Tax Deadlines & Payments

Can't Pay Taxes by April 15? Your Exact 2026 Playbook

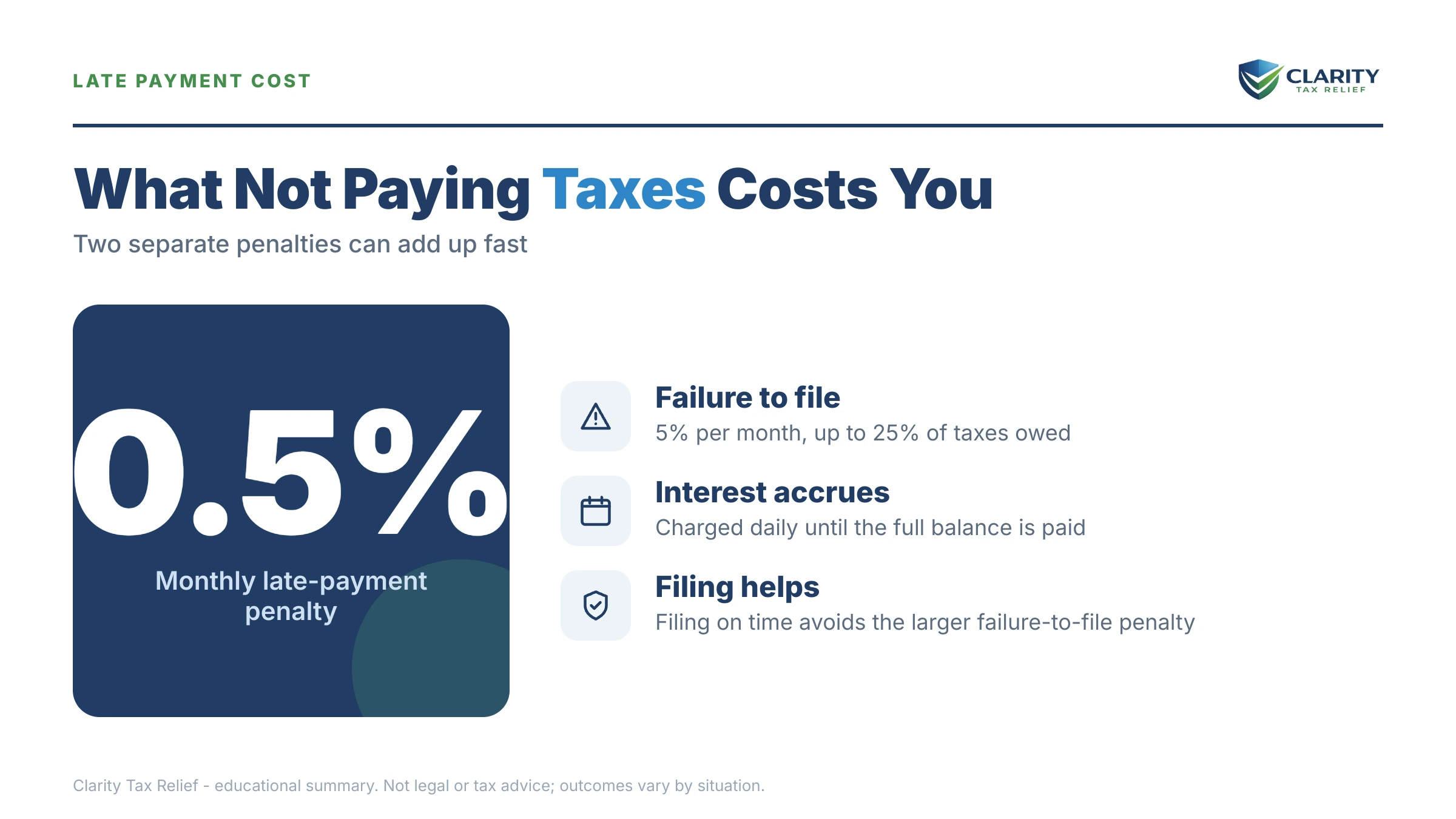

The short answer: if you can't pay taxes by April 15, file your return anyway and pay whatever you can. The failure-to-file penalty is 5% per month — ten times the 0.5% failure-to-pay penalty. Then set up an IRS payment plan: up to 180 days at no setup cost, or monthly for up to 72 months on balances under $50,000.

