Tax Debt Relief

Does Bankruptcy Clear IRS Debt? What Chapter 7 and Chapter 13 Actually Wipe Out (2026)

The short answer: bankruptcy can clear IRS debt — but only income taxes that pass three date tests: the return was due at least 3 years ago, filed at least 2 years ago, and assessed at least 240 days before your petition. Recent taxes, payroll taxes, fraud years, and recorded tax liens survive.

So the answer to "does bankruptcy clear IRS debt" is not yes or no — it's which years. Maybe you and your spouse are sitting at the kitchen table with three years of IRS statements totaling $92,700, wondering whether one court filing could end all of it. Part of it probably could. Part of it almost certainly can't — and knowing which is which, before you file anything, is the entire game.

⏱ The clock that matters: there's no notice deadline on this question — the calendar itself is the eligibility test. Every discharge rule is measured backward from the day your petition is filed: 3 years from the return due date, 2 years from filing, 240 days from assessment. Filing even a few weeks too early can leave an entire tax year on your back — and penalties and interest keep accruing monthly on everything until you act.

Does bankruptcy clear IRS debt? Three date tests decide

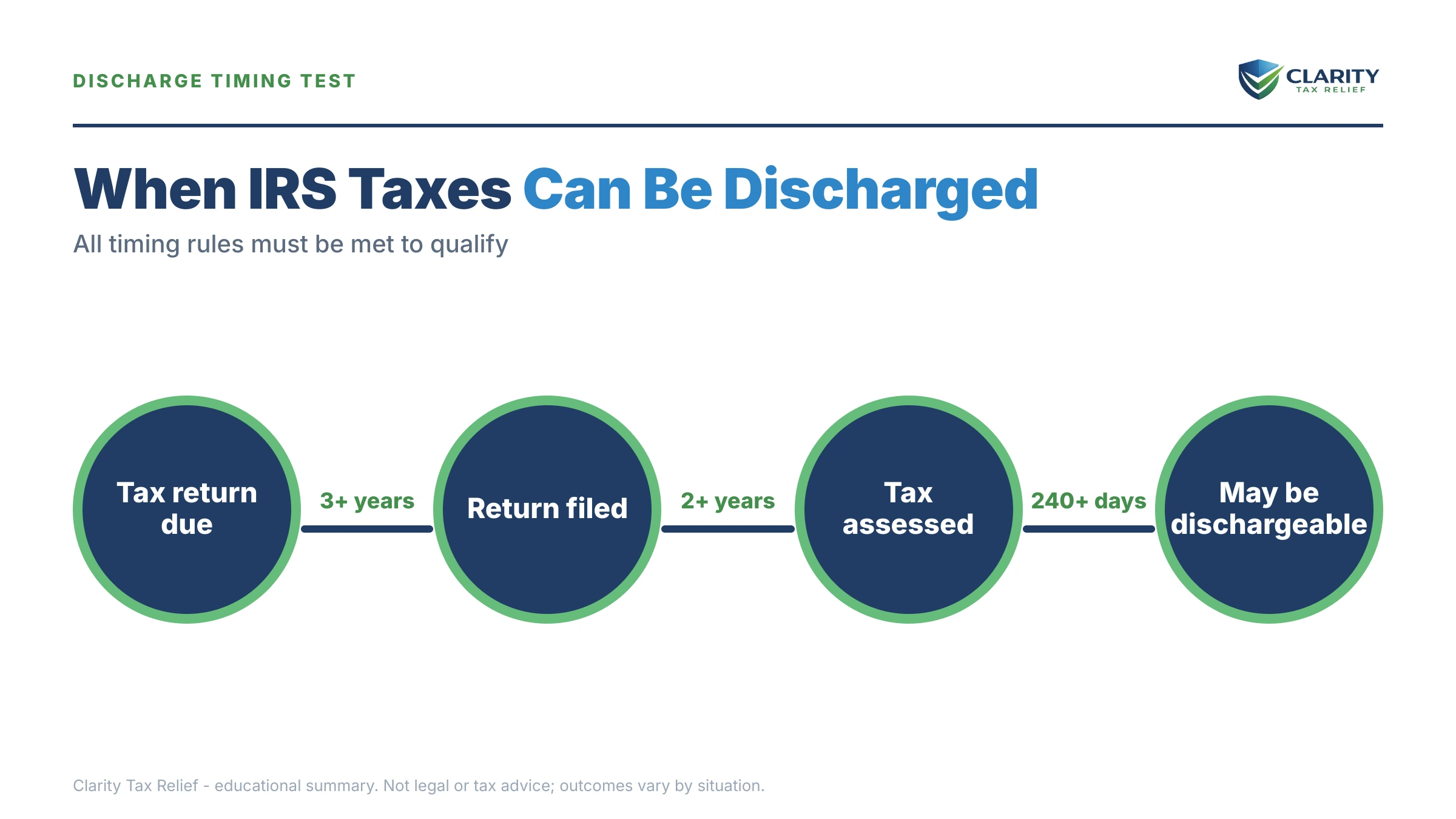

Bankruptcy clears IRS income tax only when the debt passes three timing tests measured from your petition date: the 3-year, 2-year, and 240-day rules. All three must pass, for each tax year, plus two more conditions — a real return was filed, and there was no fraud or willful evasion.

Each tax year on your account is judged separately. That's why one bankruptcy can erase your 2021 balance while your 2024 balance walks out of court untouched. The dates come from your IRS account transcripts, not from memory — an assessment date that's off by a month can flip a year from dischargeable to permanent.

| Test | What it requires | Example (petition filed July 2026) |

|---|---|---|

| 3-year rule | The return was due — including extensions — at least 3 years before your petition | 2021 return due April 2022 → passes after April 2025 |

| 2-year rule | You actually filed the return at least 2 years before your petition | Return filed June 2023 → passes after June 2025 |

| 240-day rule | The IRS assessed the tax at least 240 days before your petition | Assessed in 2022 → passed long ago; a fresh audit assessment restarts this clock |

