Tax Deadlines

Missed October 15 Tax Deadline: What It Costs and What to Do Now (2026)

The short answer: missed October 15 tax deadline? File your return now, even if you can't pay. The failure-to-file penalty adds 5% of the unpaid tax every month (up to 25%) — ten times the late-payment penalty. If you're owed a refund, there is no penalty, but you have three years to claim it.

The extension you filed back in the spring was supposed to buy breathing room. Then the divorce swallowed the year — the house, the attorneys, splitting the retirement accounts — and October 15 slipped past with the return still sitting in a folder. Here's the part that matters: this is fixable, the fix starts with filing (not paying), and every option gets cheaper the sooner you act.

If you actually filed by the deadline and just can't cover the balance, you have a different — and better — problem; that path is covered in our guide to the October 15 tax deadline can't pay situation. This page is for the return that never went in.

⏱ Your real clock: there is no new deadline coming — the penalty clock is already running. Each month (or part of a month) your return stays unfiled adds 5% of the unpaid tax, up to a 25% cap, on top of the late-payment penalty and daily-compounding interest running since April 15. Filing this week is the only thing that stops it.

What actually happens when you miss the October 15 deadline

October 15 is the final filing deadline of the tax year — the IRS does not grant a second extension. Form 4868 gave you six extra months to file; there is no form that grants six more. From the day after the deadline, an unfiled return with a balance due starts accruing the failure-to-file penalty, and the extension's protection is used up.

Two clocks have actually been running the whole time, and people confuse them constantly:

