Tax Deadlines

October 15 Tax Deadline: Can't Pay What You Owe? Your 2026 Playbook

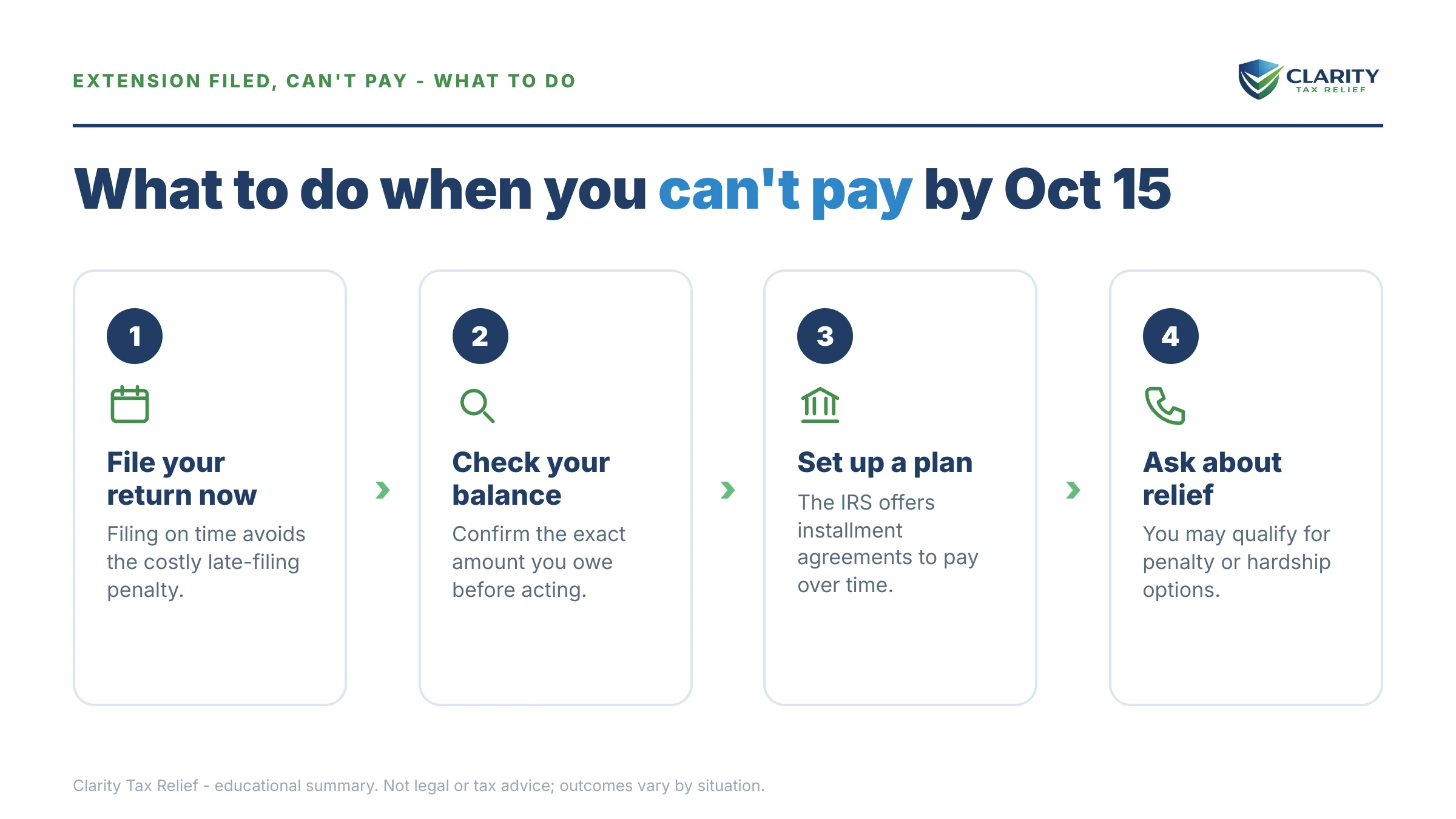

The short answer: if you're facing the October 15 tax deadline and can't pay, file the return anyway. October 15 is a filing deadline, not a payment deadline — missing it triggers a 5%-per-month penalty, ten times the 0.5% rate you're paying now. File, then set up a payment plan.

You filed the extension back in April because the divorce made this year's return a mess — a new filing status, the house, the retirement split. Now the return finally exists, the software says you owe, and the account that would have covered it went into the settlement. That's a solvable problem — and the fix starts with a filing decision, not a payment.

