IRS Payment Plans

IRS Payment Plan Defaulted: What Happens Now and How to Fix It (2026)

The short answer: if your IRS payment plan defaulted, the IRS sends notice CP523 and typically gives you 30 days from the notice date before the agreement terminates and levy powers return. Most defaulted plans can be reinstated — usually for an $89 fee ($43 low-income) — if you act inside that window.

You held up your end for months — the payments came out, the balance was shrinking — and now a letter says the deal is off. Maybe a payment bounced during a slow month, or a new tax year landed with a balance you couldn't cover. It's an unnerving letter to get, but a defaulted agreement is one of the most fixable problems in all of IRS collections — and fixing it cheaply is measured in days, not months.

This guide covers the whole path: why plans default, exactly what the IRS does next, what reinstatement costs, and how to keep the new agreement from failing the same way. Farther down, you'll also see exactly what a CP523 termination notice looks like and where the deadline sits on the page — many people read the wrong line first.

⏱ Your deadline: you typically have 30 days from the date printed on your CP523 notice before the IRS terminates your installment agreement. Cure the default or contact the IRS inside that window and the agreement stays alive; let it pass and the IRS begins moving toward enforcement. The dates printed on your notice control.

Why your IRS payment plan defaulted

An IRS installment agreement defaults when you break any condition of the agreement — a missed payment is only the most obvious of five triggers. The mechanics of how plans get set up and what they require live in our guide to how to set up an IRS payment plan online; here's what breaks them.

Missed or bounced payment. One skipped or returned payment can start the default process, though the IRS usually flags it first on your monthly CP521 statement and gives you a chance to catch up. If you're at this early stage, see our guide to a missed IRS payment plan payment — there's often still a cure window before any termination notice issues.

A new balance you didn't pay. Your agreement requires you to stay current on all future taxes. File this year's return with a balance you can't cover, and the existing plan defaults even if you never missed a monthly payment. This is the number-one trap for self-employed and 1099 workers, because no employer is withholding tax and skipped quarterlies come due all at once in April.

An unfiled required return. Not filing at all breaks the agreement the same way. If you set up a plan for one bad year and then stopped filing — say you're a 1099 worker who hasn't filed taxes in 3 years — the IRS treats those unfiled years as a broken condition, and it will not reinstate anything until they're filed.

You didn't send updated financials. Some agreements — especially partial-pay plans — come with periodic financial reviews. Ignore the request for an updated Form 433-F and the agreement can default with your payments still current.

A processing error. Occasionally a payment posts to the wrong tax year or a direct-debit change doesn't take, and the system reads it as a miss. These are the easiest defaults to fix — but only if you catch them and call.

| Default trigger | What actually happened | The fix |

|---|---|---|

| Missed or bounced payment | A monthly payment didn't arrive or was returned | Catch up the payment(s) before termination; switch to direct debit |

| New unpaid balance | A new return posted with tax you didn't pay | Ask the IRS to add the new year to the agreement (restructure) |

| Unfiled required return | A return the IRS expected never arrived | File every past-due return, then request reinstatement |

| No updated financials | You didn't respond to a financial review request | Submit Form 433-F and renegotiate the payment |

| Processing error | Payment posted to the wrong year or debit failed | Call with proof of payment and have the account corrected |

