IRS Penalties

Accuracy-Related Penalty (IRS): What the 20% Penalty Means and How to Fight It in 2026

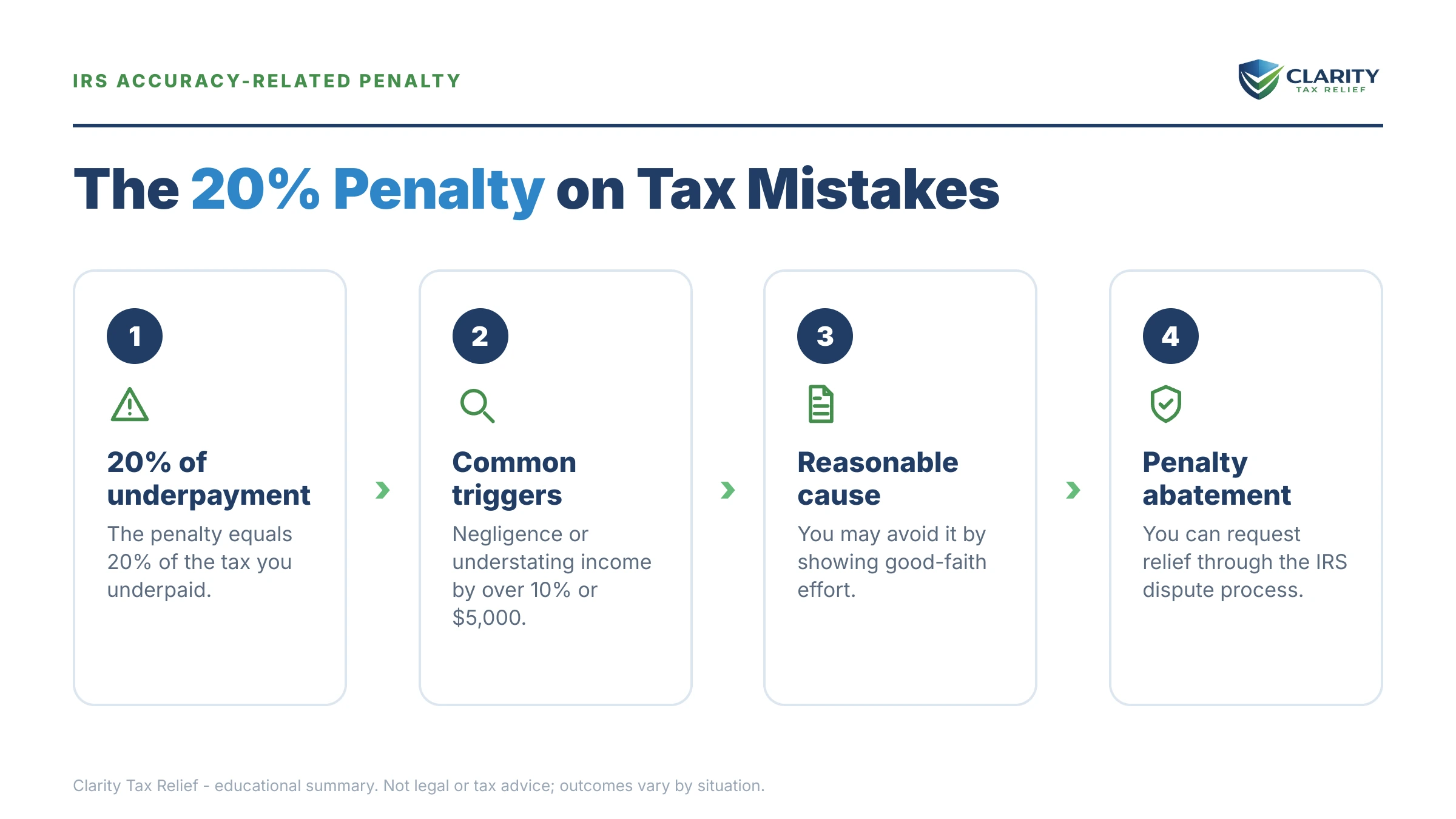

The short answer: the IRS accuracy-related penalty is 20% of the tax you underpaid, charged under IRC §6662 for negligence or a "substantial understatement" — an understatement over $5,000 or 10% of your correct tax. It can be removed by proving reasonable cause, but first-time abatement does not apply to it.

