Tax Debt Resolution

How to Settle Tax Debt Yourself in 2026: Every DIY Option, Step by Step

The short answer: you can settle tax debt yourself using the same IRS programs professionals use — a payment plan (up to 72 months online for balances of $50,000 or less), penalty abatement, Currently Not Collectible status, or an Offer in Compromise ($205 fee, waived for low-income filers). No company is required for any of them.

You've seen the ads promising settlements, you've priced the retainers, and the honest question underneath is whether learning how to settle tax debt yourself is realistic — or a trap. For most balances under $50,000 with returns filed, it's realistic. The IRS's programs were built to accept applications directly from taxpayers, and every one of them can be started from your couch tonight.

This guide walks the whole path: which program fits which finances, exactly what each costs, the forms and the order to file them in, and — honestly — the specific situations where doing it alone tends to cost more than help would.

⏱ The real clock: there's no printed deadline on the decision to resolve your debt — but the meter never stops. The failure-to-pay penalty adds 0.5% of your balance every month, interest compounds daily on top of it, and each ignored notice moves you one step closer to a levy. Every month of "I'll deal with it later" is a real dollar cost.

Why you owe — and why the balance keeps growing

A tax debt is almost always tax plus two moving parts: penalties and interest, and both keep compounding until something is set up. If you filed but couldn't pay, the failure-to-pay penalty accrues monthly. If you didn't file at all, the failure-to-file penalty runs at 5% per month — ten times the pay penalty — which is why filing always comes before negotiating, even when you can't pay a dime. The math on that is laid out in file even if you can't pay.

Life changes are the most common trigger. A divorce alone can create a balance three different ways: withholding set for married-filing-jointly that's suddenly wrong for single, a retirement account split or cashed out during the settlement, or a joint-year balance your decree assigned to your ex — which, to the IRS, you still owe in full. If a notice is what brought you here and you're not sure what it means, start with why did I get a letter from the IRS, then come back — the resolution playbook below is the same regardless of which notice arrived.

One myth to clear before we start: there is no "pennies on the dollar" hotline and no IRS one-time forgiveness program. Those phrases are marketing wrapped around the real programs below — programs with real eligibility math that you can run yourself.

What happens if you do nothing

An unresolved tax debt escalates through an automated notice sequence that ends in a levy — no human has to approve each step. In 2025 the IRS cut its workforce by roughly 27%, which made phone lines slower but changed nothing about the machine: notices, liens, and levies still fire on schedule. The sequence runs like this:

- Silent accrual. Before any notice, penalties and interest are already compounding on the balance.

- CP14 — the first bill. You get roughly 21 days to pay or arrange something before the reminders start — 10 business days when the balance is $100,000 or more.

- CP501 and CP503 — reminders. Still just bills, but each one arrives with a bigger number on it.

- CP504 — intent to levy your state refund. The IRS can now take your state tax refund under IRC §6331(d), and a federal tax lien becomes a live possibility.

- LT11 / Letter 1058 — final notice. A 30-day clock starts on your Collection Due Process rights (requested with Form 12153). After it runs, the IRS can levy.

- Enforcement. A bank levy freezes funds for a 21-day hold before they're sent to the IRS; a wage levy is continuous until released; Social Security can be levied at up to 15% through the Federal Payment Levy Program. Balances that grow past $66,000 (the 2026 threshold) add passport certification to the list.

Two more clocks run quietly underneath all of this. The IRS generally has 10 years from assessment to collect — the 10-year collection statute (CSED) — and your refunds will be swept toward the balance every filing season until it's resolved. Everything below exists to stop this sequence before the levy stage, where your options narrow sharply.

Want a second set of eyes before you commit to a program?

Send us what you're working with — your balance, your notices, your budget. An experienced tax professional will tell you which DIY path fits and whether you're missing penalty relief you could claim first. Free, confidential, before another month of penalties posts.

How to settle tax debt yourself: your seven real options in 2026

Seven programs cover essentially every tax-debt situation, and each one accepts a direct application from you. Which fits depends on two numbers: what you owe, and what your budget can actually spare each month.