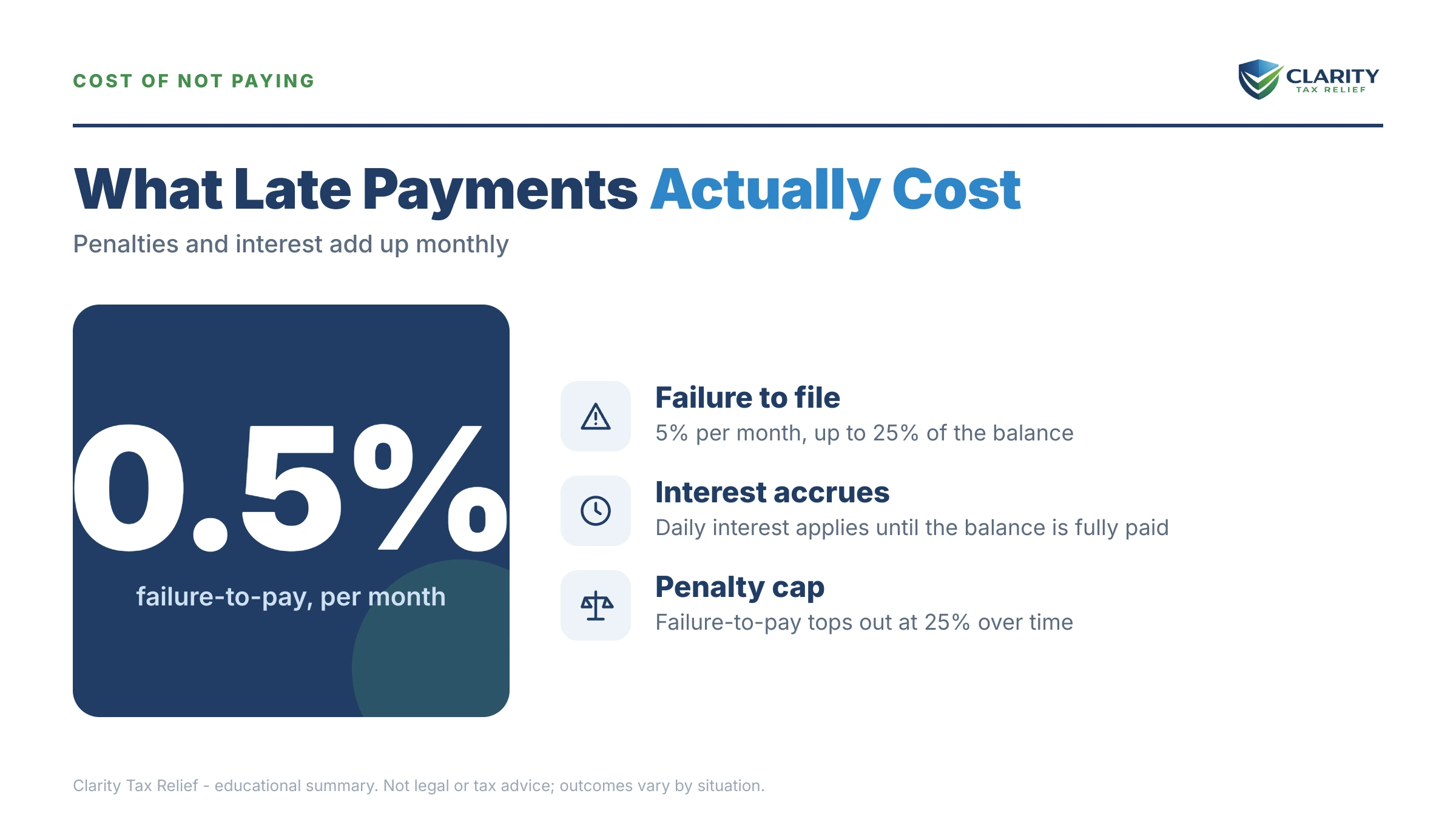

⏱ Your deadline: extended 2025 returns are due October 15, 2026. Filing by that date keeps the failure-to-file penalty — 5% of the unpaid tax per month, up to 25% — off your account entirely. The payment itself was due April 15, so interest and the smaller 0.5% monthly late-payment penalty are already running and will continue until the balance is resolved.