You finished the return, hit "calculate," and the software spit out a number your checking account can't touch — with the deadline days away. The instinct is to close the laptop and not file at all. That instinct is the single most expensive mistake you can make in April, and everything below exists to stop you from making it.

⏱ The real deadline: April 15, 2026 is both the filing deadline and the payment deadline. Interest and the 0.5% monthly failure-to-pay penalty start the next day on any unpaid balance — and if you don't file (or file Form 4868 for an extension) by April 15, the failure-to-file penalty adds 5% per month on top.

Why your April 15 balance is bigger than you can pay

Most surprise April 15 balances trace to withholding or estimates that stopped matching your life sometime during the year. The tax was always accruing — nobody was setting it aside.

The most common triggers: a divorce that changed your filing status while your W-4 stayed set for a joint return, a second job where each employer withheld as if it were your only income, 1099 or gig income with zero withholding, a retirement-account withdrawal, or capital gains from selling investments or a house.

Two of those deserve their own guides: if a retirement distribution caused the bill, see 401k withdrawal tax bill can't pay; if a layoff drained the savings you'd earmarked for taxes, see lost my job can't pay IRS.

Whatever the cause, the diagnosis matters for exactly one reason: fixing it (step 4 below) is what keeps you from standing in this same spot next April.

File anyway — the 10× mistake most people make

Filing without paying costs 0.5% of the balance per month; not filing at all costs 5% per month — ten times more, and both penalties cap at 25% of the unpaid tax. The IRS charges these separately from interest, which compounds daily on top.

Read that again, because it's the whole game in April: the IRS punishes silence far harder than it punishes empty pockets. A return filed on time with $0 attached protects you from the worst penalty on the books. The full math is in should I file if I can't pay, and you can estimate your own penalty and interest with our Penalty & Interest Calculator.

One more myth to kill: an extension is not extra time to pay. Form 4868 moves your filing deadline to October 15 — the money is still due April 15, and the failure-to-pay penalty and interest run regardless. An extension only helps if your return genuinely isn't ready, and it works best when you send an estimated payment with it. The details are in does an extension give more time to pay — and if you already extended and October is now the problem, see October 15 tax deadline can't pay.

What happens if you don't pay taxes by April 15

Nothing dramatic happens on April 16 — no agent calls, no account freezes — but interest and the failure-to-pay penalty start that day, and the IRS's automated notice sequence begins queuing behind them. The sequence runs in a fixed order, and each stage carries more enforcement power than the last:

- April 16 — interest (compounding daily) and the 0.5% monthly failure-to-pay penalty begin. No enforcement, just accrual.

- CP14 — the first bill, typically mailed within weeks of your return processing. You get roughly 21 days to pay or arrange before the reminders queue. If you're already holding one, go straight to got a CP14 and can't pay.

- CP501 / CP503 — reminder notices. Still just bills, but every month adds another penalty charge and another month of interest.

- CP504 — Notice of Intent to Levy under IRC §6331(d). The IRS can now seize your state tax refund, and a federal tax lien becomes a live possibility.

- LT11 / Letter 1058 — the final notice. It starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). After those 30 days, the IRS can garnish wages and levy bank accounts — bank levies come with a 21-day hold before the money leaves.

In 2026 this sequence is more automated than ever. The IRS workforce shrank roughly 27% in 2025, so reaching a human is harder — but the notice-and-levy machinery is software, and it never stopped running. Waiting for the IRS to "get around to you" is not a strategy; the computer already has.

Staring at a balance you can't pay this April?

Get it reviewed free before another month of penalties and interest posts. An experienced tax professional will match your numbers to the right IRS program — no pressure, no obligation.

Your options when you can't pay taxes by April 15

The IRS offers four real alternatives to paying in full on April 15: a 180-day short-term plan, a monthly installment agreement, hardship status, and — for the minority whose finances qualify — an Offer in Compromise. Penalty relief can shrink the balance under any of them. The broader self-help playbook lives in our guide to how to settle tax debt yourself; here's how each option applies to a fresh April 15 balance:

| Option | Who may qualify | Cost to set up | Key detail |

|---|---|---|---|

| Pay in full (Direct Pay) | Anyone with the funds | $0 | Stops penalties and interest immediately |

| Short-term payment plan | You can clear the balance within 180 days | $0 setup fee | Penalties and interest continue, but enforcement stops |

| Guaranteed installment agreement | You owe $10,000 or less in tax and meet compliance conditions | Setup fee (lowest online with direct debit) | The IRS must accept it if the conditions are met |