You're retired, your income is mostly Social Security plus a few 1099s, and an IRS letter just proposed thousands in extra tax — then added a separate line labeled "accuracy-related penalty" that tacks 20% on top of whatever the tax turns out to be. That penalty line feels like an accusation of dishonesty. It isn't one — and it's far from final.

The accuracy-related penalty is one of the most contestable charges the IRS makes, because it's a percentage of a number that is itself often wrong. Fight the underlying tax successfully and the penalty shrinks or disappears with it. If you're not sure which line on your letter is the penalty, the image below shows what it looks like on the page and where to find the figure that drives it.

⏱ Your deadline: the response date printed on the notice proposing the penalty — typically 30 days on a CP2000 or audit report, and exactly 90 days from the date on a CP3219A (150 days if the notice is addressed to you outside the United States) — a deadline the IRS cannot extend. Respond inside that window and you can contest the penalty before it is ever assessed, without paying a dollar first.

Why the IRS charged you an accuracy-related penalty

The accuracy-related penalty under IRC §6662 adds 20% to the portion of tax you underpaid because of negligence or a substantial understatement of income tax. It is not a late-filing or late-payment charge — it targets what was on the return, not when you filed or paid it.

For individuals, two triggers do almost all the work. Negligence or disregard of rules means the IRS believes you didn't make a reasonable attempt to report correctly — ignored 1099s, deductions with no records, positions with no plausible basis. Substantial understatement is pure arithmetic: the tax you reported was short by more than the greater of $5,000 or 10% of the correct tax. No carelessness required — the math alone can trigger it.

How the penalty reached you matters. Most people first see it as a proposed line on a CP2000 notice, where the IRS's automated underreporter system matched your return against 1099s and W-2s and calculated the penalty by computer. The rest see it on an exam report after an audit, where a human examiner asserted it — and for most examiner-asserted penalties, the law requires written supervisory approval, a technical requirement that occasionally becomes a defense.

Here is every version of the penalty and what triggers each rate:

| Trigger | Rate | Threshold / standard |

|---|---|---|

| Negligence or disregard of rules | 20% | No dollar threshold — failure to make a reasonable attempt to comply (missing records, ignored income documents) |

| Substantial understatement of income tax | 20% | Understatement exceeds the greater of $5,000 or 10% of the correct tax (individuals) |

| Substantial valuation misstatement | 20% | Value or basis claimed at 150% or more of the correct figure |

| Gross valuation misstatement | 40% | Value or basis claimed at 200% or more of the correct figure |

| Undisclosed foreign financial asset understatement | 40% | Understatement tied to assets that should have been reported (Form 8938 and related filings) |

Two boundaries keep this penalty in perspective. It is not the fraud penalty — the civil fraud penalty is 75% and requires proof of intent, and the IRS cannot charge both on the same portion of an underpayment. And if your case involves offshore accounts, the 40% prong overlaps with a separate set of exposures covered in our guide to an undisclosed foreign account IRS problem. For how this penalty compares to every other charge the IRS stacks on back taxes, see how much are IRS penalties on back taxes.

How much is the accuracy-related penalty? A worked example

The accuracy-related penalty is always 20% (or 40%) of the underpayment — so the fastest way to cut the penalty is to cut the underpayment it's calculated on. A hypothetical shows why that matters so much.

Say you're retired, living on Social Security and an inherited brokerage account. Two years ago you sold the inherited stock. The broker's 1099-B reported the gross proceeds but no cost basis, so the IRS's matching system treated the entire sale as taxable gain and mailed you a CP2000 proposing $61,200 in additional tax.

