IRS Payment Plans

Direct Debit Installment Agreement: How It Works, What It Costs, and When It's Required (2026)

The short answer: a direct debit installment agreement (DDIA) is an IRS monthly payment plan that auto-withdraws from your bank account. It carries the lowest setup fee — $31 online — and is required for streamlined plans on balances between $25,001 and $50,000. Interest and a reduced 0.25% monthly penalty still accrue until payoff.

You're on the last screen of the IRS payment-plan application, and it's asking for your routing and account numbers. Handing the IRS a direct line into your checking account feels like a lot — especially if that account is brand new after a divorce and every dollar in it is already spoken for. Here's the good news: the authorization is narrower than it feels, the plan is cheaper than the alternatives, and this page maps exactly what you're agreeing to.

Direct debit is a payment method, not a different program — the debt, the interest, and the 10-year collection clock are the same either way. What changes is the fee you pay, the paperwork the IRS demands, and how hard it is to accidentally default. The image below shows exactly what the direct-debit setup looks like and which details deserve a second look before you commit.

⏱ The real clock: there's no letter deadline on this decision, but there is a running meter. Until an installment agreement is approved, the failure-to-pay penalty accrues at 0.5% of your balance per month; once your plan is in place, it drops to 0.25% — and interest compounds on top either way. Every month you wait costs real money.

What a direct debit installment agreement actually is

A direct debit installment agreement is an IRS payment plan where your monthly payment is pulled automatically from your checking account on a date you choose. You authorize it either inside the Online Payment Agreement application or on the banking section of Form 433-D, the installment agreement confirmation form.

The fear most people have — "the IRS can now take whatever it wants from my account" — is not how the authorization works. The debit authorization covers only the agreed payment amount on the agreed date, nothing more. If the IRS ever wanted more than that, it would have to go through the formal levy process, with its own required notices, which an active agreement prevents.

Once the plan is running, there's nothing to mail and nothing to remember. The withdrawals continue until the balance is paid in full or the collection statute expires, whichever comes first. For the general mechanics of applying — screens, verification, what the tool asks — see our walkthrough on how to set up an IRS payment plan online; this page covers what's specific to the direct-debit version.

Why the IRS pushes direct debit — and what you get in return

Direct debit cuts the IRS setup fee by $99 online and removes the single most common way payment plans fail: a forgotten payment. The IRS prefers agreements it doesn't have to babysit, so it prices and structures the rules to steer you toward auto-pay.

What you get for agreeing:

- The lowest fee tier. $31 online instead of $130 for the identical plan paid manually — and the fee is waived entirely for low-income applicants who set up direct debit online.

- Far lower default risk. Manual plans die from missed mail, forgotten due dates, and life getting busy. A debit that runs itself can't be forgotten — only underfunded.

- Lien protection in the $25,001–$50,000 band. Choosing direct debit there generally lets you avoid the financial-statement review and the lien-filing determination that come with other payment methods.

- A path to lien withdrawal. If a federal tax lien has already been filed and your balance is $25,000 or less, a direct debit agreement opens the door to requesting lien withdrawal on Form 12277 after three consecutive direct debit payments clear. Withdrawal erases the public notice — a meaningful difference if you're trying to rent, borrow, or rebuild after a divorce.

The trade-off is control. The money leaves on the schedule whether or not this was a good month, which is why choosing the right amount and debit date (covered below) matters more on a DDIA than on any other plan type.

When a direct debit installment agreement is required: the $25,000 and $50,000 rules

Direct debit is mandatory for streamlined installment agreements on individual balances between $25,001 and $50,000. Below that band it's a money-saving option; above it, the payment method stops being the gating issue and financial disclosure takes over.

| Total balance (tax + penalties + interest) | Is direct debit required? | What that gets you |

|---|---|---|

| $10,000 or less | No — optional | You likely fit the guaranteed installment agreement rules; approval is essentially procedural if your filings are current |

| $10,001–$25,000 | No, but it cuts your fee | Streamlined installment agreement with no financial statement; direct debit also opens the lien-withdrawal path |

| $25,001–$50,000 | Yes — direct debit or payroll deduction | Streamlined approval without Form 433-F, and typically without a lien-filing determination |

| Over $50,000 | No, but often smart | Financial disclosure is required regardless of payment method — see IRS payment plans over $50,000 |

Two edge cases worth knowing. First, the balance that matters is your total assessed balance across all years, not just the newest bill — two moderate years can push you over $25,000 together and trigger the direct-debit requirement. Second, businesses have their own version: an operating business with payroll tax debt can qualify for an express-type agreement, and direct debit is generally required in the upper part of that band — details in our guide to the business payroll tax payment plan.

