IRS Payment Plans

Installment Agreement Interest Rate: The True Cost of Paying Over Time (2025)

The short answer: the IRS installment agreement interest rate is the federal short-term rate plus 3%, reset every quarter and compounded daily. On a plan, the late-payment penalty also drops from 0.5% to 0.25% per month. Interest never stops until the balance is paid in full.

Not sure a payment plan is your cheapest option?

Send us your notice and balance. An experienced tax professional will run the numbers — installment agreement, penalty relief, or another route — and tell you what fits your situation. Free, confidential, no pressure.

⏱ Timing matters: interest compounds daily, so every day you wait adds cost. Setting up a plan before the IRS files a final levy notice also keeps the lower 0.25% monthly penalty and protects you from enforcement. There is no penalty for paying off your balance early.

How the installment agreement interest rate works

When you owe the IRS and pay over time on an installment agreement (a monthly payment plan), the balance keeps growing two ways: interest and penalty. The installment agreement interest rate is not a fixed number the IRS picks. By law it equals the federal short-term rate plus 3 percentage points for individual taxpayers, and the IRS resets it every quarter. You can confirm the current figure on the IRS page for quarterly interest rates.

Two details make this rate sting more than it looks:

- It compounds daily. You pay interest on your tax, then interest on that interest. A balance left alone grows faster each month.

- It can change every quarter. The rate can rise in January, April, July, or October, so the cost of your plan is a moving target.

For a deeper look at how the math snowballs, see our guide on how IRS interest actually compounds.

The penalty cut you get on a plan

Here is the part the IRS doesn't advertise loudly. Normally the failure-to-pay penalty is 0.5% of the unpaid balance per month. Once you have an approved installment agreement in place, that penalty is cut in half — to 0.25% per month — for any month the plan is active. The details are on the IRS payment plans page.

So a plan does two helpful things: it stops collection enforcement, and it lowers your monthly penalty. What it does not do is stop interest. Interest keeps running daily until you reach zero.

A worked example: the real cost of paying over time

Say you owe $20,000 and set up a 72-month streamlined installment agreement. Assume an interest rate around 8% per year (this changes quarterly — check the current figure) plus the reduced 0.25% monthly penalty.

- Roughly the first year of interest alone on $20,000 at 8% is about $1,600 — and that's before the penalty.

- The 0.25% monthly penalty on $20,000 starts near $50 a month, shrinking as you pay the balance down.

- Stretch the full balance over six years and the total interest and penalty you pay can add several thousand dollars on top of the original $20,000.

The lesson isn't "never use a plan." A plan is often the smart, affordable choice. The lesson is that the longer you take, the more you pay — so pay as much as you can, as fast as you can.

What happens if you ignore the balance instead

Skipping a plan doesn't make the cost go away — it makes it worse and adds enforcement. Without an agreement, the higher 0.5% monthly penalty applies, and the automated collection sequence keeps moving:

- CP14 — first bill. Penalty runs at the full 0.5% per month.

- CP501 / CP503 — reminders. Interest and penalty keep compounding.

- CP504 — Notice of Intent to Levy. Your state refund can be seized.

- LT11 / Letter 1058 — Final Notice. After 30 days, wage garnishment and bank levies become possible.

An installment agreement set up early keeps you out of this entire chain — at the lower penalty rate.

Ways to lower the true cost

You can't usually get the interest rate itself waived, because the law requires the IRS to charge it. But you have real levers to pull:

- Pay faster. Send extra whenever you can. There's no early-payoff penalty, and every early dollar cuts future daily interest. See the best ways to pay the IRS compared.

- Use direct debit. A direct-debit installment agreement carries a lower setup fee and prevents accidental defaults that reset your costs.

- Attack the penalties, not the interest. First-time abatement or reasonable-cause relief can remove penalties — and a smaller balance means less interest. Read our guide to first-time penalty abatement.

- Pick the right plan. For balances under $50,000, a streamlined installment agreement is simple to set up over up to 72 months. If you truly can't afford the minimum, a partial-pay plan or hardship status may fit better.

- Compare a loan. If you can borrow at a lower true annual cost than the IRS rate plus penalty, paying in full and repaying a lender may cost less. Never use credit-card rates to do it.

