Back Taxes & Filing

Should I File If I Can't Pay? Yes — Here's the Math (2026)

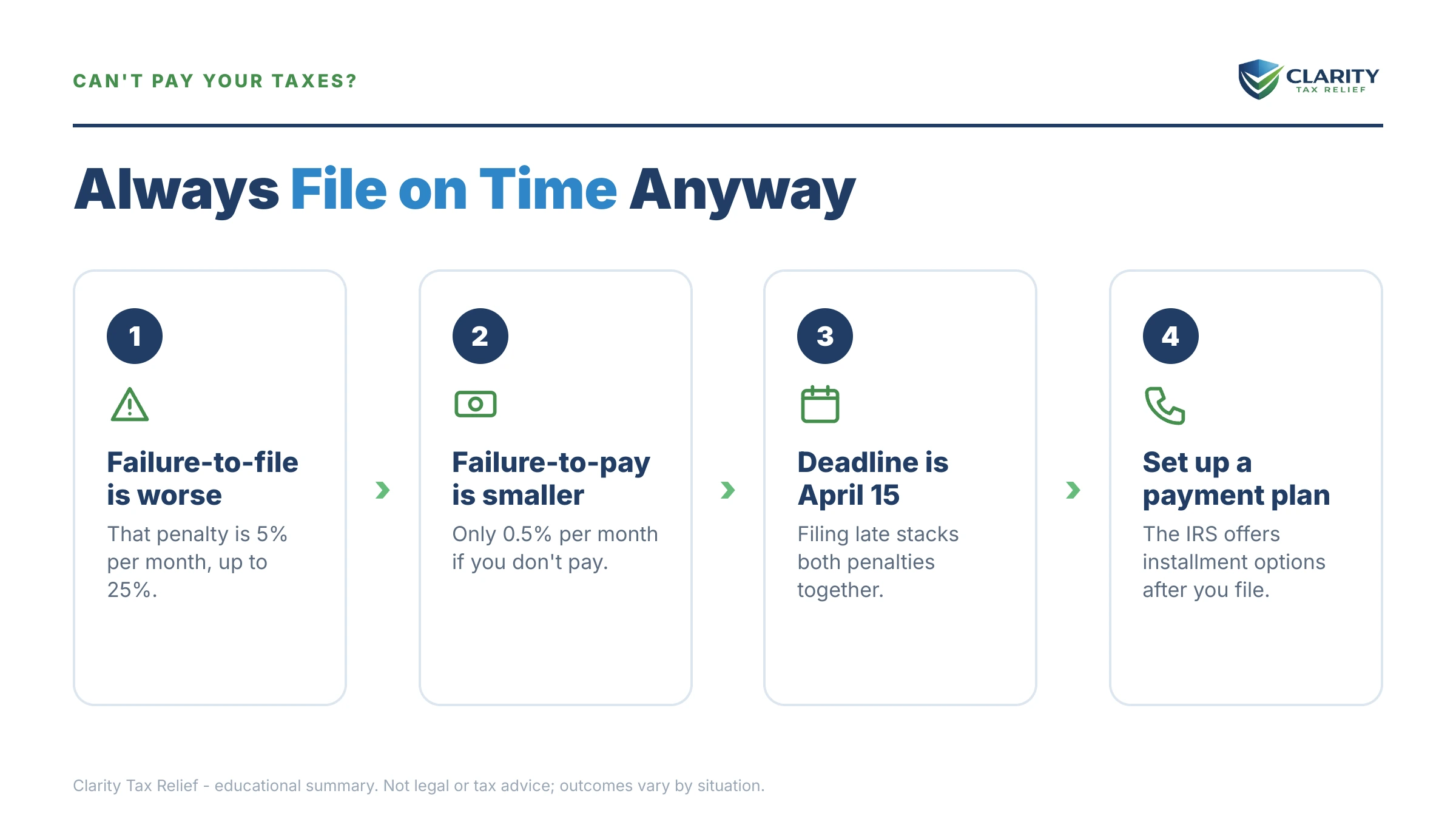

The short answer: should I file if I can't pay? Yes — file anyway, on time if possible and immediately if you're already late. The failure-to-file penalty is 5% of your unpaid tax per month; the failure-to-pay penalty is only 0.5%. Filing with no payment attached cuts your monthly penalty by roughly 90%.

