Unfiled Returns

How to File Back Taxes Without Records (2026 Guide)

The short answer: you can file back taxes without records because the IRS already has your income data. Free wage and income transcripts show every W-2, 1099, and 1098 filed under your SSN for roughly the last ten years. Pull them, rebuild each return, file, then resolve the balance.

You need to file back taxes without records — the W-2s are gone, the shoebox never existed, and maybe a move, a divorce, or a closed business took whatever paperwork you had. Here's the part almost nobody tells you: missing records are the most solvable problem in an unfiled-return case, because employers, banks, brokers, and clients already sent the IRS a copy of nearly every income document you're missing.

Your job isn't to recreate a filing cabinet. It's to pull the IRS's own copy of your income history, rebuild your deductions from third-party sources, and file returns the IRS will accept. Further down, the image on this page shows you exactly what a wage and income transcript looks like and where each year's reported income appears — so you'll recognize what you're reading the moment you download yours.

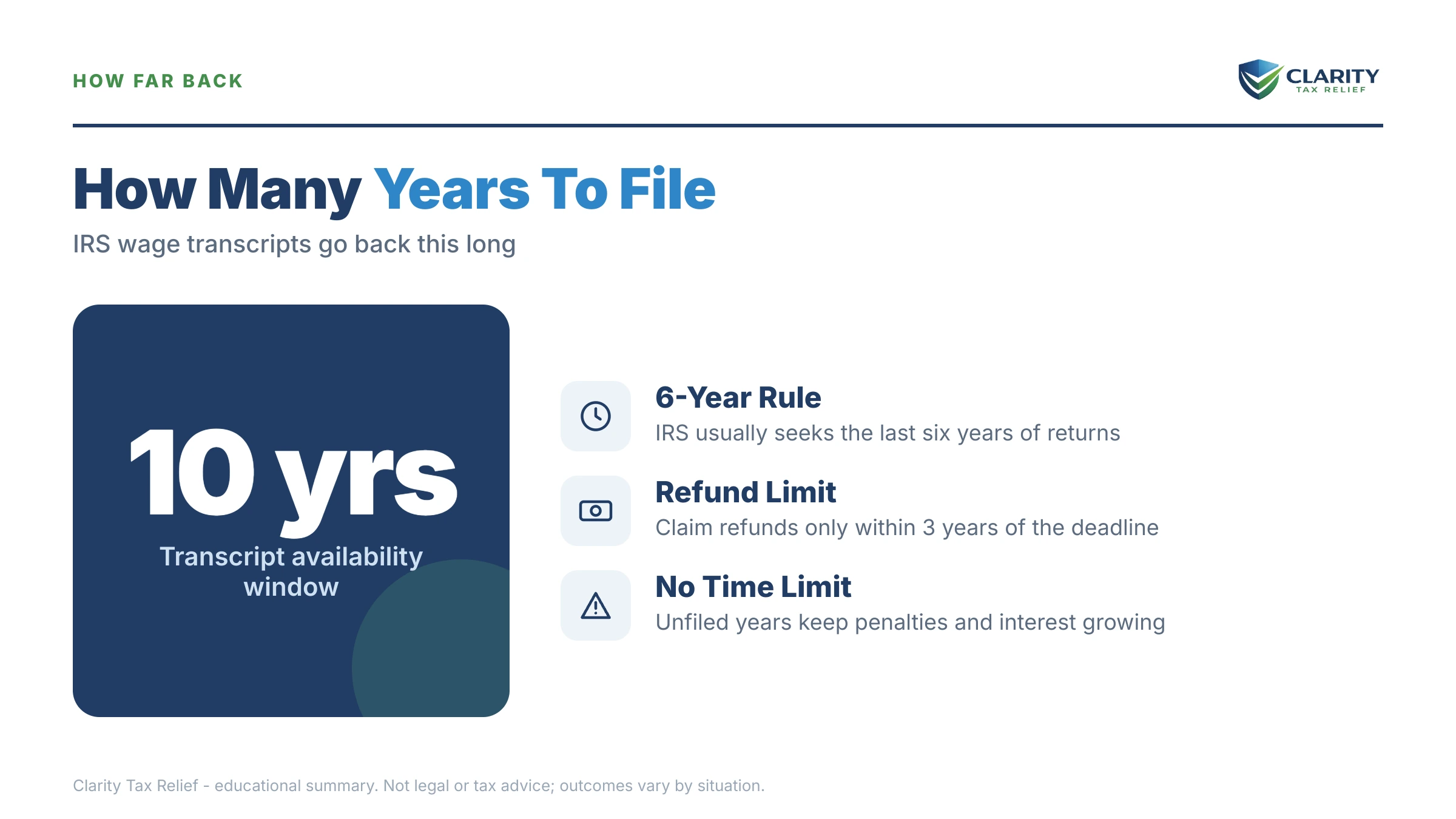

⏱ The real clocks: there's no single due date for old returns, but two clocks are running. You have 3 years from a return's original due date to claim any refund from that year — after that, the money is gone forever. And on years where you owe, the failure-to-file penalty grows at 5% per month (reduced to 4.5% in months where the failure-to-pay penalty also applies, keeping the combined rate at 5%) until it caps at 25%, with interest compounding on top.

Why you're filing without records — and why it doesn't stop you

Most unfiled-return cases involve missing records, because the same disruption that stopped the filing usually scattered the paperwork. A job loss, a divorce, a death in the family, a business shutting down, a cross-country move, a flood — the return didn't get filed and the documents didn't get kept. That's the normal version of this problem, not the exception.

The system is built for it. Every employer that issued you a W-2, every client that issued a 1099-NEC, every bank that paid you interest, every broker that sold your stock, and every mortgage lender that received your interest payments filed an information return with the IRS. That third-party data sits in your file for roughly ten years, retrievable free as a wage and income transcript.

What the IRS does not have is your deduction side: mileage, business expenses, dependents, your correct filing status, the cost basis on things you sold. That's exactly why filing your own reconstructed return almost always beats letting the IRS compute the year for you — its version uses your gross income and none of your write-offs.

What happens if you never file the missing years

Unfiled years don't fade out — they escalate through an automated sequence that ends with the IRS writing your return for you, at the worst possible numbers. The stages run in this order:

- CP59 notice — the IRS's records show income under your SSN but no return for the year. This is the polite ask.

- CP516 / CP518 — escalating reminders; CP518 is the final "file now" notice before the IRS acts on its own.

