Bankruptcy & Tax Debt

Chapter 13 and IRS Back Taxes: What Gets Paid, What Gets Discharged (2026)

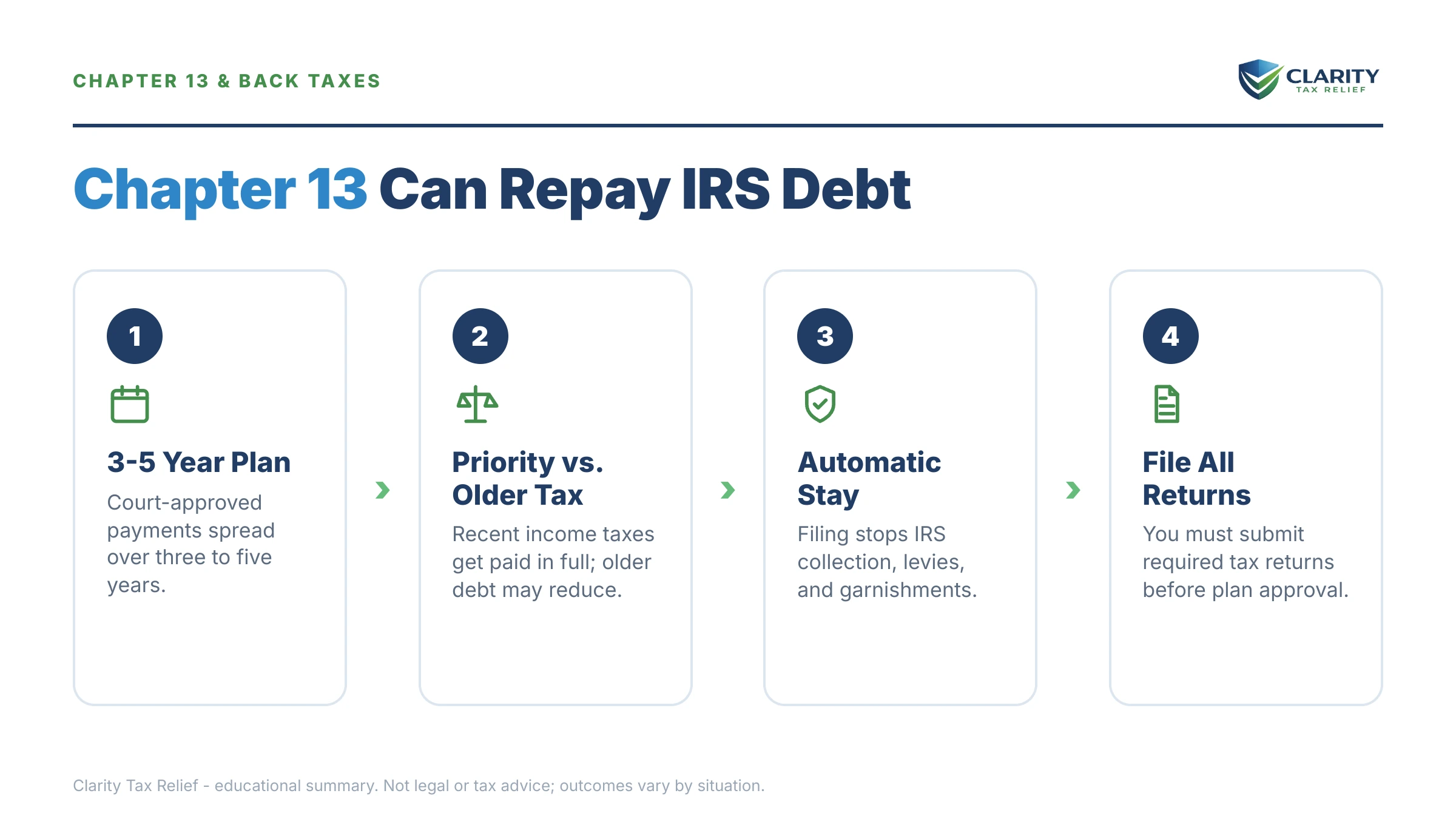

The short answer: Chapter 13 bankruptcy stops IRS levies the day you file and pays your back taxes through a 3-to-5-year court-supervised plan. Income taxes first due within the last three years must be paid in full; older income taxes and most tax penalties can be discharged when you complete the plan.

