Penalties & Interest

IRS Interest Rate on Back Taxes 2026: How Daily Compounding Grows Your Balance

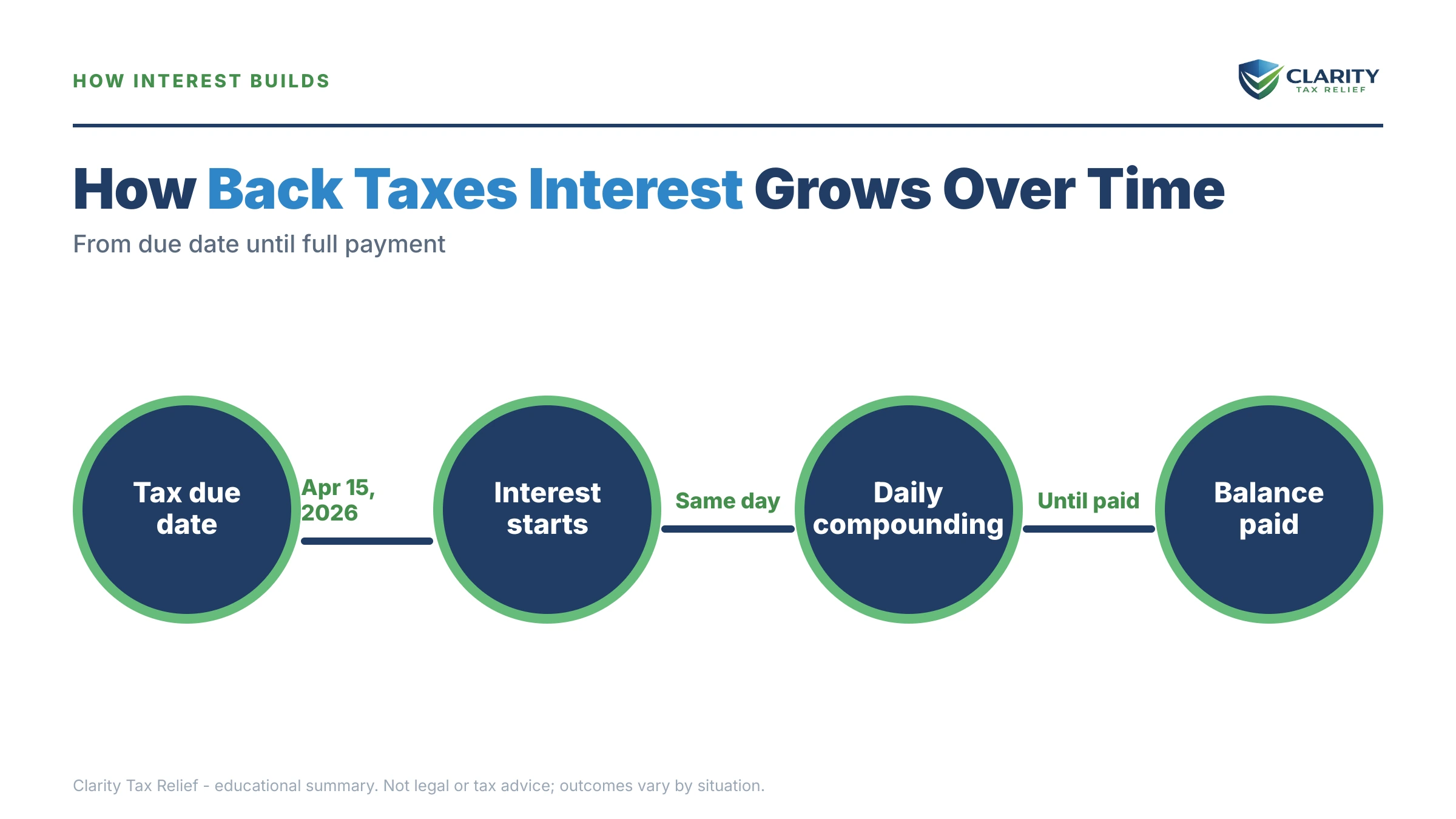

The short answer: the IRS interest rate on back taxes 2026 charges is the federal short-term rate plus 3 percentage points — 7% per year for individuals as of the latest quarterly reset — compounded daily. Interest starts the day after your original due date and runs until the balance hits zero, on top of monthly penalties.

