Unfiled Returns

Never Filed Taxes and Scared? Here's What to Actually Do in 2026

The short answer: if you've never filed taxes and you're scared, here's the fact that changes everything: the IRS generally requires only your last six years of returns to get back in good standing — not your whole life. Filing voluntarily, before enforcement finds you, is the single move that shrinks penalties and reopens every relief option.

You've never filed a return — not last year, not ever — and for years the plan was to fix it "soon." Now IRS envelopes are stacking up unopened, one of them may threaten a levy, and the same fear that stopped you from starting is stopping you from opening them. The way out isn't confession to a courtroom; it's six returns and one decision about the balance.

If IRS mail is already arriving, the image below shows you exactly what a non-filer notice looks like and where on it to find the tax year and the response date that matter — so you can sort your stack in minutes instead of dreading it for another month.

⏱ Your clock: if an LT11 or Letter 1058 (Final Notice of Intent to Levy) is anywhere in your mail, you have 30 days from the date printed on it to request a Collection Due Process hearing before levies can begin. If no final notice has arrived, your clock is the failure-to-file penalty — 5% of the unpaid tax per month, up to 25%, plus interest, accruing on every unfiled year with a balance.

Why never filing feels criminal — and what the IRS actually knows

The IRS already holds a copy of nearly every W-2, 1099, and 1099-K ever issued in your name — not filing hides nothing; it only leaves the IRS's version of your income unchallenged. Every employer and bank reported you the whole time. Your silence never made you invisible.

That's actually good news twice over. First, it means the records you're afraid you lost still exist: your wage and income transcript lists everything reported under your Social Security number, year by year. Second, it means the IRS's fear-inducing numbers are built from gross income only — no deductions, no expenses, no filing status that fits your life — which is why they're usually inflated.

And the jail question, directly: criminal prosecution targets willful evasion — hidden income, fake documents, ignoring direct agent contact — not a scared person who comes forward on their own. Voluntarily filing before the IRS opens an investigation is the strongest legal protection a non-filer has. The full civil-versus-criminal line is covered in can you go to jail for not filing taxes; for almost everyone reading this page, the answer is a fixable civil debt.