| Option | Who typically qualifies | How you apply yourself |

|---|---|---|

| Short-term payment plan (180 days) | Anyone who can pay in full within 180 days | Online Payment Agreement tool — $0 setup fee |

| Guaranteed installment agreement | $10,000 or less in tax, returns filed, clean prior 3 years, full pay within 3 years | Online or Form 9465 — approval is required by law if you qualify |

| Streamlined installment agreement | $50,000 or less in combined tax, penalties, and interest | Online, up to 72 months, no financial statement required |

| Non-streamlined agreement | Over $50,000, or a payment lower than the streamlined math allows | Form 9465 plus a Form 433-F financial statement |

| Currently Not Collectible (CNC) | Allowable living expenses equal or exceed your income | Call the number on your notice with Form 433-F figures ready |

| Offer in Compromise (OIC) | Reasonable Collection Potential below the balance owed | Form 656 + Form 433-A (OIC), $205 fee (waived if AGI ≤ 250% of poverty) |

| Penalty abatement | Clean prior 3 years (first-time) or events beyond your control (reasonable cause) | Phone request, written statement, or Form 843 after payment |

Payment plans: the workhorse for most balances

A streamlined installment agreement covers balances up to $50,000 for as long as 72 months — no financial disclosure, and online applications are usually approved on the spot. If you can pay in full within 180 days, the short-term plan is better: $0 setup fee and the notice sequence stops the day it's approved. The full walkthrough with screenshots is in IRS payment plan online, step by step. Interest and a reduced late-payment penalty continue on any plan, so paying faster than the minimum always saves money.

Currently Not Collectible: when there's nothing to pay with

If the IRS's allowable-expense standards show your necessary living costs eat your whole income, collection pauses. You'll walk a collector through your finances — Form 433-F is the worksheet — and if you qualify, levies and garnishments stop while the debt sits. The balance still accrues interest and your refunds still get taken, but the 10-year clock keeps running the whole time. Details and the hardship test are in Currently Not Collectible status.