What a direct debit installment agreement costs in 2026

A direct debit installment agreement carries the lowest setup fee the IRS charges: $31 when you apply online, under the current fee schedule. Here's the full grid, because the same plan can cost anywhere from $0 to $225 depending on how you apply and how you pay.

| How you apply | Direct debit fee | Non-direct-debit fee |

|---|---|---|

| Online (Online Payment Agreement tool) | $31 | $130 |

| Phone, mail, or in person | $107 | $225 |

| Low-income (AGI at or below 250% of the federal poverty level) | $0 online — fee waived | $43, reimbursable when you complete the plan |

The setup fee is a one-time cost — the real expense is time. Interest accrues at the federal short-term rate plus 3%, adjusted quarterly, and the failure-to-pay penalty runs at 0.25% per month while the agreement is active. Neither stops because you're on a plan; they stop when the balance reaches zero. You can estimate what your specific balance will add over the life of a plan with our IRS penalty and interest calculator.

Fee tiers occasionally change, so confirm before you apply — our breakdown of the IRS payment plan setup fee tracks the current schedule and every waiver.

Worked example: putting $19,700 on direct debit after a divorce

Say you're recently divorced and holding a $19,700 balance from the last joint return you filed with your ex. The divorce decree says the debt is theirs — but the IRS isn't bound by a decree, and it can collect the full joint balance from either of you (more on that in divorce and IRS debt: who pays). Until that's sorted out, a payment plan in your own name keeps enforcement off your paycheck. Here's the math, all of it hypothetical:

- Minimum payment: $19,700 ÷ 72 months = about $274/month. The online tool will accept any amount at or above that floor.

- Penalty savings from the plan itself: without an agreement, the failure-to-pay penalty on $19,700 is roughly $98 in month one (0.5%). With an approved agreement it's about $49 (0.25%). The agreement cuts your monthly penalty roughly in half from day one.

- Fee savings from choosing direct debit: $31 online instead of $130 — $99 kept in your pocket for entering a routing number.

- Paying more than the minimum: at $274/month, interest and penalty stretch the payoff toward the full six years. Push the debit to $450–$475/month and you're done in roughly four years, with meaningfully less interest paid — there's no penalty for paying it down faster.

One divorce-specific note: any tax refund you're owed while the plan runs will be offset against the balance — the debit still happens, but the refund shortens the payoff. If that stings because the underlying debt was your ex's income, that's exactly the fact pattern where innocent spouse relief is worth exploring before you accept the whole balance as yours. See will the IRS take my refund on a payment plan for how the offset works.

What happens if a direct debit payment fails

One returned direct debit payment does not automatically terminate your installment agreement — but a pattern of them will, and the sequence from bounce to levy is automated. Here's the order it unfolds in:

- The debit is returned. Your bank may charge its own fee, and the IRS can add a dishonored-payment penalty — generally 2% of the payment for payments of $1,250 or more, a small flat amount below that.

- The IRS flags the account. A single returned payment usually draws a notice rather than termination. What to do in that window is covered in missed IRS payment plan payment — the short version is: call before the IRS does.

- CP523 arrives. Repeated failures — or a new unpaid balance on a later return — trigger the CP523 notice, the IRS's intent to terminate the agreement. You typically have about 30 days to cure the default or appeal before termination takes effect.

- The agreement terminates. The full remaining balance becomes collectible at once, the failure-to-pay penalty snaps back from 0.25% to 0.5% per month, and reinstating the plan means a reinstatement fee and, sometimes, new terms.

- Collection restarts. The notice ladder resumes toward a final notice of intent to levy; once that notice ages 30 days, wage and bank levies become legal. Everything you avoided by setting up the plan comes back — with a bigger balance.

The practical takeaway: the danger point for a DDIA isn't forgetting — it's an underfunded or closed account. If you know a debit will fail, call the IRS before the withdrawal date. A revision requested in advance almost always beats a default cured afterward.

On a plan that's slipping — or not sure direct debit is the right move?

Every month without a working agreement adds another 0.5% penalty plus interest to your balance. An experienced tax professional will review your balance, your notices, and your options free — before another month posts.

