Tax Deadlines & Penalties

Does an Extension Give More Time to Pay? No — Here's What Form 4868 Actually Does (2026)

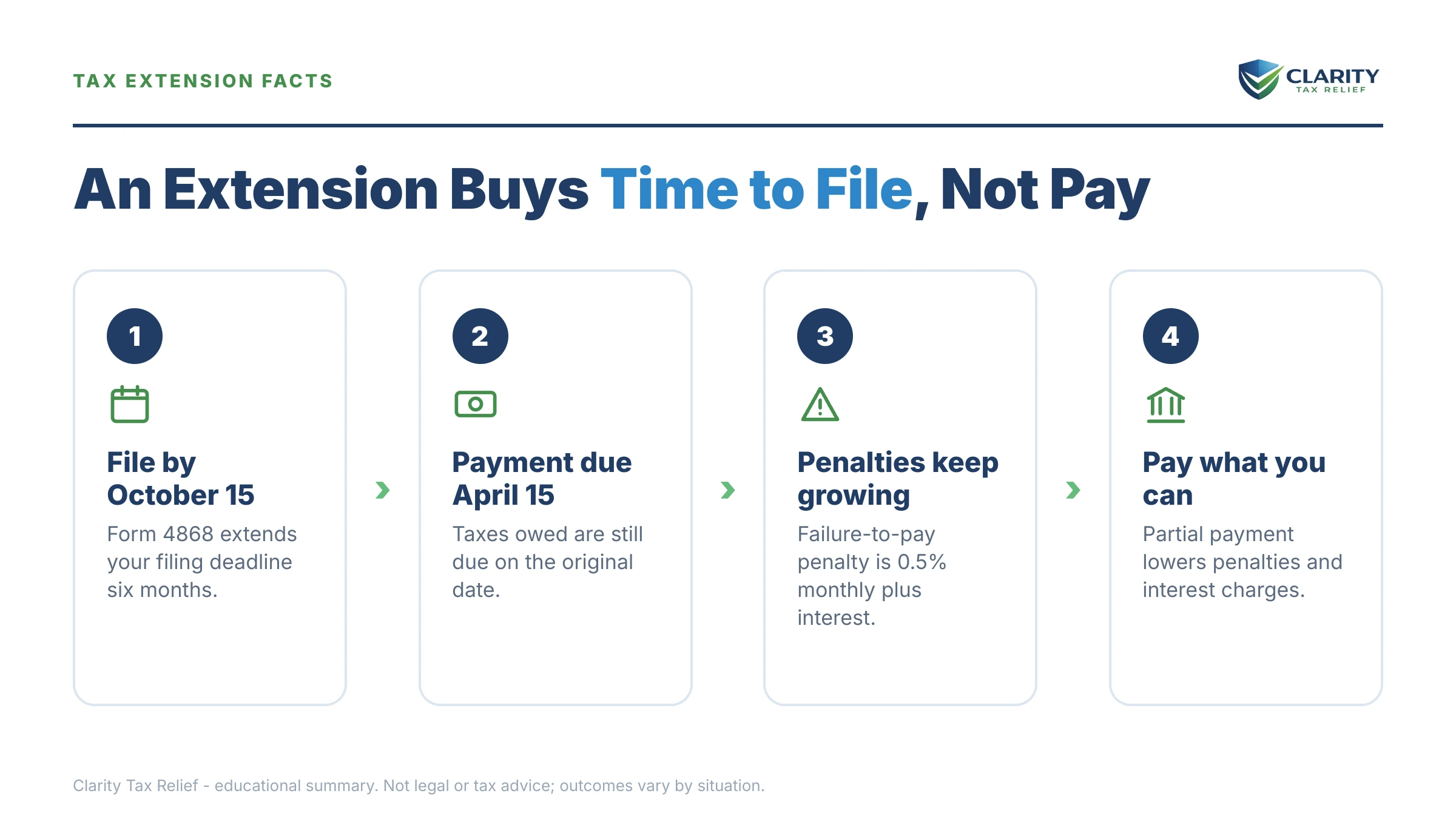

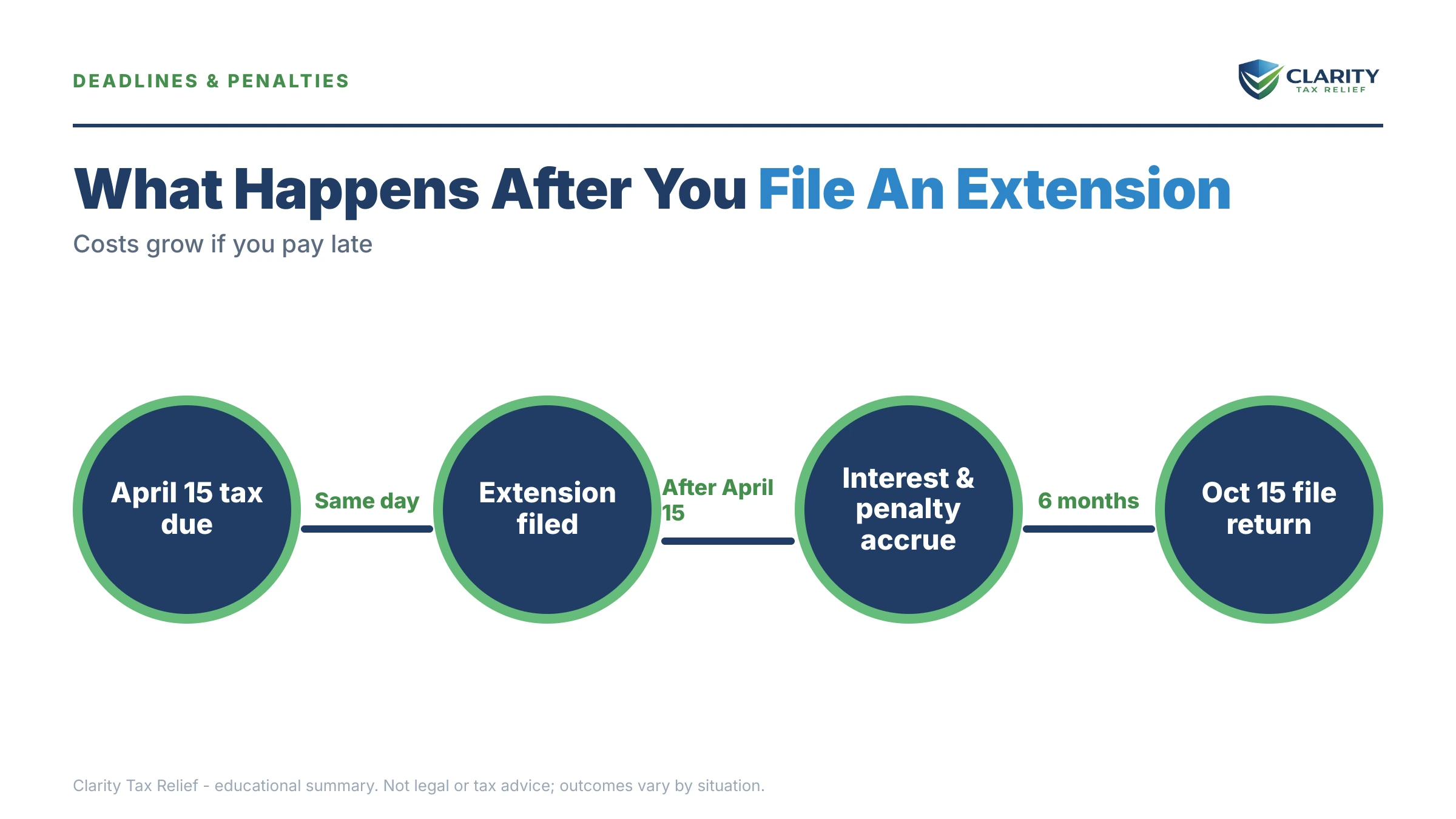

Does an extension give more time to pay? No. Form 4868 gives you six extra months to file — until October 15 — not to pay. Your payment was still due April 15, and the IRS charges a 0.5% monthly failure-to-pay penalty plus daily-compounding interest on any unpaid balance from that date forward.

You filed the extension in April, exhaled, and figured the tax bill could wait until fall. Now the IRS says you owe more than you did in the spring — and if the letters on your kitchen table have escalated to a levy warning, your paycheck or bank account is next in line. This is fixable, and the fastest fix depends on exactly which letter you're holding.

