IRS Payment Plans

Pay Off IRS Payment Plan Early: Interest Savings and How to Do It (2025)

The short answer: you can pay off an IRS payment plan early with no penalty. The IRS charges no prepayment fee on an installment agreement, and interest compounds daily — so every month you cut off the plan saves you money. Just pay the current payoff balance through your IRS online account.

Not sure if paying early is your best move?

Sometimes penalty relief or a different program saves you more than prepaying. An experienced tax professional can review your account and tell you the smartest order to handle it — free, confidential, no pressure.

⏱ Worth knowing: interest is added to your balance every single day you carry it. There's no deadline to pay off early — but the sooner you do, the less you pay. Always use the payoff amount shown in your account, not last month's balance, because it changes daily.

Can you pay off an IRS payment plan early?

Yes. You can pay off an IRS payment plan early any time you want, and there is no prepayment penalty for doing it. An IRS installment agreement is not like a car loan with a payoff fee buried in the fine print. You can send more than your required monthly amount, make extra one-time payments, or wipe out the whole balance in a single payment — all without asking permission.

The reason to do it is simple: money. As long as you owe a balance, the IRS keeps charging interest and a monthly late-payment penalty. Paying early stops that clock.

Why paying early saves you money

Two charges keep growing on your balance while you're on a plan:

- Interest — set quarterly by the IRS (the federal short-term rate plus 3%) and compounded daily. You can see the current figure on the IRS quarterly interest rates page. We explain how this daily compounding actually adds up in our guide to how IRS interest compounds.

- Failure-to-pay penalty — normally 0.5% of the unpaid tax per month, but it drops to 0.25% per month while you have an active installment agreement. It still adds up the longer the balance lives.

Both charges are calculated on the balance you still owe. Knock that balance down faster, and there's less left for interest and penalty to feed on. That's the whole game.

A real-dollar example

Say you owe $12,000 in tax and you're on a 72-month streamlined plan paying about $185 a month. Imagine the combined interest-and-penalty cost runs roughly 0.8% to 0.9% of the remaining balance each month early in the plan.

- Stretch it the full 72 months and you'll pay interest and the 0.25% penalty on a slowly shrinking balance the entire time — adding up to well over a thousand dollars in charges before it's gone.

- Pay it off 12 months early by sending a lump sum or doubling up payments, and you erase a full year of those daily interest charges and monthly penalties on the still-large balance — easily several hundred dollars saved.

The exact number depends on the current interest rate and your balance, but the rule never changes: every month you remove from the back end of the plan saves real money, because that's when interest has had the most time to compound.