You've added up the 1099s in a spreadsheet, you know roughly what you owe, and you know you can't pay it — so skipping the return feels safer than officially confirming a debt you can't cover. That instinct is understandable, and it is exactly backwards. The IRS prices silence ten times higher than honesty, and every relief program it offers requires a filed return first.

⏱ Your clock: there's no letter deadline on this question — the deadline is the penalty itself. The failure-to-file penalty adds 5% of your unpaid tax every month a return is late, hitting its 25% cap around month five. Separately, any refund from an unfiled year expires three years after that return's original due date. Both clocks are already running.

Should I file if I can't pay? The penalty math says yes

Not filing costs 10 times more per month than filing and not paying — 5% versus 0.5% of the unpaid tax. That single ratio answers the question. The IRS treats a missing return as a far bigger offense than a missing payment, because the whole system runs on returns being filed.

Here's how the two penalties work. The failure-to-file penalty is 5% of the unpaid tax for each month (or part of a month) the return is late, capped at 25%. The failure-to-pay penalty is 0.5% per month, also capped at 25% — but it takes about four years to get there instead of five months. Both run on top of interest, which compounds daily. The full mechanics of both are in our guide to failure to file penalty vs failure to pay.

Put real numbers on it. On a $31,200 balance:

| Scenario | Monthly penalty rate | Monthly cost on $31,200 | Where it caps |

|---|---|---|---|

| File on time, pay $0 | 0.5% (failure-to-pay) | $156 | 25% ($7,800) — after roughly 4 years |

| Don't file, don't pay | 5% combined while both penalties run | $1,560 | Filing penalty caps at 25% in ~5 months; the 0.5% keeps running after that |

| File late, before the IRS acts | Filing penalty stops accruing the month you file | Frozen at whatever has built up | Only the 0.5% and interest continue |

One more number worth knowing: once you're on an approved installment agreement, the failure-to-pay rate is typically cut in half, to 0.25% per month. So the cheapest posture at every stage is: filed, on a plan. You can run your own numbers with our IRS Penalty & Interest Calculator — it estimates what a balance grows to, month by month.

What filing protects, even when you send $0

Filing a return you can't pay starts five protections that never begin while the return sits unfiled. None of them require a single dollar of payment:

- It starts the 10-year collection statute. The IRS has 10 years from assessment to collect — and assessment can't happen until there's a return. An unfiled year is a debt with no expiration date.

- It blocks a substitute for return. If you don't file, the IRS eventually files for you using only the income documents it has — single status, no dependents, and for a gig worker, zero business deductions. Our guide to the IRS filing a substitute return for you covers how to undo one, but it's far cheaper to never let it happen.

- It preserves refunds. Any year with withholding or refundable credits pays out only if you file within three years of the due date — see the 3-year refund deadline for old returns. Miss it and the money is forfeited, even if you owe other years.

- It unlocks every relief program. Payment plans, hardship status, penalty abatement, and offers in compromise all require you to be current on filing. An unfiled year disqualifies you from all of them.

- It keeps the matter civil. Willful failure to file carries potential criminal exposure; filing voluntarily — even years late, even without payment — is what the system is built to reward.

If your hesitation is really about this year's return while older years already have balances, that's a slightly different question with the same answer — see should I file taxes if I owe back taxes.

What happens if you don't file: the escalation sequence

An unfiled return doesn't slip through the cracks — the IRS matching system already holds every 1099 and W-2 issued under your Social Security number. When a required return never arrives, a specific sequence starts, each stage worse than the last:

- CP59 — the first "we have no return on file" notice. A request, not yet a consequence.

- CP516 / CP518 — escalating demands to file; CP518 is the final one. Your window to file on your own terms is closing.

- Substitute for return (SFR) — the IRS prepares your return from its records: gross income, worst-case filing status, no deductions, no expenses.

- CP3219N — a notice of deficiency proposing the SFR balance. You get a window to file your own return or petition Tax Court before it's assessed.

- Assessment and collection — the inflated balance becomes legally owed and moves onto the normal collection track: bills, then intent-to-levy notices, then liens, wage garnishment, and bank levies.

Note what happened by stage five: you now owe a larger amount than a real return would show, penalties computed on that larger amount, and you've lost control of the numbers. In 2026, with IRS staffing down roughly 27%, this sequence is almost entirely automated — humans are harder to reach, but the notices and levies never stopped.