- Substitute for return (SFR) — the IRS prepares the year itself using only the reported income: no dependents, no deductions, typically the least favorable filing status. If this already happened to you, see the IRS filed a substitute return for me.

- CP3219N notice of deficiency — the formal assessment proposal. You get 90 days to file your own return or petition Tax Court; silence lets the inflated SFR balance become legally assessed.

- Collection — once assessed, the balance enters the ordinary billing-and-levy stream: balance-due notices, a possible federal tax lien, then levy authority against wages, bank accounts, and state refunds.

Two quieter consequences hurt just as much. Refund years expire — file more than three years late and the refund from 3 years ago is forfeited outright. And an unfiled year never closes: the assessment statute of limitations doesn't even start running until a return is filed, so a 2015 non-filed year is just as open in 2026 as it was then. Filing is what starts every protective clock you have.

Years unfiled and no paperwork to start from?

We pull your IRS transcripts, tell you exactly which years the IRS wants and what it already knows about each one, and map the cheapest route to compliant — free, confidential, before penalties grow another month.

How to get your records back: every source, by document

Nearly every document a back-tax return needs can be replaced from a third party, and the most important source — the IRS itself — is free. Start with your IRS online account, or mail Form 4506-T if you can't verify identity online (our walkthrough: how to get IRS transcripts online). Then work down this list for whatever the transcripts don't cover.

| Missing record | Replacement source | How to get it |

|---|---|---|

| W-2s, 1099s, 1098s, K-1 data reported to IRS | IRS wage & income transcript (free) | IRS online account, or Form 4506-T by mail; roughly 10 years available |

| Copies of returns you actually filed | IRS tax return transcript (free) or Form 4506 (fee) for a full copy | Online account for the transcript; mail Form 4506 for exact copies |

| Self-employment income with no 1099s | Bank and payment-app statements | Request archived statements from your bank; total deposits, back out transfers |

| Business expenses and receipts | Bank/credit-card statements, vendor reprints | Card issuers keep years of statements; suppliers can reissue invoices |

| Mortgage interest and property taxes | Lender payoff history, county tax records | Ask your servicer for year-end 1098 reprints; county records are public |

| Lifetime earnings verification | Social Security Administration earnings record | Free at ssa.gov via your my Social Security account |

| State withholding and state copies | Your state revenue agency or old employer's payroll provider | Most states supply their own wage records on request |

One timing caveat: a wage and income transcript for the most recent tax year isn't complete until payer filings finish processing, usually by summer. For any older year, the data is settled and reliable. If a specific employer's W-2 truly never shows up, getting old W-2s for back taxes covers the fallback routes — including Form 4852, the substitute W-2 you can file with your best evidence.

