IRS Payment Plans

Streamlined Installment Agreement: The Under-$50,000 IRS Payment Plan (2026)

The short answer: a streamlined installment agreement is an IRS monthly payment plan for individuals who owe $50,000 or less in combined tax, penalties, and interest. You get up to 72 months to pay, no financial statement is required, and balances between $25,001 and $50,000 must be paid by direct debit or payroll deduction.

The IRS letter threatening to take your money is sitting next to this month's rent check — and because you rent, there's no house for the IRS to sit on. A levy would go straight for what you actually have: your paycheck and your bank account. If your total balance is under $50,000, though, you're standing in front of the widest door the IRS offers, and this guide shows exactly how to walk through it before the levy lands.

⏱ Two clocks matter here. If an LT11 or Letter 1058 is in your stack, you have 30 days from its date to request a Collection Due Process hearing. And every month you wait, the 0.5% failure-to-pay penalty plus interest pushes your balance closer to the $50,000 cutoff — cross it, and the streamlined door closes.

What a streamlined installment agreement is — and the 2026 limits

A streamlined installment agreement lets an individual who owes the IRS $50,000 or less pay over up to 72 months without submitting a financial statement. "Streamlined" is the IRS's own word for it: because the balance is under the threshold, the agency approves the plan on the numbers alone — no Form 433-F, no bank statements, no line-by-line review of your rent, groceries, and car payment.

The program has two tiers. At $25,000 or less, you can pay by any method you like — check, Direct Pay, card, or bank draft. From $25,001 to $50,000, the IRS requires a direct debit installment agreement or a payroll-deduction agreement; a manual monthly check is not an option at that tier. The $50,000 test counts everything the IRS has assessed against you — tax, penalties, and interest, across every year you owe — not just the tax line.

Two boundaries define the term length. Your payments must full-pay the balance within 72 months, or by the collection statute expiration date if that comes first — if the IRS's 10-year collection statute runs out in four years, four years is your ceiling. And one quiet benefit is easy to miss: the IRS generally does not file a Notice of Federal Tax Lien on a streamlined agreement, which matters enormously if you ever want to finance a car, pass a rental application's credit screen, or buy a home.

If you owe $10,000 or less, an even simpler version exists — the guaranteed installment agreement, which the IRS must accept if you meet its conditions. (And to clear up a naming collision: this has nothing to do with the IRS's "streamlined" offshore filing procedures for expats — completely different program.) For the general click-by-click of the application itself, see our walkthrough on how to set up an IRS payment plan online; the rest of this page covers what's unique to the streamlined tier.

| Agreement type | Balance limit | Financial disclosure | Key requirement |

|---|---|---|---|

| Guaranteed | $10,000 or less | None | Full pay within 3 years; clean filing history |

| Streamlined | $25,000 or less | None | Full pay within 72 months (or by the CSED); any payment method |

| Streamlined (upper tier) | $25,001–$50,000 | None | Direct debit or payroll deduction required |

| Non-streamlined | Over $50,000 | Form 433-F required | Payment negotiated from your financials; lien determination standard |

| Large-dollar / revenue officer | Over $100,000 | Full financials + asset review | Usually assigned to a human collector |

Do you qualify? Streamlined installment agreement requirements

Eligibility comes down to three tests: a combined assessed balance of $50,000 or less, every required return filed, and a payment that full-pays within 72 months. There is no income limit and no hardship showing — the streamlined program is deliberately open. But a handful of situations change the answer:

- Married filing jointly: a joint balance is one debt owed by both of you, and it counts once toward the $50,000 test. Either spouse can set up the agreement, but both remain fully liable, and a default exposes both.

- Self-employed or 1099: you can absolutely get a streamlined agreement — but "staying compliant" means making your quarterly estimated payments. A new balance at next April's filing is the single most common way self-employed taxpayers default a plan they just set up.

- Business and payroll debt: the individual streamlined program covers 1040 balances (including a sole proprietor's income and self-employment tax). Payroll tax owed by an operating business runs on different, stricter rails.