Maybe a bankruptcy attorney floated it, or a 2 a.m. search did: you're a 1099 worker with three years you never filed, a balance the IRS puts around $76,400, and now the question of whether Chapter 13 can carry IRS back taxes at all. Putting "bankruptcy" and "IRS" in the same sentence feels like admitting defeat — but the mechanics are more favorable than most people expect, and they follow rules you can check year by year.

Three rules decide everything: the automatic stay freezes IRS collection the moment you file, "priority" taxes (roughly, the last three years) must be paid at 100 cents on the dollar through the plan, and older taxes can be discharged — but only if the returns were actually filed. That last rule is where unfiled years become the whole ballgame.

⏱ The clock that matters: Chapter 13 has no IRS notice deadline — but under 11 U.S.C. §1308, every tax return for the four years before your petition must be filed by the day before your first scheduled meeting of creditors, typically held within weeks of filing. Miss that window and your case can be dismissed or converted.

Why Chapter 13 keeps coming up when you owe IRS back taxes

Chapter 13 is the only tax-debt path where a federal court — not the IRS — sets the repayment terms. Every IRS program is discretionary: the agency decides whether your installment agreement, hardship status, or offer gets approved. A confirmed Chapter 13 plan binds the IRS whether it likes the terms or not.

That matters most in three situations. First, when a levy or garnishment is already in motion and you need it stopped today, not after weeks of phone queues. Second, when your balance is too large or your budget too tight for the payment the IRS demands. Third, when you have other debts — car loans, mortgage arrears, credit cards — that a single plan can organize alongside the tax debt.

It is not free relief. You'll pay a court filing fee, attorney fees, and a trustee commission that in most districts runs up to 10% of every plan payment, and the case sits on your credit history for years. If your only problem is the IRS, one of the non-bankruptcy paths in our guide to how to settle tax debt yourself may cost far less — the comparison table below puts real numbers on that. And if your tax years are old enough to discharge outright, Chapter 7 vs. 13 for tax debt is the first fork in the road.

What the automatic stay stops — and what it doesn't

The automatic stay halts IRS levies, wage garnishments, and collection lawsuits the moment your Chapter 13 petition is filed. No negotiation, no hold music — the IRS's collection systems flag your account (you'll see it as a code 520 transcript entry) and enforcement stops.

Concretely, the stay means: a continuous wage levy against your pay ends, new bank levies can't issue, and if a bank levy is sitting inside its 21-day holding period with the money not yet sent to the Treasury, your attorney can often get those funds released. The full mechanics are in does bankruptcy stop an IRS levy.

What the stay does not stop: the IRS can still audit you, assess tax, send you notices of deficiency, and demand missing returns — the Bankruptcy Code carves those out. It also doesn't erase a tax lien already recorded, and it doesn't excuse you from staying current on new taxes while the case runs. The stay buys structure and safety, not amnesia.