The penalty math on that proposal:

- Proposed additional tax: $61,200

- Substantial understatement test: $61,200 exceeds both $5,000 and 10% of the correct tax — the penalty applies automatically

- Accuracy-related penalty: 20% × $61,200 = $12,240

- Plus interest on the tax and the penalty, running from the return's original due date

Now the fix. Inherited assets get a stepped-up basis to date-of-death value. Say you document that basis and the true gain produces only $4,800 of additional tax. The underpayment drops from $61,200 to $4,800 — and because $4,800 is under the $5,000 threshold, the substantial-understatement prong fails entirely. A good-faith basis error on inherited stock, backed by records, is also a weak negligence case. One well-documented response can turn a $12,240 penalty into $0, and roughly $73,000 of proposed debt into under $5,000.

To see how penalties and interest compound on your own numbers before you respond, you can estimate the total with our Penalty & Interest Calculator.

What happens if you ignore the penalty notice

An ignored accuracy-related penalty stops being a proposal and becomes an assessed debt that enters the IRS collection machine. The sequence is automated, and each stage removes an option you have today:

- The response window closes. The date on your CP2000 or exam report passes with no reply, and the IRS treats its proposed figures — tax plus 20% penalty — as unchallenged. If you disagree with the underlying numbers, the CP2000 disagree playbook works only inside this window.

- Notice of Deficiency. The IRS mails a CP3219A notice of deficiency — your last chance to contest the tax and penalty in Tax Court, within 90 days, without paying first.

- Assessment. The 90 days pass, and the tax, the penalty, and interest all post to your account as legally owed. Interest on the penalty is backdated to the return's original due date, so the balance is already larger than the notice suggested.

- The collection sequence begins. A CP14 bill arrives, followed by reminder notices, then a CP504 (the IRS can seize your state refund), then an LT11 final notice — after which, 30 days later, wage garnishment and bank levies become legal. If Social Security is your income, up to 15% of it can be levied through the Federal Payment Levy Program.

In 2026 there's a practical wrinkle: IRS staffing is down roughly 27%, which makes disputing a penalty by phone slower than ever — but the automated systems that assess penalties and issue levies never slowed down. Delay costs you options; it never costs the IRS anything.

Staring at a proposed 20% penalty right now?

Send us the notice before the response date printed on it passes. An experienced tax professional will check whether the underlying tax is even right, whether the penalty legally applies, and what your strongest removal argument is — free, confidential, no pressure.

How to get the IRS accuracy-related penalty removed: your options

Every path to removing the accuracy-related penalty runs through one of two arguments: the underlying tax is wrong, or you acted with reasonable cause and good faith. Which procedure you use depends on where you are in the timeline — and one popular shortcut is off the table. First-time abatement does not apply to the accuracy-related penalty. The first time penalty abatement waiver — and the Automatic Exemption from Penalty (AEP) replacing it starting summer 2026 — covers late-filing, late-payment, and deposit penalties, not §6662. A spotless compliance history helps your credibility, but it isn't a ticket by itself.

| Option | Who it fits | IRS cost | Typical timeline |

|---|---|---|---|

| Respond to the CP2000 / exam report | Penalty is still proposed, not assessed — the strongest position | $0 | Weeks to a few months for the IRS to process |

| Appeals conference | You responded, the examiner disagreed, and appeal rights were offered | $0 | Several months; collection generally waits |

| Tax Court petition | You received a Notice of Deficiency within the last 90 days | $60 filing fee | Many cases settle with Appeals before trial |

| Reasonable-cause abatement request | Penalty already assessed; honest mistake with a documented good-faith story | $0 | Varies; written requests often take months |

| Audit reconsideration | Assessed after an exam you didn't (or couldn't) respond to, and you have new information | $0 | Months; enforcement can sometimes be paused meanwhile |

| Pay, then Form 843 refund claim | Abatement denied or window missed; you can pay and reclaim | $0 to file | Months; preserves the right to sue for a refund |