- Multiple years: all of them ride on one agreement, and all of them count toward $50,000. If an old year is still unfiled, nothing gets approved until it's in — the IRS generally wants the last six years filed.

- Disputed amounts: don't lock a payment plan onto tax you don't actually owe. If the balance came from a CP2000 you disagree with or an audit you never responded to, fixing the number first — through a response, audit reconsideration, or amended return — can shrink or erase the debt a plan would have paid.

- Just over the line: at $52,000 or $55,000, a lump-sum payment that brings the assessed balance to $50,000 or below can restore streamlined eligibility and spare you the full financial disclosure a plan over $50,000 requires. Run that math before you apply, not after a rejection.

One more thing an IRS agreement does not do: cover state tax. State revenue agencies run their own payment plans on their own thresholds, so a state balance needs its own arrangement.

What happens if you skip the payment plan: the levy sequence

IRS collection escalates through an automated notice sequence that ends in levy — and in 2026, with the IRS workforce down roughly 27%, the automated side is the part still running at full speed. Nobody reviews your file before the next notice goes out. The stages, in order:

- CP14 — the first bill. No enforcement power yet; the cheapest moment to set up your agreement.

- CP501 / CP503 — reminder notices, weeks apart. Still just bills, but the balance is compounding.

- CP504 — Notice of Intent to Levy. The IRS can now seize your state tax refund.

- LT11 / Letter 1058 — the final notice. A 30-day clock starts on your Collection Due Process rights; after it runs, wage and bank levies become legal.

- Levy — a bank levy freezes funds for 21 days before they're sent to the IRS; a wage levy is continuous, paycheck after paycheck, until released. Up to 15% of Social Security can go through the Federal Payment Levy Program.

Here's the part most people don't know: the streamlined door never closes because of the stage you're at. You can set up the same agreement after an LT11 that you could have after a CP14 — and once a valid installment agreement request is pending, levy action is generally suspended while the IRS considers it, while the agreement is in effect, and for 30 days after any rejection or termination. What changes as you wait is the price: more penalty, more interest, and the risk that accruals push you past $50,000 into financial-disclosure territory.

| Notice | What it can do | Your window | Streamlined IA still available? |

|---|---|---|---|

| CP14 | First bill; no enforcement | Typically about 21 days before the next notice queues | Yes — the cheapest moment to act |

| CP501 / CP503 | Reminders; balance compounding | Pay-by date printed on each notice | Yes |

| CP504 | State tax refund can be seized | 30 days printed on the notice | Yes |

| LT11 / Letter 1058 | Final notice before wage/bank levy | 30 days to request a CDP hearing | Yes — and a pending request generally suspends levy |

| Levy served | Bank funds held 21 days; wage levy continuous | 21-day bank hold before funds transfer | Yes — an approved agreement is grounds to request release |

Facing a levy with a balance under $50,000?

A streamlined agreement can shut the levy machine down — but it works best in place before the levy lands, and if you're holding an LT11, the 30-day hearing window is already running. Get your notices and balance reviewed free by an experienced tax professional — no pressure, no obligation.

Streamlined IA vs. your other options

A streamlined agreement is the default answer for balances under $50,000 — but it isn't the only one, and for some budgets it's the wrong one. The honest comparison:

- Short-term payment plan (up to 180 days): $0 setup fee, no monthly commitment — you just pay in full within the window. If you can clear the balance in six months, this beats a streamlined agreement outright because you skip the setup fee. Disqualifier: you actually have to have the money coming.

- Streamlined installment agreement: $22–$178 setup, up to 72 months, no financial disclosure, generally no lien. Disqualifiers: unfiled returns, or a combined balance over $50,000.

- Partial-pay installment agreement: a monthly payment based on what you can actually afford, even if it never full-pays before the 10-year statute runs. Requires Form 433-F disclosure and periodic re-review — see the partial payment installment agreement guide. Disqualifier: meaningful equity or income the IRS thinks should go to the debt first.