Which back taxes Chapter 13 can discharge: the 3-year, 2-year, and 240-day tests

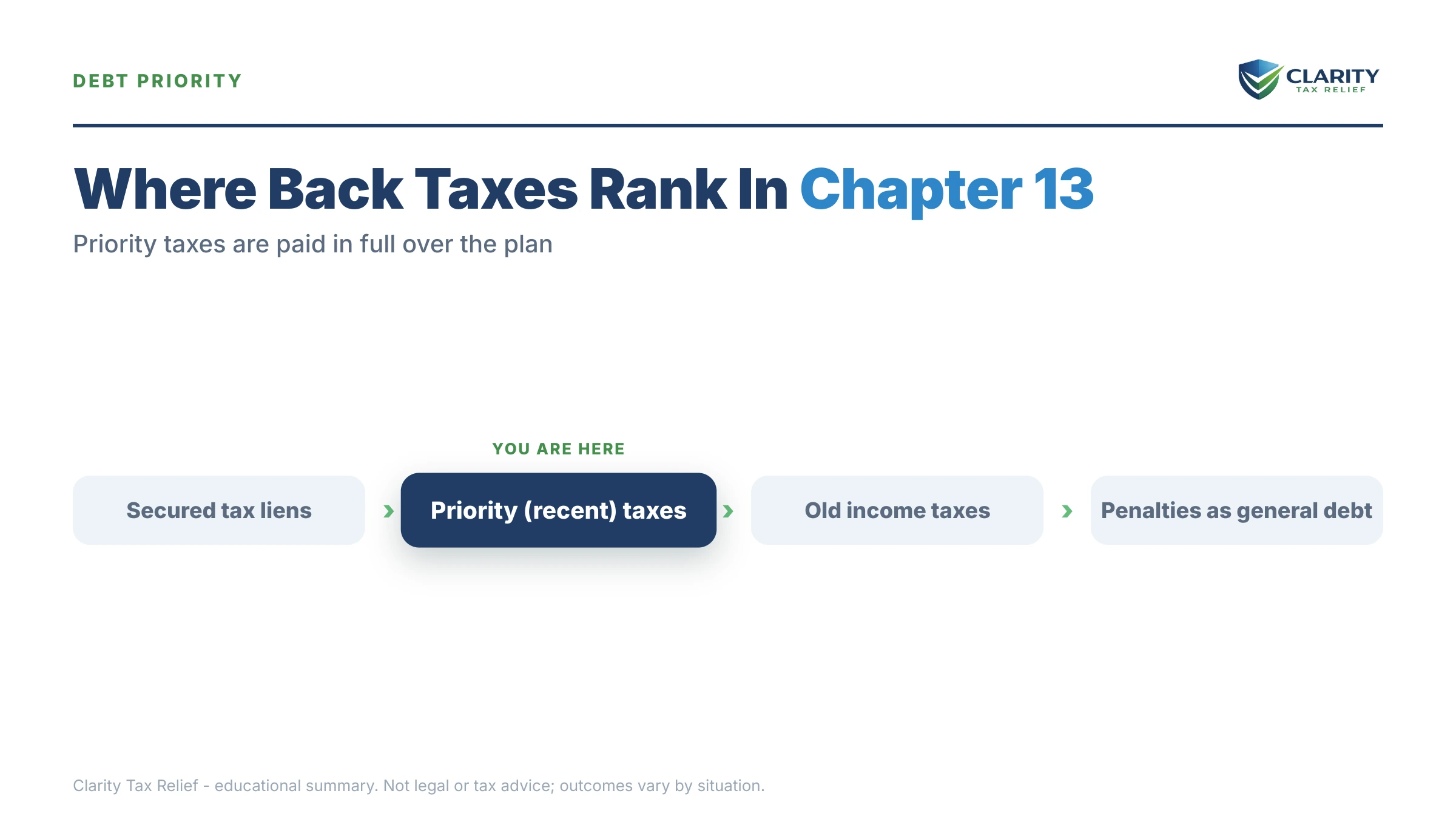

Income taxes first due within three years of your bankruptcy petition are "priority" claims that your Chapter 13 plan must pay in full. Everything else gets sorted by a set of date tests that decide whether a tax year rides in the front of the plan or gets discharged at the end. The full doctrine lives in our guide to the rules for discharging taxes in bankruptcy; here's how the buckets work inside a Chapter 13:

| Claim type | Which back taxes fall here | How your plan treats it |

|---|---|---|

| Priority unsecured | Income tax first due (including extensions) within 3 years of the petition; tax assessed within 240 days; withheld "trust fund" taxes of any age | Paid 100% through the plan — generally without new interest accruing while the case is open |

| Secured | Any tax covered by a federal tax lien recorded before the petition, up to the equity the lien actually reaches | Paid as a secured claim through the plan, typically with interest |

| General unsecured | Older income taxes that pass all three date tests; most tax penalties regardless of age | Paid the same percentage as your other unsecured creditors; the remainder is discharged at plan completion |

| Nondischargeable regardless of age | Taxes tied to fraudulent returns or willful evasion; in most courts, taxes for years you never filed or the IRS filed for you | Survive the case unless paid — see the filing requirement for discharge before assuming anything falls here |