Why the October 15 deadline matters when you can't pay

An extension gives you six extra months to file — it never gave you extra time to pay. The tax was legally due April 15, which is why an extension gives more time to file, not pay, and why interest and a 0.5%-per-month failure-to-pay penalty have been quietly accruing since spring even though you did everything right by extending.

That sounds discouraging, but flip it around: the expensive penalty hasn't touched you yet. The failure-to-file penalty (5% per month) is ten times the failure-to-pay penalty (0.5% per month) — and filing by October 15 is all it takes to keep it that way. The single worst move available to you right now is not filing because you can't pay.

People make that mistake constantly, usually out of a vague sense that filing "activates" the debt. It doesn't. The IRS already has your W-2s, 1099s, and — if you split retirement accounts this year — the 1099-R from the plan administrator. The balance exists whether you file or not. Filing just decides which penalty schedule you're on. See the full comparison in failure-to-file vs. failure-to-pay penalties.

If you were in a federally declared disaster area this year, your deadline may already be later than October 15 — check disaster relief tax deadline extension 2026 before assuming the clock applies to you.

Say you owe $11,300 after your divorce: the actual math

A hypothetical, but a common one. Say the divorce was finalized last year: you filed single for the first time, your withholding was still set for a two-income joint return until August, and a QDRO distribution added taxable income. The return shows $11,300 due. Here's what each path costs:

Path 1 — file by October 15, set up a payment plan. By October 15 you've accrued roughly six months of failure-to-pay penalty: 6 × 0.5% × $11,300 ≈ $339, plus daily-compounding interest on top. At $11,300 you're under the $25,000 streamlined threshold, so a monthly installment agreement over up to 72 months is available without detailed financial disclosure — the floor payment is about $11,300 ÷ 72 ≈ $157/month, though paying $250–$300 shortens the plan and cuts total interest meaningfully. Bonus: once the agreement is approved, the failure-to-pay rate is cut in half to 0.25% per month.

Path 2 — don't file because you can't pay. The failure-to-file penalty starts at 5% per month: $565 the first month, $1,130 by month two, capping at 25% — $2,825 — plus the failure-to-pay penalty and interest still running underneath. Same debt, roughly $2,500 more expensive, for no benefit whatsoever.

Want to run your own numbers on a different balance? Our Penalty & Interest Calculator estimates what a balance grows to under each penalty schedule.

One more divorce-specific note: if part of what you owe traces to an early retirement withdrawal from the split, the 10% early-distribution addition may be part of the balance — 401k withdrawal tax bill can't pay covers that math and the exceptions (a distribution paid to you under a QDRO, for instance, avoids the 10% penalty even though the income is still taxable).

What happens after October 15 if the balance goes unpaid

Once you file with a balance due, the IRS's automated collection sequence starts — and in 2026, with the IRS workforce down roughly 27%, that sequence is more automated than ever. Humans are harder to reach; the notice machine never slowed down. The stages run in this order:

- Balance posts — your return processes and the $11,300 (plus accruals) becomes an assessed debt. No notice yet; this is your quietest window to set up a plan on your own terms.

- CP14 — the first bill, typically giving about 21 days to pay or arrange payment. Still no enforcement power behind it.

- CP501 / CP503 — reminder notices, each arriving weeks after the last, each with a bigger balance printed on it.

- CP504 — Notice of Intent to Levy. The IRS can now seize your state tax refund, and a federal tax lien becomes a realistic risk.

- LT11 / Letter 1058 — the final notice. It starts a 30-day clock, after which the IRS can levy bank accounts and garnish wages. You gain formal Collection Due Process appeal rights here (Form 12153) — but far fewer good options than you have today.

And if you don't file at all? Eventually the IRS prepares a substitute return for you using only the income documents it has — no deductions, no basis on asset sales, single-rate assumptions — and assesses tax on that inflated number. Everything above then happens anyway, on a worse balance. If October 15 has already passed as you read this, go to missed October 15 tax deadline for the recovery sequence.

Staring down October 15 with a balance you can't pay?

Get your situation reviewed free before the filing deadline locks in the wrong penalty schedule. An experienced tax professional will map your cheapest path — file-and-plan, penalty relief, or hardship options — in one call.