Unfiled years and a balance you can't pay?

Get your situation reviewed free before the IRS files its version of your returns — the no-deduction version. An experienced tax professional will map the filing order, the penalty relief, and the payment option that fits. Penalties compound monthly, so the review is cheapest today.

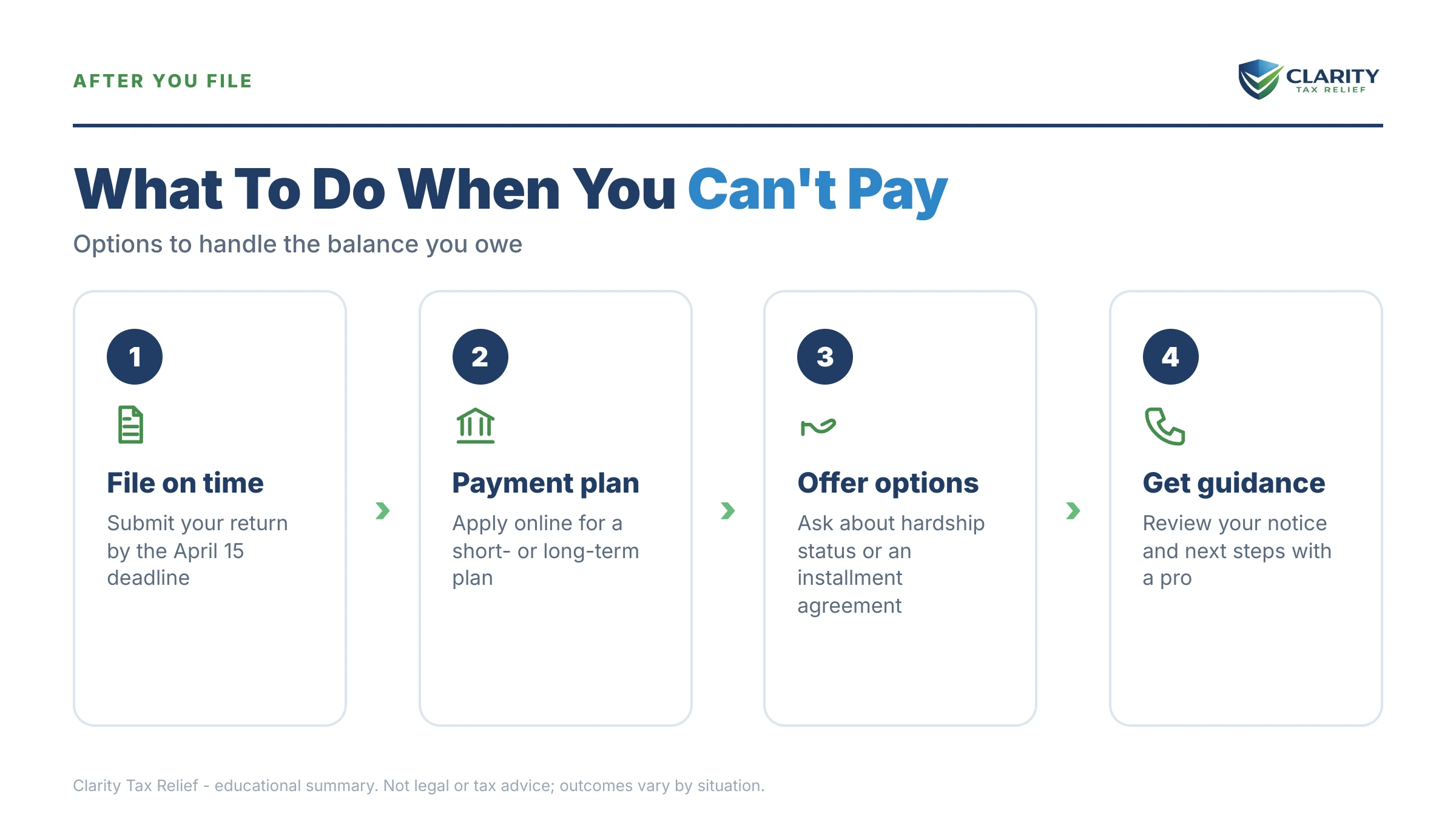

Your payment options once you file

Filing doesn't obligate you to pay the balance immediately — it qualifies you for programs that fit the balance to your finances. Which one applies depends mostly on how much you owe and what you can genuinely afford:

| Option | Who may qualify | Cost & terms |

|---|---|---|

| Short-term payment plan | You can pay in full within 180 days | $0 setup fee; penalties and interest continue until paid |

| Long-term installment agreement | Combined balance of $50,000 or less can be set up online | Up to 72 months; setup fee (reduced or waived for low income); failure-to-pay rate typically drops to 0.25%/month |

| Guaranteed installment agreement | You owe $10,000 or less in tax and have a clean recent filing history | The IRS must accept it if you can pay within 3 years |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living expenses (shown on Form 433-F) | Free; collection pauses, but the debt remains and keeps growing; reviewed periodically |

| Offer in Compromise | Your assets and future income genuinely can't cover the debt — a means test, not a discount program | $205 fee plus 20% down on lump-sum offers (both waived with low-income certification); the IRS accepted roughly 1 in 5 offers in FY2024 |

| Penalty abatement | Clean compliance for the prior 3 years, or circumstances beyond your control | Free to request; removes penalties, not the tax or interest |

The full decision framework for choosing between these — and how to apply for each without paying anyone — lives in our DIY pillar, how to settle tax debt yourself. On penalties specifically, first-time penalty abatement can wipe out an entire year's failure-to-pay penalty if your prior three years were clean — and starting in summer 2026, the IRS is replacing it with an Automatic Exemption from Penalty (AEP) that applies without a request, so don't assume a formal letter is your only path.

Worked example: a gig worker, three years unfiled, $31,200 owed

Say you drive and deliver on 1099s, you haven't filed for three years, and the tax across those years totals $31,200 — roughly $10,400 per year, most of it self-employment tax that no one withheld. This is a hypothetical, but the arithmetic is real:

- Failure-to-file penalty: every year is more than five months late, so the filing penalty has already maxed out — up to 25% × $31,200 = $7,800 across the three years.

- Failure-to-pay penalty: 0.5% × $31,200 = $156 per month, still accruing on every unpaid year until its own 25% cap.

- Interest: compounding daily on the tax and the penalties.

- Illustrative total: depending on how old each year is, the $31,200 could plausibly stand somewhere around $42,000 by the time you file — an illustration, not a quote for your case.

Now the path out. Because the total is still under $50,000, you can file all three returns and set up a 72-month online installment agreement: roughly $42,000 ÷ 72 ≈ $585 per month, with interest continuing but the penalty rate cut in half once the plan is approved. If the numbers genuinely don't work — income too low, no assets — Currently Not Collectible or an offer in compromise become the conversation instead.

Compare the do-nothing path: the IRS's substitute returns would tax your gross 1099 income. If you grossed $58,000 a year but had $17,000 in mileage and expenses, the SFR ignores all $17,000 — per year. The assessed debt could land dramatically above $31,200, and every penalty would be computed on that inflated figure. Filing your own returns, with your own deductions, is the single biggest dollar decision in this whole situation. If the three-years-behind part is your real worry, our guide for people who haven't filed taxes in 3 years walks that catch-up specifically.