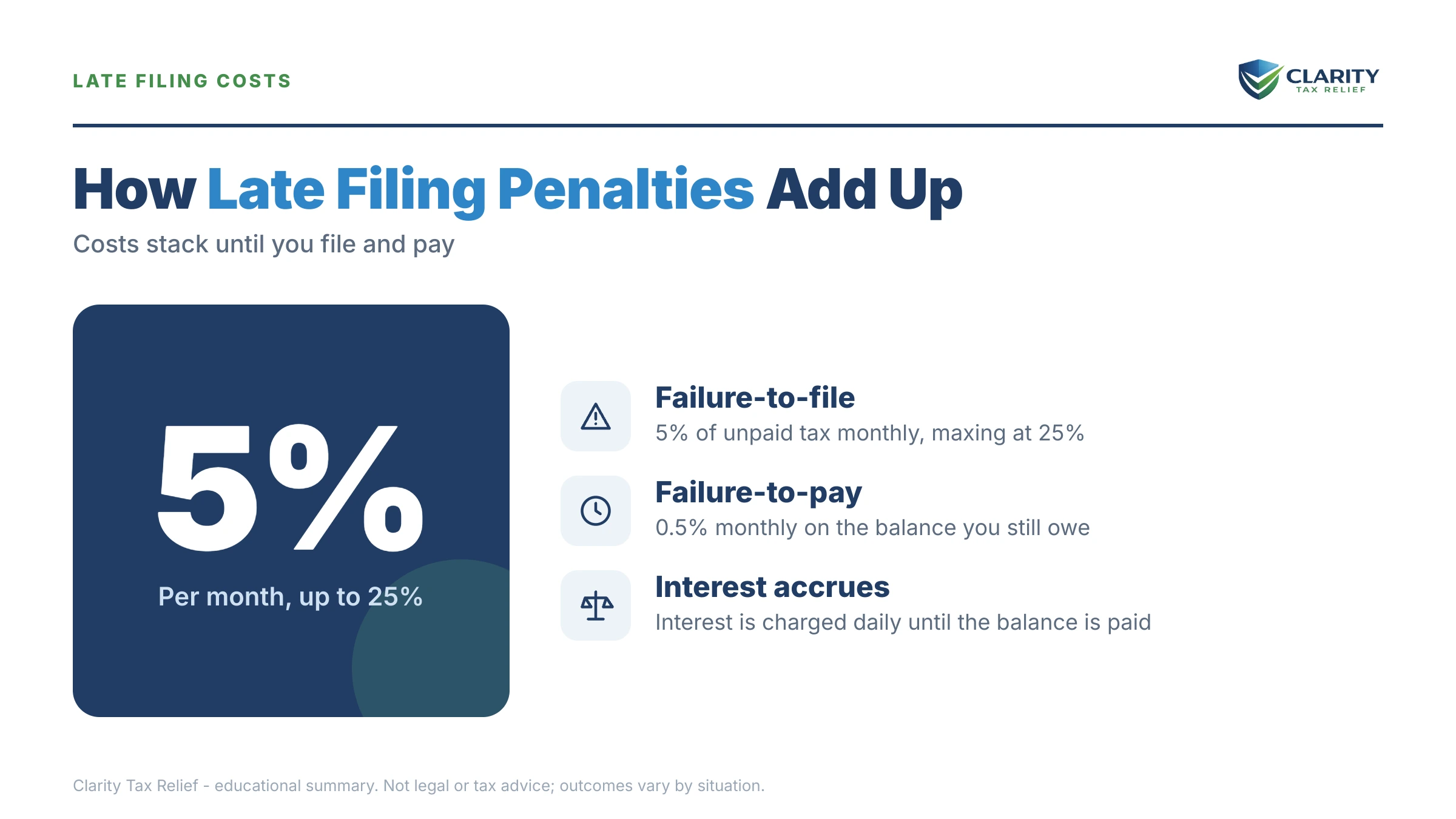

- Payment clock (since April 15): the extension never extended your time to pay. The failure-to-pay penalty (0.5% per month) and interest have been accruing on any unpaid balance since spring, whether or not you filed.

- Filing clock (since October 15): the failure-to-file penalty — 5% per month — starts once you blow the extended deadline. This is the expensive one, and it's the one you control today.

One nuance worth knowing: if the IRS decides your extension was invalid — typically because it wasn't filed properly or the tax estimate on it wasn't made in good faith — it can compute the late-filing penalty all the way back to April 15. The full breakdown of how the two penalties interact is in our guide to the failure to file penalty vs failure to pay penalty.

Three groups get more time automatically, no request needed: taxpayers in federally declared disaster areas (see the current disaster relief tax deadline extension 2026 list), military members serving in combat zones, and certain U.S. citizens abroad. If none of those describe you, October 15 was it.

And if you're owed a refund? Breathe. Both penalties are percentages of unpaid tax, so a refund year carries no penalty at all — your only deadline is the three-year window to claim the money, explained in can I still get a refund from 3 years ago.

What a missed October 15 tax deadline actually costs

A missed October 15 tax deadline costs 5% of your unpaid tax per month in late-filing penalty, capped at 25% — plus the 0.5% monthly late-payment penalty and interest at the federal short-term rate plus 3 points, compounded daily. When both penalties run in the same month, the filing penalty drops to 4.5% so the combined monthly hit is 5% — but over time the two can stack to as much as 47.5% of the tax.

Two more multipliers hide in the fine print. Once a return is more than 60 days late, a minimum flat penalty applies — the lesser of an inflation-adjusted dollar amount or 100% of the unpaid tax — even on small balances. And because interest compounds on the penalties too, the balance grows on itself every day.

Here's what that looks like on a real number. This table uses $83,100 of unpaid tax — the figure we'll carry through the worked example below:

| Months past October 15 | Late-filing penalty accrued | Dollar cost on $83,100 |

|---|---|---|

| 1 month (or any part) | 4.5% | $3,740 |

| 2 months | 9% | $7,479 |

| 3 months | 13.5% | $11,219 |

| 4 months | 18% | $14,958 |

| 5+ months (cap) | 22.5% | $18,698 |

The rate shows 4.5% rather than 5% because the concurrent late-payment penalty absorbs 0.5% each month — that penalty, plus daily interest, sits on top of every row above. You can run your own balance and dates through our IRS penalty and interest calculator to estimate the total.