| No fraud or evasion | The return wasn't fraudulent and you didn't willfully evade payment | A fraud finding makes that year permanently nondischargeable |

Two traps hide inside these clean-looking rules. First, certain events pause the clocks — a prior offer in compromise, a previous bankruptcy, or a collection due process appeal can add months to the waiting periods. Second, if the IRS filed a substitute return for a year you skipped, most courts treat that year as never properly filed — see our guide to unfiled returns bankruptcy rules. The full date-math walkthrough lives in our guide to how to discharge taxes in bankruptcy.

Chapter 7 vs. Chapter 13: two very different answers

Chapter 7 erases qualifying tax years outright, typically within a few months; Chapter 13 repays the surviving taxes through a court-protected plan lasting 3 to 5 years. Which one you can use — and which one helps — depends on your income and on how much of your debt passes the tests above.

Chapter 7 requires passing the means test: roughly, your household income falls below your state's median for your family size, or your budget shows you genuinely can't repay. For a married couple filing jointly, both incomes count. If most of your tax debt is old enough to discharge, Chapter 7 is the cleaner tool.

Chapter 13 fits when much of the debt is too new to discharge, or when you have assets — home equity, for instance — you'd risk in Chapter 7. The nondischargeable "priority" taxes get paid in full through the plan, but under court protection, on a schedule the IRS can't unilaterally change. Our side-by-side on chapter 7 vs 13 tax debt breaks down which chapter fits which mix.

What bankruptcy never clears — and the lien problem

Bankruptcy never discharges trust-fund payroll taxes, fraud-based assessments, or income tax for years where no genuine return was filed. If you withheld taxes from employees' paychecks and didn't remit them, that debt follows you through any chapter, in any court, indefinitely.

The nondischargeable categories — recent income taxes, trust-fund taxes, fraud years — are what the bankruptcy code calls priority tax claims, and in Chapter 13 they must be paid in full through your plan. For a deeper look at why new balances always survive, see are recent taxes dischargeable.