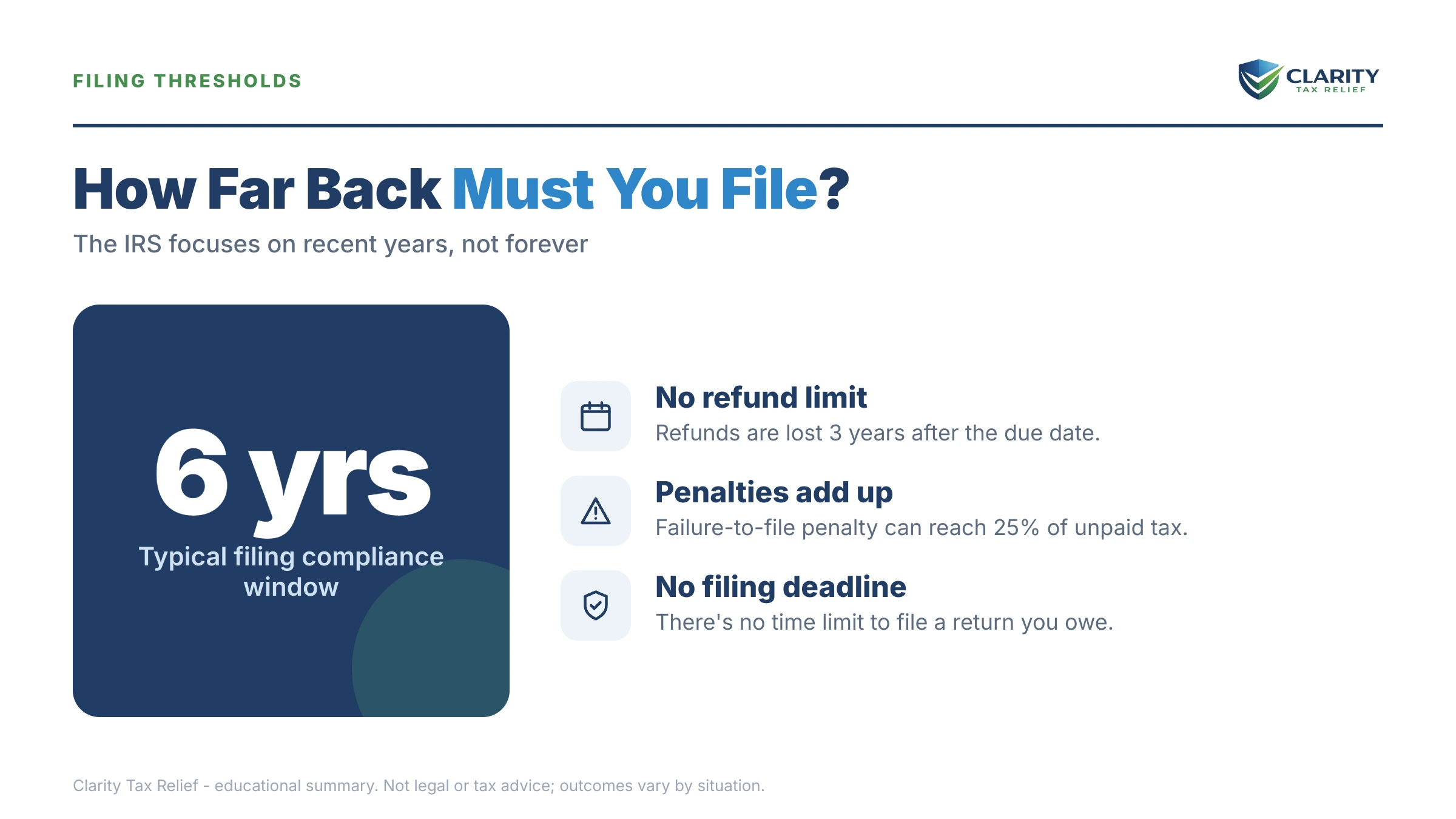

The six-year rule: you don't have to file every year you've been alive

Under IRS Policy Statement 5-133, the IRS generally requires only the last six years of returns to consider a non-filer back in compliance. Whether you skipped four years or twenty, the practical job in front of you is usually the same six returns — a manager can require more in unusual cases, but six is the working standard. The details live in how many years of back taxes do I have to file.

Two more facts shrink the job further. Years when your income fell below the filing threshold never required a return at all. And years with solid paycheck withholding may hold refunds — but refunds expire three years after the return's original due date, so the newest unfiled years are the ones bleeding money you can still recover. See can I still get a refund from 3 years ago before you assume every year is a debt.

If your gap is shorter than "never" — say a few years — the math and urgency shift; those situations are covered separately in haven't filed taxes in 3 years and haven't filed taxes in 10 years. This page is for the reader whose gap has no clear starting point.

What happens if you keep not filing: the escalation sequence

For a non-filer, IRS escalation always ends the same place: a substitute-for-return assessment, then levies on your paycheck and bank account. None of it requires a human to review your file — the sequence is automated, and the 2025 workforce cuts thinned the people who answer phones, not the systems that send levies.

The math driving it: the failure-to-file penalty runs 5% of the unpaid tax per month, capping at 25% — ten times the 0.5% monthly failure-to-pay penalty — with interest compounding on top. You can estimate what your unfiled years have already accrued with our IRS Penalty & Interest Calculator. Here's the order the letters come in:

- CP59 — "we have no record of your return." The system has matched income documents to your SSN and found no filing.

- CP516 / CP518 — escalating requests to file, with CP518 as the final unfiled-return notice. Still no enforcement — but the next stage writes your return for you.

- Substitute for Return (SFR) — the IRS prepares a return on your behalf: single, no dependents, standard deduction, zero expenses. It proposes the tax by mail (often a CP3219N deficiency notice with a 90-day window to contest), and if you stay silent, the inflated number becomes a legal assessment. What that looks like and how to undo it is covered in the IRS filed a substitute return for me.

- Billing notices, then CP504 — once assessed, the debt enters the normal collection track: bills, then an intent-to-levy notice that lets the IRS take your state refund.

- LT11 / Letter 1058 — the final notice. Thirty days later, levies are legal: a bank levy freezes funds for 21 days before they're sent to the IRS, and a wage levy is continuous until released.

- Passport certification — once assessed debt passes $66,000 (the 2026 threshold), the IRS can certify it to the State Department, which can deny or revoke your passport. Details in passport revoked for tax debt.

One more thing, specifically because you rent: no house means no home equity for a lien to sit on quietly. That's not protection — it means enforcement skips straight to the assets you do have. For renters, the levy on wages and bank accounts is the enforcement, which is why the LT11 stage matters more to you than to a homeowner.

Never filed and the mail is piling up?

You've carried this alone for years — the review takes 30 minutes. An experienced tax professional will read your notices, tell you which six years actually need filing, and whether a levy clock is already running. Free and confidential. If an LT11 or Letter 1058 is in your stack, its 30-day hearing window is real and already counting down.