Worked example: divorced, $83,100 owed, three months late

Filing three months after October 15 on an $83,100 balance costs roughly $11,200 more than filing on time would have — even if you couldn't pay either way.

Say your divorce finalized last year. Your withholding was still set at the married rate, you sold the house, and half of a 401(k) came your way and partly out in cash. The return you finally prepare in mid-January shows $83,100 due. (If a retirement cash-out drove your number, the 401k withdrawal tax bill can't pay guide covers that shock specifically.) The hypothetical math:

- Late-filing penalty: 3 months × 4.5% = 13.5% → $83,100 × 0.135 = $11,218.50

- Late-payment penalty: 9 months since April 15 × 0.5% = 4.5% → $83,100 × 0.045 = $3,739.50

- Total penalties: roughly $14,958, before daily-compounding interest on all of it

Now compare: had the same return gone in by October 15 with nothing paid, the only penalty would be the $3,739.50 late-payment charge. The unfiled return itself cost about $11,219 — and every additional month of waiting adds roughly $4,155 more until the filing penalty caps. That is why "file first, solve payment second" isn't a slogan; it's arithmetic.

One more divorce-specific trap: if the balance is from a joint year, the IRS can collect all of it from either ex-spouse, no matter what the decree says. Who actually ends up paying is its own fight — see divorce who pays irs debt.

What happens if you keep waiting

An unfiled return doesn't fall through the cracks — the IRS already has your W-2s, 1099s, and retirement-account forms, and its automated systems escalate in a fixed sequence. Here's the order of what comes next:

- Penalties compound silently. You are here. Each month unfiled adds another 5% combined penalty until the filing portion caps at 22.5%, with interest compounding daily on top.

- The IRS notices the missing return. A CP59 notice asks where it is. Ignore it and the IRS can prepare a Substitute for Return — its own version of your return using only the income forms it holds, with no deductions, no basis on the house sale, and the least favorable filing status. That path, and how to undo it, is covered in the IRS filed a substitute return for me.

- The balance gets assessed and billed. Once a return posts — yours or the IRS's version — a CP14 bill arrives, with roughly 21 days to pay or arrange before the sequence escalates.

- Reminders, then enforcement notices. CP501 and CP503 reminders give way to a CP504 (the IRS can seize your state refund) and then an LT11 final notice, which starts a 30-day clock before wage garnishment and bank levies become legal.

- Passport certification becomes possible. At $83,100, you're above the $66,000 seriously-delinquent threshold for 2026. Once the debt is assessed and a lien is filed or levy issued, the IRS can certify it to the State Department, which can deny or revoke your passport — details in passport revoked for tax debt.

A note on 2026 reality: the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder than ever — but every step above is generated by automated systems that never stopped running. Understaffing delays your help, not your notices.

Missed October 15 and staring at a balance you can't pay?

Every month the return stays unfiled adds another 5% in penalties. Get a free review of your missed-deadline situation — an experienced tax professional will map the filing, the penalties, and the payment options before the next month's 5% posts.

Your options after filing late — especially above $50,000

Filing the return unlocks every IRS resolution program; not filing locks you out of all of them. The general playbook for resolving a balance on your own lives in our guide to how to settle tax debt yourself — here's how each option maps to a missed-October-15 balance:

| Option | Who it fits | Cost & limits |

|---|---|---|

| Pay in full | You can liquidate or borrow cheaper than IRS interest | Stops all penalties and interest immediately |

| Short-term payment plan | Can pay everything within 180 days | $0 setup fee; penalties and interest continue until paid |

| Streamlined installment agreement | Balance $50,000 or less | Up to 72 months, set up online, no financial disclosure; interest continues |

| Non-streamlined installment agreement | Balance over $50,000 (e.g., $83,100) | Requires Form 433-F financial disclosure; payment set by ability to pay |

| Currently Not Collectible | Paying anything would prevent basic living expenses | Collection pauses; debt, penalties, and interest keep accruing |

| Offer in Compromise | Assets plus future income genuinely can't cover the debt | $205 fee, 20% down on lump-sum offers (both waived with low-income certification); the IRS accepted roughly 1 in 5 offers in FY2024 |

| Penalty abatement | Clean 3-year record, or reasonable cause | Removes penalties, not the tax or interest on the tax |