Can't pay by the October 15 tax deadline? Your real options

Filing on time with no payment attached opens every option below — none of them require paying in full first. Which one fits depends on your balance, income, and how fast your post-divorce finances stabilize. (For the full DIY walkthrough of each program, see our pillar guide to how to settle tax debt yourself — this table is the October-15-specific map.)

| Option | Who qualifies | Cost to set up | What it does |

|---|---|---|---|

| Short-term payment plan | Anyone who can pay in full within 180 days | $0 setup fee | Buys six months; interest and penalties keep accruing, but collection notices stop escalating |

| Guaranteed installment agreement | Individuals only, with an income-tax balance of $10,000 or less (excluding penalties and interest); all returns filed; timely filing and payment for the past 5 years with no installment agreement in that period; full payment within 3 years | Setup fee (reduced with direct debit) | IRS must accept a 3-year payoff plan — note an $11,300 balance just misses this; paying it below $10,000 first can qualify you |

| Streamlined installment agreement | Balance of $25,000 or less ($50,000 with direct debit); up to $50,000 qualifies online | Setup fee (reduced with direct debit; waived or reimbursed for low-income) | Monthly plan up to 72 months, no detailed financial disclosure required |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living expenses (financial disclosure required) | $0, but financial documentation | Pauses collection while the debt (and interest) remains — see IRS Currently Not Collectible |

| Offer in Compromise | Assets + future income genuinely can't cover the debt; the IRS accepted roughly 1 in 5 offers in FY2024 | $205 fee + 20% down on lump-sum offers (both waived if AGI ≤ 250% of poverty) | Settles for less than the full balance when the IRS's own math says full collection is impossible |

| Penalty relief (FTA / AEP) | Clean filing and payment record for the prior 3 years | $0 | Removes the failure-to-pay penalty; AEP makes this automatic starting summer 2026 |

Two notes on that table for a recently divorced filer. First, if this year's balance is yours alone (a single or head-of-household return), your ex has nothing to do with it — but if you also owe on a prior joint return, the IRS can pursue either of you for the whole joint amount regardless of what the decree says; divorce and IRS debt: who pays explains how that liability actually splits. Second, don't chase an Offer in Compromise reflexively at $11,300: if you have home equity from the settlement or steady income, the IRS's collection math will usually show it can collect in full, and a streamlined plan is faster and cheaper than a rejected offer.

| Notice | Response window | What it can do |

|---|---|---|

| CP14 (first bill) | About 21 days from the notice date | No enforcement — the cheapest moment to set up a plan if you haven't already |

| CP501 / CP503 (reminders) | The pay-by date printed on each notice | Still bills only, but the balance grows every month |

| CP504 (intent to levy) | The date printed on the notice | IRS can seize your state tax refund; lien filing becomes likely |

| LT11 / Letter 1058 (final notice) | 30 days | Bank levies and wage garnishment become legal after the window; Form 12153 preserves your appeal rights |

How to respond before October 15, step by step

- File your return by October 15 — even with no payment attached. Filing on time keeps the failure-to-file penalty (5% per month) off your account entirely.

- Pay whatever you can with the return. Every dollar you pay now shrinks the base that penalties and interest are calculated on for every month that follows.

- Set up a payment plan online once the balance posts — up to 180 days with no setup fee if you can pay it off short-term, or a monthly installment agreement of up to 72 months for balances of $50,000 or less.

- Request penalty relief once the plan is in place. If your prior three years are clean, First-Time Abate can remove the failure-to-pay penalty — and starting summer 2026, the Automatic Exemption from Penalty applies without a request.

- Watch the mail for a CP14 and verify it against your records and your IRS online account before paying anything beyond your plan — payments and notices routinely cross in the mail.

Step 3 is genuinely a 20-minute job for most balances at this level — our walkthrough of how to set up an IRS payment plan online shows every screen. For step 4, first-time penalty abatement covers the clean-compliance test in detail, and the Automatic Exemption from Penalty (AEP) for 2026 explains what changes this summer. And when the CP14 lands — it will, even with a plan pending — got a CP14 and can't pay tells you exactly how to read it.

When you can handle this yourself — and when help changes the outcome

Most people in this exact situation do not need professional help. If your only issue is one year's balance under $25,000, you agree with the number on your return, and you have income to support a monthly payment, the file-then-plan sequence above is entirely DIY: the online agreement takes minutes, and penalty relief is a phone call or — under AEP — automatic.

Experienced help earns its cost in the messier versions: you also owe on prior joint years and need liability actually reassigned, not just paid; the divorce left unfiled years behind (the extension only covers this return); you're self-employed and behind on quarterly estimates, so next April will repeat this; or your budget genuinely can't support any payment and you need the hardship or offer math done right the first time. In those cases the order you fix things in — returns first, then penalties, then the balance — often changes the total you pay.

