IRS Payment Plans

Non Streamlined Installment Agreement: Above the Streamlined Threshold (2025)

The short answer: a non streamlined installment agreement is a monthly IRS payment plan for people who owe more than the streamlined limit of about $50,000 — or who need longer than 72 months to pay. It usually requires a full financial disclosure so the IRS can confirm what you can actually afford each month.

Owe more than $50,000 and not sure what to propose?

The monthly number you offer the IRS is the whole ballgame — too high and you can't keep it, too low and they reject it. An experienced tax professional can review your finances, run the math, and tell you what's realistic before you file anything. It's free, confidential, and there's no pressure.

⏱ Why timing matters: if a "Final Notice of Intent to Levy" (LT11 or Letter 1058) is already in your mail, you have 30 days to act before the IRS can garnish wages or levy a bank account. Setting up an installment agreement before that window closes generally stops enforcement. Penalties and interest keep adding up until the balance is paid.

What a non streamlined installment agreement is

The IRS sorts payment plans by how much you owe. If your total balance is at or under about $50,000, you usually qualify for a streamlined installment agreement — a simple monthly plan, up to 72 months, with no detailed financial review. A non streamlined installment agreement is what you fall into when you're above that threshold or you need more time than 72 months.

The difference isn't the monthly payment itself. It's the paperwork. Once you're above the streamlined line, the IRS wants to see your numbers before it agrees to a payment. That means a Collection Information Statement — and the figure you propose has to hold up against what the IRS thinks you can afford.

The financial disclosure you'll need to provide

For most non streamlined agreements, you file one of two forms:

- Form 433-F — the shorter Collection Information Statement, often used when you set up a plan over the phone or through automated collection.

- Form 433-A — the longer, more detailed version, often required when a revenue officer is assigned or the balance is large.

These forms list your monthly income, your living expenses, and your assets — bank accounts, vehicles, retirement, home equity. The IRS compares your expenses against its published Collection Financial Standards to decide which expenses it will allow. What's left over after allowed expenses is, in the IRS's view, what you can pay each month.

One important exception exists for individuals who owe between $50,000 and $250,000. The IRS may let you skip the full financial statement if you agree to pay by direct debit and the plan full-pays the balance within the time left on the collection statute — as long as your account hasn't been assigned to a revenue officer yet. This is sometimes the cleanest path for someone just over the streamlined line.

How long the plan can run

The IRS has a 10-year limit to collect a tax debt, called the Collection Statute Expiration Date, or CSED. Every payment plan lives inside that clock. (We break the clock down in our guide to how long the IRS can collect back taxes.)

A streamlined plan caps at 72 months. A non streamlined plan can run longer if there's enough time left on the statute — but it can never extend past your CSED. If the full balance can't be paid before the statute runs out, you're looking at a different solution, like a partial-pay agreement (more on that below).

A worked example

Say you owe $78,000 in back taxes. That's above the $50,000 streamlined line, so a non streamlined installment agreement applies. You file Form 433-F. After the IRS allows your housing, food, transportation, and other standard expenses, your statement shows $950 left over each month.

- At $950/month, the balance plus ongoing interest would take roughly 7–8 years to clear.

- Because your CSED is more than 8 years out, the plan fits inside the statute — so the IRS can approve it.

- If your CSED were only 5 years away, $950/month wouldn't full-pay in time. At that point you'd ask about a partial-payment installment agreement, where you pay what you can and the rest expires with the statute.

These numbers are an illustration, not a promise. Your allowed expenses and your CSED decide the real figure.

What happens if you ignore the balance

The IRS collection system is automated and unforgiving of delay. Above $50,000, the notices escalate the same way they do for smaller balances — but with a federal tax lien far more likely in the mix:

- CP14 — the first bill. No enforcement yet.

- CP501 / CP503 — reminder notices. The balance keeps growing with the 0.5%-per-month late-payment penalty plus interest.

- CP504 — Notice of Intent to Levy. The IRS can seize your state refund, and a Notice of Federal Tax Lien becomes likely on a balance this size.

- LT11 / Letter 1058 — Final Notice. After 30 days, the IRS can garnish wages and levy bank accounts. You also get formal appeal rights here.

Setting up a non streamlined installment agreement before this runs its course is what stops the machine. The plan you start today prevents the levy you'd otherwise face later.