Notice where $83,100 lands: above the $50,000 streamlined line and above the $66,000 passport threshold. That combination changes the strategy, so here's the full map by balance size:

| Balance owed | Realistic path |

|---|---|

| Under $10,000 | A guaranteed installment agreement — the IRS must accept it if you can pay within 3 years and your filings are current |

| $10,000–$25,000 | Streamlined agreement online, no financial disclosure |

| $25,001–$50,000 | Streamlined online for up to 72 months; direct debit typically required at the top of this band |

| $50,001–$100,000 | Financial disclosure required — or pay down below $50,000 to unlock the streamlined path; above $66,000, passport certification risk applies |

| Over $100,000 | Full financials, possible revenue officer assignment; professional representation strongly worth pricing out |

At $83,100, the pivotal question is often whether you can scrape roughly $33,100 together — from the house proceeds, a loan, or a family bridge — to drop under $50,000 and take the simpler online plan. If not, the disclosure route is manageable but unforgiving of mistakes; the mechanics are in irs payment plan over 50000.

On penalties: divorce alone is not "reasonable cause," but the circumstances around one can be — records held by an ex, a court fight over documents, a health crisis mid-split. And if your prior three years were clean, first time penalty abatement can wipe both penalties for the year. Starting summer 2026, the new automatic exemption from penalty (AEP) begins applying similar relief automatically — so don't assume the penalty on your account is final.

How to respond after missing October 15, step by step

The fix has a strict order, and getting it wrong costs money — file before you negotiate, verify before you file.

- File the return this week. Even if you can't pay a dollar, filing immediately stops the 5%-per-month failure-to-file penalty — the single most expensive part of this problem.

- Pull your IRS income records first. Download your wage and income transcript from your IRS online account so the return matches every W-2, 1099, and retirement-account form the IRS already has — a missed form triggers a second bill later.

- Pay whatever you can with the return. Every dollar paid now shrinks the base that penalties and daily interest are calculated on, and a partial payment can pull you under a program threshold.

- Set up the arrangement that fits your balance. Under $50,000, apply online for a payment plan of up to 72 months; above it, submit financial disclosure or pay the balance down below the threshold first.

- Request penalty relief once penalties post. Ask for First-Time Abatement or reasonable-cause relief after the failure-to-file penalty is assessed — relief applied to the assessed amount removes the most money.

When you can handle this yourself — and when help changes the outcome

Most people who missed October 15 by a few weeks with a modest balance can fix this alone. If your return is straightforward, you agree with the number, and the balance fits a short-term plan or a streamlined agreement under $50,000, the DIY path is genuinely fine: file, pay what you can, set up the plan online, request abatement. The full walkthrough is in should I file if I can't pay.

Experienced help starts changing outcomes when the facts get heavier: a balance over $50,000 (financial disclosure determines your payment, and how the 433-F is prepared matters), a divorce-year return where liability could be split or shifted, more than one unfiled year, a Substitute for Return already on file, or a balance above the $66,000 passport threshold where sequencing the plan before certification matters. In those cases, the order and packaging of the filings often changes the total cost more than any negotiation does — a free review before you file can confirm which camp you're in.

Terms you'll run into, decoded

- Form 4868 — the automatic extension you filed in April; it extended the time to file to October 15, never the time to pay.

- Failure-to-file penalty — 5% of unpaid tax per month (or part of one) the return is late, capped at 25%.