You pulled your IRS balance to get a payoff figure for the refinance file, and the number staring back is thousands more than the tax you actually missed. That gap isn't a mistake — it's daily-compounded interest plus penalties, and it grew while you weren't looking. The upside: the growth is completely predictable, and most of it can be stopped this week. Here's the full math.

⏱ The real clock: interest has no response deadline — the meter simply runs. At 2026's 7% rate, a $19,700 balance grows by about $3.78 in interest every single day, before penalties. It stops only on the day the balance reaches zero.

What is the IRS interest rate on back taxes in 2026?

The IRS interest rate on back taxes in 2026 is the federal short-term rate plus 3 percentage points — 7% per year for individuals — compounded daily. The formula comes from Internal Revenue Code Section 6621, and the IRS has no discretion over it: no agent, appeals officer, or resolution company can negotiate the rate down.

The rate resets every quarter. The IRS looks at the federal short-term rate, adds 3 points, rounds, and announces the result in a revenue ruling before each quarter begins. When the Federal Reserve moves rates, the IRS underpayment rate follows a quarter or two behind — which is why it climbed from 3% in 2021 to 8% in 2024 before easing back to 7%. For the quarter-by-quarter numbers and where the rate is likely headed next, see our IRS interest rates 2026 quarterly tracker, and confirm the current figure before you run payoff math for anything time-sensitive like a closing.

Two more things the formula tells you. First, interest is retroactive to the original due date of the return — generally April 15 of the year it was due — even if you filed on extension. An extension moves the filing deadline, never the payment clock. Second, the same rate applies to every year you owe, but each year's meter started on its own due date, so a 2021 balance carries several more years of accrual than a 2024 one.

Why your balance is so much bigger than the tax you owed

Interest is only about half of what a back-tax balance actually costs — the failure-to-pay penalty adds another 0.5% per month on top, and interest then compounds on the penalties too. Three separate meters can run on the same balance at once:

| Charge | 2026 rate | How it accrues |

|---|---|---|

| Underpayment interest | Short-term rate + 3% (currently 7%) | Compounds daily from the original due date until paid — charged on the tax and on penalties |

| Failure-to-pay penalty | 0.5% per month (0.25% on an approved payment plan; 1% after a final levy notice) | Monthly, capped at 25% of the unpaid tax |

| Failure-to-file penalty | 5% per month | Monthly, capped at 25% — ten times the pay penalty, so file even when you can't pay |

| Interest on penalties | Same 7%, compounded daily | Runs from the return due date on filing penalties, from assessment on most others |

Notice the asymmetry in that table: not filing costs ten times more per month than not paying. If any return is still unfiled, that penalty is the fire to put out first — the full comparison is in our guide to the failure to file penalty vs failure to pay penalty. To see all three meters applied to your own numbers, our Penalty & Interest Calculator estimates what a balance has grown to and what it will grow to next.

Daily compounding: the math the IRS actually uses

IRS interest compounds daily under IRC Section 6622, which turns a stated 7% rate into an effective annual cost of roughly 7.25%. Every night, one day's interest — the balance times 0.07 divided by 365 — is added to what you owe, and tomorrow's interest is computed on that slightly bigger number.

Daily compounding is why two intuitions fail people. First, "it's only 7%" understates the true cost, because the penalty meters run alongside it: an unresolved balance grows at roughly 13% per year all-in (7% interest plus 6% per year of failure-to-pay penalty). Second, "I'll deal with it after the refinance closes" gets the order backwards — the balance you'd pay off in six months is meaningfully larger than the one you could resolve today, and waiting risks a lien filing that can stall the closing itself.