Then there's the trap that surprises people most: a federal tax lien recorded before your petition survives the discharge. Bankruptcy wipes out your personal liability — the IRS can't garnish future wages for a discharged year — but the lien stays attached to everything you owned on filing day. Home equity, vehicles, even retirement accounts. If you sell the house, the lien gets paid from the proceeds. Full details in does bankruptcy remove tax lien.

Timing insight: if you're considering bankruptcy and no lien has been filed yet, that's a real strategic difference. Once the lien records, discharge becomes far less valuable for any equity you hold.

What filing does immediately: the automatic stay and the 10-year clock

The automatic stay stops IRS garnishments, bank levies, and most collection activity the day your petition is filed — no negotiation required. If a levy is already in motion, this is bankruptcy's most immediate power; we cover the mechanics in does bankruptcy stop irs levy.

But the stay cuts both ways. The IRS normally has 10 years from assessment to collect a tax debt, and bankruptcy suspends that 10-year clock for the entire case plus 6 months afterward. If your oldest debt was two years from expiring on its own, a bankruptcy that doesn't discharge it hands the IRS extra time to collect. Before filing, estimate your expiration dates with our CSED Calculator — for some readers, simply outlasting the statute is the better play.

What happens to $92,700 if you do nothing

A $92,700 IRS balance sits well above the $66,000 passport-certification threshold for 2026, which means doing nothing risks your passports on top of everything else. Whether or not bankruptcy is your answer, "wait and see" is the one option with no upside — the IRS's collection machine is automated and escalates on its own schedule:

- Balance-due notices — CP14, then CP501 and CP503 reminders. Bills only, but the failure-to-pay penalty and daily-compounding interest grow the balance every month.

- CP504 — Notice of Intent to Levy — the IRS can now seize your state tax refund, and a federal tax lien filing becomes likely. Once that lien records, bankruptcy loses much of its power over your home equity.

- LT11 / Letter 1058 — Final Notice — a 30-day clock starts on wage garnishment and bank levies, along with your Collection Due Process appeal rights.

- Enforcement — continuous wage levies, bank account seizures with a 21-day hold, and passport revoked for tax debt certification to the State Department for balances over $66,000.

In 2026 the IRS workforce is roughly 27% smaller than it was, which makes humans harder to reach — but every step above is issued by automated systems that never stopped running. The escalation happens whether anyone reads your file or not.

Weighing bankruptcy against a $92,700 IRS balance?

Before you pay a bankruptcy retainer, find out what would actually discharge — and whether an IRS program clears more for less. An experienced tax professional will pull your transcripts, run the date tests year by year, and map every option. Free and confidential, while interest is still compounding on the full balance.

Bankruptcy vs. the IRS's own programs: your options compared

The IRS runs its own resolution programs — payment plans, settlement, hardship status — and for many balances they beat bankruptcy on cost, credit impact, and certainty. Bankruptcy stays on your credit report for years; the IRS programs, by contrast, barely touch it (more on that in does owing the irs affect credit). Our hub on how to settle tax debt yourself walks through setting up each program; here's how they stack against filing:

| Option | What it does to the debt | Key eligibility / cost |

|---|---|---|

| Chapter 7 discharge | Erases qualifying income-tax years entirely | Must pass the means test; only years meeting the 3-year/2-year/240-day tests; court and attorney costs, credit impact for years |

| Chapter 13 plan | Repays surviving priority taxes over 3–5 years under court protection | Regular income required; nondischargeable taxes paid in full through the plan |

| Short-term IRS plan | Full payment within 180 days; collection stops | $0 setup fee; interest and penalties continue until paid |

| Long-term installment agreement | Monthly payments, up to 72 months | Online setup for balances ≤ $50,000; larger balances require financial disclosure |

| Offer in Compromise | Settles for what the IRS could realistically collect from you | $205 fee and 20% down on lump-sum offers (both waived with low-income certification); roughly 1 in 5 offers accepted in FY2024 |

| Currently Not Collectible | Pauses collection during genuine hardship; debt remains | Financial disclosure showing income can't cover basic living costs; interest keeps accruing |