| Streamlined installment agreement | Balance ≤ $25,000 (≤ $50,000 with direct debit) | Setup fee (reduced or waived for low-income filers) | No full financial disclosure; up to 72 months online for balances ≤ $50,000 |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living costs (shown on Form 433-F) | $0 | Collection pauses; the debt and accruals remain while the 10-year CSED runs |

| Offer in Compromise (Form 656) | Your assets and future income genuinely can't cover the debt | $205 fee + 20% down for lump-sum offers (both waived with low-income certification, AGI ≤ 250% of poverty) | The IRS accepted roughly 1 in 5 offers in FY2024 — real, but means-tested |

| Penalty relief (FTA / AEP) | Clean compliance in the prior 3 years; AEP becomes automatic starting summer 2026 | $0 | Removes penalties, not the tax itself |

A few notes the table can't hold. The streamlined installment agreement is the workhorse for April 15 balances — most people under $50,000 can set one up online without ever mailing a financial statement. Currently Not Collectible is the right call only when your budget genuinely has nothing left after necessities; how the IRS tests that is covered in IRS Currently Not Collectible.

On penalties: if this is your first slip after three clean years, first-time penalty abatement can erase the failure-to-pay penalty on request — and starting summer 2026, the new Automatic Exemption from Penalty (AEP) applies similar relief automatically, no request needed. Don't pay penalties you may not have to.

And ignore anyone promising to settle your fresh April balance for "pennies on the dollar" — that pitch is a scam signal, not a program. An Offer in Compromise exists, but the IRS runs the math on your assets and income, not on what a salesperson promises.

Say you owe $23,800: the math on every path

Here's a hypothetical that matches how these bills usually happen. Say you finalized a divorce last spring, but your W-4 stayed set for a joint return all year. Filing single for the first time, you owe $23,800 — and there's no joint savings account to pull from anymore. Your paths:

- Don't file at all: the failure-to-file penalty runs about 5% × $23,800 = $1,190 per month, up to the 25% cap of $5,950 — plus interest. This is the only truly catastrophic choice on the list.

- File on time, pay nothing: the failure-to-pay penalty is 0.5% × $23,800 = about $119 per month plus interest. Filing alone saves you roughly $1,071 a month in penalties versus not filing.

- Short-term plan: $23,800 ÷ 6 months ≈ $3,967/month. Realistic only if a bonus, tax refund from your state, or asset sale is coming.

- Streamlined installment agreement: at $23,800 you're under the $25,000 threshold, so no full financial disclosure is required. Spread across 72 months, the balance alone is about $331/month; the IRS sets the actual payment somewhat higher so accruing interest and penalties retire within the term. Once the agreement is approved, the failure-to-pay penalty drops to 0.25% per month — roughly $60 at the start, shrinking as you pay down.

One more divorce-specific trap: if part of your balance comes from a prior joint year, the IRS can collect all of it from either of you no matter what the decree says. That fight has its own playbook — see divorce and IRS debt: who pays.