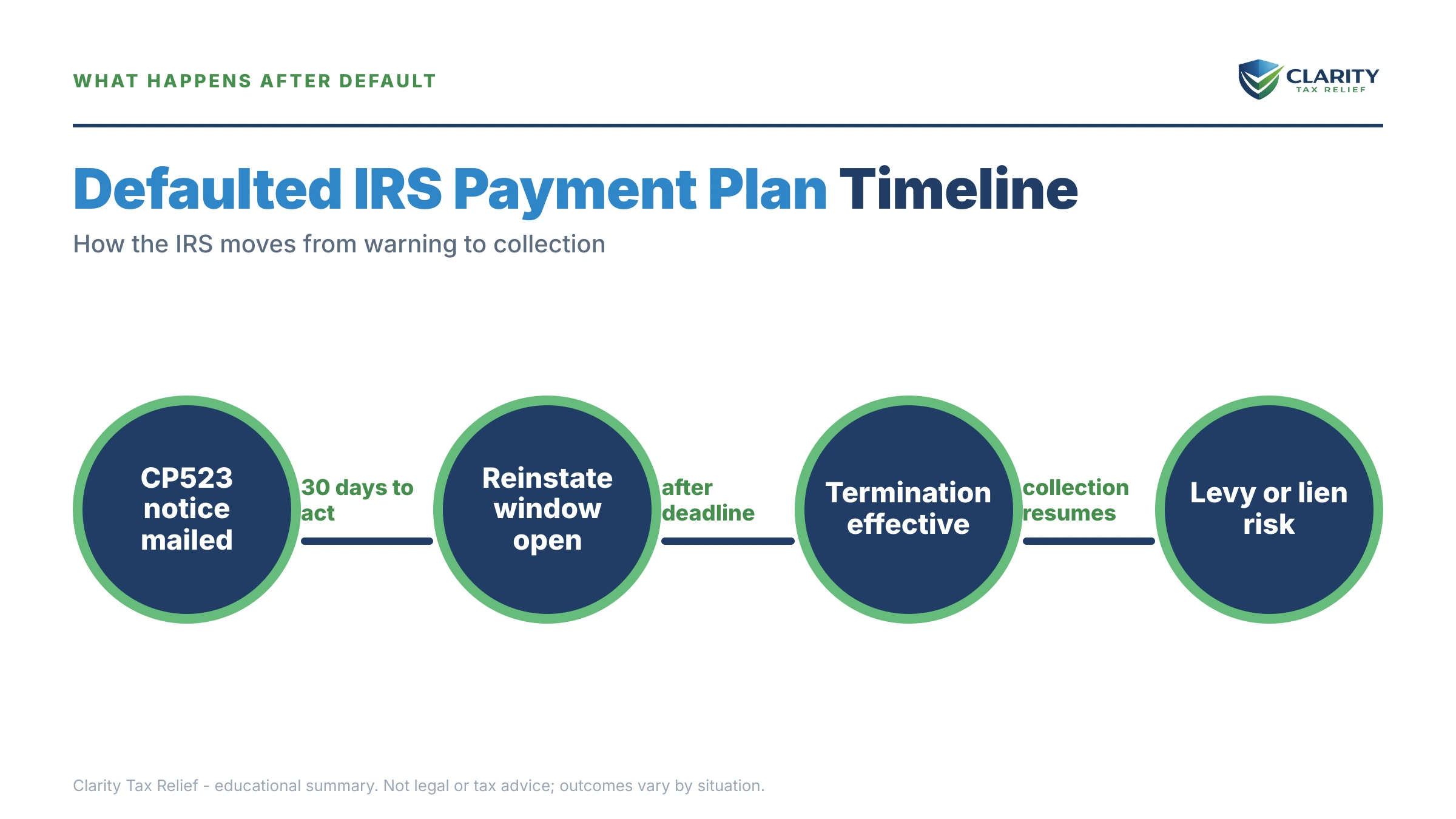

What happens if you ignore a defaulted installment agreement

A terminated installment agreement puts the IRS's full levy powers back on the table — bank accounts, wages, and 1099 income. The sequence from default to levy is automated, and each stage strips away a protection you have right now:

- Past-due flag. Your monthly CP521 (or a CP522 review letter) shows the account behind. Nothing is terminated yet — this is the cheapest moment to fix it.

- CP523 — intent to terminate. The formal default notice. You typically have 30 days from its date before the agreement dies; our full CP523 notice guide breaks down every line. While the window is open, levy protection generally remains in place.

- Termination. The agreement is dead. The failure-to-pay penalty jumps from the reduced 0.25% per month back to 0.5% per month, and the "in a valid agreement" exception that protects larger balances from passport certification (the threshold is $66,000 in 2026) disappears. You generally get 30 days from termination to appeal through the Collection Appeals Program (Form 9423) — see how a CAP appeal works — and the IRS is generally barred from levying while a timely appeal is pending.