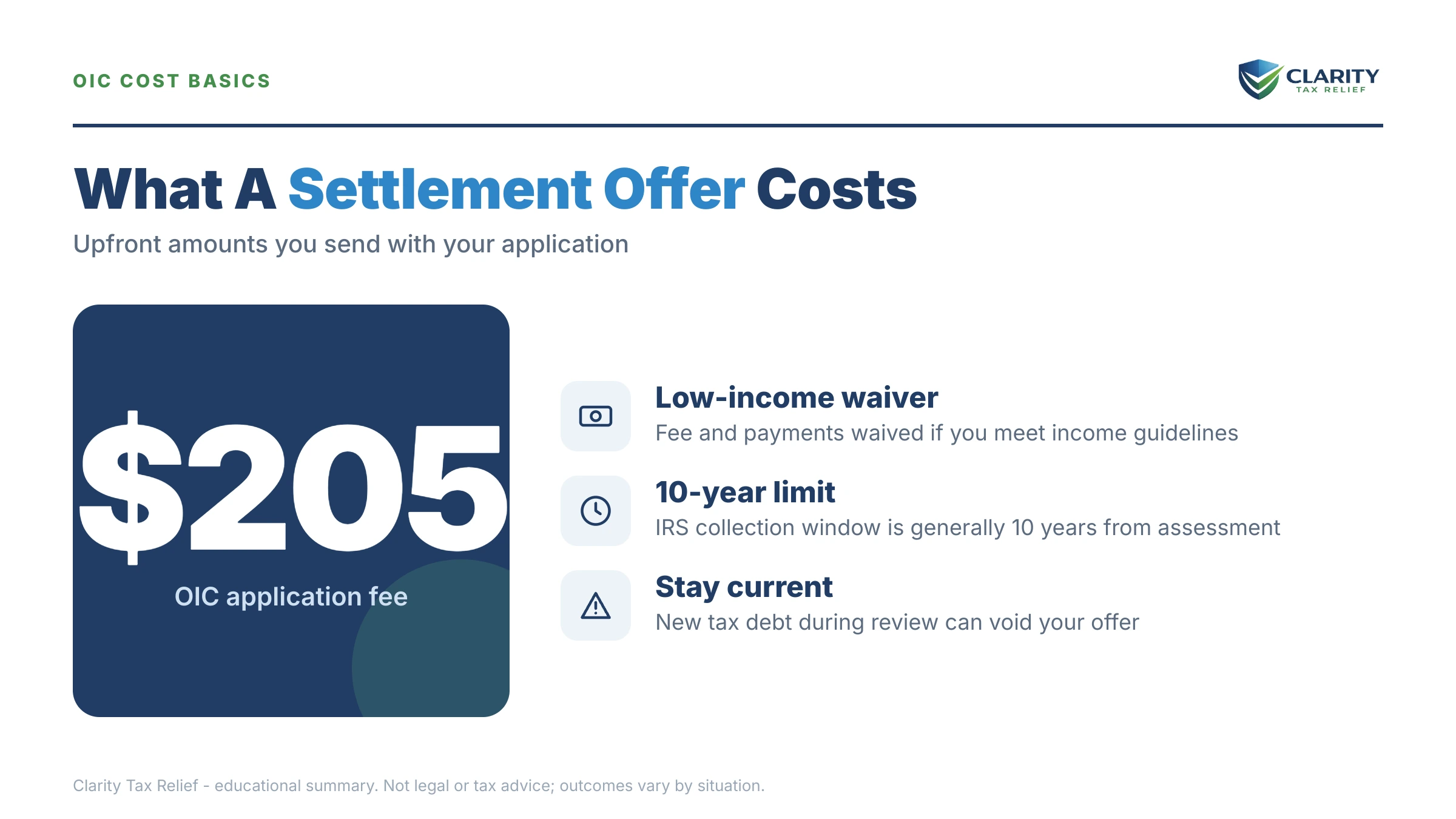

Offer in Compromise: real, means-tested, and DIY-able

An OIC settles the debt for less than you owe — but only when the IRS's own formula says it can't collect in full. That formula is your Reasonable Collection Potential (RCP): the equity in what you own, plus a multiple of the monthly income left after allowable expenses. If RCP comes in at or above your balance, the offer gets rejected no matter how it's written — the IRS accepted roughly 1 in 5 offers in FY2024. You can estimate your own numbers with our Offer in Compromise Calculator before spending the $205 application fee. Low-income certification (AGI at or below 250% of the poverty line) waives that fee, the 20% down payment on lump-sum offers, and payments during review. How the review actually unfolds is covered in how an offer in compromise actually works.

Penalty abatement: the discount most DIYers skip

If your prior three years were penalty-free, one phone call requesting first-time abatement can remove failure-to-file and failure-to-pay penalties from a year — often granted on the spot. Do this before setting up a plan, so you're financing a smaller number. The script and eligibility rules are in first-time penalty abatement, complete guide. Two 2026 notes: starting this summer, the Automatic Exemption from Penalty (AEP) begins applying qualifying relief automatically, with no request needed — but it doesn't cover reasonable-cause situations, which you still request in writing. And abatement removes penalties, not the interest charged on the underlying tax.

Amend the return: when the balance itself is wrong

Sometimes the cheapest settlement is correcting the number. A missed deduction, an unclaimed dependent after a custody change, or basis the IRS didn't know about can shrink the debt at the source via Form 1040-X. The mechanics and when it's worth it are in amend return to reduce tax debt.

Bankruptcy: the option nobody markets

Older income-tax debt can sometimes be discharged in bankruptcy if it passes strict age and filing tests — a genuine path when tax debt sits inside a larger pile of unpayable debt. It's a court process, not an IRS one, and the tradeoffs between chapters are compared in chapter 7 vs 13 tax debt.

A note on state tax debt

None of the federal thresholds above apply to a state balance. States run their own plans, their own hardship rules, and their own clocks — California's FTB, for instance, has a 20-year collection statute, double the IRS's. If you owe both, resolve them as two separate problems with the correct agency for each; never assume the IRS deal covers the state.

What each option costs and how long it takes

Every DIY path has a price tag and a timeline, and knowing both up front keeps you from quitting halfway through the slow ones.

| Option | Upfront cost | Ongoing cost | Typical timeline |

|---|---|---|---|

| Short-term plan (180 days) | $0 setup fee | Interest + late-payment penalty until paid | Approved online in minutes |

| Long-term installment agreement | Setup fee — lowest online with direct debit; waived or reimbursed for low-income filers | Interest + late-payment penalty at a reduced rate while the plan is active | Online approval usually immediate; up to 72 months to pay |

| Currently Not Collectible | $0 | Interest and penalties accrue; refunds offset each year | One phone call plus financial review; periodic re-checks after |

| Offer in Compromise | $205 fee + 20% of the offer for lump-sum (both waived with low-income certification) | Offer payments per your terms; collection generally paused during review | Commonly many months; auto-accepted by law if the IRS doesn't decide within 2 years, with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count |

| First-time penalty abatement | $0 | None — it removes cost | Often granted on the phone the same day |

| Reasonable-cause abatement | $0 (Form 843 if already paid) | None — it removes cost | Weeks to months for a written determination |

A worked example: settling $13,600 yourself after a divorce

Say you owe $13,600 — a hypothetical recently divorced filer whose withholding stayed set to "married" all year, plus a slice of a retirement account cashed out during the settlement. Returns are filed, income is a steady W-2, and this is the first tax problem in years. Here's how each path prices out:

- Penalty relief first. Suppose $1,450 of the $13,600 is failure-to-pay penalty. With a clean prior three years, a first-time abatement call could remove it — cutting the balance to roughly $12,150 before a single payment is made.

