IRS Payment Plans

Reinstate IRS Payment Plan: How to Restart After Default (2025)

The short answer: to reinstate an IRS payment plan after it defaults, log into the Online Payment Agreement tool at IRS.gov or call the number on your CP523 notice, bring any missed payments and unfiled returns current, and pay the reinstatement fee. Act within the notice window — usually about 30 days.

Defaulted and not sure how to restart?

Send us a photo of your CP523 or payment-plan notice. An experienced tax professional will tell you exactly how to reinstate, what it should cost, and whether better terms are within reach — free, confidential, no pressure.

⏱ Your deadline: if you received a CP523, you generally have about 30 days from the notice date to reinstate before the agreement is terminated and the IRS can levy. The faster you act, the cheaper and simpler it is — reinstating before termination is far easier than rebuilding from scratch.

Why your IRS payment plan defaulted

An installment agreement is a deal: you make every monthly payment on time, file every return on time, and pay any new balance in full. Break any one of those promises and the IRS can declare the agreement in default. The most common triggers are simple:

- You missed a monthly payment, or a direct-debit payment bounced.

- You filed this year's return late — or didn't file it at all.

- You owe a new balance for the current tax year and didn't pay it.

- You gave the IRS updated financial information and the numbers no longer support your terms.

Most people find out through a CP523 notice — "Intent to Terminate Your Installment Agreement." It's automated and it doesn't care why you missed. The good news: a CP523 is a warning, not the end. You still have a clear path to reinstate. For a full walkthrough of that notice, see our CP523 notice guide, and for the bigger picture read what to do when your payment plan defaulted.

What happens if you ignore it

Reinstating is easy now and hard later. The IRS collection machine runs on a schedule, and a defaulted agreement removes the protection that kept levies off the table:

- CP523 — Intent to Terminate. You are here. The agreement is still alive, and you have a short window to reinstate.

- Termination — about 30 days later, if you do nothing, the agreement officially ends. Levy protection is gone.

- Enforcement — the IRS can levy your bank account (after a 21-day hold) or garnish your wages, and a federal tax lien may already be on file.

- Higher cost to restart — once terminated, reinstatement may require new financial disclosure and a fresh review, on top of all the interest and penalties that kept growing the whole time.

The lesson isn't that the IRS is out to get you — it's that the system is automated and unforgiving of delay. A phone call this week beats a levy next month.