Your options once you file: what you can qualify for

The IRS will not approve any payment plan, hardship status, or settlement until your required returns are filed — filing is the key that unlocks every option below. The programs themselves are the same ones every taxpayer with a balance uses; the full self-service playbook lives in our guide to how to settle tax debt yourself. What's specific to you is the order: returns first, SFR corrections second, resolution third.

| Option | Who it fits | Key threshold |

|---|---|---|

| Short-term payment plan | You can pay in full soon | Full payment within 180 days; $0 setup fee |

| Guaranteed installment agreement | Small remaining balance | $10,000 or less, paid within 3 years |

| Streamlined installment agreement | Most newly compliant filers | $50,000 or less; up to 72 months, set up online |

| Non-streamlined agreement | Balances above the online limit | Over $50,000; financial disclosure (Form 433) required |

| Currently Not Collectible | Income barely covers necessities | IRS allowable-expense math shows nothing left to pay |

| Offer in Compromise | Assets and income genuinely can't cover the debt | $205 fee and 20% down on lump-sum offers (both waived with low-income certification); roughly 1 in 5 accepted in FY2024 |

| Penalty relief | Anyone assessed failure-to-file penalties | Reasonable cause; new automatic AEP rules begin summer 2026 |

A candid note on penalty relief for lifelong non-filers: first-time penalty abatement requires a clean prior three years, which a never-filed history usually can't show for most years. Reasonable cause — illness, hardship, circumstances beyond your control — becomes the main path, and the Automatic Exemption from Penalty program rolling out in summer 2026 may apply without any request at all.

| Option | Upfront cost | Typical timeline |

|---|---|---|

| Filing six years of returns | Preparation costs only; nothing owed to the IRS to file | Days to weeks to prepare; back-year processing can take months |

| Short-term payment plan | $0 setup | Up to 180 days to pay in full |

| Streamlined installment agreement | Setup fee (lower with direct debit; waived for qualifying low-income) | Up to 72 months; interest and penalties continue until paid |

| Currently Not Collectible | $0 | Indefinite; reviewed if your income rises |

| Offer in Compromise | $205 plus 20% down on lump-sum offers (both waived with low-income certification) | Commonly many months; auto-accepted if the IRS doesn't decide within 2 years, with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count |

| Penalty abatement | $0 | Weeks to months after the request |

A worked example: $76,400 assessed against a renter facing levy

Say you owe $76,400 — every number here is hypothetical, but the mechanics are exactly how these balances get built. You were self-employed for three of your unfiled years. The IRS filed substitute returns using roughly $85,000 of reported 1099 income per year, filing status single, standard deduction, and zero business expenses. With the failure-to-file penalty capped at 25%, monthly failure-to-pay penalties, and compounding interest, the three assessments total $76,400 — and an LT11 just arrived.

Now you file accurate original returns for those years showing about $31,000 of legitimate, documentable expenses annually — mileage, supplies, insurance, software. Taxable income drops by more than a third, and because penalties are calculated as a percentage of the tax, they shrink along with it. In this hypothetical, the corrected total lands near $41,000.

That one correction changes three things at once:

- It moves you under the $50,000 line, so a streamlined installment agreement of up to 72 months can be set up online — roughly $570 a month on $41,000 ($41,000 ÷ 72), while interest and the 0.5% monthly failure-to-pay penalty continue until it's paid.

- It moves you under the $66,000 passport threshold for 2026, taking passport certification off the table.

- It changes what the levy notice can do to you. A pending hearing request and a resolution in motion are how wage and bank levies get prevented; an ignored SFR balance is how they happen. If no records survive from those years, reconstruction is still possible — see file back taxes without records.

None of this is guaranteed for your facts — your expenses, filing status, and years all move the numbers. But the direction is reliable: SFR math almost always overstates, and your real return is the correction.

How to respond when you've never filed, step by step

- Open and sort every IRS notice. Find any LT11 or Letter 1058 first — its 30-day hearing window outranks everything else in the stack.

- Pull six years of wage and income transcripts. Download them from your IRS online account; they list every W-2 and 1099 filed under your Social Security number and are the raw material for every back return.

- Prepare and file the last six years of required returns. Skip years that fell below the filing threshold, and file the most recent three first to claim any refunds still open under the three-year rule.

- Ask the IRS to replace any SFR assessments. File an accurate original return for each SFR year so the single-no-deductions math is recomputed with your real filing status and expenses.

- Set up a resolution for what remains. Choose a payment plan, Currently Not Collectible status, or an Offer in Compromise based on the eligibility table above — filing compliance unlocks all of them.

- Request penalty relief. Pursue reasonable-cause abatement on the failure-to-file penalties once returns are filed, and watch for the new Automatic Exemption from Penalty rules starting summer 2026.

Transcripts come from the IRS Get Transcript tool, and payment arrangements are set up through the IRS payment plans page once your returns have posted.

When you can handle this yourself — and when help changes the outcome

Plenty of never-filed cases are genuinely DIY. If your unfiled years are W-2 jobs with withholding, no SFR assessments exist yet, and no levy notice has arrived, you can pull transcripts, file the six years with tax software or a preparer, and likely discover the damage is smaller than you feared — some years may even hold refunds. If you're being harmed by an IRS delay or error along the way, the Taxpayer Advocate Service is a free, independent resource.