One comparison deserves special attention: an offer in compromise can sometimes reach debt that bankruptcy can't — including recent years — because the OIC tests your ability to pay, not the debt's age. But it's means-tested and hard to win. The decision framework is its own article: bankruptcy or offer in compromise. And if you've heard the IRS "forgives" debt outright, read does the irs ever forgive tax debt — forgiveness always runs through one of these structured programs.

| Balance | Where bankruptcy fits | Usually the better first move |

|---|---|---|

| Under $10,000 | Almost never worth the cost for tax debt alone | Guaranteed installment agreement |

| $10,000–$25,000 | Rarely, unless it's buried in larger dischargeable debt | Streamlined installment agreement |

| $25,000–$50,000 | Competitive only if most years pass the date tests | Streamlined plan with direct debit, or an OIC if income is low |

| $50,000–$100,000 | Genuinely competitive when older years dominate the balance | Full-disclosure installment agreement or OIC — run both sets of math first |

| Over $100,000 | Often one piece of a layered strategy | Professional review before anything else; a revenue officer is likely involved |

Say you owe $92,700: how the discharge math plays out

Here's a clearly hypothetical example. Say you and your spouse owe $92,700 from jointly filed returns, broken down like this:

- $58,400 from tax year 2021 — return filed on time in April 2022, tax assessed that June. By a petition filed in July 2026, it passes all three tests: due more than 3 years ago, filed more than 2 years ago, assessed far more than 240 days ago. Dischargeable in Chapter 7 — assuming no fraud and no lien recorded first.

- $21,300 from tax year 2024 — the return was due in April 2025, barely a year ago. It fails the 3-year rule. Priority debt; survives any bankruptcy filed in 2026.

- $13,000 from tax year 2019 — you never filed, and the IRS created a substitute return. Because no real return was filed, most courts treat this year as never dischargeable, no matter how old it gets.

Run the arithmetic: $58,400 + $21,300 + $13,000 = $92,700. A well-timed Chapter 7 could erase the $58,400 — roughly 63% of the balance — leaving $34,300 to resolve. That remainder fits under the $50,000 online threshold, so a streamlined installment agreement over 72 months works out to roughly $477 a month before the interest that keeps accruing, call it about $500 in practice.

Now change one fact: the IRS recorded a lien in 2024, and you have $70,000 of home equity. The 2021 liability still discharges, but the lien survives against that equity — the discharge saved your future paychecks, not your house proceeds. Or change another fact: you wait until mid-2027 to file, and the $21,300 from 2024 becomes dischargeable too. Timing is worth real money in both directions, which is exactly why the transcripts come before the petition.

How to decide, step by step

- Pull your IRS account transcripts — get the account transcript for every year you owe; the exact return-filed and assessment dates printed on it decide everything.

- Run the three date tests on each year — sort every balance into "passes the 3-year, 2-year, and 240-day tests" or "survives bankruptcy," and check whether a lien has already been recorded.

- Price the alternatives — compare what bankruptcy would actually clear against an installment agreement, an offer in compromise, or hardship status on the full balance.

- Get two professional opinions — have a bankruptcy attorney and an experienced tax professional look at the same numbers; each sees traps the other can miss.

- Time your petition date — if a large year misses a test by weeks, waiting to file can move tens of thousands of dollars from "survives" to "discharged."

Bankruptcy itself is a federal court process — the courts' own overview at uscourts.gov explains the filing mechanics — while the tax treatment of your case runs through the IRS's rules, summarized on its declaring bankruptcy page.

When you can handle this yourself — and when the stakes demand help

If your balance is small enough to pay within 180 days, or fits a simple online installment agreement, you don't need a bankruptcy attorney or a tax firm — set it up yourself on the IRS payment plans page and be done. Bankruptcy costs real money — court fees plus attorney fees that commonly run into the low thousands for Chapter 7 — and it isn't worth that for a debt a $0-setup-fee plan can handle.

Experienced help changes outcomes in specific situations: a levy already in motion, multiple unfiled years (which block discharge entirely until fixed), trust-fund payroll debt, a lien racing your petition to the courthouse, or a balance like $92,700 where the discharge math, OIC math, and installment math all need to be run side by side. Getting the sequencing wrong — filing the petition before the returns, or after the lien — can cost more than any professional fee.

