IRS Collections & Appeals

IRS CAP Appeal: How the Collection Appeals Program Stops a Levy, Lien, or Terminated Payment Plan (2026)

The short answer: an IRS CAP appeal — a Collection Appeals Program request, filed on Form 9423 — is the fastest way to challenge a specific collection action: a levy, lien filing, seizure, or a rejected or terminated installment agreement. It usually pauses that action while Appeals reviews it, but the decision is binding and you cannot dispute the tax itself.

Maybe a revenue officer just told you a levy is next. Maybe a CP523 says the payment plan that was holding everything together is being terminated. Either way, the IRS is about to take one specific action against you — and CAP exists to put an independent set of eyes on that action first. The appeal is real, it works, and the window to use it is brutally short.

Form 9423 itself is a single page. The image below shows you exactly what the form looks like and where the entries that decide your appeal go — keep it in mind as you read, because what you write in the "reason" and "proposed solution" sections matters more than everything else combined.

⏱ Your deadline: CAP windows are the shortest in IRS collections. In a revenue officer case, the Form 9423 instructions say to tell the collection office within 2 business days after the manager conference that you plan to appeal, then get Form 9423 submitted (received or postmarked) within 3 business days of the conference — miss either and collection can resume. For a rejected or terminated installment agreement, you generally have 30 days from the date on the letter — check the exact date printed on yours.