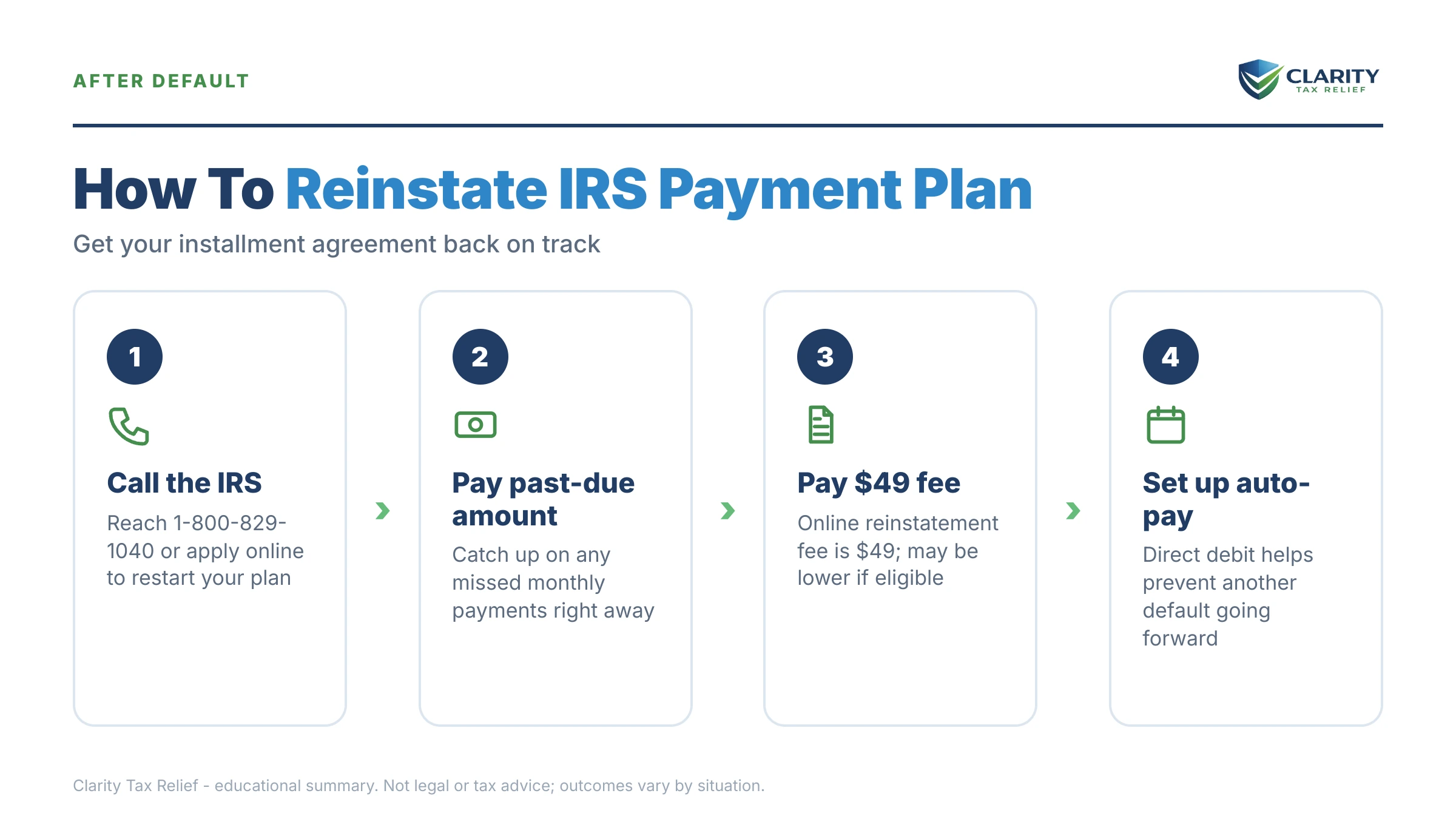

How to reinstate your IRS payment plan, step by step

There is no single magic "reinstatement form." How you restart depends on whether your situation has changed. Here's the process:

- Fix the underlying problem first. If a return is unfiled, file it. If you owe a new year, plan to roll it into the agreement. The IRS will not reinstate a plan while you're still out of compliance.

- Try the Online Payment Agreement tool. Log into your IRS Online Payment Agreement application. If you qualify, you can reinstate or revise the plan there — and the reinstatement fee is lower online than by phone.

- If the same monthly payment still works, bring any missed payments current and reinstate at the original terms. Switching to direct debit lowers your fee and prevents future missed-payment defaults.

- If you can no longer afford the old payment, request new terms. You may file Form 9465 (Installment Agreement Request) and, for many cases, a Form 433-F collection information statement showing your income and expenses. See our guide to lowering your IRS monthly payment.

- Pay the reinstatement fee. The IRS charges a fee to restart a defaulted agreement. It's reduced for online setup and direct debit, and low-income taxpayers may qualify for a reduced fee or reimbursement. Check the current amounts on the IRS payment plans page.

- If the window has closed or a levy is coming, call the number on your CP523 right away. Contacting the IRS to reinstate or appeal generally pauses enforcement while your request is reviewed.

A worked example: what reinstatement looks like

Say you owe $18,000 and were paying $300 a month by direct debit. Your bank account ran short one month, the debit bounced, and a few weeks later a CP523 arrived. You're not behind on filing — you just missed one payment.

Here, reinstatement is straightforward. You log into the Online Payment Agreement tool, bring the one missed payment current, confirm your direct-debit details, and pay the reduced online reinstatement fee. Because your income hasn't changed, you keep the $300 monthly payment and the plan is back on track — usually without any new financial disclosure. Total time: an afternoon. That's why acting inside the 30-day window matters so much.

You also have options beyond just restarting

Reinstating the same plan is the fastest fix, but it isn't your only choice — especially if money got tighter:

- Lower monthly payment — if your income dropped, new terms based on Form 433-F may give you a payment you can actually keep.

- Currently Not Collectible status — if paying anything would cause real hardship, the IRS can pause collection entirely. Read about Currently Not Collectible status.

- Offer in Compromise — settling for less than the full balance is real, but only when your assets and income genuinely can't cover the debt. Anyone promising to settle for "pennies on the dollar" before reviewing your finances is selling you something, not telling you the truth.

- Penalty relief — first-time abatement or reasonable cause may erase some of the penalties that piled up while the plan was in default.

Reinstating an IRS payment plan: your questions, answered

Is there a form to reinstate an IRS payment plan?

There's no single dedicated reinstatement form. Most people reinstate through the Online Payment Agreement tool at IRS.gov or by calling the number on their CP523 notice. If your finances changed and you need a lower monthly amount, you may file Form 9465 or submit a Form 433-F collection information statement to set new terms.

How much does it cost to reinstate a defaulted installment agreement?

The IRS charges a reinstatement fee to restart a defaulted installment agreement. The fee is lower when you reinstate online and lower still for direct debit, and low-income taxpayers may qualify for a reduced fee or a reimbursement. Check the current amount on the IRS payment plans page before you apply.

How long do I have to reinstate after a CP523 notice?

A CP523 gives you a limited window — generally about 30 days from the notice date — before the agreement is officially terminated and the IRS can move to levy. Acting within that window is the easiest, cheapest way to reinstate. You can still request reinstatement after termination, but your options narrow quickly.

Can the IRS levy me while I'm trying to reinstate?

Once an agreement defaults, levy protection ends. During the CP523 window the IRS usually holds enforcement, and contacting them to reinstate or appeal generally pauses levy action while it's reviewed. The danger is silence — ignore the notice and the automated system can move to garnish wages or levy a bank account.

Why did my IRS payment plan default in the first place?

The most common reasons are a missed monthly payment, a bounced direct-debit payment, filing a new return late, or owing a new balance for the current year without paying it. Even one of these can trip the agreement. When you reinstate, you usually have to fix the underlying problem too, such as filing any missing return.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.