- Failure-to-pay penalty — 0.5% per month on unpaid tax from April 15; it drops to 0.25% while an installment agreement is active and can rise to 1% after a final levy notice.

- Substitute for Return (SFR) — the return the IRS files for you if you don't: income only, no deductions, worst-case filing status.

- Seriously delinquent tax debt — an assessed balance above $66,000 (2026) with a lien filed or levy issued, which the IRS can certify for passport denial or revocation.

- Streamlined installment agreement — the no-financial-disclosure payment plan available up to $50,000, spread over as many as 72 months.

Missed October 15: your questions answered

What is the penalty for missing the October 15 tax deadline?

The failure-to-file penalty is 5% of your unpaid tax for each month or part of a month the return is late, capped at 25%. It stacks on top of the 0.5%-per-month failure-to-pay penalty and daily-compounding interest that have been running since April 15. Once a return is more than 60 days late, a minimum flat penalty also applies unless you owe nothing.

Is there a penalty if the IRS owes me a refund?

No. Both late-filing and late-payment penalties are calculated as a percentage of unpaid tax, so if your withholding covered your bill, missing October 15 costs you nothing in penalties. The real risk is the refund statute: you generally have three years from the original due date to file and claim that money, after which the Treasury keeps it permanently.

Can I get another extension after October 15?

No — October 15 is the final filing deadline for the year, and the IRS does not grant second extensions. The main exceptions are automatic: taxpayers in federally declared disaster areas get postponed deadlines, military members in combat zones get extra time, and U.S. citizens living abroad have their own extension rules. If none apply to you, the only fix is filing now.

Should I still file if I can't pay anything?

Yes — file immediately even with zero payment. Filing stops the 5%-per-month failure-to-file penalty, which is ten times the 0.5% penalty for not paying. On an $83,100 balance, that's the difference between roughly $415 and $4,155 in new penalties each month. Once filed, you can set up a payment plan or hardship status; unfiled, you have no options at all.

Will the IRS waive penalties for missing October 15?

Often, yes. First-Time Abatement removes failure-to-file and failure-to-pay penalties if you had a clean compliance record for the prior three years — and starting in summer 2026, the new Automatic Exemption from Penalty (AEP) applies similar relief automatically, with no request needed. If you don't qualify, reasonable-cause relief may apply when circumstances beyond your control — serious illness, a disaster, records tied up in a divorce dispute — caused the delay. Interest on the tax itself is rarely waived.

Does missing October 15 cancel my extension and make penalties retroactive to April?

Usually not — if your extension was valid, the failure-to-file penalty runs from October 15, not April. But the IRS can void an extension that wasn't filed properly or didn't include a good-faith estimate of the tax owed, and then the late-filing penalty is computed from April 15. Either way, the failure-to-pay penalty and interest have been running since April, because an extension never extends the time to pay.

My divorce decree says my ex pays the taxes — do I still have to file and pay?

Yes. A divorce decree binds you and your ex, not the IRS: if the return is joint, the IRS can collect the entire balance from either spouse regardless of what the decree says. File your own required return now, and if your ex ignores the decree, your remedies are enforcing it in family court or, in limited cases, requesting innocent spouse relief from the IRS.

Your next 24 hours

- Confirm what the IRS already knows. Log into your account at IRS.gov/payments and pull your wage and income transcript — that's the list of forms your late return must match.

- Gather the divorce-year documents. The decree, the closing statement on the house, the 401(k)/QDRO paperwork, and every W-2 and 1099 — these decide whether $83,100 is even the right number. (Payment-plan mechanics are on the IRS payment plans page, and free independent help exists through the Taxpayer Advocate Service.)

- Get the return and the plan reviewed before the next 5% posts. Use the 2-minute form or call (888) 825-7779 — a free case review maps the filing, the penalty relief, and the payment path for a missed-October-15 balance in one call.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.