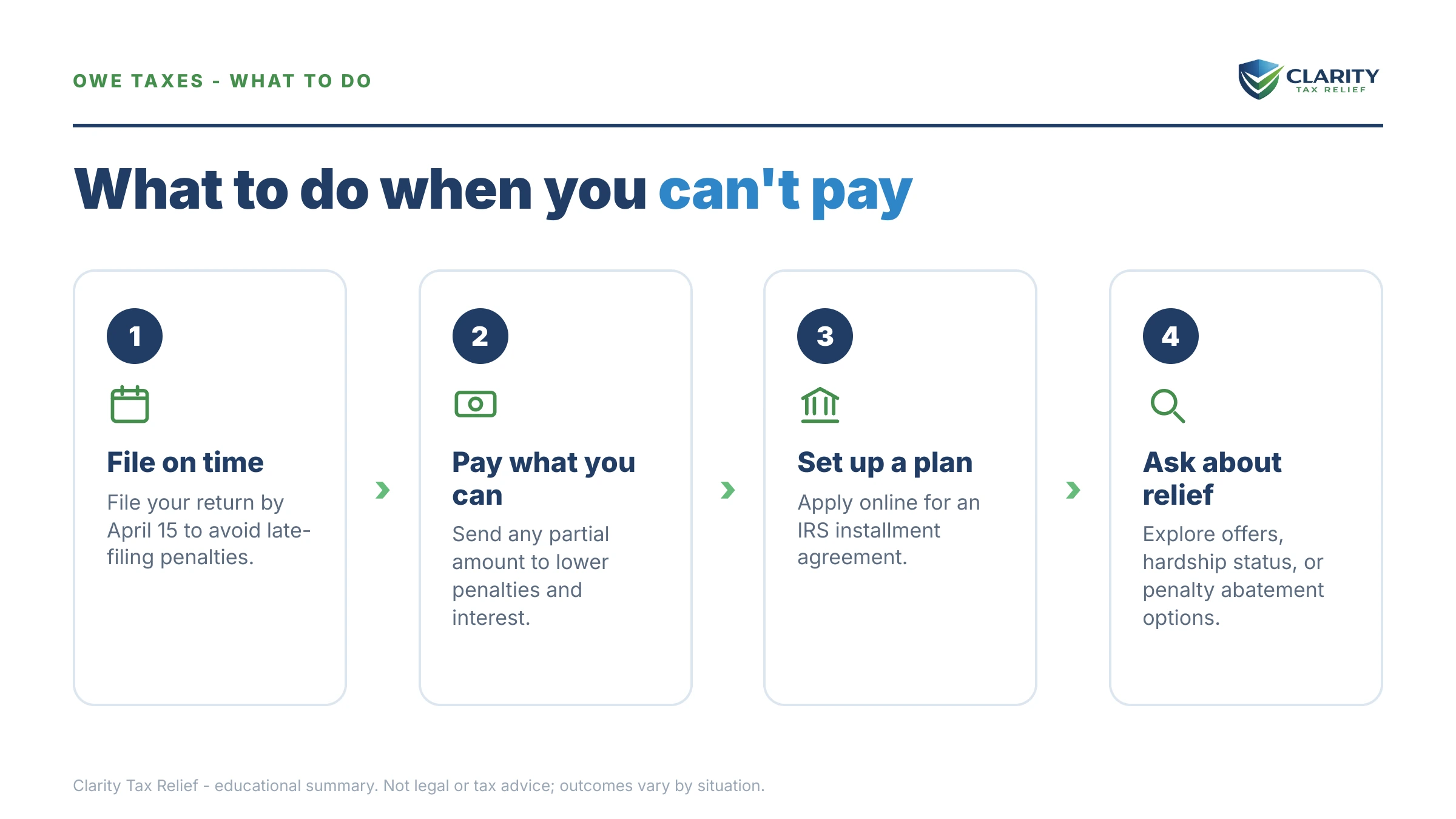

How to respond when you can't pay by April 15, step by step

- File your return by April 15. E-file or postmark it on time even with zero payment attached. This single step avoids the 5%-per-month failure-to-file penalty.

- Pay whatever you can now. Send any amount through IRS Direct Pay — penalties and interest are calculated only on what remains unpaid.

- Choose and apply for a payment option. Use the IRS Online Payment Agreement for a 180-day plan or a monthly installment agreement, or mail Form 9465 with your return; balances that don't fit the streamlined thresholds also need Form 433-F. Our walkthrough: how to set up an IRS payment plan online.

- Fix the cause before next April. Update your W-4 withholding after a divorce or job change, or start quarterly estimated payments if you have 1099 income.

- Watch the mail and keep the agreement current. A CP14 bill will still arrive for any unpaid balance; confirm it matches your records, and never miss a monthly payment once your plan is active.

What your transcript shows after you file with a balance

Within weeks of filing an unpaid return, your IRS account transcript documents the debt in a predictable set of codes. Checking your transcript (free through your IRS online account) is how you confirm the balance the IRS actually has on file — before the CP14 even arrives:

| Code | What it means | What to do |

|---|---|---|

| 150 | Return filed and tax assessed — the balance is now official | Confirm the amount matches the return you filed |

| 806 | Withholding and estimated payments credited to the year | Verify every payment you made actually appears |

| 276 | Failure-to-pay penalty charged for the month — see code 276 transcript | Expect one each month until you pay or get on a plan |

| 196 | Interest assessed on the unpaid balance | It compounds daily; only a $0 balance stops it |

| 971 | Notice issued — your CP14 is in the pipeline | Don't wait for the letter; set up your payment option now |

When you can handle this yourself — and when help changes the outcome

If you owe under $10,000, agree with the number, and can commit to a monthly payment, you can usually set this up yourself online in under 30 minutes. The guaranteed installment agreement exists for exactly this situation, and balances under $25,000 flow through the streamlined process almost as easily. One tax year, a number you trust, income to pay it down — do it yourself and keep your money.