The date tests themselves are mechanical. A tax year is potentially dischargeable only if all three pass: the return was due more than 3 years before the petition, the return was actually filed more than 2 years before the petition, and the tax was assessed more than 240 days before the petition. Here's what that looks like for a petition filed in July 2026:

| Tax year | Return due date | Likely status in a July 2026 petition |

|---|---|---|

| 2025 | April 15, 2026 | Priority — inside the 3-year window; the plan must pay it in full |

| 2024 | April 15, 2025 | Priority — inside the 3-year window |

| 2023 | April 15, 2024 | Priority — inside the 3-year window |

| 2022 | April 15, 2023 | Potentially dischargeable — but only if the return was filed at least 2 years before the petition and the tax was assessed 240+ days ago |

| 2021 and older | April 15, 2022 or earlier | Potentially dischargeable under the same tests — extensions, prior bankruptcies, and offer periods can shift every window |

Two traps hide in that table. An extension you filed years ago pushes the "due date" — and the 3-year clock — to October, not April. And tolling events (a prior bankruptcy, a pending offer, a collection due process hearing) freeze the clocks, which is why recent taxes aren't dischargeable even when the calendar looks close. Never eyeball these dates; pull transcripts and count precisely.

Three years unfiled? The §1308 rule can sink the whole case

Under 11 U.S.C. §1308, every tax return for the four years before your petition must be filed before your first meeting of creditors — or your Chapter 13 can be dismissed. For a gig worker who hasn't filed in three years, this is the single most important paragraph on this page.

The sequence is unforgiving: the 341 meeting is usually scheduled within weeks of the petition, and the returns must be in by the day before that meeting. The trustee can hold the meeting open briefly, but the IRS can move to dismiss or convert a case built on unfiled years. Filing bankruptcy does not make the returns optional; it makes them urgent.

There's a second reason to file those returns carefully, not just quickly. If the IRS already prepared substitute returns for your missing years, or you file the returns late, most courts treat those years as nondischargeable forever — the debt can still be paid through the plan, but it will never be wiped away by discharge. For three recent unfiled years this matters less (they'd be priority and paid in full anyway), but for an old unfiled year it can be the difference between discharge and a debt that follows you out of bankruptcy.

Practical order of operations: reconstruct income from your 1099s and IRS wage-and-income transcripts, claim every legitimate expense (mileage, platform fees, supplies — gig returns filed without deductions overstate the debt badly), and get the returns filed before the petition whenever possible so the numbers in your plan are real, not estimates.

What a federal tax lien does to your Chapter 13

A federal tax lien recorded before your petition survives Chapter 13 — the bankruptcy discharges people, not liens. The lien converts part of your tax debt into a secured claim, sized to the equity it actually reaches: your car, your house, even the value of household goods in some cases.

Inside the plan, that secured slice generally gets paid with interest, while the rest of the same tax year may be priority or unsecured. The upside: no new lien can be filed while the stay is in effect, and once the secured claim is paid or the liability resolved, the IRS releases the lien. The details — including what happens to lien rights after discharge — are in does bankruptcy remove a tax lien.

If no lien has been filed yet, that's a genuine timing advantage of acting now: filing the petition before the IRS records a lien keeps that entire slice of debt unsecured — and, if it's old enough, dischargeable.

A worked example: $76,400, three unfiled years, one 60-month plan

Say you're a gig worker filing Chapter 13 in July 2026 owing $76,400 across four tax years. This is hypothetical, but the arithmetic is exactly how a real plan gets built:

- 2021 — filed on time in April 2022, $19,400 still owed (including roughly $5,200 of penalties and interest). Due more than 3 years ago, filed more than 2 years ago, assessed long past 240 days: general unsecured.

- 2023, 2024, 2025 — never filed. You prepare and file all three now under §1308; tax plus additions comes to $57,000. All three were due within 3 years of the petition: priority, payable in full.

The priority math: $57,000 ÷ 60 months = $950/month for the tax alone. Add the trustee's commission (up to 10% in most districts) and the tax side of the plan runs roughly $1,045/month. If the plan pays general unsecured creditors 10%, the 2021 debt adds about $1,940 over five years — call it $32/month — bringing the payment to roughly $1,080/month before any attorney fees paid through the plan.