- Final notice of intent to levy. For any tax period that never received one, the IRS must issue an LT11 notice or Letter 1058 before levying, which starts a 30-day clock and Collection Due Process rights via Form 12153. Important: if you already received a final notice before your plan was approved, the IRS doesn't have to send a new one — enforcement can move faster.

- Levy. A bank levy freezes funds for a 21-day hold before the money leaves; a wage levy is continuous until released; for gig and contract workers, the IRS can send one-time levies to platforms and clients that owe you money. Your state refund is also fair game.

One 2026 reality makes this timeline more dangerous, not less: the IRS workforce was cut roughly 27% in 2025, so reaching a human to negotiate takes longer — but the notices, terminations, and levies are generated by automated systems that never slowed down. The machine escalates on schedule whether or not anyone reads your file.

| Stage | Your window | What you keep — or lose |

|---|---|---|

| Past-due flag (CP521/CP522) | Until CP523 issues — no fixed window | Catch up now and there's no default at all |

| CP523 issued | Typically 30 days from the notice date | Cure or reinstate to keep the agreement and its levy protection |

| Termination date passes | Generally 30 days to file a CAP appeal (Form 9423) | Levy is generally barred while a timely appeal is pending |

| Final notice (LT11/1058), if required | 30 days | CDP hearing rights via Form 12153; miss it and levy can proceed |

| Levy issued | Bank: 21-day hold; wages: continuous | Only narrow release paths remain |

Holding a CP523 right now?

Get your defaulted payment plan reviewed free before the 30-day termination window printed on your notice closes. An experienced tax professional will map the fastest path back — reinstatement, restructure, or something better — in one call.

Your options after your IRS payment plan defaulted

Most defaulted IRS payment plans can be reinstated or restructured without starting collections from scratch — usually for $89 or less. Which route fits depends on why the plan failed and whether the old payment still matches your income:

| Option | Cost | Typical timeline | Best when |

|---|---|---|---|

| Cure before termination | The missed payments (about $10 if revising terms online) | Same day to a few weeks | CP523 just arrived and you can catch up |

| Reinstate after CP523/termination | $89 fee ($43 low-income) | One call, plus weeks for written confirmation | You can resume the old payment and all returns are filed |

| Restructure the agreement | About $10 online; $89 by phone/mail | Days to weeks | A new year's balance needs to be folded in, or the payment must drop |

| Partial-pay installment agreement | Setup fee plus Form 433-F disclosure | Weeks to months | You can't full-pay before the 10-year collection statute runs |

| Currently Not Collectible | $0, with financial proof | Weeks to months | Any payment would leave you unable to cover basic living costs |

| Offer in Compromise | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) | Months, up to 2 years | Your assets and future income genuinely can't cover the debt |

Reinstatement is the default path for a reason: it restores the exact protections you had, including the reduced 0.25% monthly failure-to-pay penalty. The IRS conditions it on compliance — every required return filed and current-year taxes being paid through withholding or estimates. The full process, including what to say on the call, is in our guide to how to reinstate an IRS payment plan.

Restructuring fits when the old plan no longer matches reality. If a new year's balance caused the default, ask to add it to the agreement rather than run two debts side by side. If the payment itself was the problem, you can often lower your IRS monthly payment — sometimes online for about $10, sometimes with a Form 433-F financial statement behind it. Note that fee tiers and online thresholds shift; the IRS payment plan changes for 2026 guide tracks what's current.

If you genuinely can't pay, don't force a plan that will default again. A partial payment installment agreement pays what your budget supports until the collection statute expires; Currently Not Collectible status pauses collection entirely during hardship (interest and penalties still accrue in both). An Offer in Compromise settles for less than you owe only when the IRS's own math shows it can't collect more — it accepted roughly 1 in 5 offers in FY2024, so treat it as a calculated application, not a promise.

Two edge cases change the playbook. If the defaulted plan covered business or payroll tax, thresholds and rules differ sharply — see the business IRS installment agreement guide. And a brand-new agreement (via Form 9465 or the IRS online tool at the official IRS payment plans page) is always available if reinstating the old one doesn't make sense.