Terms on your situation, decoded

- Extension (Form 4868): the automatic six-month extension of time to file — it never extends the time to pay, which stayed April 15.

- Failure-to-pay penalty: 0.5% of the unpaid tax per month (capped at 25%), running since April 15; halved to 0.25% while an approved installment agreement is active.

- Failure-to-file penalty: 5% of the unpaid tax per month (capped at 25%) — the one you avoid completely by filing on or before October 15.

- Installment agreement: the IRS's formal monthly payment plan; balances of $50,000 or less can be set up online for up to 72 months.

- CP14: the first collection bill the IRS mails after a balance posts — expect one even if your payment plan application is already pending.

- CSED: the Collection Statute Expiration Date — the IRS generally has 10 years from assessment to collect, though certain actions pause that clock.

October 15 and can't pay: your questions, answered

Do I have to pay by October 15, or just file?

October 15 is only a filing deadline — your payment was due back on April 15, and interest plus the failure-to-pay penalty have been running since then. Filing by October 15 is what protects you: it prevents the failure-to-file penalty, which is ten times larger. Pay what you can with the return, but never hold the return hostage to the payment.

What is the penalty if I file by October 15 but can't pay?

You keep accruing the failure-to-pay penalty of 0.5% of the unpaid tax per month, plus daily-compounding interest. On an $11,300 balance that penalty is about $57 a month. Once an installment agreement is approved, the failure-to-pay rate is cut in half to 0.25% per month — one more reason to set up a plan quickly instead of waiting for notices.

What happens if I miss October 15 and still owe?

The failure-to-file penalty starts stacking at 5% of the unpaid tax per month, up to 25% — ten times the rate of the failure-to-pay penalty. On $11,300 that can add up to $2,825 on top of everything else. If you have already missed it, file immediately anyway; every month you wait adds another 5% until the cap. See our guide to a missed October 15 deadline for the recovery steps.

Can I get another extension after October 15?

For most taxpayers, no — October 15 is the final filing deadline for the year, and the IRS does not grant a second extension because you can't pay. The main exceptions are automatic: federally declared disaster areas get postponed deadlines, and taxpayers serving in a combat zone get extra time. If neither applies to you, the answer is to file on time and arrange payment separately.

Can I set up a payment plan before the IRS sends me a bill?

Yes — you do not have to wait for a CP14 notice. Once your return is processed and the balance posts, you can apply online: a short-term plan gives up to 180 days with no setup fee, and balances of $50,000 or less can qualify for a monthly plan of up to 72 months. Setting the plan up early stops the collection-notice sequence before it starts.

My divorce decree says my ex pays the taxes — am I still on the hook?

If the balance comes from a jointly filed return, yes — the IRS can collect the full amount from either spouse, and a divorce decree does not bind the IRS. The decree gives you a claim against your ex in state court, not protection from federal collection. Depending on the facts, innocent-spouse or separation-of-liability relief may reassign part of a joint debt, but you have to request it.

Will the IRS keep my refund next year if I owe from this year?

Yes. Any federal refund you are due in a future year is automatically applied to your unpaid balance until it is gone — even if you are current on an installment agreement. If you expect a refund next spring, treat it as a built-in payment toward this debt, and consider adjusting your withholding so you are not overpaying the rest of the year.

Does first-time penalty abatement apply to a balance like this?

Often, yes. If you filed and paid on time for the prior three years, First-Time Abate can remove the failure-to-pay penalty that accrued on this balance — a few hundred dollars back on a typical extension-season debt. Starting in summer 2026, the IRS is replacing this with the Automatic Exemption from Penalty (AEP), which applies without a request, so check whether relief has already posted before you ask.

Your next 24 hours

- Open your draft return and circle the "amount you owe" line — that number, not a guess, decides which options in the table above you qualify for. Confirm your April extension was actually filed (your software or preparer has the acceptance confirmation).

- Gather three things: the completed return, this year's income documents (W-2s, 1099s, any 1099-R from a retirement split), and any prior joint-year balances — those change the strategy.

- Get a free case review before October 15 — the form takes two minutes, or call (888) 825-7779. Filing on the right side of that deadline is the difference between a 0.5%-per-month problem and a 5%-per-month one.

You can pay any amount, any time, at IRS.gov/payments, and apply for a plan at the IRS's payment plans and installment agreements page. If an IRS error or delay is blocking you and you can't get through by phone, the independent Taxpayer Advocate Service exists for exactly that.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.