Experienced help changes outcomes in specific situations: an LT11 clock already running, SFR assessments that need to be rebuilt and replaced, multiple self-employed years with thin records, a corrected balance still above $50,000, or passport certification in play. In those cases the sequencing — hearing request, returns, SFR reconsideration, then resolution — determines what you ultimately pay, and getting the order wrong closes doors. The mistake that costs the most is agreeing to pay the SFR number before filing your real returns.

Terms on your notices, decoded

- Substitute for Return (SFR): a return the IRS prepares for a non-filer using reported income only — single, no deductions, no expenses — which becomes a legal assessment if you don't respond.

- Wage and income transcript: the IRS's year-by-year record of every W-2, 1099, and information return filed under your SSN — the source documents for your back returns.

- CSED: the Collection Statute Expiration Date — the IRS gets 10 years to collect from the date a tax is assessed; unfiled, unassessed years have no clock running at all.

- Refund statute: the three-year window after a return's due date to claim a refund; miss it and the money is forfeited permanently.

- Levy vs. lien: a lien is a legal claim against what you own; a levy is the actual taking — from a bank account (21-day hold) or a paycheck (continuous until released).

- CDP rights: Collection Due Process — your right, after a final notice like LT11, to request a hearing within 30 days (Form 12153) before levies begin.

Never filed taxes? Your scariest questions, answered

Can you go to jail for never filing taxes?

Jail is reserved for willful, provable tax evasion — not for people who come forward voluntarily. Criminal non-filing prosecutions are rare and almost always involve large income, fraud indicators, or ignoring direct IRS contact. Filing your back returns before the IRS opens an investigation is the strongest protection you have; the realistic cost of never filing is civil penalties and interest, not handcuffs.

How many years of unfiled tax returns do I have to file?

Generally six years, under IRS Policy Statement 5-133. In most cases the IRS considers you back in filing compliance once the last six years of required returns are in, even if you have never filed in your life. A revenue officer can demand more years in unusual situations — large business income or existing SFR assessments on older years — so confirm before assuming older years are closed.

Will I get refunds for the years I never filed?

Only for returns filed within three years of their original due date. If withholding or credits would have produced a refund, you can still claim it for roughly the last three filing years — after that, the money is forfeited permanently. Many first-time filers discover the IRS actually owed them for recent years, even while older years show balances.

What if I have no W-2s or records from those years?

The IRS already has them. Wage and income transcripts list every W-2, 1099, and most other information returns filed under your Social Security number, generally covering about the last ten years. You can pull them through your IRS online account or by mail, and a tax professional can pull them with a signed authorization — most back returns are built almost entirely from these transcripts.

What is a substitute for return, and is the amount real?

An SFR is a return the IRS prepares for you using only reported income — filed as single with no dependents, no itemized deductions, and no business expenses. The assessed amount is legally collectible but usually overstated, sometimes badly. Filing your own accurate return for that year asks the IRS to replace the SFR figures, which is often the single biggest reduction available to a non-filer.

Do I owe taxes for every year I never filed?

No. Years when your income fell below the filing threshold did not require a return at all, and years with enough paycheck withholding may show refunds rather than balances. Only years where tax was genuinely due — commonly self-employment years with no withholding — carry a balance. That is why pulling transcripts before panicking matters: the real number is often smaller than the fear.

Can the IRS levy my bank account or wages if I never filed?

Yes, once it assesses tax through a substitute for return and sends a final notice of intent to levy. A bank levy freezes funds for 21 days before the bank sends them to the IRS; a wage levy is continuous until released. If you have received an LT11 or Letter 1058, you have 30 days to request a Collection Due Process hearing before levies can begin.

Should I just start filing this year and hope the IRS never notices the past?

Filing the current year is good — but it does not erase assessed SFR balances or stop collection on them, and it will not qualify you for a payment plan, hardship status, or an Offer in Compromise, all of which require full filing compliance. Catching up the last six years voluntarily costs less than waiting for the automated system to find you, because penalties and interest grow monthly either way.

Your next 24 hours

- Open every IRS envelope and find the most recent notice — look for "LT11" or "Letter 1058" near the top and note the date printed on it; that date starts your 30-day hearing window if one exists.

- Log into (or create) your IRS online account and download wage and income transcripts for the last six years — that stack of pages is the entire record you need to start.

- Get your situation reviewed free — call (888) 825-7779 or use the 2-minute form at the top of this page. Whether or not a levy clock is running, the failure-to-file penalty and interest are growing every month you wait, and coming forward first is what keeps every option open.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.