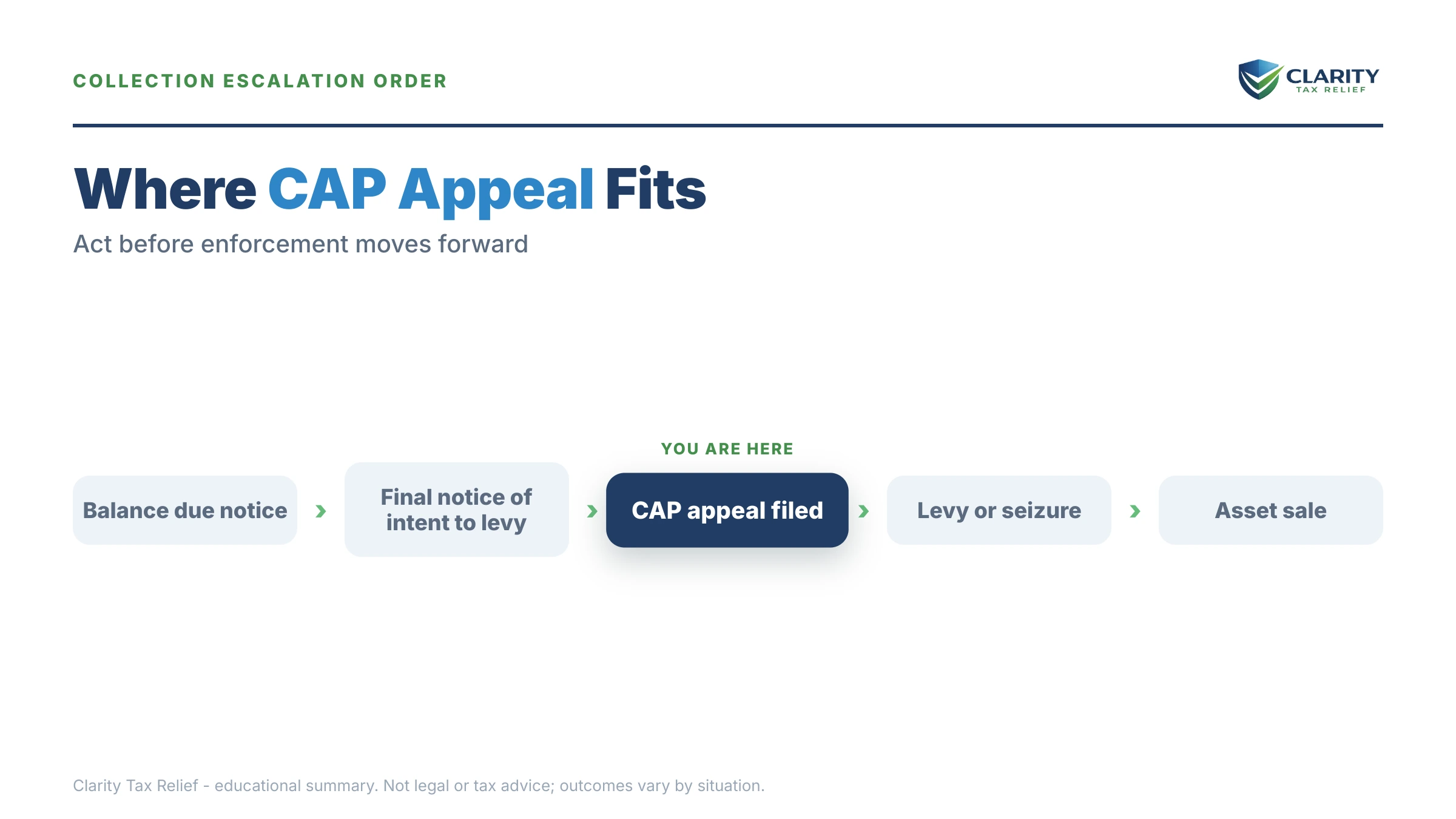

When an IRS CAP appeal can stop a collection action

The Collection Appeals Program (CAP) covers four kinds of IRS collection actions — levies, lien filings, property seizures, and installment-agreement rejections, modifications, or terminations — and in most cases you can appeal before the action happens, not just after. That "before" is what makes CAP different from almost everything else in the collection playbook: it is designed to interrupt an action that is queued up but not yet done.

You generally have 30 days from the date on a CP523 or an installment-agreement rejection letter to file a CAP appeal of that action. For installment-agreement disputes, CAP is usually the only appeal available, because no levy or lien notice with formal hearing rights is involved. If your plan defaulted, a CP523 notice is the letter that starts this clock.

Who you're dealing with changes how you start. If a revenue officer is handling your case, you must first ask for a conference with that officer's manager; only if the manager doesn't resolve it do you file Form 9423. If your case sits in the automated system (ACS) — you've only received computer-generated letters — you request CAP by calling the number on your notice and telling them you want to appeal under the Collection Appeals Program.

Two hard limits. First, CAP reviews only whether the collection action is appropriate — it cannot change how much you owe. Second, the CAP decision is binding on you and the IRS, with no Tax Court review afterward. That trade-off — speed for finality — is the whole strategic question of this article.

| Collection action | CAP available? | Your window / how to start |

|---|---|---|

| Levy — proposed or already served | Yes, before or after the levy | Revenue officer case: manager conference, then typically 3 business days to file (per the Form 9423 instructions). ACS case: call the number on your notice. |

| Notice of Federal Tax Lien | Yes, before or after filing | Same manager-conference route; act before the filing when you can — unwinding a recorded lien is much harder. |

| Seizure of property | Yes | Per the Form 9423 instructions, generally within 10 business days of the Notice of Seizure. |

| Installment agreement rejected | Yes — often the only appeal route | Generally 30 days from the date on the rejection letter. |

| Installment agreement terminated or modified (CP523) | Yes — often the only appeal route | Generally 30 days from the date on the letter; a timely appeal typically keeps the agreement's protections in place. |

| The amount of tax you owe | No | Use audit reconsideration, an amended return, penalty abatement, or a CDP hearing where liability can sometimes be raised. |

What happens if you skip the CAP window

Once a CAP window closes, the action you could have paused simply proceeds — and every action on this list is harder to undo than to prevent. For a 1099 contractor especially, the sequence tends to run like this:

- The terminated agreement takes effect. Your account drops back into active collections and the notice stream restarts — the order of IRS collection letters picks up where it left off, with the balance larger than before.

- A final notice arrives. An LT11 notice or Letter 1058 starts a 30-day clock, after which the IRS can levy without further warning.

- A lien gets recorded. A Letter 3172 notice of federal tax lien means the filing is public record — it attaches to everything you own and complicates financing and, for some contractors, contract bids.

- Levies land. A bank levy freezes funds for 21 days before they're sent to the IRS. A levy served on one of your clients takes 100% of whatever that client owes you on that day — contractor levies are one-time grabs of the full receivable, not a percentage like a W-2 garnishment.

In 2026, no human has to touch most of this. IRS staffing fell sharply in 2025, but the systems that terminate agreements, file liens, and issue levies are automated — the appeal windows are the moments a person is required to look at your file, which is precisely why they're worth using.

Facing a levy, lien, or terminated agreement right now?

Your CAP window may be measured in business days — 3 after a manager conference, 30 from an installment-agreement letter. Get your notice and Form 9423 strategy reviewed free before the window closes, including whether CDP is the stronger play for your case.