- Currently Not Collectible: collection pauses when paying anything would leave you unable to cover basic living expenses. The debt, interest, and refund offsets continue, and the IRS re-checks your income. Disqualifier: a budget that can support even a modest payment.

- Offer in Compromise: settling for less than you owe — real, means-tested, and slow. The application costs $205 (waived with low-income certification), lump-sum offers require 20% down, and the IRS accepted roughly 1 in 5 offers in FY2024. If your income comfortably covers a $671-a-month plan, your offer math almost certainly doesn't work; the payment plan vs. offer in compromise comparison shows how the IRS decides.

- Penalty relief on top: whichever route you take, first-time abatement can strip penalties if your prior three years were clean — and starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) begins applying that relief automatically, no request needed. Reasonable cause covers illness, disaster, and similar events.

What a streamlined installment agreement costs in 2026

Setting up a streamlined installment agreement costs between $0 and $178, depending on how you apply and how you pay. Online with direct debit is the cheapest by far — and since direct debit is mandatory above $25,000 anyway, most people at the upper tier should simply apply online.

| How you apply | How you pay | Setup fee |

|---|---|---|

| Online Payment Agreement tool | Direct debit | $22 |

| Online Payment Agreement tool | Check, Direct Pay, or card each month | $69 |

| Phone, mail (Form 9465), or in person | Direct debit | $107 |

| Phone, mail (Form 9465), or in person | Other methods | $178 |

| Low-income certified (AGI ≤ 250% of federal poverty level) | Direct debit | $0 (waived) |

| Low-income certified | Other methods | $43, reimbursable at completion |

The setup fee is the small cost. The real cost is accrual: interest keeps running on the unpaid balance for the entire life of the agreement, compounding at the federal underpayment rate. There's one built-in break — the failure-to-pay penalty is cut in half, from 0.5% to 0.25% per month, while an installment agreement is in effect for a return you filed on time. You can estimate how fast your own balance is growing with our IRS Penalty & Interest Calculator, and there's no prepayment penalty, so every extra dollar you send shortens the accrual clock.

Say you owe $48,300: the worked math

Here's a hypothetical to make it concrete. Say you owe $48,300 across two tax years, you rent, you're paid W-2, and an LT11 arrived last week.

- Minimum payment: $48,300 ÷ 72 = roughly $671 per month. (The online tool may quote slightly more, because it calculates a payment that covers interest accruing along the way.)

- Method: your balance is over $25,000, so direct debit or payroll deduction is required. Applying online with direct debit, setup costs $22.

- The accrual break: with the agreement in effect, the failure-to-pay penalty on $48,300 drops to about $121 in the first month instead of $242 — shrinking further as the balance falls.

- Paying faster: at $1,000 a month instead of $671, the principal alone clears in about 48 months — call it a bit over four years once interest is added, instead of six. That's roughly two fewer years of interest compounding against you.

- The cost of waiting: unresolved, the balance grows by roughly $242 a month in failure-to-pay penalty alone, plus interest on top. Drift for a few months and $48,300 can cross $50,000 — at which point streamlined is off the table and the IRS gets to examine your finances line by line before naming your payment.

- The cost of doing nothing: after the LT11's 30 days run, a bank levy can freeze whatever is in your account (held 21 days, then gone), and a wage levy attaches to every paycheck until released. For a renter with no home equity, your paycheck is the collateral.

The bottom line of the example: about $22 and twenty minutes online converts a levy threat into a predictable $671-a-month bill — with no lien filed and no financial interrogation.