One quirk worth knowing: interest is one of the few IRS charges with no cap. Penalties max out at 25% of the tax. Interest never maxes out — it runs until the balance is paid or until the 10-year collection statute (the CSED) extinguishes the debt.

What $19,700 in back taxes really costs at 2026 rates

A $19,700 back-tax balance grows by roughly $212 in its first month at 2026 rates — about $114 of daily-compounded interest plus $98.50 of failure-to-pay penalty. Say you're that homeowner: you owe $19,700 from an under-withheld year, you're planning a refinance, and you're deciding whether to deal with the IRS before or after closing. Here's the cost of waiting (all figures approximate and hypothetical):

| If you wait | Interest added (≈7%, daily) | Failure-to-pay added (0.5%/mo) | Approximate balance |

|---|---|---|---|

| Today | — | — | $19,700 |

| 6 months | ~$715 | ~$591 | ~$21,000 |

| 12 months | ~$1,470 | ~$1,182 | ~$22,350 |

| 24 months | ~$3,090 | ~$2,364 | ~$25,150 |

| 36 months | ~$4,870 | ~$3,546 | ~$28,100 |

Now the plan math. Put that $19,700 on a 72-month direct-debit installment agreement and the failure-to-pay penalty drops to 0.25% per month, making the combined carrying cost roughly 10% per year — a payment of about $365 a month and roughly $26,300 paid in total. Pay the same balance off in 24 months instead — about $909 a month — and the total falls to roughly $21,800. Stretching the same debt from 24 to 72 months costs about $4,500 more, which is why paying off an IRS payment plan early is one of the few no-downside moves in tax resolution.

For the refinancing reader there's a third comparison: cash-out proceeds at a typical mortgage rate almost always cost less per year than carrying an IRS balance at 10–13%. The catch is timing. If the IRS files a Notice of Federal Tax Lien before you close, underwriting gets complicated — you may still be able to close using tax lien subordination (Form 14134), but it adds weeks. Our guide to refinancing with an IRS lien walks through both paths. Resolving or paying the balance before a lien hits is the clean version of this story.

What happens if you ignore the interest

Left alone, a back-tax balance grows at roughly 13% per year while the IRS's automated collection sequence escalates around it. Interest is the quiet damage; the notice stream is the loud damage. The stages run in a fixed order:

- CP14 — the first bill. You get about 21 days to pay or arrange payment. Interest and the 0.5% monthly penalty are already running.

- CP501 / CP503 — reminders. Nothing new legally; the balance simply compounds between letters.

- CP504 — intent to levy your state refund. The IRS can seize your state tax refund, and a Notice of Federal Tax Lien becomes a live risk — the event that turns a refinance from routine into a workout.

- LT11 / Letter 1058 — final notice. A 30-day clock starts on your Collection Due Process rights. Ten days after this notice, the failure-to-pay penalty doubles to 1% per month, pushing the all-in growth rate toward 19% per year.

- Levy and lien enforcement. Wages, bank accounts, and state refunds are all reachable — and every dollar levied still gets applied to a balance that kept compounding the whole time.

Two thresholds are worth watching as the balance grows. Interest and penalties count toward the $66,000 passport-certification threshold for 2026, so a debt that started well below the line can cross it on accruals alone. And in 2026's understaffed IRS — the workforce shrank about 27% in 2025 — these notices are generated by automation that never got cut. The compounding and the escalation both run without a human touching your file.

Watching the balance grow while you plan a refinance?

Every month unresolved adds roughly $212 to a $19,700 balance — and a lien filing can stall your closing. Get your balance, payoff options, and lien exposure reviewed free by an experienced tax professional before the next accrual posts.

