your monthly number. Divide your balance by 72 (that's line 10); if you owe $50,000 or less, propose at least that amount on line 11a and round up a few dollars for interest.

- Complete Part I. Fill in names and SSNs exactly as they appear on your return, your balances, any payment sent with the request (line 8), a payment date from the 1st to the 28th (line 12), and your bank routing and account numbers for direct debit (line 13).

- Attach what your balance requires. Add Form 433-F if you owe more than $50,000 or you're proposing less than the divide-by-72 minimum, and Form 2159 if you chose payroll deduction on line 14.

- File it the right way. Attach Form 9465 to the front of a return you're mailing, e-file it with your return through your tax software, or mail it standalone to the state-specific address in the official IRS instructions.

- Confirm and calendar it. Watch for the IRS response letter (typically within about 30 days), sign and return Form 433-D if the IRS sends one, and set a reminder so the first payment never slips.

About that last step: some approvals arrive with Form 433-D, the agreement-confirmation form that finalizes direct debit terms — it isn't a rejection or a do-over, just the signature page of the deal you requested. And if a payment ever slips later, the warning shot is a CP523 notice; act inside the window printed on it and the agreement is usually salvageable.

When you can handle Form 9465 yourself

Honestly: much of the time, you don't need help with this form. If you owe $50,000 or less, agree with the balance, and can afford the divide-by-72 payment, Form 9465 — or better, the online tool — is a job you can finish today. A single year, a payment you're confident in, direct debit on line 13: file it and move on. The same goes for balances under $10,000 with a clean filing history, where approval of a guaranteed installment agreement is effectively automatic.

Experienced help changes the outcome in a narrower set of situations: balances over $50,000, where how your Form 433-F presents income and allowable expenses directly sets your payment and influences the lien decision; a refinance, sale, or security clearance where a lien filing has consequences far beyond the tax debt; multiple unfiled years that need to be filed in the right order before any agreement will stick; business or payroll tax in the mix; a defaulted prior agreement; or a balance large enough that a partial-payment agreement or an Offer in Compromise deserves a real comparison before you sign up to full-pay. In those cases, the strategy around the form is worth more than the form itself.

Not sure which side of that line you're on? Send us your balance and the years involved — a free review at the 2-minute form or (888) 825-7779 will tell you whether this is a do-it-yourself afternoon or a case worth building properly.

Terms on Form 9465, decoded

- Installment agreement — the IRS's formal name for a monthly payment plan; enforcement stops while it's in good standing, but interest doesn't.

- Streamlined installment agreement — a plan approved without financial disclosure because the balance is $50,000 or less and full-pays within 72 months.

- Direct debit installment agreement (DDIA) — a plan paid by automatic bank withdrawal; cheapest setup fee and required to keep $25,001–$50,000 balances streamlined.

- User fee — the one-time setup charge for the agreement, which varies by application method and can be waived or reimbursed for low-income taxpayers.

- Form 433-F — the Collection Information Statement listing your income, expenses, and assets; required with Form 9465 above $50,000 or for partial-payment requests.

- CSED — the Collection Statute Expiration Date, generally 10 years from assessment; it caps how long any agreement can run and shapes partial-payment math.

- Notice of Federal Tax Lien — the public filing that secures the government's claim against your property; generally avoided on streamlined direct-debit plans, likely considered above $50,000.

Official resources sit on the IRS site: the current form and its mailing addresses are on the IRS About Form 9465 page, and the full menu of plan types, fees, and online applications lives at the IRS payment plans and installment agreements page. Payments themselves — including the line 8 payment you send with the request — can be made at IRS.gov/payments.

Form 9465 questions people actually ask

Can I file Form 9465 online?

No — Form 9465 itself is filed on paper or attached to an e-filed return through your tax software. The online alternative is the IRS Online Payment Agreement tool, which most people who owe $50,000 or less should use instead: the setup fee is lower and approval is often instant instead of a roughly 30-day wait. Use the paper form when you can't pass the online identity check, you owe more than $50,000, or you're mailing a return anyway.

Where do I mail Form 9465?

It depends on how you're filing. If the form goes with your tax return, attach it to the front of the return and mail everything to your regular filing address. If you're sending Form 9465 by itself, the address varies by the state you live in and is listed in the official IRS instructions for the form. A misrouted request can add weeks, so check the current address before you mail it.

How long does the IRS take to approve Form 9465?

A standalone Form 9465 typically gets a written response within about 30 days. Requests attached to a return filed during the spring rush can take longer, and IRS staffing cuts have stretched paper processing times in 2026. While your request is pending, the IRS generally holds off on levy action, but interest and the late-payment penalty keep accruing until the balance is paid.

Do I have to attach Form 433-F to Form 9465?

Only in certain situations: your balance is over $50,000, you're asking for a partial-payment agreement that won't full-pay the debt, or the IRS specifically requests it. If you owe $50,000 or less and propose at least your balance divided by 72 each month, no financial statement is required. Skipping the disclosure is one of the biggest advantages of staying at or below the $50,000 line.

What is the minimum monthly payment on Form 9465?

For balances of $50,000 or less, the working minimum is your balance divided by 72 — that's what line 10 of the form calculates, and proposing at least that amount usually gets approval without financial disclosure. On an $18,000 balance, that's $250 a month. If you propose less than the divide-by-72 amount, the IRS will ask for financial information before deciding what you can actually afford.

Does an installment agreement stop penalties and interest?

No. Interest keeps compounding daily on the unpaid balance, and the failure-to-pay penalty continues — though it drops from 0.5% to 0.25% per month while an approved agreement is in effect, as long as you filed the return on time. An installment agreement stops enforcement, not accrual, which is why paying as much as you can up front on line 8 always saves money.

Will the IRS file a tax lien if I set up a payment plan with Form 9465?

Generally not on streamlined agreements — if you owe $50,000 or less and pay by direct debit or payroll deduction, the IRS usually doesn't file a Notice of Federal Tax Lien. Above $50,000, a lien determination is part of processing your request, and a filed lien becomes public record. If you're planning to refinance or sell property, that difference alone can justify paying a balance down below the threshold first.

Can a business use Form 9465?

Only in limited cases — Form 9465 is designed for individuals, including sole proprietors, and for owners of businesses that are no longer operating. An operating business that owes payroll or income tax uses different channels, with stricter rules because payroll taxes include employee trust-fund money. Line 2 of the form is where a defunct business's name and EIN go.

What happens if I miss a payment on my installment agreement?

One missed payment doesn't instantly kill the agreement — the IRS typically sends notice CP523, which states its intent to terminate and gives you a window, printed on the notice, to catch up or appeal before the agreement actually ends. If the agreement terminates, the full balance becomes collectible again and a reinstatement fee applies. Missing a payment, filing a return late, or leaving a new year's balance unpaid are the three most common ways agreements default.

Your next 24 hours

- Get your true total. Log into your IRS online account or pull the newest notice for every year you owe, and add them up — that single number decides whether you're in streamlined territory or facing Form 433-F and a lien determination.

- Gather three things: your last filed return, your bank routing and account numbers for line 13, and a realistic monthly figure you can pay every single month, not just the good ones.

- Get the numbers checked before you sign up for six years. A free case review — the 2-minute form or (888) 825-7779 — will confirm your line 11a payment, flag lien exposure if you're above $50,000, and tell you whether a cheaper route exists, while penalties and interest are still adding to the balance every month.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.