Rebuilding the deduction side the IRS can't see

Transcripts rebuild your income, but your deductions have to be reconstructed from your own money trail — and reasonable, documented reconstruction is accepted practice, not a trick. The standard is credibility: numbers tied to bank records, contemporaneous evidence, and sensible methodology.

- Self-employment expenses: pull every bank and card statement for the year and categorize the business charges. Recurring items — software, insurance, phone, supplies — establish patterns that support the year's totals.

- Vehicle mileage: rebuild a mileage log from calendars, job records, and route history. A reconstructed log beats a guess; it's the same approach we cover for gig drivers who didn't track miles.

- Cost basis on sales: brokers report proceeds to the IRS but old transcripts may not show your basis. Request historical statements from the broker — without basis, the SFR treats the entire sale as gain.

- Dependents and filing status: school, medical, and lease records establish who lived with you. This alone can swing a year from balance-due to refund.

If your missing years involve rental or platform income — the pattern we see with Airbnb host back taxes — reconstruct the platform's payout history first; hosts routinely overpay by forgetting cleaning fees, commissions, and depreciation that never hit their bank as income.

How many years do you actually have to file?

IRS policy generally treats you as compliant once your last six years of returns are filed. That's the practical scope of most catch-up projects, and it's why "I haven't filed since 2009" rarely means preparing seventeen returns. The full rule, and its exceptions, are in how many years of back taxes you have to file.

Three situations pull years back into scope beyond the six: a year where the IRS already filed an SFR (file your own return to replace the inflated numbers), a year with a refund still inside its three-year window (file it or lose the money), and a case assigned to a revenue officer who specifically demands more years. Filing order matters: refund years first — their deadlines are hard, and their refunds can offset the balance-due years.

And keep filing forward while you catch up. Skipping the current year because old years are open makes everything worse — here's whether you should file this year if you owe back taxes (short version: always).

A worked example: $61,200, no records, and a refinance on the line

Say you own your home, you're planning to refinance, and four unfiled years — rebuilt entirely from transcripts and bank statements — come out to $61,200 in combined tax, penalties, and interest. This is hypothetical, but the math is real:

- The refinance is blocked until you file. Underwriters pull IRS transcripts; four missing years is an automatic condition on the loan. Filing is step one no matter what.

- At $61,200 you're over the $50,000 line for a streamlined online installment agreement. Above it, the IRS wants a Form 433-F financial disclosure — slower, more invasive, and more likely to trigger a federal tax lien filing, which is exactly what a refinance can't absorb (see refinancing with an IRS lien).

- Pay down $11,200 and the picture changes. At $50,000, a streamlined installment agreement can be set up online with no financial statement: $50,000 ÷ 72 months ≈ $695/month, with interest and the 0.5%/month late-payment penalty still accruing on the declining balance, so paying faster than 72 months saves real money.

- Watch the passport line. The 2026 certification threshold is $66,000. At $61,200 you're about $4,800 below it — and accrual alone can push a parked balance across, putting your passport at risk on top of the loan.

- Penalty relief may shrink the number before you ever pay it. If the earliest unfiled year followed three clean years, first-time abatement can strip that year's penalties; documented disaster, illness, or records destroyed beyond your control supports reasonable cause on the others. On four late years, the failure-to-file penalty alone can be a five-figure chunk of the $61,200 — you can rough out your own exposure with our Penalty & Interest Calculator.

The sequence for this reader: file all four years, request abatement, pay the balance to $50,000, lock the direct-debit streamlined agreement — then go to the lender with filed returns and a payment history instead of a red flag.