How to set up and minimize an installment agreement, step by step

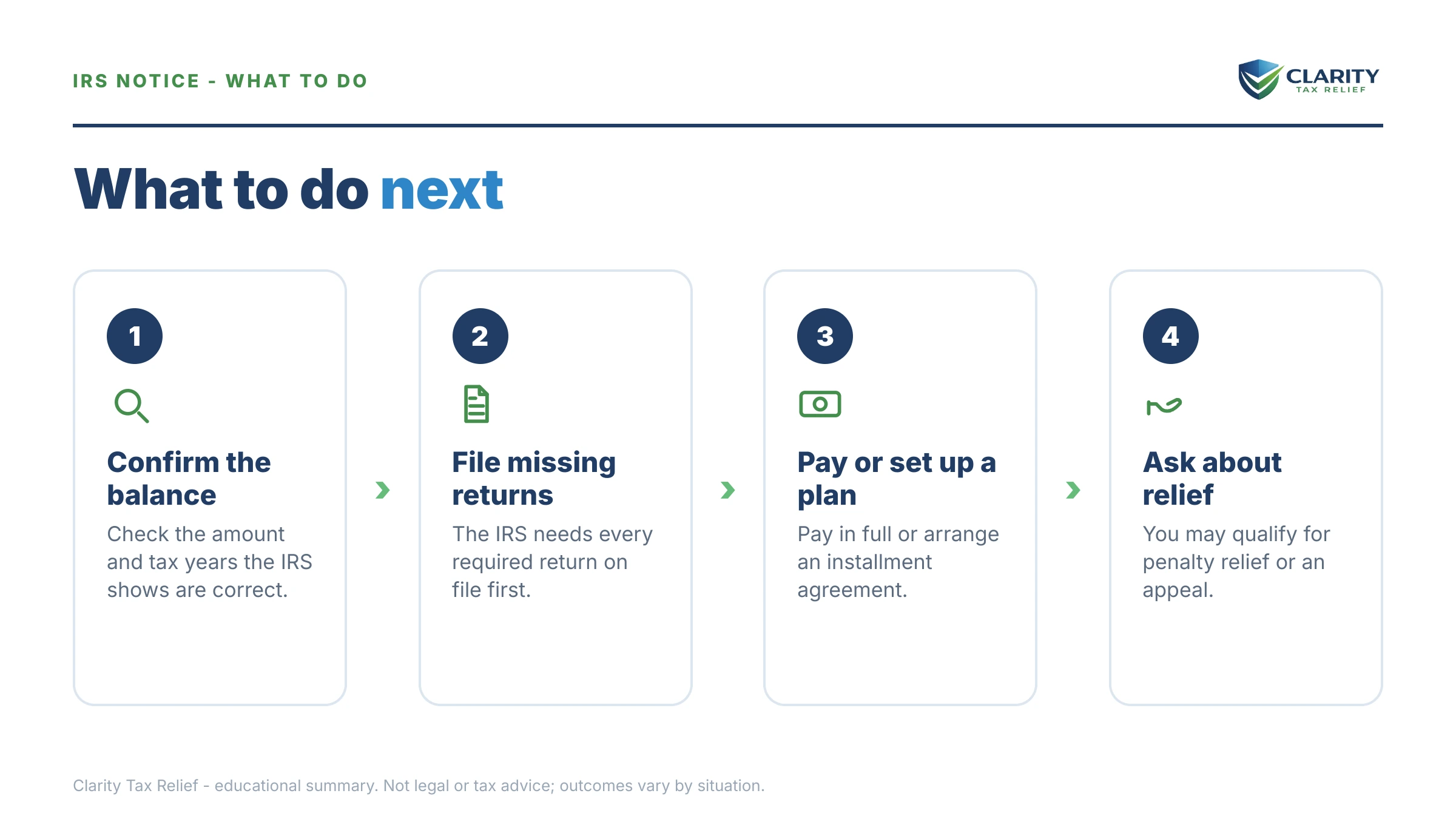

- Confirm what you owe in your IRS online account, including the tax, penalties, and interest split.

- File any missing returns first. The IRS won't approve a plan while returns are unfiled.

- Choose the shortest term you can afford. A higher monthly payment over fewer months saves the most interest.

- Set it up online using our walkthrough on setting up an IRS payment plan online, and select direct debit for the lower fee.

- Ask about penalty relief before or after setup — removing penalties shrinks the base that interest grows on.

- Pay extra whenever possible to beat the daily compounding.

Installment agreement interest questions, answered

Does interest stop when I'm on an IRS installment agreement?

No. Interest keeps adding up every day until the balance hits zero, even while you make on-time monthly payments. What does change is the late-payment penalty: on most installment agreements it drops from 0.5% per month to 0.25% per month. So a plan slows the bleeding but doesn't stop interest.

How is the IRS installment agreement interest rate set?

The IRS interest rate is the federal short-term rate plus 3 percentage points for individuals. It is set every quarter, so the rate on your balance can change in January, April, July, and October. Interest compounds daily, which means you pay interest on prior interest.

Can I get the installment agreement interest rate waived or lowered?

Interest is almost never waived, because the law requires the IRS to charge it. It can only be reduced or removed if it was caused by an IRS error or delay. Penalties are different — first-time abatement or reasonable-cause relief can remove penalties, which lowers the balance that interest is calculated on.

Is it cheaper to pay the IRS with a loan instead of an installment agreement?

Sometimes. If you can borrow at a lower rate than the combined IRS interest and 0.25% monthly penalty, paying the IRS in full with a loan and repaying the lender can cost less overall. Compare the true annual cost of both before deciding, and never borrow at credit-card rates to do it.

How do I pay off my installment agreement faster to save on interest?

You can pay more than the minimum or pay extra lump sums at any time with no penalty. Because interest compounds daily on the remaining balance, every extra dollar you send early saves you interest later. Setting up direct debit also lowers the setup fee and prevents accidental defaults.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. Interest rates and penalty figures change — confirm current numbers on IRS.gov.