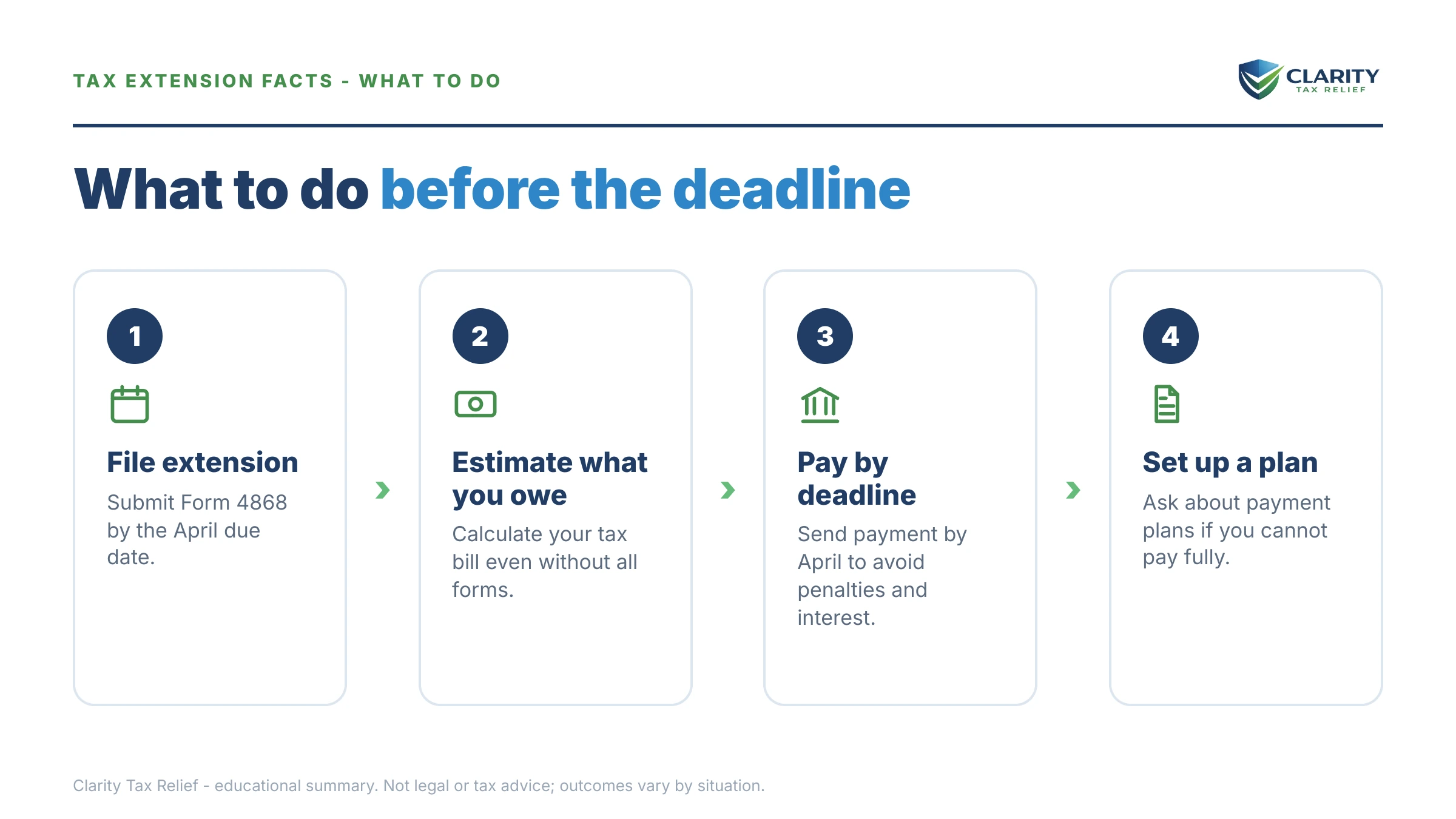

Part of the confusion starts with the form itself. Form 4868 actually asks you to estimate your tax and send a payment along with the extension request — the image below shows exactly what the form looks like and where that payment estimate sits, the part most people skip right past.

⏱ The clock that actually matters: an extension moves your filing deadline to October 15 — your payment deadline stays April 15. From April 15 forward, the failure-to-pay penalty (0.5% per month) and daily-compounding interest accrue on whatever you didn't pay, extension or not.