How to set up a streamlined installment agreement, step by step

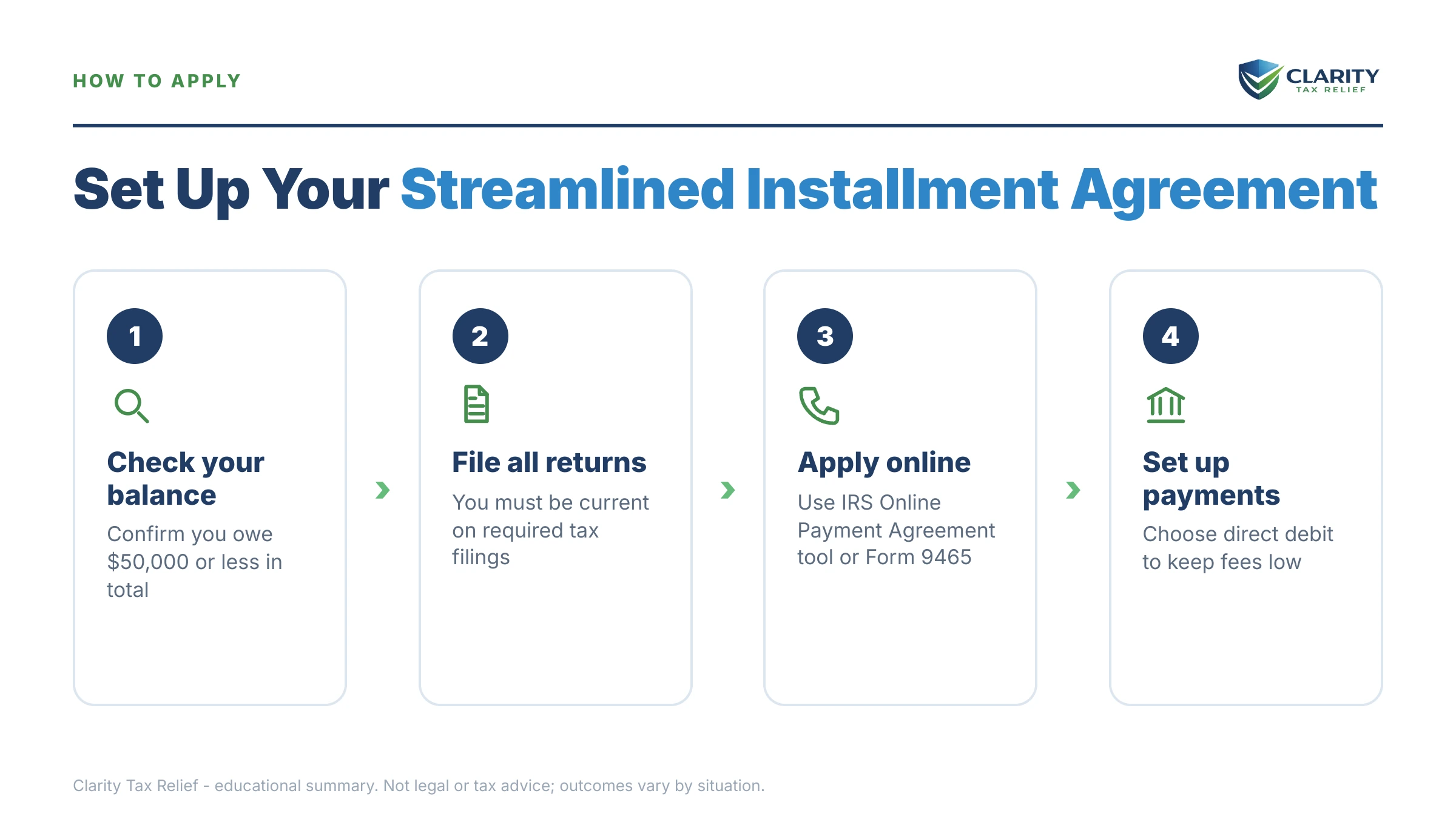

- File any missing returns. The IRS will not approve a payment plan while required returns are unfiled, so filing compliance is step zero.

- Verify your exact combined balance. Log in to your IRS online account and total every year you owe — the $50,000 streamlined limit applies to tax, penalties, and interest combined.