What you get for that: levies stop on day one, post-petition interest generally stops accruing on the unsecured tax claims, and at month 60 the remaining ~$17,460 of the 2021 balance is discharged. Compare the alternative: outside bankruptcy, the full $76,400 keeps compounding — see how IRS interest compounds on back taxes — until every dollar plus growth is paid or the collection statute runs out.

Now flip the facts and the answer flips too: if most of the $76,400 were from 2019–2021 returns you filed on time, those years might discharge in a cheaper, faster Chapter 7 — or shrink dramatically in an Offer in Compromise. The year-by-year date math, not the total, decides the right tool.

What happens if you do nothing — or your Chapter 13 fails

A $76,400 IRS debt left alone moves through an automated escalation sequence that ends in levies — and at that balance, passport certification. IRS staffing is down sharply after the 2025 workforce cuts, but the notice-and-levy machinery is automated and never stopped. The stages, in order:

- Bills and reminders — CP14, then CP501/CP503. No enforcement yet, but the failure-to-pay penalty and daily-compounding interest grow the balance every month.

- CP504 — Notice of Intent to Levy. The IRS can now seize your state tax refund, and a federal tax lien filing becomes likely, converting future bankruptcy leverage into secured debt.

- LT11 / Letter 1058 — Final Notice. A 30-day clock starts, along with your Collection Due Process appeal rights. After it runs, levies are authorized.

- Levies. Bank accounts (with a 21-day hold before funds leave), continuous wage levies, and — the gig-economy version — one-time levies served on the platforms and clients that pay your 1099 income.

- Passport certification. At $76,400 you are above the $66,000 seriously-delinquent threshold for 2026, so the IRS can certify your debt to the State Department, blocking passport issuance or renewal.

There's a second failure path this article's siblings don't face: a Chapter 13 that dies mid-plan. Most cases fail through missed plan payments or new unpaid tax years. When a case is dismissed, the stay evaporates, the IRS resumes exactly where it left off — and because the collection statute was paused the whole time, it resumes with more runway, not less. A Chapter 13 you can't realistically fund for 60 months is worse than never filing one.

Weighing Chapter 13 against your IRS back taxes?

Before you pay a bankruptcy retainer, get a free year-by-year review of your balance — which years are priority, which could discharge, and whether an IRS program would cost less. Interest and penalties are compounding while you decide; the review takes minutes.

Chapter 13 vs. your other options for IRS back taxes

Chapter 13 is one of four realistic paths for a five-figure IRS debt, and it is rarely the cheapest — it wins on speed of protection and forced terms, not price. Here's how the options stack up against a balance like $76,400 (note that above $50,000, an installment agreement requires financial disclosure rather than the streamlined online setup):

| Option | Upfront cost | Timeline | What happens to the balance |

|---|---|---|---|

| Chapter 13 plan | Court filing fee (a few hundred dollars) plus attorney fees, often paid partly through the plan; trustee keeps up to 10% of payments | 36–60 months | Levies stop at filing; priority years paid in full; older filed years and most penalties can be discharged at completion |

| Installment agreement | Modest setup fee (reduced or waived for low-income taxpayers); balances over $50,000 require a financial statement | Until paid or the 10-year statute expires | Full balance plus ongoing interest and penalties; enforcement stops while you stay current |

| Offer in Compromise (Form 656) | $205 application fee plus 20% down on lump-sum offers — both waived with low-income certification (AGI ≤ 250% of poverty) | Months to two years for a decision; auto-accepted if the IRS doesn't decide within 2 years, with narrow exceptions - a returned or rejected offer stops the clock, and time during court disputes does not count | Settles only if $76,400 exceeds what the IRS could realistically ever collect from you; roughly 1 in 5 offers were accepted in FY2024 |

| Currently Not Collectible | $0 | Until your finances improve; reviewed periodically | Nothing is forgiven — levies pause during documented hardship while interest accrues and refunds are kept |

The head-to-head that matters most for people with genuinely limited means is bankruptcy or offer in compromise — an accepted offer can resolve even priority-age debt for less than full payment, but acceptance is means-tested math, never a promise, and a pending offer takes far longer than the stay takes to protect you. If a levy is already active, Chapter 13's day-one protection often decides the question by itself.