CAP vs. CDP: choosing the right appeal

CAP and CDP are the two formal ways to appeal IRS collection, and picking the wrong one can cost you your only shot at Tax Court. A Collection Due Process hearing — requested on Form 12153 — is only available after specific notices (an LT11 final levy notice or a lien-filing notice), but it preserves judicial review. CAP covers more situations and moves faster, but ends with a binding decision.

| Feature | CAP (Form 9423) | CDP (Form 12153) |

|---|---|---|

| What it covers | Levies, lien filings, seizures, installment-agreement rejections/modifications/terminations | Only levy and lien notices that carry CDP rights (e.g., LT11, Letter 3172) |

| When you can file | Before or after most actions; often the only route for payment-plan disputes | Within 30 days of the CDP notice |

| Speed | Fastest IRS appeal — often days to weeks | Commonly takes months |

| Dispute the tax amount? | No — action only | Sometimes, if you never had a prior chance to contest it |

| Tax Court afterward? | No — decision is binding | Yes |

| Pauses the 10-year statute (CSED)? | No | Yes, while pending |

| Collection while pending? | The appealed action is generally held | Levy action is generally held |

That CSED row deserves a second look. The IRS has 10 years from assessment to collect, and a timely CDP request stops that clock while the hearing is pending — a CAP appeal does not. If your debt is old, CAP gets you review without gifting the IRS extra collection time; the details of what extends the IRS collection statute matter here, and you can estimate your own expiration date with our CSED Calculator.

CAP is also not the only lever. If a levy is causing immediate hardship, a §6343 economic-hardship release can be faster than any appeal. If the real problem is a plan you can simply fix, curing the default directly may beat appealing the termination — see my payment plan defaulted — now what. And for the full menu of resolution programs behind whichever appeal you choose, the overview in how to settle tax debt yourself covers the shared ground so this page doesn't have to.

A worked example: $19,700, a defaulted plan, and one client invoice

Say you're a 1099 contractor who owes $19,700 across two tax years — well under the $50,000 line, so you set up a streamlined installment agreement at roughly $274/month ($19,700 ÷ 72 months, before the interest and late-payment penalty that keep accruing on top). Then a slow quarter hits, you miss two payments, and a CP523 arrives saying the agreement is being terminated.

Here's the math on doing nothing. If the termination stands, the account goes back to enforced collection. A levy served on your biggest client takes 100% of whatever they owe you the day it lands — if that's a $6,800 invoice, the whole $6,800 goes to the IRS, because an IRS levy on a 1099 contractor is a one-time seizure of the full receivable, not a paycheck percentage. One levy notice to one client can cost more than a year of the plan payments you were struggling with.

Here's the CAP alternative. Within the 30-day window you file Form 9423 appealing the termination, explain the income dip, and propose reinstatement at a payment you can document — say $300/month with the two missed payments caught up over the next quarter. Appeals can approve a workable proposal quickly, the agreement's protections stay in place while the appeal is pending, and no client ever gets a levy notice with your name on it. Interest still accrues either way, and a reinstatement fee may apply — but you keep your cash flow and your client relationships intact. (This scenario is hypothetical, but the mechanics are exactly how these cases run.)