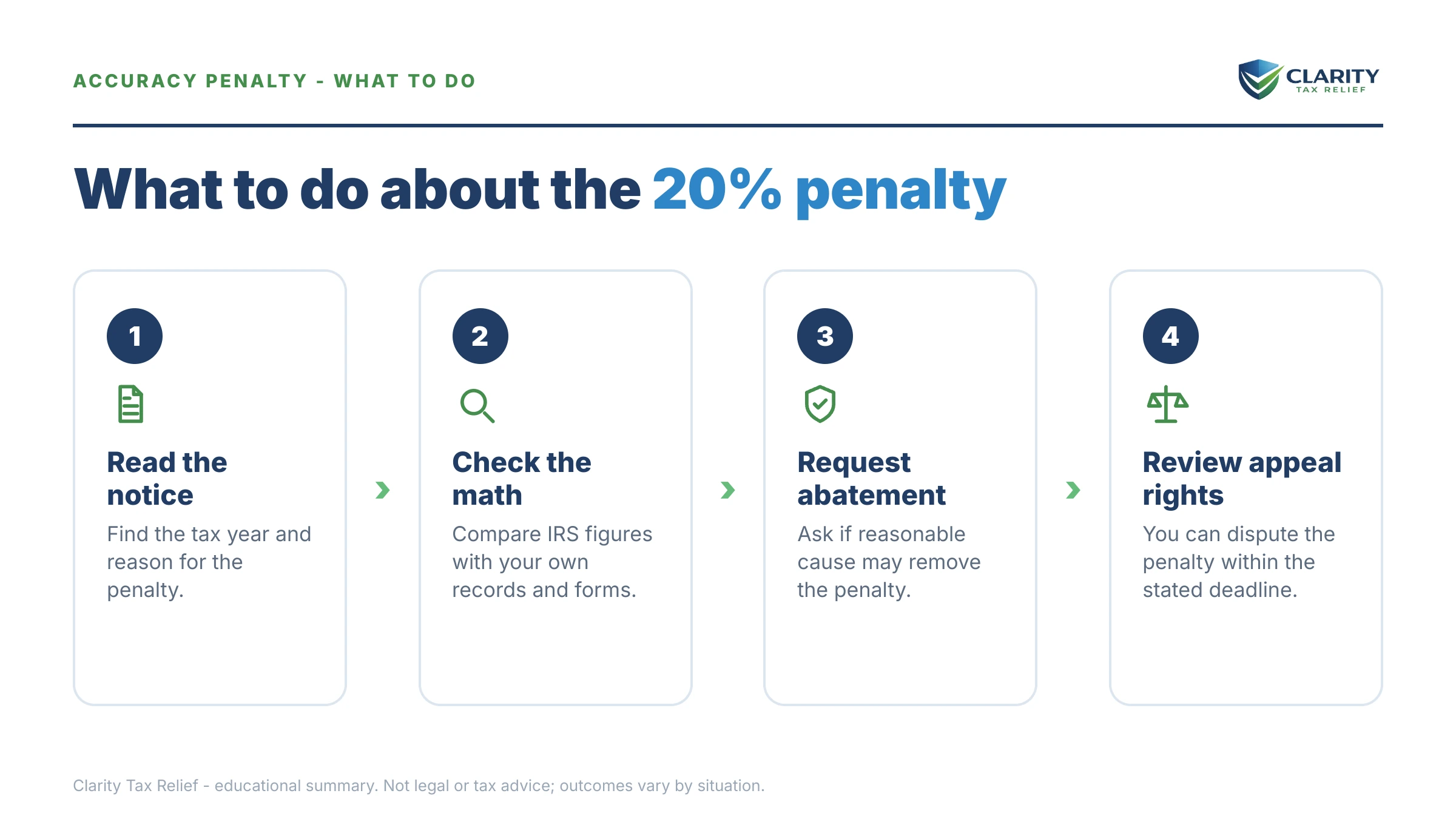

Before assessment is where cases are won. Answer the CP2000 or exam report with documents that correct the underlying tax, and contest the penalty in the same letter — both on the math (does the understatement still clear the $5,000/10% bar after your corrections?) and on the conduct (reasonable cause). If the examiner won't budge, take the free Appeals conference before the deficiency notice issues.