How to handle IRS back taxes in Chapter 13, step by step

- Pull your IRS transcripts. Get account and wage-and-income transcripts for every year so you know each balance, each assessment date, and which returns the IRS never received.

- File every missing return. Prepare and file all unfiled returns — before the petition if possible, and no later than the day before your first meeting of creditors under §1308.

- Date-test every tax year. Run each year through the 3-year, 2-year, and 240-day tests to sort priority debt you must pay in full from debt your plan can discharge.

- Price the alternatives. Compare the projected 60-month plan payment against an installment agreement, an Offer in Compromise, and Currently Not Collectible status before committing.

- Get both professional opinions. Have a bankruptcy attorney evaluate the case itself and an experienced tax professional evaluate the tax-side alternatives — the cheaper path is not always bankruptcy.

Refunds, interest, and the 10-year clock during your plan

Your tax refunds don't automatically become yours again just because you filed Chapter 13. The IRS can generally offset a refund from a pre-petition year against pre-petition tax debt, and in many districts the trustee requires refunds earned during the plan to be turned over as additional plan funding. The broader offset rules are covered in will the IRS take my refund for back taxes — the practical fix is adjusting withholding or estimates so you stop generating large refunds at all.

Interest works in your favor for once: post-petition interest generally stops accruing on unsecured tax claims while the case is open, which is a structural advantage over every IRS payment plan. The exception is secured claims — a lien-backed slice typically earns interest through the plan.

And the 10-year Collection Statute Expiration Date pauses for the entire bankruptcy, generally plus about six months afterward. That cuts both ways: a completed plan makes the CSED irrelevant for discharged years, but a dismissed case hands the IRS back all the time it lost. If part of your strategy involves how much collection time the IRS has left, estimate each year's deadline with our CSED Calculator before deciding whether a bankruptcy filing helps or hurts.

One more in-plan obligation: stay current. A self-employed debtor who skips quarterly estimated taxes during the plan builds exactly the kind of new balance that gets Chapter 13 cases dismissed in year three — after thousands paid in and no discharge to show for it.

When you can handle this yourself — and when help changes the outcome

You don't need Chapter 13 — or professional help — for every back-tax problem. If your returns are all filed, you owe under $50,000, and a streamlined 72-month installment agreement fits your budget, setting it up online yourself is faster and dramatically cheaper than any bankruptcy. Same if you can pay the balance within 180 days: a short-term plan costs nothing to set up and ends the problem.

Experienced help changes outcomes in the situations this article describes: a levy or garnishment already in motion, multiple unfiled years where the returns must be reconstructed and filed on a §1308 deadline, a lien on your home, date-test math where one tolling event flips a year from dischargeable to permanent, or a genuine Chapter 13 vs. Offer in Compromise decision where the two paths differ by tens of thousands of dollars. And one thing should never be DIY: the bankruptcy petition itself belongs in a bankruptcy attorney's hands — the tax-side analysis is where an experienced tax professional earns their fee, before you commit to a five-year plan.

Primary sources worth reading before any decision: the federal courts' Chapter 13 bankruptcy basics, the IRS's own page on declaring bankruptcy with tax debt, and — if the IRS mishandles your account during the case — the Taxpayer Advocate Service.

Terms in your case, decoded

- Automatic stay — the court order, effective the instant you file, that halts IRS levies, garnishments, and most collection against you.

- Priority claim — tax debt the plan must pay in full: recent income taxes and withheld trust-fund taxes of any age.

- Proof of claim — the IRS's formal statement of what you owe, split into secured, priority, and unsecured pieces; you can object if it's wrong.

- 341 meeting — the meeting of creditors held shortly after filing; the §1308 tax-return deadline is anchored to it.

- Discharge — the court order at plan completion that erases your remaining qualifying debts, including old dischargeable taxes.

- CSED — the Collection Statute Expiration Date, the IRS's 10-year collection deadline, which pauses during bankruptcy plus roughly six months.

Staring at three unfiled years and a five-figure balance and unsure whether the answer is a courtroom or an IRS program? An experienced tax professional can sort your priority years from your dischargeable ones for free before you spend a dollar on either path — call (888) 825-7779 or use the 2-minute form.