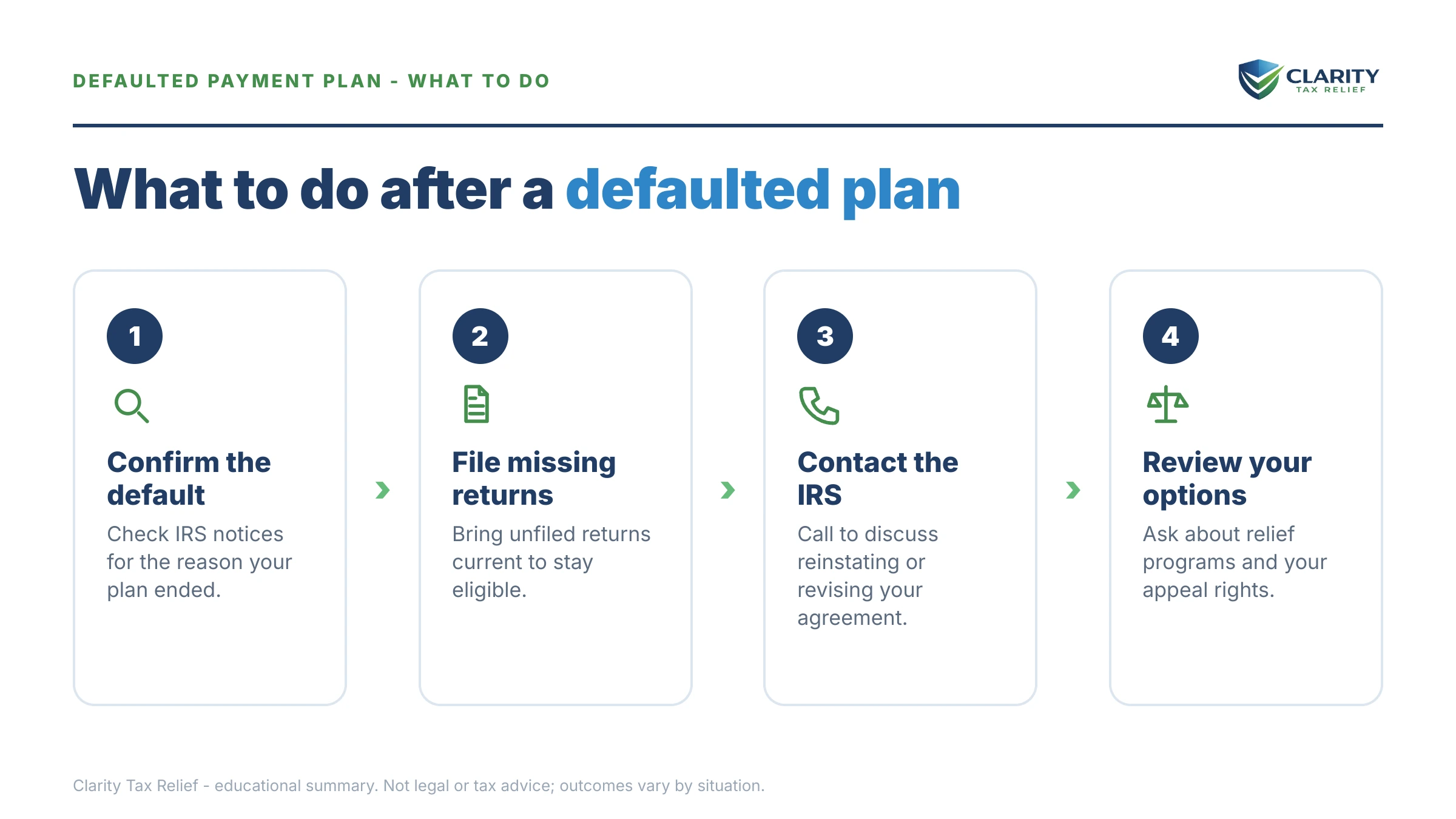

How to reinstate a defaulted IRS payment plan, step by step

- Find your dates. Locate the notice date and the termination deadline on your CP523 — the 30-day window runs from the notice date, not from the day you opened the envelope.