How to set up a non streamlined installment agreement, step by step

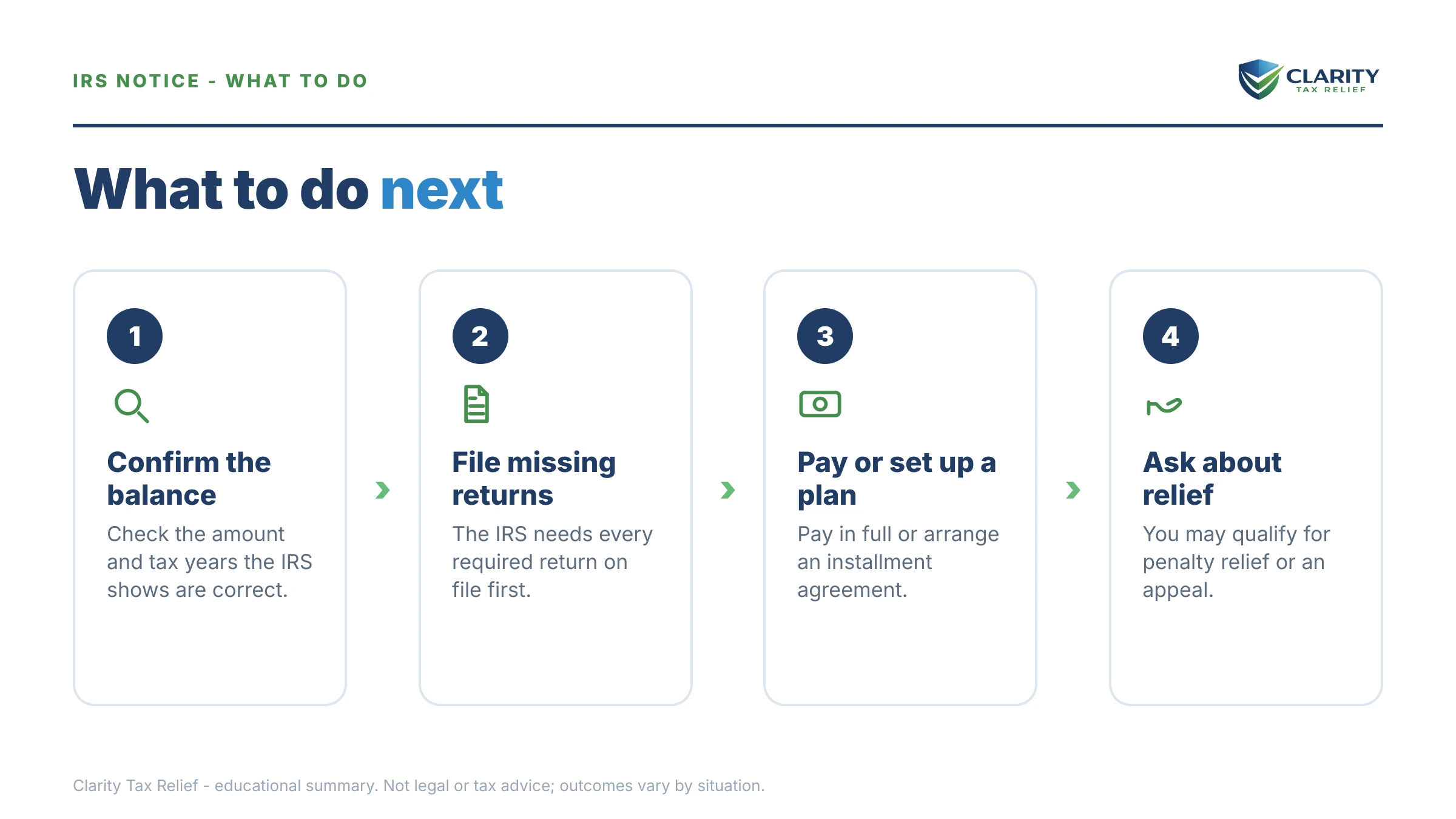

- File any missing returns first. The IRS won't approve a payment plan if you have unfiled years. All required returns must be in.

- Pull your transcripts and confirm the balance. Check your IRS online account so you're proposing a plan against the right number.

- Gather your financials. Income, monthly expenses, and assets for Form 433-F or 433-A — unless you qualify for the $50,000–$250,000 direct-debit exception.

- Apply. You can often start online through the IRS payment plans page, by phone, or by mailing Form 9465 with your financial statement.

- Choose direct debit if you can. Direct-debit plans cost less to set up, default less often, and can help you avoid a lien on balances at or under $25,000.

- Stay current going forward. A new balance or a missed payment can default the agreement. File and pay on time while the plan runs.

Non streamlined installment agreement questions, answered

What is a non streamlined installment agreement?

It's a monthly IRS payment plan for taxpayers who owe more than the streamlined limit of about $50,000, or who need longer than 72 months to pay. Unlike a streamlined plan, it usually requires a full financial disclosure so the IRS can confirm what you can afford.

Do I have to show my finances for a non streamlined installment agreement?

Usually yes. You file a Collection Information Statement — Form 433-F or 433-A — listing income, expenses, and assets. One exception: individuals who owe between $50,000 and $250,000 may avoid full disclosure if they agree to direct debit and can pay within the collection statute, before the account reaches a revenue officer.

How long can a non streamlined installment agreement last?

Long enough to full-pay the balance before the IRS's 10-year collection statute (the CSED) expires. Streamlined plans cap at 72 months; non streamlined plans can run longer if the time remaining on the statute allows it, but they cannot extend past the CSED.

Will the IRS file a lien if I owe more than $50,000?

Often yes. Above roughly $50,000 the IRS frequently files a Notice of Federal Tax Lien even when you're on a payment plan. Agreeing to direct debit can help you avoid a lien on balances at or under $25,000, but on larger balances a lien is common regardless of the plan.

What if I can't afford the monthly payment the IRS wants?

Tell them with numbers, not words. A complete financial statement may support a lower payment, a partial-pay installment agreement that ends when the statute does, Currently Not Collectible status, or — if your finances genuinely qualify — an Offer in Compromise. No outcome is guaranteed; eligibility depends on your facts.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.