Does an extension give more time to pay the IRS? No — here's why

An IRS extension is an extension of time to file, never an extension of time to pay — every dollar of tax for the year was still due April 15. Form 4868 is granted automatically when you submit it on time; the IRS doesn't approve or deny it, and it doesn't ask why you need it. But nothing in it touches the payment deadline.

The form even builds this in. It asks you to estimate your total tax liability, list what you've already paid, and send the difference with the extension. The extension is still valid if you pay $0 — but the unpaid difference starts accruing penalty and interest the day after April 15.

Two narrow exceptions exist, and it's worth knowing why neither is the everyday extension:

- Disaster postponements. When FEMA declares a disaster in your county, the IRS can postpone both filing and payment deadlines. That's a different mechanism entirely — see disaster relief tax deadline extension 2026.

- Form 1127. There is a separate application for an extension of time to pay due to undue hardship. It's rarely granted, requires proving that paying on time would cause real financial harm (not just inconvenience), and the IRS can require security. For most people, a payment plan is faster and more realistic.

So if you extended and didn't pay, you did half the right thing — and the half you did was genuinely valuable. Here's the math on why.

What a tax extension changes — and what it doesn't

An extension blocks the 5%-per-month failure-to-file penalty, which is ten times larger than the 0.5%-per-month failure-to-pay penalty. That single fact is why filing an extension (or the return itself) is always worth it even when you can't send a dollar — the deeper comparison is in failure to file penalty vs failure to pay.

| Item | Without an extension | With a timely Form 4868 |

|---|---|---|

| Filing deadline | April 15 | October 15 |

| Payment deadline | April 15 | April 15 — unchanged |

| Failure-to-file penalty (5%/month, 25% cap) | Starts April 16 if no return filed | Blocked, as long as you file by October 15 |

| Failure-to-pay penalty (0.5%/month, 25% cap) | Starts April 16 on unpaid tax | Starts April 16 on unpaid tax — the extension doesn't stop it |

| Interest (set quarterly, compounds daily) | Starts April 16 | Starts April 16 — no extension ever pauses interest |

Read the last three rows together and the picture is clear: the extension protects you from the catastrophic penalty, not from the slow one. If you're deciding right now whether to send anything at all, file even if you can't pay — the math is one-sided.

The real cost of waiting: a worked example

On a $23,800 unpaid balance, the failure-to-pay penalty alone adds about $119 every month the balance sits. Say that's your situation — you're a renter, you extended in April, and you plan to file on October 15 without having paid anything in between. Here's the arithmetic, using a 7% annual interest rate purely for illustration (the actual rate is set quarterly):

- Failure-to-pay penalty: 0.5% × $23,800 = $119/month × 6 months ≈ $714

- Interest: roughly 7% ÷ 2 on $23,800 ≈ $830, compounding daily

- Balance on October 15: roughly $25,340 — about $1,540 of growth for six months of waiting

Now the counterfactual that shows what the extension was worth. If you had skipped the extension and the return, the failure-to-file penalty would run 5% per month until it caps at 25% — up to $5,950 on the same balance, in as little as five months. Your extension saved you roughly $5,200 in penalties even though it didn't buy you a single day on the payment. You can estimate your own numbers with our IRS Penalty & Interest Calculator.

And the meter doesn't stop on October 15. The 0.5% penalty keeps accruing until it hits its own 25% cap, and interest compounds until the balance is resolved. That's why "I'll deal with it when I file" quietly becomes "I'll deal with it when the levy notice arrives."

What happens if you never pay the balance

A balance from an extended return enters the same automated collection pipeline as any other tax debt — and left alone, that pipeline ends at a levy. The sequence typically looks like this:

- Your October return posts a balance due. The IRS assesses the tax, and the first bill goes out.

- CP14 notice — the first bill, showing tax, penalties, and interest. You typically have about 21 days before the sequence advances. This is the cheapest moment to fix everything.

- CP501 and CP503 — reminder notices. Still just bills, but the balance grows every month they're ignored.

- CP504 — Notice of Intent to Levy under IRC §6331(d). The IRS can now take your state tax refund, and a federal tax lien becomes a live possibility.

- LT11 notice or Letter 1058 — the Final Notice of Intent to Levy. A 30-day clock starts, along with your right to a Collection Due Process hearing. After it runs, the IRS can levy.