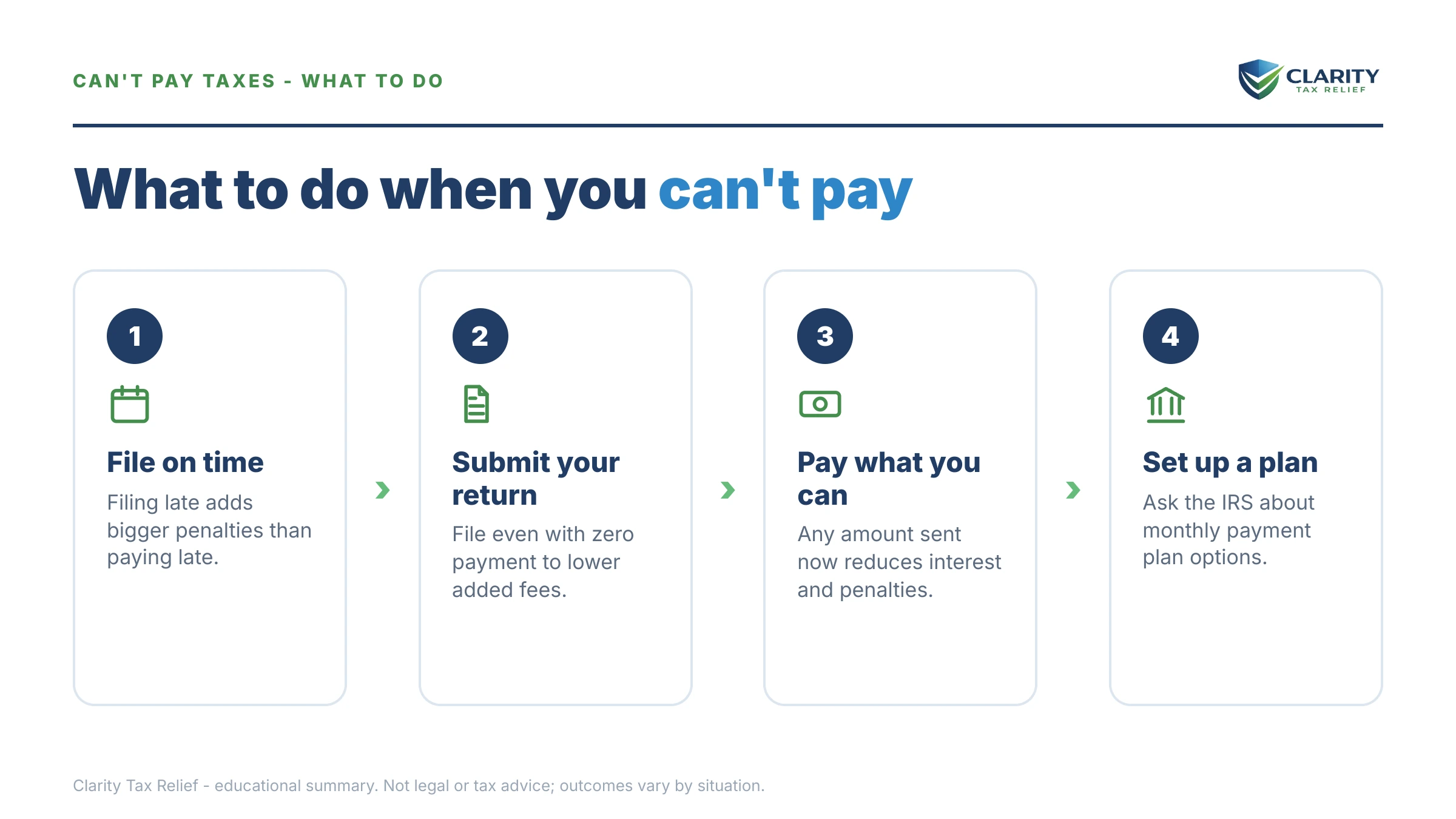

How to file when you can't pay, step by step

- Pull your income records — get your wage and income transcripts from your IRS online account so every 1099 and W-2 the IRS has on file is accounted for before you prepare anything.

- Prepare every missing return, oldest year first — real deductions, mileage, and expenses go on a real return; that is what beats the IRS's no-deduction version of your year.

- File now, with or without money — filing stops the 5%-per-month failure-to-file clock the month each return goes in, even if you send $0 with it.

- Pay anything you can with each return — every dollar shrinks the base that penalties and daily interest are computed on.

- Set up a payment arrangement — apply online for a short-term plan or installment agreement before the first bill arrives, so the collection sequence never starts. Our walkthrough for setting up an IRS payment plan online covers each screen.

- Request penalty relief after the balances post — first-time abatement or reasonable-cause relief can remove penalties once the returns are processed and the amounts are assessed.

If you file and don't set up a plan, expect a CP14 bill for each balance-due year within weeks of processing. That's not a crisis — it's the first, cheapest notice — but don't sit on it either; here's exactly what to do if you got a CP14 and can't pay.

When you can handle this yourself — and when help changes the outcome

Most people asking this question can fix it themselves. If you're missing only this year's return, you have your 1099s and records, and the balance is under $50,000, the entire fix is: file, then set up the online plan. That's a weekend project, and you don't need to pay anyone. The same is true if you missed April because money was tight — the playbook in can't pay taxes by April 15 is fully DIY.