Experienced help earns its cost when the situation has layers: multiple unfiled years behind this one (the order you file and resolve them changes what you pay), a balance tied to a joint return with an ex you dispute, self-employment income where quarterlies are already going wrong for the current year, a genuine hardship case that needs Form 433-F built correctly, or Offer in Compromise math you shouldn't guess at. If money is impossibly tight, the Taxpayer Advocate Service and Low Income Taxpayer Clinics offer free help for those who qualify.

Terms you'll run into, decoded

- Failure-to-file penalty: 5% of the unpaid tax per month for filing late, capped at 25% — the penalty filing on time eliminates.

- Failure-to-pay penalty: 0.5% of the unpaid tax per month (0.25% while an approved installment agreement is in effect), also capped at 25%.

- Form 4868: the automatic extension of time to file until October 15 — it does not extend the time to pay.

- Installment agreement: a formal monthly payment plan with the IRS; enforced collection stops while you stay current.

- CSED: the Collection Statute Expiration Date — the IRS generally has 10 years from assessment to collect, though certain actions pause that clock.

Can't-pay-by-April-15 questions, answered

What happens if I file my taxes but don't pay by April 15?

You'll owe the failure-to-pay penalty of 0.5% of the unpaid balance per month plus daily-compounding interest, and the IRS will mail a CP14 bill — usually within a few weeks of processing. No levy, lien, or garnishment happens at this stage. Filing on time protects you from the far larger 5%-per-month failure-to-file penalty, which is why filing without payment is always the right move.

Should I file an extension if I can't pay my taxes?

Only if your return isn't finished. Form 4868 extends your filing deadline to October 15, but payment is still due April 15 — the failure-to-pay penalty and interest run either way. If your return is done and you simply lack the money, filing it now costs nothing extra and opens your payment-plan options immediately. An extension helps most when you also send an estimated payment with it.

Is there a penalty for paying late if I'm on an IRS payment plan?

Yes, but a smaller one. Once an installment agreement is approved, the failure-to-pay penalty drops from 0.5% to 0.25% per month, and enforced collection stops as long as you keep the terms. Interest continues at the IRS's quarterly rate until the balance is gone, so paying more than the minimum whenever you can shortens the total cost.

Can I pay my taxes by April 15 with a credit card?

You can — the IRS accepts cards through approved third-party processors that charge a processing fee. Whether it's smart depends on your card's rate: IRS interest plus the reduced 0.25% payment-plan penalty is often cheaper than typical credit-card APRs. A card makes the most sense for a small balance you'll clear within a promotional 0% window; for larger balances, an installment agreement usually costs less.

How much should I pay with my return if I can't pay the full amount?

Every dollar you can spare. Both the failure-to-pay penalty and interest are calculated only on the unpaid balance, so a $5,000 payment against a $23,800 bill cuts every future month's charges by about 21%. Paying something can also drop your balance under key thresholds — below $25,000, you may qualify for a streamlined installment agreement without submitting full financial disclosure.

Will the IRS garnish my wages right after April 15?

No. Wage garnishment can't legally start until the IRS sends a final notice of intent to levy (LT11 or Letter 1058) and 30 more days pass — and that notice comes only after a series of earlier bills, starting with the CP14. In practice you have months of warning. The mistake is using that runway to do nothing while the balance grows every month.

Am I responsible for the balance if it comes from a joint return with my ex?

If the return was filed jointly, the IRS can collect the entire balance from either spouse — that's joint and several liability, and a divorce decree assigning the debt to your ex doesn't bind the IRS. Your options include innocent spouse relief if your ex understated income without your knowledge, or resolving the balance with the IRS and enforcing the decree against your ex in state court.

Your next 24 hours

- Find your exact number. It's on the "Amount you owe" line of your Form 1040 — and once the return processes, in your IRS online account. Write it down; every option below keys off it.

- Gather three things: the return itself, your last two months of income records (pay stubs or 1099 deposits), and a rough monthly budget. That's everything a payment-plan decision needs.

- Get a free case review at the 2-minute form or (888) 825-7779. Every month you wait adds another failure-to-pay penalty charge and another month of daily interest to the balance — an experienced tax professional can match your numbers to the right program before the next one posts.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.