Direct debit vs. payroll deduction vs. paying manually

The IRS accepts three delivery methods for installment agreement payments: direct debit from your bank, payroll deduction through your employer, and manual payments you send yourself each month. In the $25,001–$50,000 band you must pick one of the first two; everywhere else, the choice is yours.

| Feature | Direct debit | Payroll deduction | Manual payments |

|---|---|---|---|

| Setup paperwork | Online tool or the banking section of Form 433-D | Form 2159, which your employer must sign | Online tool or Form 9465; no bank authorization |

| Who sends the payment | Your bank, automatically | Your employer, each pay period | You, every single month |

| Lowest available setup fee | $31 (online) | Standard non-online fee applies — Form 2159 is a paper process | $130 (online) |

| Employer involvement | None — fully private | Required — your employer knows about the tax debt | None |

| Biggest failure risk | A closed or short account bounces the debit | A job change breaks the payment chain | A forgotten payment starts the default sequence |

| Lien-withdrawal path (balances ≤ $25,000) | Yes — after 3 consecutive payments | No — direct debit only | No |

Payroll deduction earns its keep in one situation: you need the $25,001–$50,000 streamlined treatment but genuinely can't run a bank account reliably. Its costs are privacy — your employer sees and administers your IRS debt — and fragility, since changing jobs interrupts payments through no fault of your own. For most people who qualify for either, direct debit wins on fee, privacy, and durability.