- File every missing return. The IRS will not reinstate a payment plan while required returns are unfiled, so getting past years filed comes before any phone call about the agreement.

- Call before the termination date. Contact the IRS at the number on your CP523 — or have your representative call — and ask to reinstate or restructure the agreement while it is still alive.

- Fix what caused the default. Catch up the missed payments, ask to add a new balance to the agreement, or request a lower payment backed by Form 433-F if the old amount no longer fits your income.

- Get the reinstatement confirmed. Pay the reinstatement fee, watch for the IRS's written confirmation, and verify in your IRS online account that the agreement shows as active again.

- Default-proof the new plan. Switch to direct debit and adjust your withholding or quarterly estimated payments so next year's return doesn't arrive with a balance that defaults the plan all over again.

Say you owe $41,800: what a default actually costs

Here's a clearly hypothetical example with the math shown. Say you're a gig worker whose plan covered one bad year, but three unfiled years defaulted it — and once those returns are filed, the total balance lands at $41,800.

The reinstated plan. At $41,800 you're still under the $50,000 line, so a plan spread over up to 72 months is on the table: $41,800 ÷ 72 ≈ $581 a month as a baseline, with the IRS setting the actual figure so the balance — plus accruing interest — is fully paid within the term.

The penalty spread. In default, the failure-to-pay penalty runs 0.5% per month: $41,800 × 0.005 ≈ $209/month. On a reinstated agreement it drops to 0.25%: about $105/month. Reinstatement alone saves roughly $104 a month in penalties — before you count avoiding a levy. Interest (the federal short-term rate plus 3%, compounding daily) accrues on top either way; you can estimate your own accrual with our IRS penalty and interest calculator.

The $50,000 trap. Left in default, penalties and interest on $41,800 grow by several hundred dollars a month. Within a couple of years, pure accrual could push the balance past $50,000 — the point where the streamlined online setup ends and the IRS starts demanding full financial disclosure. Acting now isn't just cheaper monthly; it preserves the easier program entirely.

If $581 doesn't fit. Gig income swings. If the number would just default again, a partial-pay agreement or CNC status based on your real budget beats a plan built on a good month. And if a strong season leaves you flush later, you can pay off an IRS payment plan early — interest stops when the balance hits zero, not on the last scheduled month.

When you can handle this yourself — and when help changes the outcome

Plenty of defaulted payment plans are a do-it-yourself fix. You likely don't need professional help when all four of these are true: the plan hasn't terminated yet, the cause was a single missed or bounced payment, every required return is filed, and you can resume the payments. One phone call, one fee, done.

Experienced help tends to change the outcome when the situation is layered: multiple unfiled years that must be prepared before the IRS will even discuss reinstatement; a plan that already terminated with a final levy notice in the pile; a balance your income genuinely can't full-pay, where PPIA, CNC, or offer math has to be built and defended; or business and payroll tax, where default draws personal-liability scrutiny. In those cases, the order you fix things in — returns first, then the agreement, then penalty relief — materially changes what you pay.

Two free resources belong in your toolkit regardless: your IRS online account (to watch the agreement status and balance in real time) and, if a levy is causing immediate hardship and you can't get through to anyone, the Taxpayer Advocate Service.

Terms on your CP523, decoded

- Default: you broke a condition of the agreement — the plan is in trouble but not yet dead.

- Termination: the agreement formally ends (typically 30 days after the CP523 date) and the IRS's collection powers switch back on.

- Reinstatement: restoring the same agreement after default, usually for an $89 fee ($43 low-income), conditioned on filing and paying current taxes.

- CAP appeal (Form 9423): a fast administrative appeal of the termination; levy is generally paused while it's pending, but the decision can't be taken to court.

- CDP rights (Form 12153): your right to a Collection Due Process hearing after a final notice of intent to levy — a 30-day clock that preserves court review.

- CSED: the Collection Statute Expiration Date — the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause the clock.

The IRS's own summary of the notice is at Understanding your CP523 notice.