Your options for the balance once the returns are filed

Filing converts an open-ended non-filer problem into an ordinary balance due — and balances have a defined menu of fixes. The full DIY playbook for working this menu lives in our guide to how to settle tax debt yourself; here's the map:

| Option | Typical eligibility | Cost & key notes |

|---|---|---|

| Short-term payment plan | Can pay in full within 180 days | $0 setup; interest and penalties continue but collection pauses |

| Streamlined installment agreement | Balance ≤ $50,000 (assessed) | Up to 72 months, set up online, no financial statement required |

| Non-streamlined installment agreement | Balance over $50,000 | Form 433-F financial disclosure; lien filing more likely |

| Currently Not Collectible | Paying anything would prevent basic living expenses | Collection pauses; debt and interest remain; reviewed periodically |

| Offer in Compromise | Assets + future income genuinely can't cover the debt; all returns filed first | $205 fee, 20% down on lump-sum offers (both waived if AGI ≤ 250% of poverty); per IRS data, roughly 1 in 5 offers were accepted in FY2024 |

| Penalty abatement | Clean prior 3 years (FTA) or documented reasonable cause | Free to request; from summer 2026 the new Automatic Exemption from Penalty (AEP) applies some relief with no request at all |

Two notes on that table. Filing every required year is a hard prerequisite for an Offer in Compromise and for most agreements — another reason filing comes first. And penalty relief stacks with everything else: abate first, then set up the plan on the smaller number. Details in our first-time penalty abatement guide.

Deadlines and rights: the clocks running on unfiled years

Every unfiled year sits inside a web of statutes, and each one either protects you or protects the IRS depending on whether you file. This is the reference most readers screenshot:

| Clock | Window | What's at stake |

|---|---|---|

| Refund statute (RSED) | 3 years from the return's original due date | File late and the refund — including withholding — is permanently forfeited |

| CP3219N deficiency notice | 90 days from the notice date | Your right to file your own return or petition Tax Court before the SFR balance is assessed |

| Assessment statute | Never starts on an unfiled year | The year stays open indefinitely until you file; filing starts the clock |

| Collection statute (CSED) | 10 years from assessment | The IRS's window to collect — it hasn't even begun on years never assessed |

| Passport certification | Balance reaches $66,000 (2026 threshold) | State Department can deny or revoke your passport while certified |

| Failure-to-file penalty cap | 5% per month (4.5% in months where failure-to-pay also applies, 5% combined), capped at 25% (month 5) | On old years the cap is usually already hit — filing today costs no more FTF penalty than filing was going to |

That last row surprises people in the best way: if a year is more than five months late, the failure-to-file penalty is already maxed. Waiting longer adds interest and failure-to-pay penalty, but the big 25% hit is sunk — so there's no penalty reason left to delay. The difference between the two penalties is broken down in failure-to-file vs. failure-to-pay.

How to file back taxes without records, step by step

- Pull your IRS transcripts. Request free wage and income transcripts and account transcripts for every unfiled year through your IRS online account or Form 4506-T.

- Confirm which years the IRS wants. In most cases the last six years — plus any year with a substitute return on file or a refund still inside the three-year window.

- Rebuild each year's income and deductions. Match every return to the transcript's reported income, then reconstruct deductions from bank statements, lender records, and reasonable mileage and expense estimates.

- File the refund years first, then the rest. Paper-file each old-year return to the address in that year's form instructions and keep certified-mail proof for every envelope.

- Resolve the balance the same week you file. Set up a payment plan, request penalty abatement, or document hardship before the balances hit the automated collection stream.

- Monitor your account transcripts. Watch each year until the return posts and the assessed balance matches what you filed, and fix mismatches in writing.

When you can handle this yourself — and when help changes the outcome

Plenty of back-tax filings without records are genuinely a do-it-yourself project. You're a good DIY candidate if: your missing years were W-2 wage years (the transcript basically is the return), you have one or two years to catch up, the resulting balances are small enough to pay within 180 days or fit a simple online plan, and no IRS notices beyond a CP59 have arrived. Old-year software or a VITA site plus your transcripts will get you there.

Experienced help earns its cost when the stakes or the reconstruction get heavy: an SFR has already been filed or a CP3219N's 90-day clock is running; multiple self-employment years need deposit-analysis reconstruction; the combined balance clears $50,000 and lien exposure threatens a mortgage, refinance, or security clearance; a revenue officer is assigned; or the unfiled years include a business with payroll — where the exposure turns personal fast (see 941 back taxes and LLC back taxes and personal liability). In those cases, the order of operations — replace SFRs, abate penalties, then negotiate the balance — routinely changes the final number by more than the fee.

If your situation looks like the second list — especially with a lien threatening a home loan — have an experienced tax professional review your transcripts free before you file anything; the filing order is the one thing you can't easily undo.

Terms on your transcripts and notices, decoded

- Wage and income transcript — the IRS's free record of every W-2, 1099, 1098, and similar form filed under your SSN for a given year.

- Substitute for return (SFR) — a return the IRS prepares for a non-filer using only reported income, with no deductions and the least favorable status.