Chapter 13 and IRS debt: your questions, answered

Can Chapter 13 discharge IRS back taxes?

Partially. Income taxes first due within three years of your petition are priority debts your plan must pay in full, while older income taxes — if the returns were filed on time or at least two years before the petition — plus most tax penalties can be discharged when you complete the plan. Taxes tied to fraud or returns you never filed generally survive no matter how old they are.

Can I file Chapter 13 with unfiled tax returns?

You can file the petition, but you cannot keep the case alive without catching up. Under 11 U.S.C. §1308, all returns for the four years before your petition must be filed by the day before your first meeting of creditors, usually held within weeks of filing. Miss that window and the IRS or the trustee can move to dismiss or convert your case.

Does Chapter 13 stop IRS wage garnishment and bank levies?

Yes — the automatic stay takes effect the moment your petition is filed, and the IRS must stop wage garnishments and new bank levies immediately. If a bank levy is inside its 21-day holding period and the money hasn't been turned over yet, your attorney can often get it released. The stay does not stop audits, assessments, or demands that you file missing returns.

Will the IRS take my tax refund during Chapter 13?

Often, yes — one way or another. The IRS can typically offset a refund from a pre-petition tax year against pre-petition tax debt, and in many districts the Chapter 13 trustee requires refunds earned during the plan to be paid in as extra plan funding. Adjusting your withholding or estimated payments so you don't generate large refunds is usually the smarter move.

What happens to IRS penalties and interest in Chapter 13?

Most tax penalties are treated as general unsecured claims in Chapter 13, paid only at whatever percentage your plan pays other unsecured creditors, with the rest discharged at completion. Post-petition interest generally stops accruing on unsecured tax claims while the case is open. That is a real advantage over an installment agreement, where interest compounds on the full balance until the last payment.

Does Chapter 13 remove a federal tax lien?

No. A lien recorded before your petition survives the bankruptcy and stays attached to property you owned on the filing date. Your plan treats the lien as a secured claim up to the equity it actually reaches, and the IRS releases it once that secured amount is paid or the underlying liability is resolved. Chapter 13 does prevent new lien filings while the stay is in effect.

What happens if I owe new taxes while I'm in Chapter 13?

New post-petition tax debt is one of the most common reasons Chapter 13 cases fail. You must file and pay each year's taxes on time during the plan; a new balance can push the trustee or the IRS to seek dismissal, and a dismissed case sends the full remaining debt straight back to IRS collections. Self-employed filers should build quarterly estimated payments into the budget from day one.

Does bankruptcy pause the IRS 10-year collection statute?

Yes. The Collection Statute Expiration Date stops running for the entire time the automatic stay is in effect, generally plus about six additional months afterward. That means a dismissed Chapter 13 doesn't run out the clock — the IRS gets back every month the case consumed, and more. Debts discharged at plan completion, by contrast, are gone regardless of the CSED.

Is Chapter 7 or Chapter 13 better for IRS back taxes?

It depends mostly on the age of the taxes and your income. Chapter 7 is faster and cheaper if your tax years already pass the discharge tests and you qualify under the means test. Chapter 13 usually fits better when recent priority taxes dominate the balance, a levy is in motion, or you have property equity to protect — the plan buys 60 months of court-supervised breathing room.

Your next 24 hours

- List every year with a problem. Log into your IRS online account or pull transcripts and write down each tax year, its balance, its assessment date, and whether you actually filed a return for it — the date tests can't be run without this list.

- Gather the raw material. Collect your 1099s and income records for the unfiled years, your last filed return, and any IRS notices you've received — especially anything mentioning intent to levy.

- Get the year-by-year review — free. Interest and penalties compound on the full balance every month you wait, and a lien filing can convert dischargeable debt into secured debt. Call (888) 825-7779 or use the 2-minute form, and an experienced tax professional will map which years Chapter 13 would pay, which it could discharge, and whether an IRS program beats both. (Balances are payable anytime at IRS.gov/payments if you'd rather simply pay a year down.)

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. Bankruptcy decisions should be made with a bankruptcy attorney licensed in your state.