If your termination date has already passed and a final levy notice may be next, don't wait to find out — have an experienced tax professional map your fastest reinstatement path free at (888) 825-7779 or through the 2-minute form.

Defaulted payment plan questions, answered

How many payments can you miss before the IRS defaults your installment agreement?

Sometimes just one. A single missed or bounced payment can put your agreement in default, though the IRS usually gives you a chance to catch up before it moves to terminate. A missed payment typically shows up as past due on your next CP521 statement; the CP523 termination notice follows if the account isn't cured. Don't wait for a second miss — call as soon as you know a payment won't go through.

Can I reinstate a defaulted IRS payment plan?

Yes — most defaulted installment agreements can be reinstated if you act quickly and fix what caused the default. The reinstatement fee is $89 by phone or mail ($43 if you meet the IRS low-income threshold), and the IRS will require every past-due tax return to be filed before it says yes. If your balance or income changed, the IRS may restructure the monthly payment as part of reinstatement.

What does IRS notice CP523 mean?

CP523 is the IRS's formal notice that it intends to terminate your installment agreement, usually because of a missed payment, a new unpaid balance, or an unfiled return. You generally have 30 days from the date on the notice before termination takes effect. Acting inside that window — curing the default or calling to reinstate — keeps the agreement alive and keeps levy protection in place.

Will the IRS levy my bank account after my payment plan defaults?

Not immediately — levies can't simply resume the day your plan defaults. The IRS generally must let the CP523's 30-day window pass, let the agreement actually terminate, and honor your appeal rights before levying; if you never received a final notice of intent to levy for a tax period, it must send one first. Once a bank levy does hit, your bank holds the funds for 21 days before sending them to the IRS — a short final window to get the levy released.

Does a new tax bill cancel my existing IRS payment plan?

Filing a new return with a balance you don't pay is one of the most common ways a payment plan defaults — the agreement requires you to stay current on all future taxes. The fix is to call before the new balance triggers a CP523 and ask the IRS to add the new year to your existing agreement, which usually means a restructured monthly payment. Self-employed taxpayers should also expect the IRS to ask whether current-year estimated payments are being made.

Does defaulting on an IRS payment plan hurt my credit score?

Not directly — the IRS doesn't report to credit bureaus, and tax liens no longer appear on consumer credit reports. The indirect damage is real, though: a Notice of Federal Tax Lien filed after default is a public record that mortgage lenders can find, and it can complicate home loans and refinances. A levy that empties your bank account can also cause bounced payments to other creditors that do hit your credit.

Can I get a new payment plan after the IRS terminated my old one?

Yes. After termination you can request reinstatement of the old agreement or a brand-new installment agreement — the IRS doesn't bar you for a prior default. Expect the $89 reinstatement fee ($43 low-income), a requirement that all returns are filed, and possibly a Form 433-F financial statement if your terms are changing or your balance has grown. After repeated defaults, the IRS may insist the new plan run on direct debit.

How long do I have to appeal a terminated installment agreement?

You generally have 30 days after the termination date to appeal under the Collection Appeals Program (CAP) using Form 9423, and the IRS is generally barred from levying while a timely CAP appeal of an installment agreement termination is pending. CAP is fast but final — you can't take the decision to court. Many people use the appeal window as leverage to negotiate reinstatement instead of fighting the termination itself.

Do penalties and interest keep growing while my plan is in default?

Yes, and the bleed gets faster. While an installment agreement is in good standing, the failure-to-pay penalty runs at a reduced 0.25% per month; once the agreement is no longer in effect, it returns to 0.5% per month — double the rate — plus daily-compounding interest on the whole balance. On a $41,800 balance, that's roughly $209 a month in penalty alone versus about $105 on an active plan.

Your next 24 hours

- Find the two dates on your CP523 — the notice date and the termination deadline — and put the 30-day mark on a calendar you'll actually see.

- Gather your file: the CP523, your last filed return, a list of any unfiled years, and rough numbers for your current monthly income and expenses.

- Get a free case review — the 2-minute form or (888) 825-7779 — before the termination date on your notice passes. Inside the window, reinstatement is a phone call and a fee; after it, you're negotiating with levy powers back in play.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.