Your options in 2026 — and what each one does to the interest meter

Every IRS resolution option changes what you pay in accruals — some stop the meter, most only slow it. The general playbook for resolving a balance lives in our guide to how to settle tax debt yourself; what follows is specifically what each option does to interest and penalties:

| Option | Who qualifies in 2026 | Effect on interest & penalties |

|---|---|---|

| Pay in full (savings, refinance proceeds) | Anyone | Both meters stop the day payment posts — the only total shutoff |

| Short-term plan (up to 180 days) | Individuals; $0 setup fee | Interest and the 0.5% monthly penalty continue; enforcement pauses |

| Long-term installment agreement | Up to $50,000 online over as long as 72 months; guaranteed installment agreement under $10,000; streamlined under $25,000 (or $50,000 with direct debit) | Interest continues; failure-to-pay penalty drops to 0.25% per month |

| Currently Not Collectible | Documented hardship shown on a financial statement | Collection pauses, but interest and penalties keep accruing the entire time |

| Offer in Compromise | Assets plus future income genuinely below the balance; $205 fee (waived with low-income certification) | An accepted offer resolves tax, penalties, and interest; roughly 1 in 5 offers were accepted in FY2024 |

| Penalty abatement (FTA / AEP / reasonable cause) | Clean prior 3 years for first-time abatement; AEP applies automatically starting summer 2026 | Removes penalties plus the interest charged on them; underlying interest stays |

| Interest abatement (Section 6404, Form 843) | IRS error or unreasonable delay only | The only path that removes interest itself — narrow, but real when the IRS caused the delay |

Three of those rows deserve a closer look through the interest lens. First-time penalty abatement is the most underused: if your prior three years are clean, the failure-to-pay penalty can come off entirely — and every dollar of interest that accrued on that penalty comes off with it, automatically. Starting summer 2026 the new Automatic Exemption from Penalty (AEP) begins granting that relief without a request, so don't let anyone charge you for something the IRS may soon do on its own. And IRS interest abatement under Section 6404 is the one true interest-removal tool — it applies only where an IRS ministerial or managerial act caused the delay, but when it applies, it's filed on Form 843 and it works.

Bankruptcy is the outlier: a Chapter 13 and back taxes plan treats interest under different rules than IRS collection does, which occasionally makes it the cheaper path for large, older balances — a fact-specific call for an experienced tax professional or bankruptcy attorney.

Which options are realistic also depends on the size of the balance — and the balance itself tells you what the interest alone is costing you each month:

| You owe | Interest alone per month (≈7%) | Realistic 2026 paths |

|---|---|---|

| Under $10,000 | Up to ~$58 | Pay within 180 days, or a guaranteed installment agreement — minimal friction |

| $10,000–$25,000 | ~$58–$146 | Streamlined installment agreement; pair it with first-time abatement |

| $25,000–$50,000 | ~$146–$292 | Streamlined plan with direct debit up to 72 months; OIC only if the finances truly support it |

| $50,000–$100,000 | ~$292–$583 | Financial disclosure required; non-streamlined agreement; lien filing likely — plan around it |

| $100,000+ | $583+ | Revenue-officer handling probable; passport certification in play above $66,000 |

Whichever route fits, the mechanics start on the IRS's own payment plans and installment agreements page, and payments themselves go through IRS.gov/payments — never anywhere else.

How to respond to growing IRS interest, step by step

- Pull your exact payoff balance. Log into your IRS online account and open the balance details for each year you owe. The figure updates with accrued interest, and you can generate a payoff amount good through a specific date — the number a refinance underwriter will want to see.

- Verify the assessment dates. Check your account transcript for the date each tax, penalty, and interest charge was assessed. Interest that started from the wrong date, or that ran during a documented IRS delay, may be removable under Section 6404.

- Stop the penalty meter. Set up a payment plan or pay what you can today. An approved installment agreement cuts the failure-to-pay penalty in half, to 0.25% per month, and every dollar paid shrinks the base that interest compounds on.

- Request penalty relief. Ask for first-time abatement if your prior three years are clean, or file Form 843 for reasonable cause. Removing a penalty also removes the interest that accrued on that penalty.