Bankruptcy tax terms, decoded

- Discharge — the court order that erases your personal obligation to pay a debt.

- Automatic stay — the instant freeze on collection (including IRS levies) that starts when your petition is filed.

- Priority tax claim — a tax debt the bankruptcy code protects from discharge, like recent income taxes and trust-fund payroll taxes.

- Federal tax lien — the IRS's recorded claim against your property, which survives discharge and stays attached to assets you owned at filing.

- CSED — the Collection Statute Expiration Date, the end of the IRS's 10-year window to collect, which bankruptcy pauses rather than shortens.

- Means test — the income screen that decides whether your household qualifies for Chapter 7.

- Substitute for Return (SFR) — a return the IRS files for you when you don't; it counts as an assessment but generally not as a "filed return" for discharge purposes.

Bankruptcy and IRS debt: your questions, answered

Does Chapter 7 wipe out IRS tax debt completely?

Only the tax years that pass the discharge tests. Chapter 7 can erase income tax that was due at least 3 years ago, filed at least 2 years ago, and assessed at least 240 days before your petition — with no fraud involved. Newer years, payroll taxes, and any tax lien recorded before you file all survive the case.

How old does tax debt have to be to file bankruptcy on it?

The return must have been due at least 3 years before your bankruptcy petition, counting extensions. So 2021 income tax, due in April 2022, generally became eligible in April 2025. But age alone isn't enough — the return also had to be filed at least 2 years ago and the tax assessed at least 240 days ago, and events like a prior offer in compromise can stretch those windows.

Does bankruptcy stop IRS garnishments and levies immediately?

Yes. The automatic stay takes effect the moment your petition is filed, and it requires the IRS to stop wage garnishments, bank levies, and most other collection during the case. It does not erase anything by itself — nondischargeable taxes resume collecting after the case ends, and the stay pauses the IRS's 10-year collection clock while it runs.

What happens to a federal tax lien after bankruptcy?

A lien recorded before your petition survives the discharge. Bankruptcy eliminates your personal liability for qualifying taxes, but the lien stays attached to property you owned when you filed — home equity, vehicles, and other assets. The IRS can't garnish future wages for a discharged year, but it can still collect from that pre-existing equity or get paid when you sell.

Does bankruptcy clear state tax debt too?

Often, under similar age-and-filing tests, but each state's collection rules differ and some are tougher than the IRS. California's FTB, for example, works with a 20-year collection statute — roughly double the IRS's 10 years — so a state balance that survives bankruptcy can follow you far longer. Have your attorney run every state year through the same analysis as your federal years.

Does bankruptcy pause the IRS 10-year collection clock?

Yes — the collection statute (CSED) is suspended for the entire bankruptcy case plus 6 months afterward. That means a Chapter 7 that runs four months adds roughly ten months to the life of any tax debt that survives. If you're close to the 10-year expiration date, filing bankruptcy can actually extend how long the IRS can collect from you.

Should a married couple file bankruptcy jointly for joint tax debt?

Usually a joint petition makes sense when the tax debt comes from jointly filed returns, because each spouse is liable for 100% of the balance. If only one spouse files, the discharge protects only that spouse — the IRS can still collect the full amount from the other. A joint case also combines court costs into a single filing.

Your next 24 hours

- Request your account transcripts for every year you owe, through your IRS online account — the return-filed date and assessment date on each one are the raw material of every decision above.

- Gather three things: your last two filed returns, any IRS notices you've received (especially anything mentioning a lien or intent to levy), and a rough monthly household budget for you and your spouse.

- Get the math run before you commit to anything. A free case review with an experienced tax professional — the 2-minute form at claritytaxrelief.com/#consult or (888) 825-7779 — will show you what bankruptcy would actually clear versus what an IRS program could do, while penalties and interest are still compounding on the full balance.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. Clarity Tax Relief does not provide bankruptcy legal services; bankruptcy petitions require a licensed attorney or pro se filing in federal court.