- Streamlined payment plan. $12,150 ÷ 72 months ≈ $169/month minimum, set up online tonight with no financial disclosure. Interest and a reduced late-payment penalty keep accruing, so pushing the payment to $300/month clears it in under four years and saves real money.

- Short-term plan. If a house-sale check or settlement payout is coming within six months, the 180-day plan holds off collection at $0 setup cost until it lands.

- Offer in Compromise — only if the math works. Say allowable expenses leave $120/month of disposable income and reachable asset equity is $2,500. A lump-sum RCP would run about $120 × 12 + $2,500 = $3,940 — well under $13,600, so an offer is worth pricing. But flip one variable — $450/month disposable instead of $120 — and RCP jumps past the balance, and the offer would be rejected. That single calculation is the honest answer to whether an OIC fits you.

- The joint-year wrinkle. If part of the debt is from a jointly filed year the decree assigned to the ex, the IRS can still collect it from either spouse. Who actually pays — and when innocent spouse relief shifts it — is covered in divorce and IRS debt: who pays.

All numbers here are illustrative, not a promised result — your allowable expenses and assets drive your outcome.

How to settle your tax debt yourself, step by step

The order matters more than most people realize: verify, file, shrink, then commit.

- Pull your IRS transcripts. Confirm every year with a balance and every dollar of penalty and interest before you negotiate anything — your online account shows the IRS's numbers, not your guess. Here's how to get IRS transcripts online.

- File every missing return. The IRS will not approve a payment plan, CNC status, or an Offer in Compromise while a required return is unfiled.

- Request penalty relief first. One phone call requesting first-time abatement can shrink the balance before you commit to paying it.

- Match your finances to one program. A payment plan if you can pay monthly, Currently Not Collectible if you can't, and an Offer in Compromise only if the RCP math genuinely comes in below your balance.

- Apply online or by form. Use the Online Payment Agreement tool for plans up to $50,000, Form 433-F for a hardship review, and Form 656 with Form 433-A (OIC) for an offer.

- Stay compliant after approval. One unfiled return or missed estimated payment can default the agreement and restart collections from the top.

That last step trips up more DIY settlements than any application error. If you're self-employed or newly single with wrong withholding, fix the current year's payments the same week you set up the plan — a new balance next April defaults the old agreement.

The DIY forms you'll actually use

Six forms cover nearly every self-directed resolution, and all of them are free downloads from the IRS.

| Form | What it does | When you'd use it |

|---|---|---|

| Form 9465 | Installment Agreement Request | Requesting a payment plan by mail instead of online |

| Form 433-F | Collection Information Statement | CNC requests and payment plans that need a financial review |

| Form 656 | Offer in Compromise application | Submitting your offer, with the $205 fee or low-income certification |

| Form 433-A (OIC) | Financial statement for an offer | The RCP math behind Form 656 — filed together |

| Form 843 | Claim for Refund and Request for Abatement | Recovering a penalty you already paid |

| Form 12153 | Collection Due Process hearing request | Preserving appeal rights within 30 days of an LT11 / Letter 1058 |

When DIY works — and when help changes the outcome

Most tax debts under $50,000 can be resolved without paying anyone. You do not need professional help when:

- You agree with the balance, your returns are filed, and a streamlined plan or 180-day payoff fits your budget — that's a 15-minute online task.

- Your only issue is penalties and your prior three years are clean — first-time abatement is a phone call.

- Your income is modest — a Low Income Taxpayer Clinic or other free help with IRS tax debt can represent you at no cost, and the Taxpayer Advocate Service exists precisely for cases the system is mishandling.

Experienced help tends to change outcomes when the problem has layers:

- A levy or garnishment is already in motion — release negotiations are time-critical and standards-driven.

- Multiple unfiled years — the sequencing of which returns to file, and how, changes what you ultimately owe.

- Business or payroll tax debt — trust-fund liability can attach to you personally, and the rules differ entirely from a 1040 balance; see construction payroll tax debt for how fast that category escalates.

- An Offer in Compromise on close math — how assets and expenses get characterized in the 433-A (OIC) can be the difference between acceptance and rejection, and a rejected offer tolls your collection clock.

- Disputed liability — an ex's income, an audit you never responded to, or identity theft calls for a different toolkit than collections.

If your situation lands in that second list, a free consultation with an experienced tax professional at (888) 825-7779 or the 2-minute form settles the DIY-or-not question in one call — before you spend months on a path the math was always going to reject.

Terms you'll hit along the way, decoded

- CSED — Collection Statute Expiration Date: the day, generally 10 years after assessment, when the IRS's right to collect a balance expires (offers, bankruptcy, and appeals pause the clock).