- Levy. A bank levy freezes funds with a 21-day hold before the money leaves; a wage levy is continuous, paycheck after paycheck, until it's released. For a renter with no home equity, your paycheck and bank account are exactly what the IRS reaches for first.

In 2026, don't count on understaffing to save you. The IRS workforce shrank roughly 27% in 2025 — humans are harder to reach than ever — but these notices and levies are generated by automated systems that never stopped running.

Filed an extension and the balance caught up with you?

Whether you're holding a first CP14 or a Final Notice of Intent to Levy, an experienced tax professional will review your notice and your numbers free and map the cheapest way out. If an LT11 has arrived, the 30-day window to protect your paycheck is already running.

Your options when the extension didn't buy time to pay

The IRS offers a short-term payment plan of up to 180 days with no setup fee — and that's just the first of several programs the notices never advertise. Which one fits depends on your balance and your budget; the full DIY roadmap lives in our guide to how to settle tax debt yourself, and the head-to-head payment comparison is in best way to pay the IRS.

| Option | Who it fits | Cost and the catch |

|---|---|---|

| Short-term payment plan | You can pay in full within 180 days | $0 setup fee; penalties and interest continue, but enforcement stops |

| Long-term installment agreement | Balances up to $50,000 can be set up online over as long as 72 months (under $10,000, a guaranteed installment agreement applies) | Setup fee varies; interest continues, and the failure-to-pay rate typically drops to 0.25%/month while the plan is active |

| Currently Not Collectible status | Paying anything would leave you unable to cover rent and basic living costs | Free; collection pauses, but the debt, penalties, and interest remain and the IRS reviews your income periodically |

| Offer in Compromise | Your income and assets genuinely can't cover the debt before the collection statute runs | $205 fee and 20% down on lump-sum offers (both waived with low-income certification); the IRS accepted roughly 1 in 5 offers in FY2024 |

| Penalty relief (FTA / AEP) | Clean compliance for the prior 3 years, or a reasonable-cause event | Free; removes penalties but not tax or interest — see the AEP note below |

Back to the $23,800 example: on a 72-month agreement, roughly $25,340 divides to about $352/month before ongoing interest — a real payment, but one that ends the notice sequence the day it's approved. As a renter, an Offer in Compromise analysis would turn almost entirely on your monthly income versus IRS allowable living expenses, since there's no home equity in the equation — which cuts both ways: nothing to protect, but also nothing to fund a lump sum with. It's means-tested math, not a discount program.

One 2026 note on penalties: first-time abatement is being replaced by the Automatic Exemption from Penalty starting in summer 2026, which applies without any request. Until your penalty is actually removed, though, it's still accruing — details in automatic exemption from penalty AEP 2026 and first time penalty abatement.

How to respond, step by step

- Pull your real balance. Log in to your IRS online account and get the current payoff figure with penalties and interest through today — the number on an old notice is already stale.

- File any unfiled return today. If October 15 has passed and the return still isn't in, filing now stops the 5% monthly failure-to-file penalty from growing further.

- Pay whatever you can now. Every dollar you send shrinks the base that the 0.5% monthly penalty and daily interest are calculated on.

- Set up a payment arrangement. A short-term plan (up to 180 days) or an installment agreement stops the notice escalation the day it's approved.

- Request penalty relief. If your prior three years are clean, first-time abatement can remove the failure-to-pay penalty — and starting summer 2026, the IRS's Automatic Exemption from Penalty applies some relief with no request at all.

- Answer any levy notice within 30 days. If you're holding an LT11 or Letter 1058, file Form 12153 for a Collection Due Process hearing before the 30-day deadline to pause levy action while your case is reviewed.

The setup itself takes minutes online for most balances under $50,000 — the walkthrough is at how to set up IRS payment plan online.

When you can handle this yourself

If you agree with the balance and can pay it within 180 days, you don't need professional help — set up the free short-term plan online and you're done. The same goes for a single-year balance under $50,000 with no other complications: the streamlined installment agreement exists precisely so you can fix this in one sitting, without financial disclosure forms.

Experienced help changes outcomes in specific situations: a Final Notice of Intent to Levy already in hand (the 30-day CDP window is easy to waste), a wage or bank levy already in motion, multiple unfiled years stacked behind this one, self-employment or payroll tax mixed in, or an Offer in Compromise where the allowable-expense math decides whether you're a candidate at all. In those cases, the order you fix things in — returns first, then penalties, then the balance — often matters more than any single form.