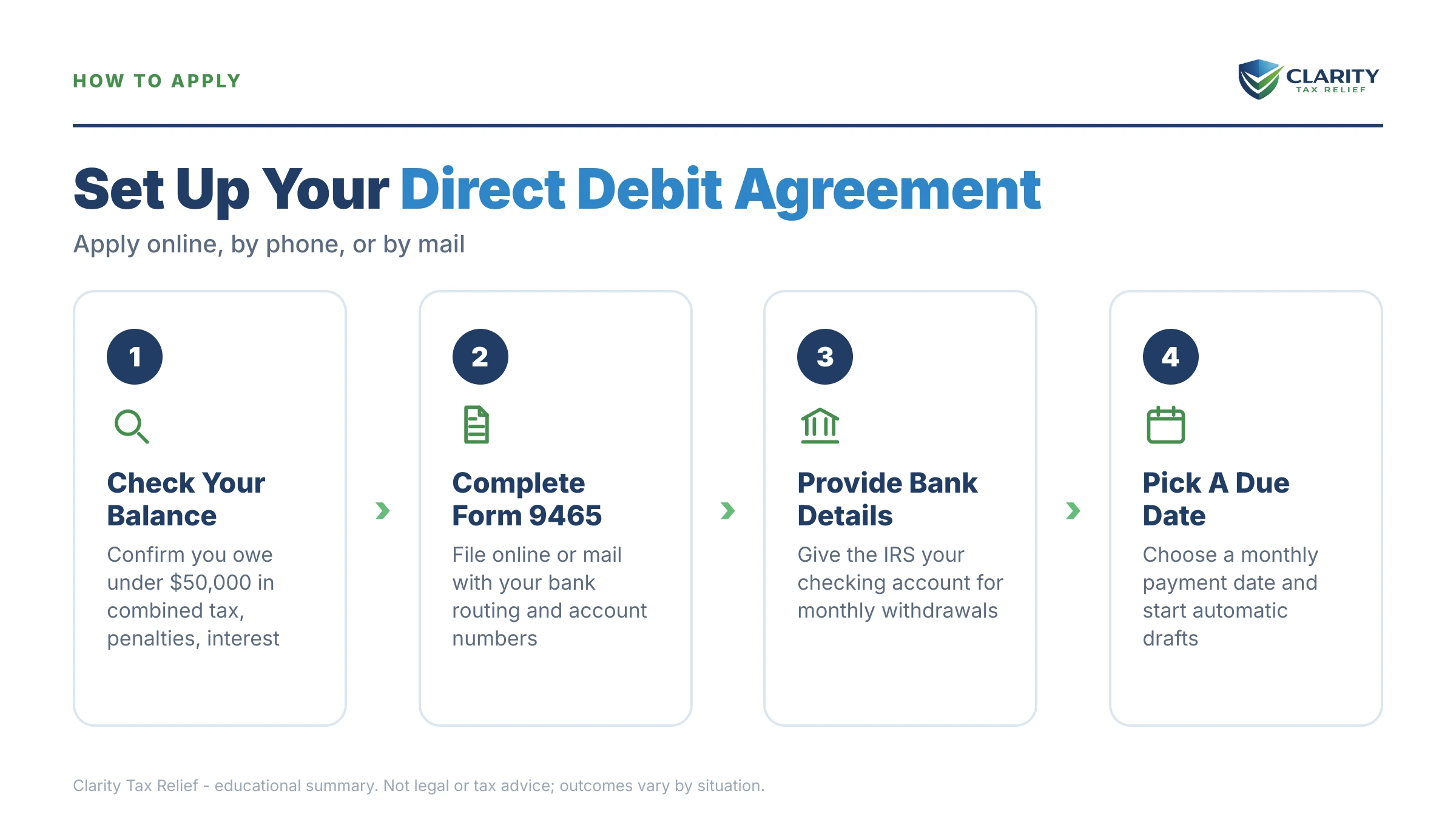

How to set up a direct debit installment agreement, step by step

Most direct debit installment agreements for balances under $50,000 can be approved online in one sitting.

- File every required return. The IRS will not approve any installment agreement while returns are missing — file them first, even if you can't pay what they show.

- Gather your banking and identity details. You'll need your routing and account numbers, your most recent tax return, and access to your IRS online account to verify your total balance.

- Apply through the IRS Online Payment Agreement tool. Balances of $50,000 or less usually get an instant decision online; if you can't apply online, mail Form 9465 with the direct-debit section of Form 433-D completed.

- Choose a payment of at least your balance divided by 72. Pick a debit date a few days after payday so the money is always there, and commit to more than the minimum if you can.

- Confirm the first withdrawal and stay compliant. Watch your bank account for the first debit, keep a cushion in the account, and file and pay every future return on time — a new balance can default the agreement.

That last step is the one that quietly kills more agreements than bounced debits do: owing again next April is itself a default event. If your withholding or estimated payments caused this balance, fix them the same week you set up the plan.

Changing banks, amounts, or debit dates on an existing agreement

You can change the bank account, monthly amount, or debit date on an existing direct debit installment agreement without starting the plan over. The Online Payment Agreement tool handles most revisions to individual plans; anything it won't accept, you can request by phone at the number on your most recent notice.

The sequencing matters, especially after a divorce, when the account being debited is often a joint account you're about to close. Never close the debited account until the IRS confirms the new one — a debit that hits a closed account is a returned payment, with the penalty and default exposure that come with it. Update first, confirm, then close.

If the payment itself has become unaffordable — new rent, one income instead of two — you can ask to restructure rather than letting it fail; our guide to lowering an existing IRS payment plan walks through when the IRS says yes. And if you come into money — a house sale, a settlement — extra payments are always allowed and always help, since interest runs until the last dollar posts.

When you can handle this yourself — and when help changes the outcome

You do not need professional help to set up a direct debit installment agreement on a single tax year under $50,000 that you agree you owe. If your returns are filed, the online tool works, and the minimum payment fits your budget, do it yourself this week — the whole process takes less than an hour and the $31 fee is the entire cost.

Experienced help changes outcomes in a narrower set of situations:

- The balance is over $50,000, where the financial statement determines your payment — and how expenses are presented can swing that number substantially.

- A levy or garnishment is already in motion, where the order of operations (release first, agreement second) matters and days count.

- Multiple years are unfiled, because the agreement can't exist until the returns do — and filing order affects penalties.

- The debt is joint and the divorce is fresh — innocent spouse or separation-of-liability relief might remove part of the balance entirely, and it's better raised before you've quietly paid the debt down for two years.

- A plan already defaulted, where reinstatement terms are negotiable and a rushed acceptance can lock in a payment you still can't afford.

- The payment the IRS wants would break your budget — sometimes hardship status or a partial-pay arrangement fits better than any full-pay plan, and that comparison is worth making before you sign.

If none of those describe you, skip the fee and set it up yourself. That honesty is the same thing we'd tell you on the phone.

Terms on your agreement, decoded

- DDIA: IRS shorthand for direct debit installment agreement — a payment plan funded by automatic bank withdrawals.

- Form 433-D: the one-page agreement confirmation where your terms and bank routing/account numbers are recorded.