- Choose full payoff or a plan — and run the numbers. Compare the roughly 10% to 13% combined annual cost of carrying an IRS balance against your alternatives, including refinance proceeds, and commit to the cheaper path this week.

If you end up on the phone with the IRS for any of these steps, our scripts for what to say when calling the IRS about back taxes will save you a second hold time.

Situations that change the interest math

The 7% rate is universal, but when interest starts, who owes it, and how fast it stacks all shift with your situation.

Married filing jointly

A joint return creates joint and several liability — the IRS can collect the full balance, interest included, from either spouse. Interest doesn't split in a divorce either; the decree binds the two of you, not the IRS.

Self-employed and 1099 earners

The estimated-tax underpayment penalty is computed using this same underpayment rate, applied quarter by quarter from each missed payment date. If quarterlies are your recurring leak, the estimated tax penalty rate 2026 guide shows how the charge is built and the exceptions that shrink it.

Businesses and LLCs

Most business underpayments accrue at the same short-term-plus-3% formula, but large corporate underpayments over $100,000 draw "hot interest" at 2 points higher after demand. Who actually owes the accruing balance depends on the entity — our guide to when an LLC owes IRS back taxes sorts pass-through liability from entity-level liability.

Multiple years owed

Each year's interest meter started on that year's original due date, so the oldest year is always the most inflated. You may designate voluntary payments to a specific year and type of tax; undesignated payments get applied however serves the government best, which is rarely how it serves you best.

Disputed amounts

Interest runs during an audit and during appeals — winning later doesn't refund the time. If you dispute an amount but want the meter stopped in case you lose, you can make a Section 6603 deposit against the disputed liability while the fight plays out.

Retired or on fixed income

Accruals hit hardest when income can't grow to match them, and hardship status pauses collection without pausing interest. The trade-offs for fixed-income taxpayers are covered in retired and owe back taxes.

State back taxes

States set their own interest rates on their own schedules — never assume the IRS's 7% applies. California's FTB, notably, can collect for 20 years under R&TC §19255, twice the federal window, so a state balance left compounding is a longer-term problem than its IRS twin.

When you can handle this yourself

Most people with one year of back taxes and a balance they can pay within 180 days need no professional help at all. If you owe under $25,000, agree with the number, and can commit to a monthly payment, setting up a streamlined plan online and requesting first-time abatement yourself is a 30-minute project — and nothing in the interest math changes because a firm did the clicking.

Experienced help changes outcomes in the harder fact patterns: a lien filed or imminent while a refinance is in motion, multiple years with unfiled returns (the resolution order changes total cost), a possible Section 6404 interest-abatement claim that needs the IRS's own delay documented from transcripts, business or payroll balances where personal liability is in play, or OIC math where a weak offer costs two years of accruals with nothing to show for it. The honest test: if the interest is the whole problem, you can likely fix it yourself; if the interest is a symptom of a bigger collection problem, get a second set of eyes first.

Terms on your notice, decoded

- Federal short-term rate — a Treasury borrowing rate the IRS uses as the base of its interest formula; your rate is this plus 3 points.

- Underpayment rate — the official name for the interest rate charged on unpaid tax under IRC §6621.

- Compounded daily — interest is added to your balance every day (IRC §6622), so each day's charge is computed on a slightly bigger number.

- Failure-to-pay penalty — a separate monthly charge of 0.5% of the unpaid tax, capped at 25%; not interest, but it accrues interest.

- Statutory additions — the notice's collective term for penalties and interest stacked on top of the tax itself.

- CSED — the Collection Statute Expiration Date: 10 years from assessment, after which the debt (and all its accrued interest) generally expires, though certain events pause the clock.

If a payoff figure has to be locked down before an underwriting deadline, a free review with an experienced tax professional at (888) 825-7779 can map the fastest route to a zero balance — or a lien-free path to closing.

IRS interest questions, answered

What is the IRS interest rate on back taxes in 2026?