- Form 4506-T — the mail-in request for free IRS transcripts when you can't use the online account.

- Form 4852 — the substitute W-2/1099-R you attach when an employer's original can't be obtained.

- RSED (Refund Statute Expiration Date) — the deadline, generally 3 years from the due date, after which an unclaimed refund is forfeited.

- CSED (Collection Statute Expiration Date) — the end of the IRS's 10-year window to collect an assessed balance; it can be paused by appeals, offers, or bankruptcy.

Filing back taxes with no records: your questions, answered

Can I file back taxes with no records at all?

Yes. The IRS already holds copies of every W-2, 1099, and 1098 that employers, banks, and clients filed under your Social Security number, and you can pull them free as wage and income transcripts. Those transcripts rebuild your income side completely for roughly the last ten years. Deductions take more work — bank statements, lender records, and reasonable reconstruction fill that gap.

How far back do IRS wage and income transcripts go?

Wage and income transcripts are generally available for roughly the past ten years through your IRS online account or Form 4506-T. That covers every year the IRS typically requires you to file under its six-year lookback policy. One caveat: the current year's data isn't complete until employers' and payers' filings finish processing, usually by summer.

How many years of back taxes do I have to file?

In most cases, six years. IRS policy generally treats a taxpayer as compliant once the last six years of returns are filed, though a revenue officer can require more in unusual cases. Years where the IRS already filed a substitute return, or where you're owed a refund inside the three-year window, are worth filing even if they fall outside the six.

What if I was self-employed and never got 1099s?

You can still reconstruct your income. Any 1099-NEC, 1099-MISC, or 1099-K a client or payment processor actually filed appears on your wage and income transcript. For cash and unreported payments, total your bank deposits for each year and back out transfers and non-income items. The IRS uses the same bank-deposit method itself, so a deposit-based reconstruction is credible.

Will I get in trouble for filing old returns voluntarily?

Coming forward voluntarily is overwhelmingly the safest path. The IRS pursues criminal non-filing cases rarely, and almost never against people who file before the agency contacts them. The realistic consequences are civil — the failure-to-file penalty of 5% per month, capped at 25% (reduced to 4.5% in months where the failure-to-pay penalty also applies, for a 5% combined rate), plus interest — and filing is what stops those penalties from growing.

Can I still get a refund from an old unfiled year?

Only within three years of the return's original due date. File inside that window and the IRS pays the refund; miss it by even a day and the money is forfeited permanently — it can't even be applied to other years you owe. If any unfiled year had solid withholding, that year should be filed first.

What is a substitute for return, and can I undo one?

A substitute for return (SFR) is a return the IRS files for you using only reported income — no dependents, no itemized deductions, usually the least favorable filing status. Yes, you can replace it: file your own original return for that year and the IRS will generally adjust the balance to your correct, lower figure.

Can I refinance my house with unfiled back taxes?

Usually not until the returns are filed. Lenders pull IRS transcripts during underwriting, and unfiled years or a fresh federal tax lien can stall or kill the loan. Most lenders will work with a balance that's inside an installment agreement with payments being made — so the sequence is file, set up the agreement, then close.

What if my records were destroyed in a fire, flood, or disaster?

Reconstruction still works, and the disaster itself may help you. IRS transcripts replace the income documents, and lenders, banks, and county records replace most of the rest. A federally declared disaster or documented casualty is also classic reasonable cause for removing failure-to-file and failure-to-pay penalties on the affected years.

Do I need my original W-2s to file old returns?

No. Your wage and income transcript shows the same wage and withholding data the employer reported, and that's sufficient to prepare the return. If a year's transcript is incomplete, Form 4852 lets you file with a substitute W-2 based on your best evidence, such as final pay stubs.

Your next 24 hours

- Open (or create) your IRS online account and download the wage and income transcript plus the account transcript for every year you didn't file — it's free, and it tells you what the IRS already knows, including whether any SFR exists.

- Gather your money trail: request archived bank and credit-card statements for the missing years, plus your mortgage servicer's payment history — that's the raw material for every deduction the transcripts can't show.

- Get the plan before you file anything. Send us what you found — or nothing at all — and an experienced tax professional will map which years to file, in what order, and how to handle the balance, free: the 2-minute form or (888) 825-7779. Every month unfiled adds interest and late-payment penalty; the reconstruction gets no easier by waiting.

Primary sources: the IRS's transcript portal at Get Transcript, the official Form 4506-T page, and current plan terms at IRS payment plans and installment agreements.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.