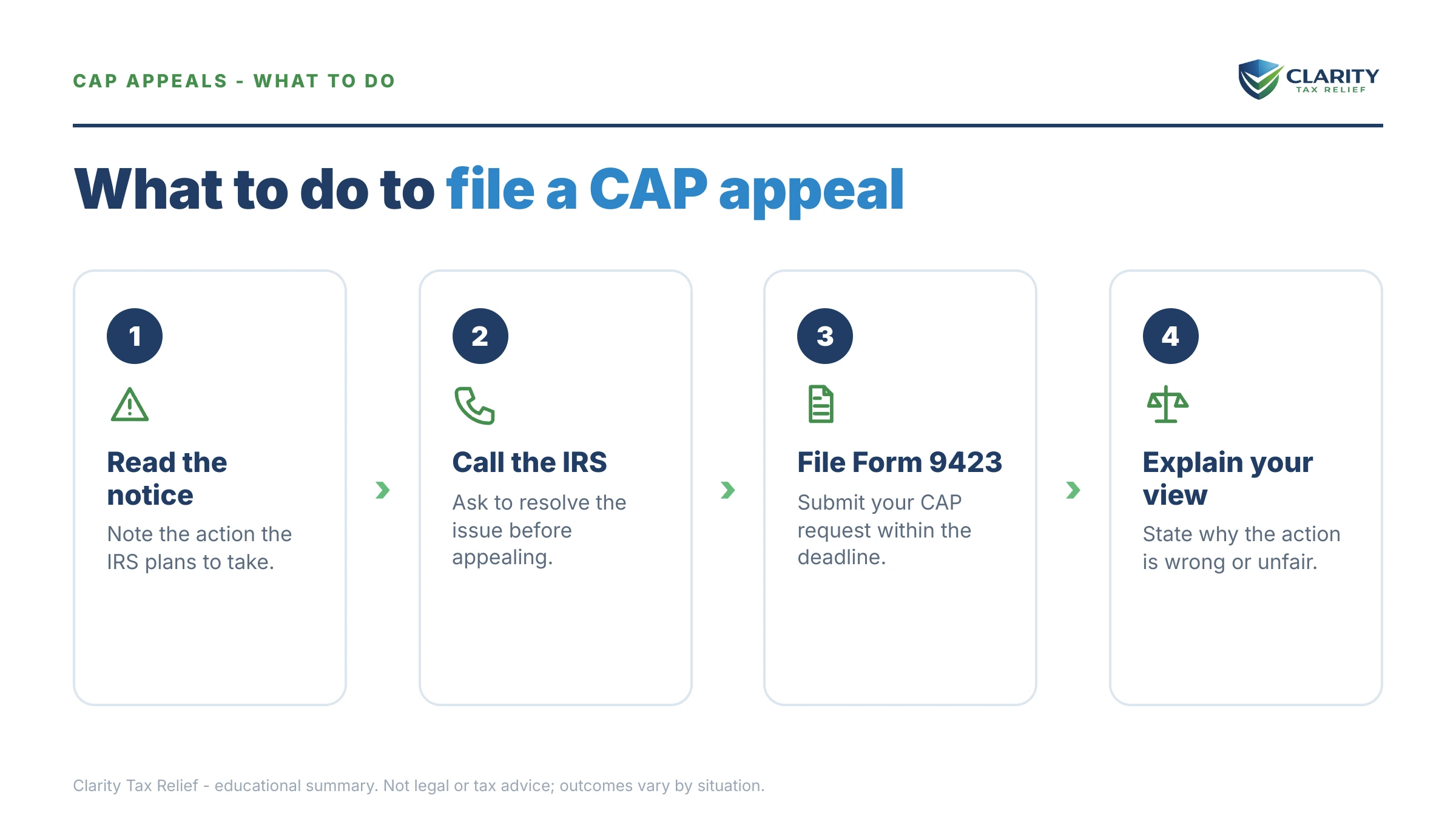

How to file a CAP appeal, step by step

- Confirm the action and its date. Pull the exact collection action being appealed — levy, lien filing, seizure, or installment-agreement rejection or termination — and the date printed on your notice, because that date starts your window.

- Request a manager conference first in revenue officer cases. Tell the revenue officer you want to discuss the action with their manager; if the conference does not resolve it, say clearly that you intend to file a CAP appeal.

- Complete Form 9423. Identify the specific action you are appealing, explain why you disagree with it, and propose a concrete alternative — such as a payment plan you can actually keep — because Appeals decides faster when it has something to approve.

- File within your window. Per the Form 9423 instructions, that is typically 3 business days after the manager conference in revenue officer cases, or 30 days for installment-agreement appeals; send the form to the Collection office handling your case.

- Follow up and stay compliant. Confirm the case reached Appeals, keep current-year filings and payments on track while it is pending, and be ready to document your proposed alternative — the decision you receive is binding.

The current form and its instructions are on the IRS site at About Form 9423, Collection Appeal Request — read the instructions for your exact situation before filing, because the windows differ by action type.

When you can handle a CAP appeal yourself

Many CAP appeals are genuinely DIY-friendly, because the form is one page and the strongest argument is usually a simple, documented proposal. You can reasonably handle it alone when the facts are clean: a payment plan that defaulted over one or two missed payments you can now catch up, a levy threatened while you were actively negotiating in good faith, or a lien filing that would plainly do more harm than good and you have an alternative to offer. In those cases, a clear Form 9423 plus proof of your proposal is most of the battle.

Experienced help changes outcomes in a narrower set of situations: a levy already served on your clients or bank, a revenue officer–managed case where the 3-business-day clock is running, multiple unfiled years that make any proposal dead on arrival until returns are in, business or payroll tax debt, or any case where you hold live CDP rights — because choosing CAP when CDP was available permanently burns your only path to Tax Court, and that decision deserves a second opinion before it becomes irreversible. An experienced tax professional can often tell you in one conversation which appeal fits.

Terms on Form 9423 and your notice, decoded

- CAP (Collection Appeals Program): the expedited appeal that reviews a specific collection action — not the tax itself — and ends in a binding decision.