- Pick a monthly payment you can sustain. The minimum is roughly your balance divided by 72, but choose the highest number you can hold every month — a defaulted plan is worse than a slower one.

- Apply through the Online Payment Agreement tool with direct debit. Online with direct debit carries the lowest setup fee ($22) and direct debit is required anyway above $25,000; the tool lives at the IRS's Online Payment Agreement application. If you can't apply online, mail Form 9465 and expect Form 433-D to finalize the bank draft.

- Protect your CDP rights if a final levy notice arrived. If an LT11 or Letter 1058 is dated within the last 30 days, file Form 12153 to preserve your hearing rights while the agreement is processed.

- Stay compliant going forward. File on time and adjust withholding or quarterly estimates so no new balance appears — a fresh liability is the most common reason streamlined agreements default.

Already facing a levy? Sequence matters

An installment agreement request generally suspends new levy action while the IRS considers it — which makes speed your best defense. If the LT11's 30-day window is still open, you can do both things at once: request the Collection Due Process hearing to freeze enforcement and preserve appeal rights, and propose the streamlined agreement as your collection alternative inside that process. If the window has already closed, apply anyway — the pending request still generally holds off the levy machinery while it's processed.

If a bank levy has already been served, the money doesn't leave immediately: your bank must hold the funds for 21 days before sending them to the IRS. An approved agreement — or a hardship showing — during that hold is grounds to request the levy's release. A wage levy is harsher: it's continuous, taking a slice of every paycheck until the IRS formally releases it, which an active installment agreement supports. Timelines here are unforgiving, and this is the one scenario in this guide where hours genuinely matter.

Two related protections come along with an agreement in good standing. Your account isn't certified as "seriously delinquent" for passport purposes — relevant if a balance ever grows past the 2026 threshold of $66,000. But one thing an agreement does not protect is your refund: the IRS keeps federal refunds and applies them to the balance for as long as the plan runs, as covered in will the IRS take my refund on a payment plan.

When you can set this up yourself — and when help changes the outcome

Most people who qualify for a streamlined installment agreement can set it up themselves, online, in about twenty minutes. If your returns are all filed, your balance is comfortably under $50,000, no levy notice has arrived, and the 72-month minimum fits your budget, you do not need to pay anyone — use the online tool and be done.

Experienced help earns its cost in specific situations: a levy already served or an LT11 clock already running, where the CDP filing and release request have to be sequenced correctly; multiple unfiled years that must be prepared before anything can be approved; a balance near or over $50,000, where paying down to the streamlined line versus disclosing financials is a real strategic fork; a minimum payment you genuinely can't afford, where the right answer may be a partial-pay agreement, hardship status, or offer math instead; and any business or payroll component, which runs on different rules entirely. In those cases the question isn't whether you can file the forms — it's whether the order and framing leave money on the table.

Terms on your paperwork, decoded

- Direct debit installment agreement (DDIA): a plan where payments pull automatically from your bank account — required for streamlined balances over $25,000.

- Form 433-F: the Collection Information Statement — the financial disclosure streamlined agreements let you skip, and non-streamlined ones don't.

- CSED: the Collection Statute Expiration Date — the end of the IRS's 10-year window to collect; your plan must full-pay by then if it arrives before month 72.

- CP523: the notice the IRS sends when it intends to terminate a defaulted agreement — a warning with a cure window, not the termination itself. Details in the CP523 guide.

- Notice of Federal Tax Lien: the public filing that attaches the government's claim to your property — generally not filed while a streamlined agreement is in place.

- Collection Due Process (CDP): the formal hearing right that an LT11 or Letter 1058 triggers, requested on Form 12153 within 30 days.

If your balance is hovering near the $50,000 line or a levy notice is already in the stack, a free case review with an experienced tax professional can map the fastest route before accruals close the streamlined door — call (888) 825-7779.

Primary sources: the IRS's payment plans and installment agreements page carries current fees and terms (confirm the user fees there before applying), and the Taxpayer Advocate Service explains your rights if collection would cause hardship.