- Streamlined installment agreement: a plan approved on thresholds alone, with no financial statement — up to $25,000 by any payment method, up to $50,000 with direct debit.

- CP523: the notice that your agreement is in default and the IRS intends to terminate it — the last cheap moment to fix a broken plan.

- Failure-to-pay penalty: the monthly late-payment charge — 0.5% of the balance normally, cut to 0.25% while an approved agreement is active.

- CSED: the Collection Statute Expiration Date — the end of the IRS's 10-year window to collect, though certain events pause that clock.

Dealing with a defaulted plan, a balance the online tool rejects, or a joint debt you're not sure is yours? A free case review with an experienced tax professional can map the fix before another month of penalties and interest posts.

Direct debit installment agreement questions, answered

Is a direct debit installment agreement required?

Only in specific situations. Individuals owing between $25,001 and $50,000 must agree to direct debit (or payroll deduction) to qualify for a streamlined plan without filing a financial statement. Below $25,000 it's optional but cheaper, and above $50,000 the IRS requires full financial disclosure no matter how you choose to pay.

What happens if my direct debit payment bounces?

One returned payment doesn't automatically end your plan. Your bank may charge you, the IRS can add a dishonored-payment penalty, and if the problem repeats you'll get a CP523 notice of intent to terminate — typically giving you about 30 days to fix it. Call the IRS as soon as you know a payment will fail; a proactive call usually preserves the agreement.

Can I change the bank account on my direct debit installment agreement?

Yes. You can update your banking information through the IRS Online Payment Agreement tool or by calling the number on your notice — allow time before the next scheduled debit for the change to take effect. This matters most after a divorce: never close the account being debited until the IRS confirms the new one, or the payment will bounce.

Can I skip a month on a direct debit installment agreement?

There's no built-in skip feature — withdrawals continue automatically until the IRS changes the agreement. If you can't cover an upcoming debit, call the IRS before the withdrawal date and ask to revise the amount or date. Letting the payment bounce instead risks a dishonored-payment penalty and starts the path toward default.

Does a direct debit installment agreement stop penalties and interest?

No, but it cuts the penalty in half. While an approved installment agreement is in effect, the failure-to-pay penalty drops from 0.5% to 0.25% of the balance per month, and interest continues at the federal short-term rate plus 3%, adjusted quarterly. That's why paying more than the minimum, whenever you can, saves real money.

Will the IRS take my tax refund while I'm on a direct debit installment agreement?

Yes. Being current on a payment plan does not stop refund offsets — the IRS applies any refund you're owed against your remaining balance until it's paid off. The offset doesn't replace your monthly debit; the scheduled withdrawal still happens. The upside is that every offset shortens your payoff.

Can direct debit get a tax lien withdrawn?

It can, in a specific window. If your total balance is $25,000 or less and you're on (or convert to) a direct debit installment agreement, you can request lien withdrawal on Form 12277 after three consecutive direct debit payments have cleared. Withdrawal removes the public notice of the lien — but if you default afterward, the IRS can file again.

How long does approval of a direct debit installment agreement take?

Online applications for streamlined balances typically get an immediate answer, and your first withdrawal is scheduled from the banking details you enter during setup. Paper requests on Form 9465 with Form 433-D take longer — often several weeks in 2026 given reduced IRS staffing — and the IRS mails confirmation before any debit begins. Keep making voluntary payments while you wait so the balance grows more slowly.

Can I pay off a direct debit installment agreement early?

Yes, with no prepayment penalty. You can make extra payments any time through IRS Direct Pay or your online account on top of the scheduled debits, and interest stops the day the balance hits zero. Since interest and the 0.25% monthly penalty run until payoff, paying early is almost always worth it.

Your next 24 hours

- Confirm your true balance. Log into your IRS online account and add up every year with a balance — the $25,000 and $50,000 direct-debit thresholds apply to the total, not the newest bill.

- Gather three things: your bank routing and account numbers, your most recently filed return, and a realistic monthly number your budget can sustain every single month.

- Act on one path today. If your situation is simple, apply online and lock in the $31 fee and the halved penalty. If it isn't — joint debt from a divorce, a defaulted plan, unfiled years — get a free case review at the 2-minute form or (888) 825-7779 before another month of interest and penalty posts to the balance.

Primary sources: the IRS's own overview of payment plans and installment agreements, the official Form 9465, Installment Agreement Request page, and the Taxpayer Advocate Service for cases where normal channels stall.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.