Experienced help changes the outcome in specific situations: multiple unfiled years where an SFR has already been assessed (that requires filing corrected returns against an existing assessment, not just filing), self-employment years where records have to be reconstructed from bank statements and app data, a balance near or above the $50,000 online threshold where financial disclosure kicks in, a levy or garnishment already in motion, or offer-in-compromise math where the sequencing of filings, abatements, and the offer itself moves the final number. A hardship-driven situation — a layoff, a medical crisis — also changes which program fits; see lost my job and can't pay the IRS for that version of this problem.

Two honest notes. First, free help exists: the Taxpayer Advocate Service can intervene when the IRS process itself is causing hardship. Second, whatever you can pay goes furthest through official channels — IRS.gov/payments for direct payments, and the IRS payment plans page for the plan applications themselves. No legitimate professional will tell you to pay them before you understand which of those you're eligible for.

Terms you'll run into, decoded

- Substitute for return (SFR): a return the IRS files for you using only the income documents it holds — no deductions, worst-case filing status, maximum tax.

- Failure-to-file penalty: 5% of the unpaid tax per month a return is late, capped at 25%.

- Failure-to-pay penalty: 0.5% of the unpaid balance per month, capped at 25%; typically halved to 0.25% while an installment agreement is in good standing.

- Refund statute (RSED): the three-year window to claim a refund from an unfiled year; after it closes, the refund is forfeited permanently.

- CSED: the 10-year limit on IRS collection — it starts at assessment, which can't happen for a year that was never filed.

- Voluntary compliance: filing before the IRS forces the issue — the posture that unlocks penalty relief and keeps the whole matter civil.

Filing when you can't pay: your questions, answered

Should I file my taxes even if I can't pay anything?

Yes — file on time even if you can't send a single dollar with the return. The failure-to-file penalty runs 5% of the unpaid tax per month, while the failure-to-pay penalty is only 0.5% per month, so filing cuts your monthly penalty by roughly 90%. Filing also starts the clocks that eventually protect you, including the 10-year collection statute.

What is the penalty if I file but don't pay?

The failure-to-pay penalty is 0.5% of the unpaid balance per month, up to a maximum of 25%, plus interest that compounds daily. On a $10,000 balance that's $50 a month in penalty. If you set up an installment agreement, the monthly rate is typically cut in half to 0.25% while the agreement stays in good standing.

What happens if I never file at all?

The IRS eventually files a substitute for return (SFR) using the 1099s and W-2s it already has — single filing status, no dependents, and no business deductions. For a gig worker, that means tax on gross 1099 income with no mileage or expense write-offs, so the assessed balance is usually far larger than a correct return would show. Once assessed, that balance moves into normal IRS collections, liens and levies included.

Can I just file an extension if I can't pay?

An extension gives you more time to file, not more time to pay — the failure-to-pay penalty and interest start on the original April deadline either way. It still helps, because it prevents the much larger 5%-per-month failure-to-file penalty during the extension period. But if the deadline has already passed, an extension is no longer available; the fix is to file now.

Can I still get a refund from an unfiled year?

Only within three years of the return's original due date. File after that window and the refund is gone permanently — the IRS keeps it and won't apply it to other years you owe. If any of your unfiled years had withholding or refundable credits, file those years first, before the deadline expires.

Can I go to jail for not filing taxes?

Willful failure to file is a misdemeanor that can carry criminal penalties, but prosecution is rare and reserved for large, deliberate cases. Voluntarily filing your late returns before the IRS contacts you about them is exactly what the system is designed to reward. The realistic consequences of not filing are financial — penalties, interest, and a substitute return — not handcuffs.

How many years of unfiled returns do I need to file?

The IRS's general policy is six years of back returns to be considered compliant, though it can require more in unusual cases. If you have three unfiled years, file all three — you can't get a payment plan, penalty relief, or an offer in compromise while any required return is missing. Start with the oldest year so payments and carryovers flow forward correctly.

Your next 24 hours

- Log into (or create) your IRS online account and pull the wage and income transcript for each unfiled year — that's the complete list of 1099s and W-2s the IRS is already holding against your name.

- Gather your expense records — mileage logs, delivery-app annual summaries, bank statements — for each year. Deductions are the difference between your real return and the IRS's worst-case version.

- Get a free case review — call (888) 825-7779 or use the 2-minute form. Every unfiled month adds up to 5% of the balance in penalty and interest compounds daily, so the cheapest day to start filing is today.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.