After assessment, the tools shift. A written reasonable cause penalty abatement request is the workhorse — it must tell a specific, documented story: you relied on a professional you fully informed, you reasonably didn't know an inherited asset's basis rules, a serious illness disrupted your recordkeeping. A well-built IRS penalty abatement letter leads with facts and proof, not apologies. If the exam happened without you — you moved, were hospitalized, never got the mail — audit reconsideration can reopen the whole adjustment, penalty included. And if abatement is denied, paying and filing a refund claim keeps the fight alive; our Form 843 instructions walk through that route.

One more defense worth knowing: for return positions with real legal support, "substantial authority" defeats the substantial-understatement prong, and a position disclosed on Form 8275 with a reasonable basis is protected from it too. These are mostly planning tools, but if your preparer took a defensible position, they belong in your response.

If some balance survives, resolve it before collection escalates — payment plans start at IRS.gov/payments, and if you're on a fixed income where any payment would be a genuine hardship, read our guide to IRS hardship social security status before agreeing to a payment you can't sustain.

How to respond to an accuracy-related penalty, step by step

- Find the response deadline. The date printed near the top of your CP2000, exam report, or Notice of Deficiency controls whether you can still contest the penalty before it is assessed — calendar it today.

- Verify the underlying adjustment. Pull the return for that year plus the records behind the disputed item — basis statements, 1099s, closing documents — and check whether the IRS's proposed tax is actually right.

- Dispute the tax and the penalty together. Every dollar you knock off the proposed tax removes 20 cents of penalty automatically, so send corrections and documentation for the adjustment in the same response that contests the penalty.

- Make a written reasonable-cause case. In the same response, explain the specific facts showing good faith — what records you kept, what advice you relied on, why the error was honest — and attach proof.

- Resolve whatever balance survives. If tax or penalty remains after your dispute, set up a payment arrangement or hardship status before the balance enters the collection notice sequence.

When you can handle this yourself — and when help changes the outcome

You can usually handle an accuracy-related penalty alone when the fix is documentary and the dollars are small. A CP2000 that missed one 1099 you agree with, a basis figure you can prove with a single brokerage statement, a proposed penalty of a few hundred dollars — those are letter-and-enclosures problems. Write clearly, attach the proof, mail it certified, keep copies. The Taxpayer Advocate Service can also help free of charge if the IRS mishandles your response or a delay is causing hardship.

Experienced help changes outcomes in four situations. First, a Notice of Deficiency has already been issued — the 90-day Tax Court clock is unforgiving, and a missed petition converts a contestable proposal into assessed debt. Second, the proposed penalty is large (five figures), because the reasonable-cause narrative has to be built to the IRS's own standards, not just told sincerely. Third, multiple years or multiple issues are in play, where the order you resolve things changes the total. Fourth, the exam report uses fraud language or a 40% rate — that's a different weight class entirely. An honest rule of thumb: if losing the argument costs more than a year of your discretionary income, get a professional review before you respond, not after.

Terms on your notice, decoded

- Underpayment — the difference between the tax you should have paid and what your return showed; the penalty is always a percentage of this number.

- Negligence — failing to make a reasonable attempt to follow the tax rules or keep adequate records; carelessness, not dishonesty.

- Substantial understatement — an understatement exceeding the greater of $5,000 or 10% of the correct tax for an individual; triggers the 20% penalty on math alone.

- Reasonable cause and good faith — the §6664(c) defense: you made an honest, documented effort to report correctly, so the penalty shouldn't apply.

- Substantial authority / adequate disclosure — legal support for a return position, or disclosure of it on Form 8275, either of which can defeat the substantial-understatement prong.

- Supervisory approval — the §6751(b) requirement that a manager approve most examiner-asserted penalties in writing; computer-calculated CP2000 penalties are treated as exempt, but exam penalties without approval can sometimes be invalidated.