- RCP — Reasonable Collection Potential: the IRS's formula (asset equity plus future disposable income) that sets the minimum acceptable Offer in Compromise.

- Streamlined agreement — a payment plan approved without a financial statement, available at $50,000 or less over up to 72 months.

- CNC — Currently Not Collectible: account status that pauses levies and garnishments when your necessary expenses consume your income.

- Allowable living expenses — the IRS's published caps on housing, transportation, food, and health costs that decide both CNC eligibility and OIC math.

- Lien vs. levy — a lien is a legal claim against your property securing the debt; a levy is the actual taking of wages, bank funds, or property.

Settling tax debt yourself: your questions, answered

Can I really settle my tax debt myself without a tax relief company?

Yes — every IRS resolution program accepts applications directly from taxpayers, and a company files the same forms you can file yourself. Payment plans up to $50,000 can be set up online in about 15 minutes, and penalty abatement can be requested with one phone call. The exception is complexity: an active levy, business payroll debt, or contested Offer in Compromise math is where experienced representation tends to change outcomes.

Does the IRS have a one-time forgiveness program?

No — "one-time forgiveness" is marketing shorthand, not an IRS program. What actually exists is first-time penalty abatement, which removes penalties if your prior three years were clean, and the Offer in Compromise, which settles the underlying tax only when the IRS's own math shows it can't collect in full. Starting in summer 2026, an Automatic Exemption from Penalty (AEP) begins applying qualifying penalty relief without a request.

How much will the IRS settle for in an Offer in Compromise?

There is no fixed percentage — the IRS settles for your Reasonable Collection Potential: the equity in your assets plus a multiple of your monthly disposable income. The IRS accepted roughly 1 in 5 offers in FY2024, and if your income shows you could full-pay through a payment plan, expect a rejection. Anyone quoting you a settlement percentage before seeing your finances is guessing or selling.

Can I set up an IRS payment plan online by myself?

Yes. If you owe $50,000 or less in combined tax, penalties, and interest and have filed all required returns, the Online Payment Agreement tool approves plans of up to 72 months, usually instantly. If you can pay within 180 days, the short-term plan has no setup fee at all. You'll need an IRS online account to apply, so set that up first.

What if I can't afford any monthly payment at all?

Ask for Currently Not Collectible status, which pauses all collection when your allowable living expenses meet or exceed your income. You'll typically provide a financial statement — Form 433-F — by phone or mail. The debt doesn't disappear: interest keeps accruing and refunds get offset, but levies and garnishments stop while the 10-year collection clock keeps running.

Does IRS tax debt really go away after 10 years?

Generally yes — the IRS has 10 years from assessment to collect, after which the balance expires. But the clock pauses (tolls) during an Offer in Compromise, bankruptcy, and certain appeals, so the real expiration date is often later than year ten. Waiting it out is only a realistic strategy when the clock is nearly done and your finances make you hard to collect from in the meantime.

My divorce decree says my ex pays the tax debt — am I off the hook?

No — the IRS is not bound by your divorce decree. On a jointly filed return, both spouses remain jointly and severally liable for the full balance, so the IRS can pursue whichever of you is easier to collect from. The decree gives you recourse against your ex in state court, and innocent spouse or separation-of-liability relief may shift the debt if your ex caused the understatement.

How do I get IRS penalties removed myself?

Call the number on your notice and request first-time penalty abatement — if your prior three years show no penalties and your returns are filed, it's often granted on the call. For illness, disaster, or other events outside your control, request reasonable-cause relief in writing, or use Form 843 to claim back a penalty you already paid. Starting summer 2026, the Automatic Exemption from Penalty applies qualifying relief with no request needed.

What does a tax relief company do that I can't do myself?

Nothing procedurally — professionals file the same forms through the same IRS channels. What they add is judgment: knowing how the IRS's expense standards get applied, how to sequence penalty relief before a plan, when an offer's math will survive review, and how to handle a revenue officer or an appeal. For a straightforward balance under $50,000 with returns filed, most people can handle it alone; layered problems are where experience pays for itself.

Your next 24 hours

- Get the real number. Log into your IRS online account and write down the balance for each year — tax, penalty, and interest separately. That penalty line is your first target.

- Gather three things. Your last filed return, any IRS notices you've received, and a rough monthly budget of income versus necessary expenses. Every program above starts from exactly these documents.

- Pick your path — or get a free read first. If a plan fits, apply on the IRS payment plans page tonight. If your numbers point toward an Offer in Compromise, hardship, or a joint-year dispute, get a free case review at the 2-minute form or (888) 825-7779 before penalties and interest add another month to the balance.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.