If the deeper problem is that April 15 keeps ambushing you every year, start with the prevention playbook in can't pay taxes by April 15 — and if it's specifically the October deadline bearing down, see October 15 tax deadline can't pay. Not sure whether your situation is a DIY fix or a real case? A free review at Clarity's consultation form settles it in one conversation.

Terms on your extension and notices, decoded

- Form 4868 — the automatic six-month extension of time to file an individual return; it never extends the time to pay.

- Failure-to-file penalty — 5% of the unpaid tax per month a return is late, capped at 25%; the penalty an extension protects you from.

- Failure-to-pay penalty — 0.5% of the unpaid tax per month, capped at 25%; the penalty an extension does not touch.

- Notice of Intent to Levy — the warning (CP504, then LT11/Letter 1058) that the IRS intends to seize refunds, wages, or bank funds if the balance stays unresolved.

- Collection Due Process (CDP) — your right, triggered by the final levy notice, to a hearing that pauses levy action; requested on Form 12153 within 30 days.

- CSED — the Collection Statute Expiration Date: the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy can pause that clock.

Extension and payment questions, answered

Does filing a tax extension mean I don't have to pay until October 15?

No. Form 4868 only extends your filing deadline to October 15 — your payment was still due April 15. From that date, the IRS adds a 0.5% monthly failure-to-pay penalty plus daily-compounding interest to whatever you didn't pay. The main exception is a federally declared disaster extension, which can postpone both the filing and payment deadlines.

What is the penalty for filing an extension but not paying?

The failure-to-pay penalty: 0.5% of the unpaid tax per month, up to a 25% cap, plus interest that compounds daily. On a $23,800 balance, that's about $119 in penalty every month. If you also miss the October 15 filing deadline, the far larger failure-to-file penalty — 5% per month — starts stacking on top.

Should I still file an extension if I can't pay anything?

Yes — always. The extension costs nothing and blocks the failure-to-file penalty, which runs 5% per month versus 0.5% for late payment — ten times worse. Filing the extension (and then the return) with zero payment attached is dramatically cheaper than skipping both because you couldn't send money.

Do I have to send a payment with Form 4868?

No payment is required for the extension itself to be valid — the extension to file is automatic if you submit the form on time. But the form asks you to estimate your tax and pay what you can, because anything unpaid after April 15 accrues the failure-to-pay penalty and interest until it's resolved.

Will the IRS charge interest even though I filed an extension?

Yes. Interest starts on April 15 and compounds daily regardless of any extension, at a rate the IRS sets quarterly (the federal short-term rate plus 3 percentage points for individuals). Unlike penalties, interest generally can't be waived — it only stops growing when the underlying balance is paid or abated.

I filed an extension and still can't pay by October 15 — what now?

File the return by October 15 anyway — that keeps the 5%-per-month failure-to-file penalty off your account permanently. Then deal with the balance separately: a short-term plan gives up to 180 days, a long-term installment agreement stretches balances under $50,000 across up to 72 months, and hardship status can pause collection entirely.

Does a state tax extension also give more time to pay?

Generally no — most states mirror the federal rule: an extension moves the filing date, not the payment date. But every state sets its own penalties, interest rates, and extension procedures, and some don't honor the federal extension automatically. Check directly with your state revenue agency rather than assuming the IRS rules apply.

Can the IRS levy my bank account over a balance from an extended return?

Yes, eventually — but never without warning. The IRS must first send a series of notices ending in a Final Notice of Intent to Levy (LT11 or Letter 1058), which starts a 30-day clock and your right to a Collection Due Process hearing. If a bank levy does hit, the bank holds the funds for 21 days before sending them, which is your window to act.

Your next 24 hours

- Find your real number. Log in to your IRS online account (or pull out the most recent notice) and write down the current balance and the notice code in the top corner — CP14, CP504, or LT11 tells you exactly how much runway you have.

- Gather three things. Your extension confirmation, the return (filed or drafted), and a rough monthly picture of income and rent — that's everything needed to pick the right payment option.

- Get the free review. Call (888) 825-7779 or use the 2-minute form. Penalties and interest are compounding on this balance every day it sits — and if a Final Notice has arrived, the 30-day levy clock is already counting.

Primary sources: the IRS's own pages on Form 4868, the automatic extension of time to file, making IRS payments, and payment plans and installment agreements.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.