Streamlined installment agreement FAQs

What is the maximum amount for a streamlined installment agreement?

The limit is $50,000 in combined tax, penalties, and interest for individuals. Up to $25,000, you can pay by any method; from $25,001 to $50,000, the IRS requires direct debit or payroll deduction. If you owe slightly more than $50,000, paying the balance down below the line before applying can restore streamlined eligibility.

Do I need to submit a financial statement for a streamlined installment agreement?

No — skipping the financial statement is the defining benefit of the streamlined program. The IRS does not require Form 433-F, so it never reviews your bank balances, expenses, or assets. Once your combined balance passes $50,000, that changes: a non-streamlined agreement requires full financial disclosure, and the IRS may demand a higher payment based on what it calculates you can afford.

Does a streamlined installment agreement stop an IRS levy?

Generally, yes. Levy action is typically suspended while your installment agreement request is pending, while the agreement is in effect, and for 30 days after a rejection or termination. If a bank levy was already served, funds are held for 21 days before they're sent to the IRS — an approved agreement during that window is grounds to request a release.

Will the IRS file a tax lien if I'm on a streamlined installment agreement?

Usually not. One of the quieter benefits of the streamlined program is that the IRS generally does not file a Notice of Federal Tax Lien while a streamlined agreement is in place — for balances between $25,001 and $50,000, that protection is tied to paying by direct debit. On non-streamlined agreements over $50,000, a lien determination is standard.

How much does it cost to set up a streamlined installment agreement?

As little as $22 if you apply online and pay by direct debit, or $69 online with another payment method; applying by phone or mail costs $107 to $178. Low-income taxpayers (AGI at or below 250% of the federal poverty level) pay a reduced $43 fee — waived entirely with direct debit — and may have it reimbursed when the agreement is completed.

Does interest stop while I'm on a streamlined installment agreement?

No. Interest keeps accruing on the unpaid balance for the life of the agreement, which is why paying more than the minimum saves real money. There is one built-in break: the failure-to-pay penalty drops from 0.5% to 0.25% per month while an installment agreement is in effect for a return you filed on time.

What happens if I miss a payment on my streamlined installment agreement?

One missed payment doesn't automatically end the agreement — the IRS typically sends notice CP523, which announces its intent to terminate and gives you a short window to catch up. If you cure the default, the plan usually continues. If you don't, the agreement terminates, the full balance becomes collectible, and levy action can resume.

Can I pay off a streamlined installment agreement early?

Yes, and there is no prepayment penalty. Every extra dollar goes to the balance, which stops that portion from accruing interest and the monthly failure-to-pay penalty. Many people set the minimum payment for safety, then add lump sums from refunds, bonuses, or tax-season windfalls to finish years ahead of the 72-month schedule.

Will the IRS take my tax refund while I'm on a payment plan?

Yes. The IRS keeps any federal refund and applies it to your remaining balance for as long as the agreement runs — this is automatic and doesn't count as your monthly payment. It isn't a default or a penalty; it simply pays the debt down faster. Adjusting your withholding so you break even at filing time keeps that money in your paycheck instead.

Can I get a streamlined installment agreement if I have unfiled tax returns?

No — filing compliance comes first. The IRS won't approve any installment agreement while required returns are missing, and an unfiled year discovered later can default an existing plan. File the missing returns (the IRS generally looks for the last six years), let the balances post, and then apply based on the true combined total.

Your next 24 hours

- Find your total. Log in to your IRS online account (or add up the "amount you owe" box on your most recent notice for every year) and confirm the combined figure is at or under $50,000 — then note the date printed on any LT11 or CP504 in the stack.

- Gather three things: your most recent filed return, every IRS notice you've received, and your bank routing and account numbers for the direct debit setup.

- Get a free case review. If a levy notice is in the pile, the 30-day hearing window is already counting down — call (888) 825-7779 or use the 2-minute form and an experienced tax professional will map whether streamlined, partial-pay, or something better fits your numbers.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.