For individuals, the rate is the federal short-term rate plus 3 percentage points — 7% per year as of the most recent quarterly announcement — compounded daily. The IRS resets the rate every quarter, so always confirm the current figure on IRS.gov or in your online account before running payoff math. The same formula has produced rates between 3% and 8% over the past decade.

Does IRS interest compound daily?

Yes. Under Internal Revenue Code Section 6622, IRS interest compounds daily, not monthly or annually. At a 7% stated rate, daily compounding works out to an effective annual cost of roughly 7.25%. Each day's interest is added to the balance, and the next day's interest is calculated on that slightly larger number — which is why old balances grow faster than most people expect.

Can the IRS interest rate be negotiated or waived?

No — the rate is set by statute, and the IRS has no authority to negotiate it or waive interest for reasonable cause. The narrow exception is Section 6404 abatement, which removes interest caused by an IRS error or unreasonable delay, requested on Form 843. The practical workaround is penalty abatement: when a penalty is removed, the interest charged on that penalty is removed with it.

Does interest stop while I'm on an IRS payment plan?

No. Interest continues to compound daily on the unpaid balance for the life of any installment agreement. What changes is the failure-to-pay penalty, which drops from 0.5% to 0.25% per month while an approved agreement is in effect. That cuts the combined annual carrying cost from roughly 13% to roughly 10%, which is why paying a plan off early saves real money.

Is the IRS interest rate different for businesses?

Mostly no — corporations pay the same short-term-rate-plus-3% on underpayments. The exception is 'hot interest': large corporate underpayments over $100,000 accrue at 2 percentage points higher once the IRS demands payment. Corporate refunds also earn less than individual refunds. If your business entity owes, the bigger variable is usually who is liable, not the rate.

Does the IRS charge interest on penalties too?

Yes. Interest accrues on failure-to-file and accuracy-related penalties from the date the return was due, and on most other penalties from the date the IRS assesses them. This stacking is why a balance can grow far past the tax itself. It is also why penalty abatement helps twice: the penalty comes off, and so does every dollar of interest that accrued on it.

Does interest keep accruing during an Offer in Compromise or appeal?

Yes. Interest continues to accrue on the full balance while an Offer in Compromise is under review and while an audit or appeal is pending. If the offer is accepted, the accepted amount resolves the entire liability — tax, penalties, and accrued interest. If it is rejected, you owe the original balance plus everything that accrued during review, so weak offers carry a real cost.

Does the IRS pay interest on refunds at the same rate?

For individuals, yes — the overpayment rate uses the same short-term-rate-plus-3% formula, and the IRS generally owes you interest if a refund takes more than 45 days after the filing deadline or your filing date. Two catches: refund interest is taxable income in the year you receive it, and a refund claim for an old year dies entirely three years after the return's due date.

Does interest count toward the $66,000 passport threshold?

Yes. The 2026 passport-certification threshold of $66,000 measures your total assessed debt — tax, penalties, and interest combined. A $50,000 tax debt left alone can cross the line on accruals alone within a few years. Once the IRS certifies the debt as seriously delinquent, the State Department can deny a passport application or renewal until you get into a qualifying arrangement.

Your next 24 hours

- Pull the real number. Log into your IRS online account and note the current payoff balance for each year — that figure, not last year's notice, is what's compounding daily.

- Gather three things: your last filed return, any IRS notices you've received, and a snapshot of monthly income and expenses — everything a plan, abatement request, or payoff decision needs.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form — at roughly $212 a month of growth on a $19,700 balance, and a lien filing capable of stalling a refinance, the cheapest version of this problem is the one you address today.

Whether IRS interest can ever come off — and the difference between the myths and the two real paths — is covered in depth in can IRS interest be waived. And for the government's own numbers, the current quarter's rate is always posted on the IRS's quarterly interest rates page; if an IRS delay inflated your interest and you can't get traction, the Taxpayer Advocate Service exists for exactly that.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.