The IRS's own summary of the penalty, its triggers, and its relief standards is at IRS.gov: Accuracy-related penalty.

Accuracy-related penalty questions, answered

Can the IRS accuracy-related penalty be removed?

Yes — but not automatically. The main path is showing reasonable cause and good faith under IRC §6664(c): you made an honest effort to report correctly, and the error came from something like missing basis records, a preparer's mistake, or genuinely confusing rules. You can also eliminate the penalty by reducing the underlying tax, since the penalty is always 20% of the underpayment — shrink the underpayment and the penalty shrinks with it.

Does first-time penalty abatement apply to the accuracy-related penalty?

No. First-time abatement covers only the failure-to-file, failure-to-pay, and failure-to-deposit penalties — a clean three-year compliance history does nothing against a §6662 penalty. The Automatic Exemption from Penalty (AEP) replacing FTA in summer 2026 is aimed at those same late-filing and late-payment penalties. For the accuracy-related penalty, your realistic paths are disputing the underlying tax or proving reasonable cause.

What counts as a substantial understatement of income tax?

For an individual, an understatement is 'substantial' when it exceeds the greater of $5,000 or 10% of the tax that should have been shown on the return. If your correct tax was $30,000 and your return showed $22,000, the $8,000 gap tops both $5,000 and $3,000 (10%), so the 20% penalty can apply. Most corporations are measured against a different threshold, and adequate disclosure or substantial authority can reduce the understatement.

Is the accuracy-related penalty the same as the fraud penalty?

No — and the difference is enormous. The accuracy-related penalty is a 20% civil charge for negligence or a substantial understatement; the civil fraud penalty is 75% and requires the IRS to prove intentional wrongdoing with clear and convincing evidence. The IRS cannot stack both penalties on the same portion of an underpayment. If your exam report mentions fraud, treat it as a different category of problem and get experienced help before responding.

When is the accuracy-related penalty 40% instead of 20%?

The rate doubles to 40% in three situations: a gross valuation misstatement (claiming a value or basis at 200% or more of the correct figure), an understatement tied to an undisclosed foreign financial asset, and certain transactions that lack economic substance. Most individual taxpayers who see this penalty face the standard 20% version triggered by a CP2000 match or an audit adjustment.

Do I have to pay the accuracy-related penalty before I can dispute it?

Not if you act before assessment. Responding to the CP2000 or exam report, going to Appeals, or petitioning Tax Court within 90 days of a Notice of Deficiency all let you contest the penalty without paying first. Once it is assessed, you can still request abatement — and if that is denied, pay the penalty and file Form 843 to claim a refund. Pre-assessment is the cheaper, stronger position.

Does relying on my tax preparer count as reasonable cause?

It can — if you gave the preparer complete and accurate information and reasonably relied on their professional judgment. Handing a qualified preparer all of your 1099s and following their advice on a genuinely debatable issue is a classic reasonable-cause fact pattern. It does not work if you withheld documents, ignored obvious red flags on the finished return, or used a preparer who promised outsized refunds.

Does interest accrue on the accuracy-related penalty?

Yes, and it accrues from further back than most people expect. Interest on the accuracy-related penalty generally runs from the due date of the return for the year at issue — not from the date the penalty was assessed — so by the time a CP2000 arrives a year or more later, meaningful interest has already stacked up. Removing the penalty removes the interest charged on it; the IRS almost never waives interest on its own.

Your next 24 hours

- Find two things on your notice: the line labeled "accuracy-related penalty" (note the amount) and the response date printed near the top — that date decides whether you can still fight this before it's assessed.

- Gather your proof: the notice itself, your tax return for that year, and the records behind the disputed item — basis or inheritance documents, 1099s, and any correspondence with your preparer.

- Get a free case review before your response window closes: call (888) 825-7779 or use the 2-minute form at claritytaxrelief.com/#consult. We'll tell you whether the underlying tax is even correct, whether the penalty legally applies, and which removal path fits your facts.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.