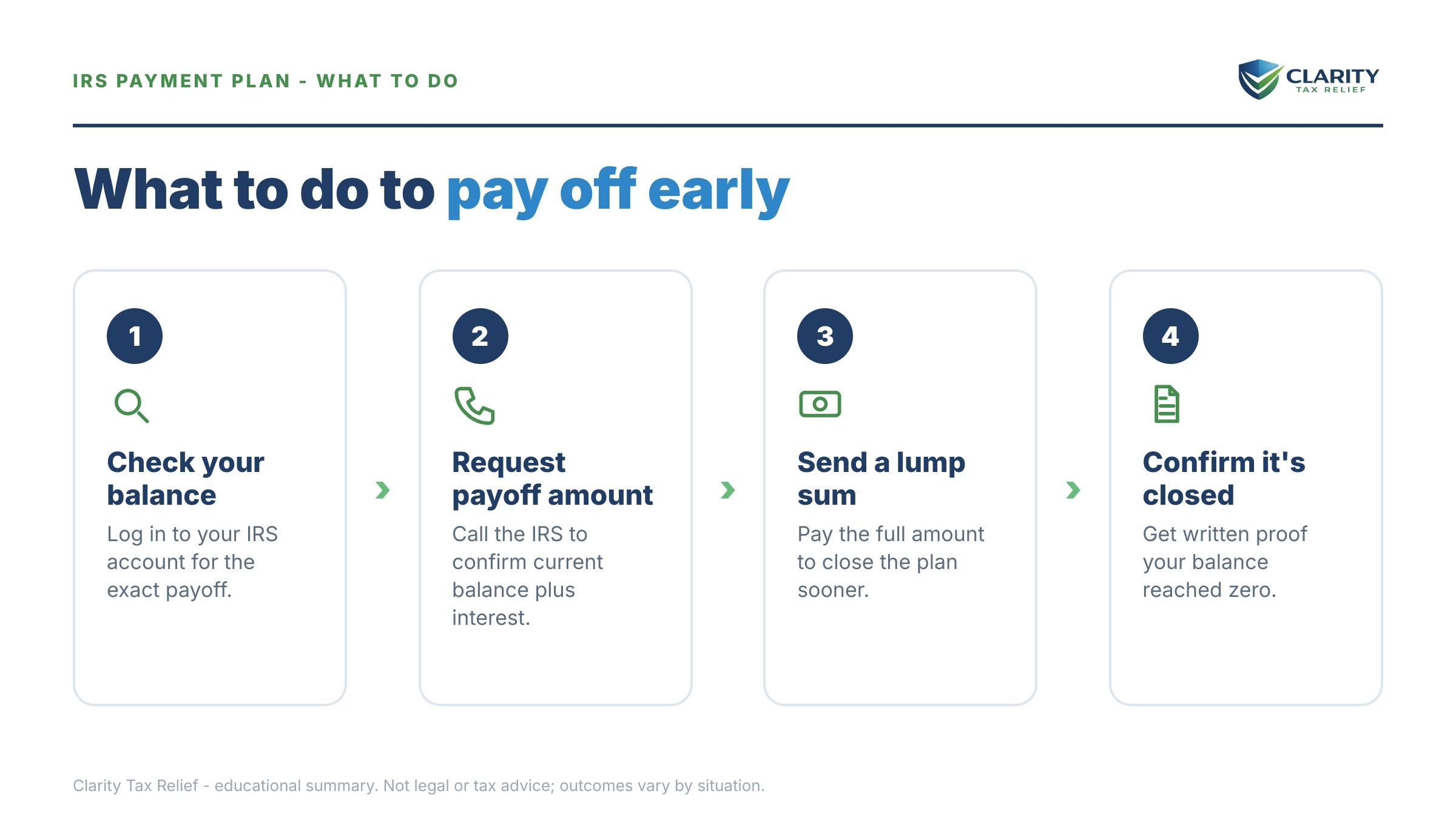

How to pay off your IRS payment plan early, step by step

- Get your real payoff amount. Log into your IRS online account and look at the current balance, including accrued interest and penalty. This number is higher than your principal and changes daily — use it, not an old statement.

- Choose how to pay. The cheapest, fastest options are IRS Direct Pay (free from a bank account), a payment inside your online account, or EFTPS. Card payments work but carry processor fees. Our breakdown of the best ways to pay the IRS compares them side by side.

- Make the payment. Apply it to the correct tax year. If you owe for more than one year, the IRS generally applies extra payments to the oldest balance first unless you direct otherwise.

- If you have a direct-debit plan, expect one more draft. Automatic monthly debits keep running until the balance hits zero. If you pay a lump sum between scheduled drafts, one more debit may still process before the system updates. See our guide to the direct-debit installment agreement for how the timing works.

- Confirm it's zero. A few days later, check your online account again to make sure the balance reads $0 and the agreement is closed. Save your payment confirmation.

Before you pay it off: two smart checks

Paying early is usually a clean win, but two things are worth a quick look first:

- Penalty relief. If this is your first balance in years, first-time penalty abatement may remove the failure-to-pay penalty entirely. It's often easier to request before the account closes, so the credit applies cleanly. Reasonable-cause relief may also apply if illness, disaster, or another event beyond your control caused the late payment.

- Your emergency fund. The IRS charges interest, but draining every dollar of savings to pay a low-cost balance can backfire if a real emergency hits. Paying off early is a good idea when you have a cushion left over — not when it leaves you exposed.

What happens after you pay it off

Once the balance reads zero, the agreement closes on its own. There's no closing form to file and no exit fee. Two things to keep in mind:

- If the IRS filed a federal tax lien against you, it should release the lien within 30 days of full payment. If it doesn't, you can follow up — our guide on getting a lien released after payment walks through the steps.

- Keep your records. Hold onto the final payment confirmation and a screenshot of the zero balance. If a stray notice shows up later, that proof settles it fast.

If you're just setting up a plan or thinking about one, our walkthrough on how to set up an IRS payment plan online covers the whole process from the start.

Pay off IRS payment plan early — FAQ

Is there a penalty for paying off an IRS payment plan early?

No. The IRS charges no prepayment penalty on an installment agreement. You can pay more than your monthly amount, make extra payments, or pay the whole balance off in one shot at any time. Paying early simply stops interest and the late-payment penalty from growing.

How much interest do I save by paying off my IRS plan early?

It depends on your balance and how many months you cut off the plan. IRS interest compounds daily, and a reduced 0.25% monthly late-payment penalty also runs while you're on the plan. On a $12,000 balance, paying off a year early can save several hundred dollars in combined interest and penalty — every month you remove saves real money.

How do I pay off my IRS installment agreement in full?

Check your current payoff amount in your IRS online account, then pay it through IRS Direct Pay, your online account, or EFTPS. Use the payoff figure, not your old balance, because interest is added daily. If you have a direct-debit plan, the monthly drafts continue until the balance hits zero, so a final lump-sum payment closes it out.

Will my direct-debit payments stop automatically after I pay off the balance?

Yes. Once the balance is fully paid, the IRS stops the automatic monthly drafts and the agreement closes. If you make a lump-sum payoff between scheduled drafts, one more debit may still process before the system catches up — check your online account a few days later to confirm the balance is zero.

Do I need to do anything after I pay off my payment plan?

Confirm the balance shows zero in your IRS online account and keep your payment confirmation. If the IRS filed a federal tax lien, it should release the lien within 30 days of full payment — if it doesn't, you can follow up. Otherwise, you're done; there's no closing form to file.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.