- CDP (Collection Due Process): the slower, stronger hearing right attached to final levy and lien notices, which preserves Tax Court review.

- Form 9423: the one-page Collection Appeal Request that starts a CAP case.

- Revenue officer vs. ACS: a revenue officer is a human assigned to your case (manager conference required first); ACS is the automated system behind computer-generated notices (you request CAP by phone).

- CSED: the Collection Statute Expiration Date — the end of the IRS's 10-year window to collect; CAP doesn't pause it, CDP does.

- Binding decision: once Appeals rules on a CAP case, both you and the IRS must follow it, with no court review afterward.

CAP cases are decided by the IRS Independent Office of Appeals, which is separate from the Collection function that took the action — its overview is at IRS.gov/appeals, and if a pending action is causing serious hardship the Taxpayer Advocate Service is a parallel route worth knowing.

CAP appeal questions, answered

What is a CAP appeal with the IRS?

A CAP appeal is a request under the Collection Appeals Program, filed on Form 9423, asking the IRS Independent Office of Appeals to review a specific collection action before or after it happens. It covers levies, lien filings, seizures, and rejected, modified, or terminated installment agreements. It is the fastest appeal route the IRS offers, but the decision is binding — you cannot take a CAP result to Tax Court.

What is the difference between a CAP appeal and a CDP hearing?

CAP is faster but narrower; CDP is slower but stronger. A CDP hearing (Form 12153) lets you propose alternatives, sometimes dispute the underlying tax, and appeal the result to Tax Court — but it is only available after specific notices, such as an LT11 or a lien-filing notice. CAP covers more actions, including installment-agreement terminations, and can be used earlier, but you cannot dispute the tax amount and cannot go to court afterward.

Does a CAP appeal stop the levy while it is pending?

Generally yes — the IRS normally holds the collection action you are appealing while Appeals reviews a timely CAP request, unless it believes collection of the debt is at risk. That pause is exactly why the filing windows are so short. A CAP appeal does not return money already taken; funds seized in a completed bank levy need a separate release or wrongful-levy claim.

Can I dispute how much I owe in a CAP appeal?

No. CAP only reviews whether the collection action itself is appropriate and follows IRS procedure — it cannot change the underlying tax assessment. If you believe the balance is wrong, you need a different path: audit reconsideration, an amended return, penalty abatement, or a CDP hearing where liability can sometimes be raised. Filing a CAP appeal to argue about the amount will get the appeal decided against you.

How long does a CAP appeal take?

CAP is designed to be the quickest review in IRS collections — Appeals works these cases on an expedited basis, and straightforward levy or installment-agreement cases are often decided in days to a few weeks rather than the months a CDP hearing can take. Your timeline depends on how complete your Form 9423 is and whether you propose a realistic alternative Appeals can approve quickly.

Can I appeal a rejected or terminated installment agreement with CAP?

Yes — installment-agreement rejections, proposed modifications, and terminations are core CAP territory, and CAP is often the only appeal available for them because no CDP notice is involved. You generally have 30 days from the date on the rejection or termination letter, and the agreement's protections typically stay in place while a timely appeal is pending. Check the exact date printed on your CP523 or rejection letter.

Does a CAP appeal pause the 10-year collection statute?

No — unlike a timely CDP hearing, a CAP appeal does not suspend the CSED, the 10-year deadline the IRS has to collect a debt. That makes CAP attractive when your balance is old: you get Appeals review without handing the IRS extra collection time. A CDP request, an offer in compromise, and bankruptcy all pause that clock while they are pending.

Can I go to Tax Court after a CAP decision?

No. A CAP decision is binding on both you and the IRS, and there is no judicial review afterward — that trade-off is the price of CAP's speed. If preserving the right to Tax Court matters and you have received a notice that carries CDP rights, filing Form 12153 within its 30-day window is usually the better move. Many taxpayers use CAP only when no CDP right is available.

Your next 24 hours

- Find the action and the date. On your notice, locate exactly what the IRS is doing (levy, lien, seizure, or agreement termination) and the printed date — that date, not the day you opened the envelope, controls your CAP window.

- Gather your proof. Pull the notice itself, your last filed return, and the income and expense records that support the alternative you'll propose — for a payment-plan appeal, that means the number you can actually pay every month.

- Get the appeal reviewed free. Before you commit to CAP and give up Tax Court rights, have an experienced tax professional confirm it's the right appeal for your window — the 2-minute form at claritytaxrelief.com/#consult or (888) 825-7779, ideally before a 3-business-day or 30-day clock runs out.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.